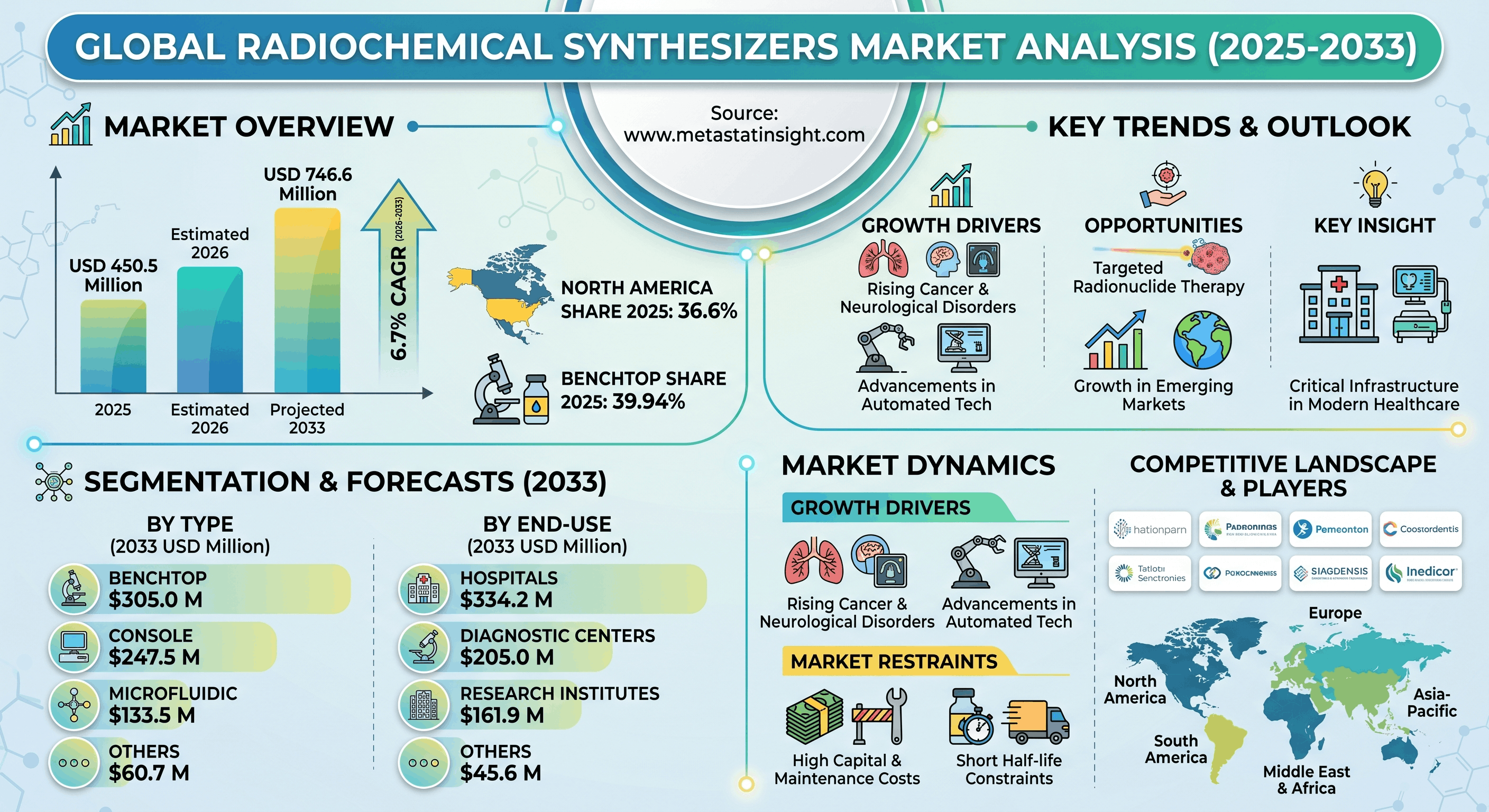

The global Radiochemical Synthesizers Market, valued at USD 450.5 million in 2025, is on a steady growth trajectory. According to a new market analysis by Metastat Insight, the industry is projected to grow at a compound annual growth rate (CAGR) of 6.7%, reaching USD 746.6 million by 2033.

As global healthcare transitions toward personalized medicine, radiochemical synthesizers are emerging as critical infrastructure. These advanced platforms are crucial for producing the targeted radiopharmaceuticals and molecular tracers used in precision diagnostic imaging modalities, specifically Positron Emission Tomography (PET) and Single Photon Emission Computed Tomography (SPECT).

Core Dynamics Driving Growth

The escalating global incidence of cancer, cardiovascular conditions, and neurological disorders is a major driver pushing healthcare facilities to expand their diagnostic capabilities. This growing reliance on precision diagnostics has created a clear industry shift toward automated synthesis technologies. Automated systems improve batch consistency, maximize laboratory efficiency, and significantly enhance safety by minimizing human exposure to radioactive substances.

However, the market faces unique operational hurdles. High upfront capital investment and ongoing maintenance costs limit equipment adoption in smaller medical facilities. Furthermore, the short half-life of radioisotopes imposes strict operational constraints, requiring highly synchronized supply chains to prevent material waste.

Key Segmentation Highlights

-

By Configuration:Benchtop Synthesizers represent the leading layout, capturing a 39.94% market share in 2025. This segment is valued at USD 189.9 million in 2026 and is forecast to reach USD 305.0 million by 2033 due to its spatial efficiency. High-capacity Console Synthesizers and precision Microfluidic Synthesizers follow as key alternative pathways.

-

By Modality:PET applications lead the segment and are projected to reach USD 375.0 million by 2033, while SPECT applications are estimated to reach USD 270.1 million.

-

By Product Type: Driven by the need for clinical safety, Fully Automated Synthesizers are poised for the fastest expansion, growing at a 7.2% CAGR.

-

By End-Use:Hospitals remain the leading segment, with expenditures expected to hit USD 334.2 million by 2033, followed by Diagnostic Centers and Research Institutes.

Regional Outlook

North America dominated the global landscape with a 36.6% market share in 2025, led by high scanning rates and major player presence in the United States. Europe maintains a strong position through established clinical networks, while the Asia-Pacific region is emerging as a high-growth territory fueled by rising investments in healthcare infrastructure.