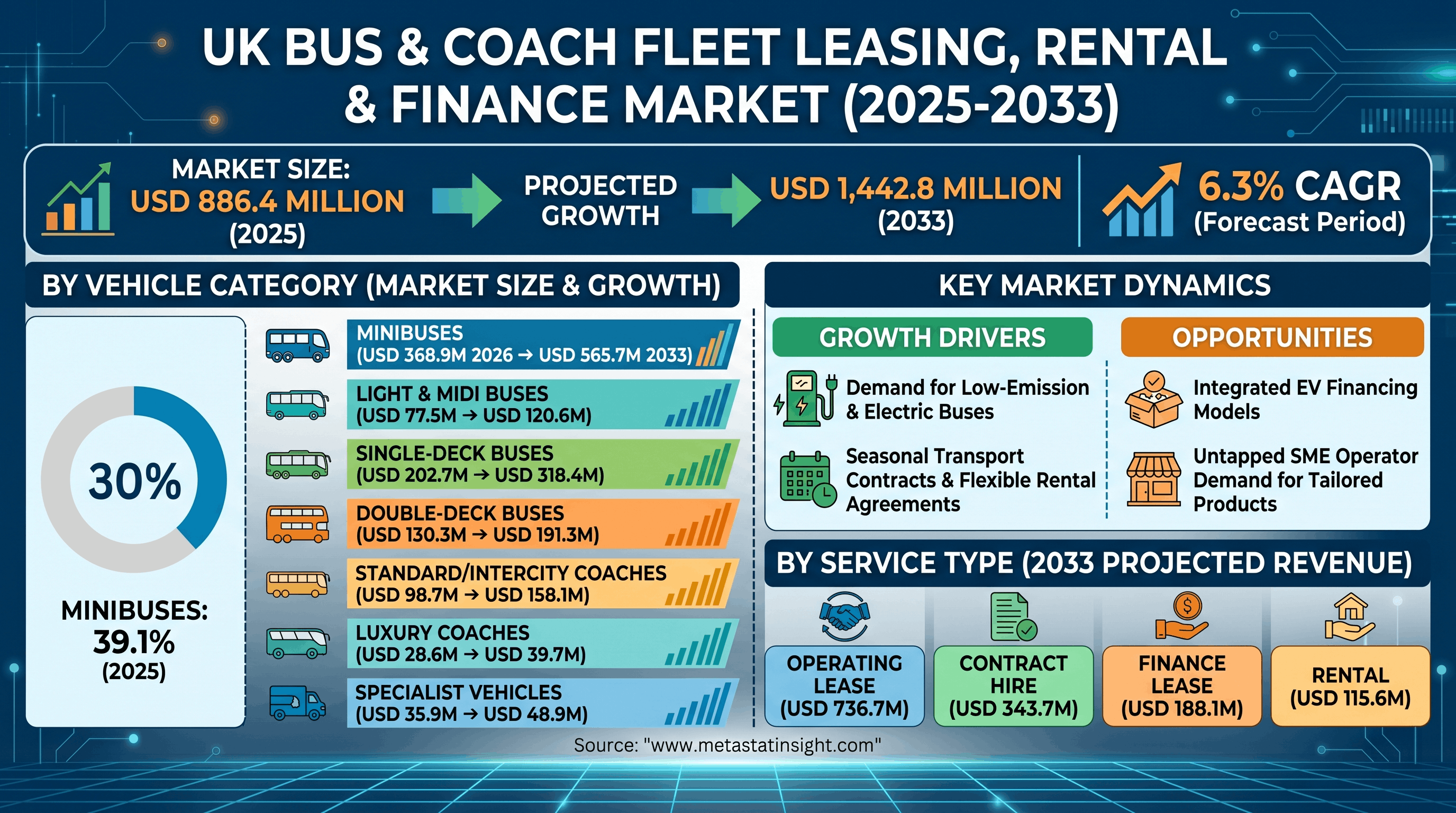

The UK Bus & Coach Fleet Leasing, Rental, and Finance Market is undergoing a major structural transformation as operators increasingly pivot from outright vehicle ownership to structured asset-light financing. According to the latest comprehensive data-driven analysis by MetaStat Insight, the market is valued at USD 886.4 million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 6.3%, ultimately reaching USD 1,442.8 million by 2033.

