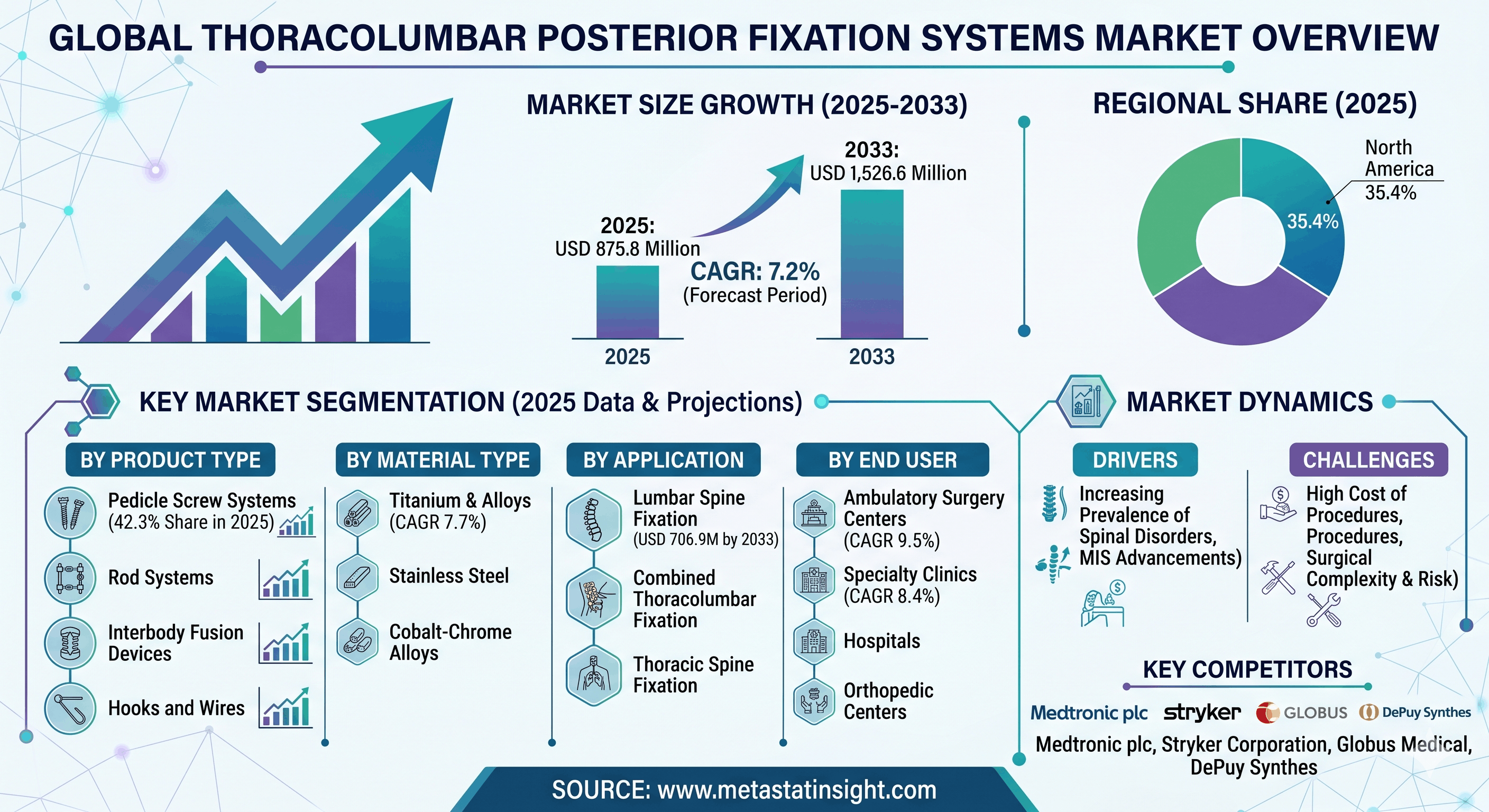

The global clinical landscape for spine care is experiencing a profound paradigm shift. According to an extensive data-driven industry analysis published by MetaStat Insight, the global Thoracolumbar Posterior Fixation Systems Market was valued at USD 875.8 million in 2025 and is mathematically projected to expand at a steady Compound Annual Growth Rate (CAGR) of 7.2%, culminating in a market valuation of USD 1,526.6 million by 2033.

