Autonomous Drone Market Size, Share, By Product (Fixed-Wing Drones, Rotary-Wing Drones, Hybrid Drones, and Solar-Powered Drones), By Range of Flight (Less than 10 KM, 10 KM - 20 KM, 20 KM - 30 KM, and More Than 30 KM), By Payload (Less Than 300 lbs, 300-400 lbs, 400-500 lbs, and More than 500 lbs), By Application (Commercial, Civilian, Military, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4579

Published

April 8, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

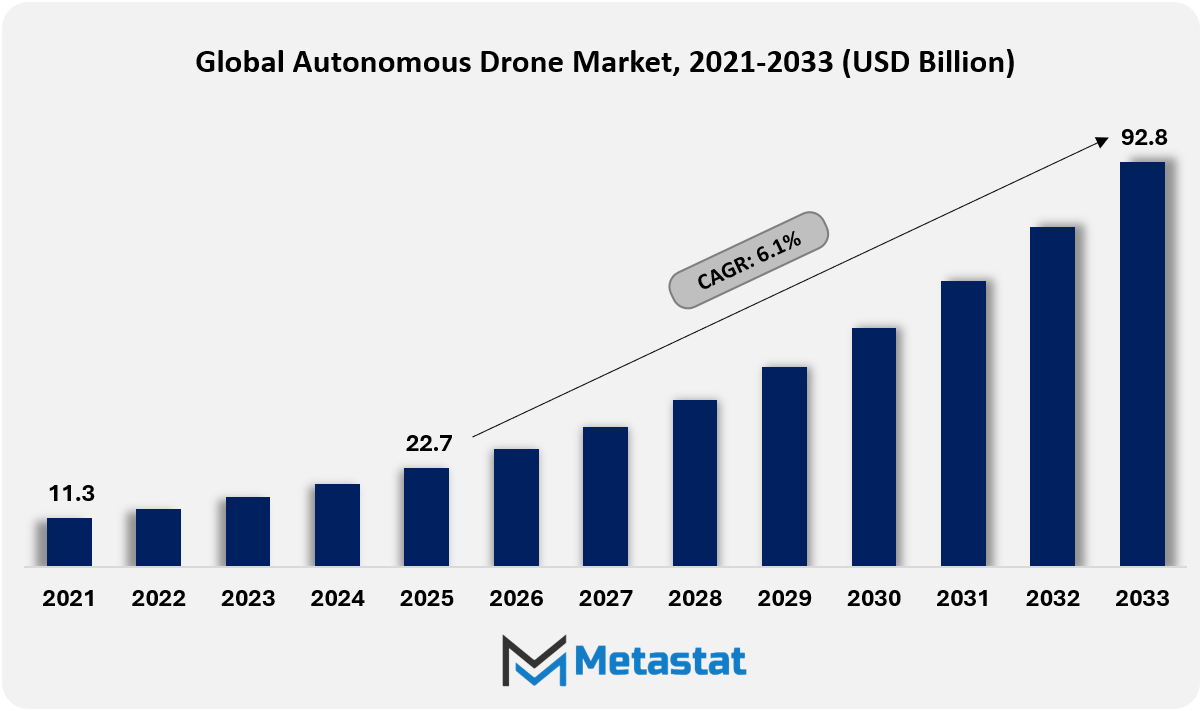

The Global Autonomous Drone market size was valued at USD 22.7 billion in 2025 and projected to grow at a CAGR of 19.3% during the forecast period, reaching USD 92.8 billion by 2033.

Global Autonomous Drone Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Autonomous Drone market valued at USD 22.7 billion in 2025, growing at a CAGR of 19.3% through 2033, with potential to exceed USD 92.8 billion.