This steady upward trajectory highlights a crucial shifts in the passenger transport financing ecosystem. Escalating vehicle acquisition costs, combined with the pressing need to modernize transport networks, are driving UK fleet operators to prioritize capital preservation, operational flexibility, and faster vehicle replacement cycles over heavy upfront capital expenditure.

Minibuses Lead Market Volumes; Single-Deck and Coach Sectors See High Growth Potential

The segmentation data reveals a diverse ecosystem catering to distinct transit requirements across the United Kingdom:

-

Minibuses: This segment dominates the landscape, commanding a substantial 39.1% market share in 2025. Evaluated at USD 368.9 million in 2026, it is forecast to touch USD 565.7 million by 2033 (6.3% CAGR), supported by robust demand for school transport, community transit, and airport feeder links.

-

Full-size Single-deck Buses: Critical for everyday scheduled municipal and suburban routes, this segment is valued at USD 202.7 million in 2026 and is expected to climb to USD 318.4 million by 2033 at a 6.7% CAGR.

-

Standard and Intercity Coaches: Driven by a recovery in regional tourism, event mobility, and long-distance commuting, this sector boasts the fastest growth at a 7% CAGR, rising from USD 98.7 million in 2026 to USD 158.1 million by 2033.

-

Other Segments: Double-deck buses (projected to reach USD 191.3 million by 2033), Light and Midi buses (targeting USD 120.6 million by 2033), and Luxury & Executive Coaches (poised to reach USD 39.7 million by 2033) continue to showcase steady demand, while specialist and accessible vehicles are expanding on the heels of evolving accessibility mandates.

The Shift Toward Flexible Operating Leases and All-Inclusive Contract Hires

On the service side, the industry is witnessing an accelerating preference for flexible, risk-mitigating agreements. The Operating Lease segment leads long-term expansion plans, projected to reach USD 736.7 million by 2033 (6.3% CAGR) as transport companies actively seek lower balance-sheet pressure and try to eliminate vehicle disposal risks.

Concurrently, Contract Hire agreements are scaling rapidly on track to hit USD 343.7 million by 2033 because they offer comprehensive, all-inclusive frameworks covering compliance support and maintenance bundles. Short-term Rental formats, accelerating at a strong 7.4% CAGR to reach USD 115.6 million by 2033, provide operators with crucial fleet elasticity to handle sudden seasonal peaks and emergency replacements. Meanwhile, Finance Leases remain a steady choice for well-established operators targeting gradual ownership control, projected to hit USD 188.1 million by 2033.

Strategic Drivers, Obstacles, and Future Market Opportunities

-

The Green Transition Accelerator: Rising clean transport targets, operators' sustainability initiatives, and stringent city emission zones are forcing rapid fleet renewals. Leasing and bundled finance structures lower the high initial capital barriers associated with electric vehicle (EV) deployment, allowing operators to secure both the vehicles and the charging infrastructure simultaneously.

-

Flexibility for Variable Demands: Fluctuating passenger volumes in school routes and private hire mean that flexible, short-term rental frameworks are essential for scaling operations seamlessly during peak demand.

-

Economic Bottlenecks: Growth is partially kept in check by tighter lending parameters and elevated interest rates, which raise repayment barriers for smaller regional entities. Furthermore, uncertainty surrounding the long-term residual value of older diesel assets prompts cautious underwriting strategies from lenders.

A Diversified and Hyper-Competitive Provider Base

The UK financing ecosystem is highly active, featuring a healthy balance of specialized asset management firms and large financial institutions. Major industry players include Asset Alliance Group, Dawsongroup Limited, Mistral Group, Close Brothers Group plc, and Siemens AG. The market is further supported by an extensive network of specialized finance providers, including Gable Asset Finance, Landmark Finance Limited, Kingsley Asset Finance, Universal Asset Finance Ltd, Coates Finance Limited, Asset Finance Arena, MAF Finance Group, First Oak Capital Limited, Simply Asset Finance Operations Limited, and Lincoln Finance Limited. This vast array of choices continues to foster intense competition, forcing advancements in approval speeds, digital underwriting tools, and contract transparency.

About MetaStat Insight

MetaStat Insight is a premier global market research and consulting firm dedicated to providing comprehensive, data-driven market analysis and strategic outlooks across varied industries. By delivering actionable insights, historical context, and accurate forecasts, MetaStat Insight empowers business leaders, lenders, and OEM specialists to make confident, long-term strategic decisions.