This comprehensive strategic outlook highlights that the accelerating demand for surgical interventions is primarily propelled by a combination of aging global populations and the rising complexity of debilitating spinal conditions. Thoracolumbar posterior fixation systems serve as a foundational anchor in modern spine care, facilitating vital posterior surgical procedures to stabilize the thoracic and lumbar spine following instances of spinal deformities, acute trauma, advanced degeneration, or localized tumor-related damage. By securing targeted vertebral segments, these systems play an indispensable role in restoring structural spinal alignment, fostering reliable bone fusion, and mitigating chronic pain for patients worldwide.

Key Market Performance & Strategic Segment Insights

-

Dominant Regional Footprint: North America positioned itself at the forefront of the global landscape, securing a commanding 35.4% of the total market share in 2025, with the United States operating as the primary engine of regional commercial progress.

-

The Crucial Role of Pedicle Screw Systems: Reflecting strong surgeon preferences, the Pedicle Screw Systems segment alone captured 42.3% of the market share in 2025. Evaluated at USD 396.7 million in 2026, this vital product category is anticipated to climb to USD 665.9 million by 2033 at an accelerated CAGR of 7.7%, fueled by its superior capability to improve spinal stability, optimize mechanical load distribution, and integrate with advanced navigation-assisted surgical placement tools.

-

Evolution of Construct Materials: Material innovation continues to dictate purchasing trends across healthcare networks. The Titanium and Titanium Alloys segment is set to reach USD 1,115.6 million by 2033, growing at a 7.7% CAGR, due to its exceptional mechanical strength, advanced biocompatible coatings, and structural imaging compatibility. Concurrently, Stainless Steel remains highly relevant in cost-conscious markets, projected to reach USD 211.4 million by 2033, while Cobalt-Chrome Alloys are steadily finding a niche in high-load, complex deformity reconstructions, tracking toward USD 199.5 million by the end of the forecast period.

-

Surgical Site Applications: Driven by an immense clinical burden of lower back conditions, Lumbar Spine Fixation represents a prominent high-demand application, projected to capture USD 706.9 million by 2033. Combined Thoracolumbar Fixation for complex multi-level instabilities is forecast to attain USD 486.2 million, while Thoracic Spine Fixation pathways are expected to reach USD 333.4 million.

-

Evolving End-User Dynamics: While traditional Hospitals maintain dominance in overall purchasing volume due to intensive postoperative resources (projected to grow at a 6.3% CAGR), Ambulatory Surgery Centers (ASCs) are emerging as the fastest-growing segment. Outpatient adoption is driving ASCs at a striking 9.5% CAGR, followed closely by Specialty Clinics at 8.4% and specialized Orthopedic and Neurosurgery Centers at 7.3%.

Catalysts, Financial Restraints, and Future Frontiers

The research study published on MetaStat Insight outlines a clear dichotomy between operational drivers and market bottlenecks. The market is enjoying robust upward momentum due to the expanding capacity of hospitals to treat trauma stemming from vehicle accidents, workplace injuries, and sports-related damages. Simultaneously, rapid innovations in modular hardware, fatigue-resistant metals, and image-guided diagnostic systems are substantially enhancing clinical safety margins.

However, the industry faces prominent economic and clinical headwinds. The premium costs associated with advanced implants, complex imaging software, operating room utilization, and specialized physician fees continue to place noticeable financial stress on healthcare systems, particularly within developing or budget-limited economies. Furthermore, the technical complexity of these surgeries carries inherent risks including implant loosening, nerve injuries, postoperative infections, and adjacent segment stress underscoring a critical industry-wide reliance on the deployment of surgical robotics and specialized training programs to streamline workflows.

Strategic Competitive Landscapes

The commercial environment remains highly fragmented and dynamic, accommodating distinct layers of market participants. Tier-1 enterprise leaders continue to leverage deep consumer trust, comprehensive product catalogs, and expansive international distribution networks. Concurrently, mid-sized competitors are successfully securing consistent business by prioritizing direct surgeon collaboration, agile engineering cycles, and enhanced operating room efficiency. The ecosystem is further diversified by highly specialized manufacturers engineering custom, case-specific hardware, alongside emerging regional participants introducing cost-efficient alternative portfolios that intensify pricing competition globally.

About MetaStat Insight

MetaStat Insight is a premier market research and consulting firm dedicated to delivering high-fidelity, data-driven market analysis and strategic intelligence. Operating with a historical study period spanning 2021–2025 and an active forecast window stretching through 2026–2033, MetaStat Insight provides granular, multi-segment reporting across diverse geographies, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.