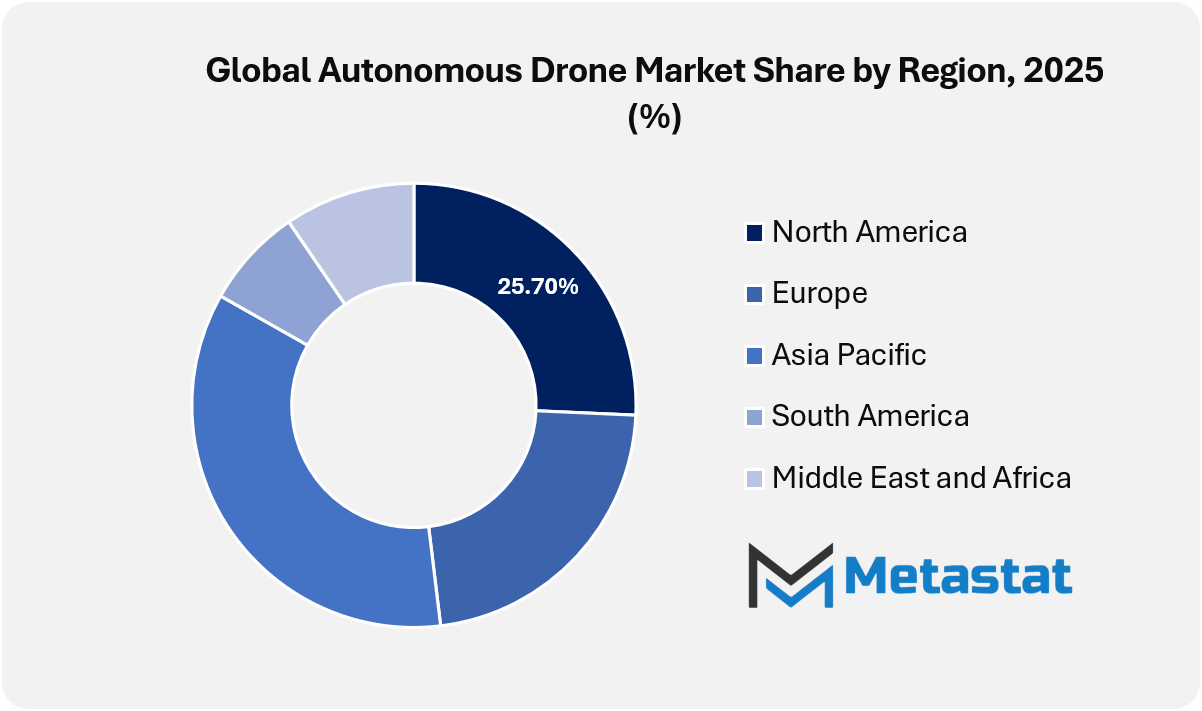

North America held a 25.7% share in 2025, led by the United States.

Key trends driving growth: Growing adoption of AI-enabled robotics to enhance inspection, surveillance, and operational efficiency across industrial sectors, and rising demand for automated aerial systems that reduce operational risk and lower labor-dependent field activities.

Opportunities include Expansion of fully automated drone-in-a-box ecosystems enabling continuous, remote, and scalable operations across industrial and commercial applications.

Key insight: Autonomous drones are transitioning from controlled defense applications toward scalable commercial use, supported by AI innovation yet moderated by regulatory and cost pressures.

The Global Autonomous Drone market will extend beyond conventional applications and will shape operating models that remain under-defined across current industry boundaries. Future trends will not remain limited to aerial mobility or automated navigation; autonomous drones will become embedded decision-making agents within digital and physical systems. These platforms will integrate directly with enterprise software, satellite intelligence, and ground-based robotics, forming closed operational loops that reduce human intervention across mission planning, execution, and post-mission evaluation.

Beyond visible use cases, autonomous drones will reshape how data ownership, accountability, and operational trust are defined. Flight systems will increasingly operate under algorithmic governance, where predictive behavior, self-correction, and adaptive risk assessment determine outcomes in real time. Regulatory frameworks will likely shift from prescriptive flight rules to performance-based oversight models that evaluate intent, reliability, and traceability.

Market Dynamics

Growth Drivers:

Growing adoption of AI-enabled robotics to enhance inspection, surveillance, and operational efficiency across industrial sectors.

Growing deployment of intelligent robotics across commercial environments continues to transform inspection and monitoring activities. The Global Autonomous Drone market gains momentum from advanced analytics, computer vision, and predictive processing, supporting faster decision-making, reduced downtime, and improved asset performance across energy, manufacturing, agriculture, and public safety operations.

Rising demand for automated aerial systems that reduce operational risk and lower labor-dependent field activities.

Increasing emphasis on workplace safety and cost control drives adoption of automated aerial solutions. Automated drone operations will update manual inspection duties in dangerous places, minimizing human publicity while retaining consistent information accuracy. Industrial operators will gain from decreased personnel dependency, stepped forward coverage, and higher operational continuity.

Restraints and Challenges:

Regulatory restrictions around BVLOS operations and airspace integration limiting large-scale deployment.

Regulatory frameworks governing beyond visual line of sight operations continue to slow large-scale adoption. Airspace coordination requirements, certification processes, and safety compliance standards will restrict rapid scaling. Delayed approvals and fragmented guidelines throughout regions will limit operational flexibility for business drone provider companies.

High upfront procurement and integration costs hindering adoption among cost-sensitive industries.

Initial funding necessities stay a prime barrier for small and mid-sized firms. Advanced hardware, software program integration, and training prices will project finances-sensitive sectors. Return on investment timelines often extend with maintenance costs and system customization needs, slowing purchasing decisions across competitive industries.

Opportunities:

Expansion of fully automated drone-in-a-box ecosystems enabling continuous, remote, and scalable operations across industrial and commercial applications.

Drone-in-a-box systems offer strong growth potential through unattended, round-the-clock operations. Integrated charging, data transmission, and independent flight management will guide scalable deployment throughout infrastructure monitoring, logistics, and protection services. Remote command capabilities will enable centralized control models with improved efficiency and reliability.

Market Segmentation Analysis

The Global Autonomous Drone market is classified based on Product, Range of Flight, Payload, and Application.

By Product, the market is further segmented into:

Fixed-Wing Drones

Fixed-Wing Drones segment is estimated at USD 7.5 billion in 2026 and is projected to reach USD 20.3 billion by 2033, at a CAGR of 15.3% during the forecast period.

Fixed-wing drones will gain relevance through long-duration missions requiring stable flight and energy efficiency. Advances in autonomous navigation, lightweight materials, and precision sensors will support expanded surveillance, mapping, and logistics operations. Demand will increase in the future from sectors seeking higher endurance and less operational interference over wider operating areas.

Rotary-Wing Drones

Rotary-Wing Drones segment is estimated at USD 13.1 billion in 2026 and is projected to reach USD 41.7 billion by 2033, at a CAGR of 18% during the forecast period.

Rotary-wing drones will experience strong adoption driven by vertical takeoff capability and controlled hovering performance. Urban surveillance, inspection activities and emergency response operations will benefit from enhanced obstacle avoidance and autonomous decision systems. Continued improvements in battery systems and AI-enabled controls will expand deployment in complex and confined environments.

Hybrid Drones

Hybrid Drones segment is estimated at USD 4.6 billion in 2026 and is projected to reach USD 21.2 billion by 2033, at a CAGR of 24.4% during the forecast period.

Hybrid drones will represent a balanced solution combining endurance and mobility. Future deployments will favor hybrid platforms for missions requiring flexible transitions between vertical lift and forward flight. Ongoing innovations in propulsion systems and autonomous flight management will position hybrid drones for diverse commercial and government use cases.

Solar-Powered Drones

Solar-Powered Drones segment is estimated at USD 1.8 billion in 2026 and is projected to reach USD 9.6 billion by 2033, at a CAGR of 26.8% during the forecast period.

Solar powered drones will support long-term operations through renewable energy integration. Advances in solar cell efficiency and lightweight energy storage will enable a persistent aerial presence. Environmental monitoring, border surveillance and communications relay missions will increasingly rely on solar-powered platforms supporting sustainability-focused operational strategies.

By Range of Flight, the market is divided into:

Less than 10 KM

Less than 10 KM segment is projected to reach USD 24.9 billion by 2033, at a CAGR of 16.2% during the forecast period.

Short-range autonomous drones operating below 10 KM will focus on localized tasks including facility inspection and real-time monitoring. Enhanced autonomy will reduce manual oversight while improving response accuracy. Demand will growth from businesses prioritizing fast deployment, cost performance, and precise quick-distance operational skills.

10 KM - 20 KM

10 KM - 20 KM segment is projected to reach USD 25.8 billion by 2033, at a CAGR of 18.2% during the forecast period.

Mid-range drones within 10 KM to 20 KM will support regional surveillance and logistics coordination. Improved communication links and autonomous route optimization will improve mission reliability. Future usage will increase within smart infrastructure tasks and business tracking applications requiring moderate operational insurance.

20 KM - 30 KM

20 KM - 30 KM segment is projected to reach USD 21 billion by 2033, at a CAGR of 20.6% during the forecast period.

Drones overlaying 20 KM to 30 KM will allow broader reconnaissance and shipping operations. Autonomous navigation supported through superior AI systems will enhance adaptability across varied terrains. Growing investment in local connectivity solutions will strengthen adoption across security, agriculture, and infrastructure development sectors.

More Than 30 KM

More Than 30 KM segment is projected to reach USD 21.1 billion by 2033, at a CAGR of 24.1% during the forecast period.

Long-range drones exceeding 30 KM will address strategic missions requiring extended reach and endurance. Autonomous choice-making frameworks will decorate project continuity throughout faraway places. Defense, environmental evaluation, and pass-regional logistics programs will pressure sustained growth for lengthy-variety self-reliant platforms.

By Payload, the market is further divided into:

Less Than 300 lbs

Less Than 300 lbs segment is projected to reach USD 43.2 billion by 2033.

Payload capacities beneath 300 lbs will assist light-weight packages including aerial imaging and environmental sensing. Future enhancements in sensor miniaturization and autonomous stability control will increase operational accuracy. Adoption will rise among commercial users seeking agility and cost-effective deployment models.

300-400 lbs

300-400 lbs segment is projected to reach USD 18.4 billion by 2033.

Payload levels between 300 and 400 lbs will enable superior gadget integration without compromising flight overall performance. Autonomous load control systems will improve protection and efficiency. Expanding use in industrial inspection and tactical logistics will encourage adoption across regulated operational environments.

400-500 lbs

400-500 lbs segment is projected to reach USD 14.3 billion by 2033.

Payload capacities from 400 to 500 lbs will support heavier contraptions and multi-sensor configurations. Autonomous flight optimization will manage increased weight while maintaining endurance. Infrastructure tracking, emergency deliver shipping, and protection-associated operations will contribute to growing call for within this category.

More than 500 lbs

More than 500 lbs segment is projected to reach USD 16.9 billion by 2033.

Payload capacities above 500 lbs will address excessive call for shipping and defense missions. Advanced propulsion and autonomous stabilization technologies will support reliable performance. Strategic logistics, military resupply, and catastrophe response operations will increasingly depend upon high-payload self-reliant drone systems.

By Application, the Global Autonomous Drone market is divided as:

Commercial

Commercial segment is projected to grow at a CAGR of 17.4% during the forecast period.

Commercial applications within the global autonomous drone market will expand through automation in logistics, infrastructure inspection, and data acquisition. Predictive analytics and AI-powered navigation will enhance operational efficiency. Enterprises will adopt autonomous drones to reduce costs while improving service precision and scalability.

Civilian

Civilian segment is projected to grow at a CAGR of 17.6% during the forecast period.

Civilian adoption will focus on public safety, environmental monitoring and urban management initiatives. Autonomous response systems will aid in faster decision-making during emergencies. Government-backed smart city programs will encourage widespread deployment, supporting monitoring, traffic analysis, and disaster preparedness objectives.

Military

Military segment is projected to grow at a CAGR of 22.1% during the forecast period.

Military use will prioritize intelligence gathering, reconnaissance and tactical support missions. Autonomous coordination and secure communication frameworks will strengthen operational effectiveness. The Defense Modernization Program will invest in advanced autonomous drone fleets that support strategic superiority and reduced human risk.

Others

Others segment is projected to grow at a CAGR of 21.3% during the forecast period.

Other applications will include research, humanitarian aid and remote connectivity support. Autonomous adaptability will enable operations in challenging terrain and disaster affected areas. Continued innovation will open up new use cases supporting scientific exploration and emergency relief initiatives in global regions.

By Region:

Based on geography, the Global Autonomous Drone market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Autonomous Drone Market is set to expand at a CAGR of 19.3% within the forecast period, reaching a market size (TAM) of USD 24.3 billion by the end of 2033.

North America is witnessing a surge in demand for autonomous drones, driven by defense modernization programs and an advanced R&D ecosystem supporting AI-enabled aerial systems.

North America benefits from strong commercial adoption in logistics, agriculture and infrastructure oversight, supported by a favorable regulatory framework.

Asia Pacific presents opportunities for growth through increased public investment in large-scale smart city projects and unmanned aerial surveillance.

Asia Pacific offers expansion prospects due to rapid industrialization and increasing use of autonomous drones in disaster management and precision farming.

Throughout the Middle East, Africa and South America, the adoption of autonomous drones progresses through improved infrastructure development and technological access, supported by safety requirements, resource monitoring and gradual regulatory alignment.

Competitive Landscape and Strategic Insights

The worldwide autonomous drone market has moved from early trials into large-scale industrial and defense use, driven by the need for faster data capture, reduced human risk, and consistent operations. Autonomous flight, supported by way of onboard sensors, vision structures, and edge processing, will permit drones to function with minimum guide input whilst retaining accuracy and protection. Adoption will continue to rise across surveillance, mapping, inspection, transport, agriculture, and emergency response. As regulations become clearer across many regions, adoption will expand beyond controlled environments into routine airspace operations.

Commercial innovation has been led by way of players centered on reliability, navigation, and smart flight manage. DJI, Autel Robotics, Parrot, and Skydio have created the economic and corporation segments via strong imaging, obstacle avoidance, and person-friendly structures. Companies which include Percepto, Airobotics, Delair, Wingcopter, Quantum-Systems, Draganfly, and AgEagle Aerial Systems have pushed automation similarly by way of permitting far flung operations, scheduled missions, and analytics-driven consequences. In parallel, companies like XAG, Yamaha Motor, ACSL, PRODRONE, EHang, and Garuda Aerospace have supported nearby boom through application-centered drones built for spraying, logistics, and urban mobility use cases.

Defense and security demand has remained a first-rate increase pillar, with self-sustaining drones helping intelligence, border monitoring, and tactical missions. Established defense contractors such as Lockheed Martin, Northrop Grumman, Boeing Insitu, General Atomics Aeronautical Systems, BAE Systems, Thales, Leonardo, Saab, Rheinmetall, Airbus Defence and Space, and L3Harris Technologies have increased unmanned portfolios to encompass higher autonomy and longer endurance. Newer protection-centered innovators consisting of Anduril Industries, Shield AI, Kratos Defense & Security Solutions, Textron Systems, and Teledyne FLIR have reinforced the marketplace with advanced sensing, AI-driven selection assist, and modular payload structures.

Regional and mid-sized producers have additionally played an important function in widening get entry to and specialization. Israel Aerospace Industries, Elbit Systems, Rafael Advanced Defense Systems, Baykar, Turkish Aerospace Industries (TAI), STM (Savunma Teknolojileri Muhendislik), Denel Dynamics, EDGE Group, Aeronautics Group, and UVision Air have supported countrywide applications whilst increasing export presence. In Asia and rising markets, ideaForge, Asteria Aerospace, and different neighborhood manufacturers have addressed fee, customization, and compliance wishes. Overall, opposition will continue to be intense, with progress shaped by autonomy software program, regulatory reputation, and the capability to supply reliable consequences at scale.

Forecast and Future Outlook

Market size is forecast to rise from USD 22.7 billion in 2025 to over USD 92.8 billion by 2033.

The industry will move forward in ethical and geopolitical considerations. Autonomous drones will impact border surveillance, disaster response prioritization, and surveillance accountability, leading to policy discussions that extend beyond aviation authorities. The long-term impact will depend on how autonomy is combined with human oversight in its place. In this context, the scope of the future will not be defined by hardware advancement alone, but by how intelligence, governance and responsibility converge within autonomous aerial operations.

This research report categorizes the Autonomous Drone market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyzes the key growth drivers, opportunities, and challenges influencing the Autonomous Drone market. Recent market developments and competitive strategies such as expansion, new site development, partnership, merger, and acquisition are included to present the competitive landscape.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Autonomous Drone market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 19.3% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Units

Segmentation

By Product, Range of Flight, Payload, Application, and Region

By Region

North America (By Product, Range of Flight, Payload, Application, and Country)

United States

Canada

Mexico

Europe (By Product, Range of Flight, Payload, Application, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Product, Range of Flight, Payload, Application, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Product, Range of Flight, Payload, Application, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Product, Range of Flight, Payload, Application, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share and Revenue

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

Import Export Trade Statistics

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Top players operating in the Autonomous Drone industry include DJI, Autel Robotics, Parrot, Skydio, AeroVironment, and Teledyne FLIR.

The Rotary-Wing Drones is the leading type segment in the Global market.

Growing adoption of AI-enabled robotics to enhance inspection, surveillance, and operational efficiency across industrial sectors and Rising demand for automated aerial systems that reduce operational risk and lower labor-dependent field activities. are key driving factors, boosting the market.

Asia Pacific region dominates the market.

The Global Autonomous Drone market is likely to grow at a CAGR of 19.3% over the forecast period (2026-2033).

Global Autonomous Drone market is estimated to reach USD 92.8 billion by 2033.

Regulatory restrictions around BVLOS operations and airspace integration limiting large-scale deployment will hamper market growth within the forecast period.

The Metastat Insights analysis shows that the North America Autonomous Drone market size is estimated to be USD 24.3 billion by 2033.

The Metastat Insights study shows that the Global Autonomous Drone market size was USD 22.7 billion in 2025.

Global Robotic Combat Vehicle (RCV) market size is valued at USD 761.5 million in 2025 and is projected to reach USD 1,297.8 million in 2033, at a CAGR of 6.9% from 2026 to 2033

Global Defense Radar market size is valued at USD 14.9 billion in 2025 and is projected to reach USD 22.9 billion in 2033, at a CAGR of 5.5% from 2026 to 2033

US Aerospace Material Testing Service Market Size, Share by 2030

US Aerospace Material Testing Service Market valued at $126.8 million in 2023 and projected to reach $201.0 million by 2030

US Aerospace Material Testing Service Market, US Aerospace Material Testing Service Market Size, US Aerospace Material Testing Service Market Share, US Aerospace Material Testing Service Market Analysis, US Aerospace Material Testing Service Market Growth, US Aerospace Material Testing Service Market Trends, US Aerospace Material Testing Service Market Research Report, US Aerospace Material Testing Service Market Forecast, US Aerospace Material Testing Service, US Aerospace Material Testing Service Market Research, US Aerospace Material Testing Service Industry, US Aerospace Material Testing Service Market Segmentation, US Aerospace Material Testing Service Market Companies, United States Aerospace Material Testing Service Market