Passive Optical LAN (POL) Solution Market Size, Share, By End User (Hospitality, Healthcare, Education, Government, and Others), By Type (GPON and EPON), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4551

Published

February 14, 2026

Pages

311 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

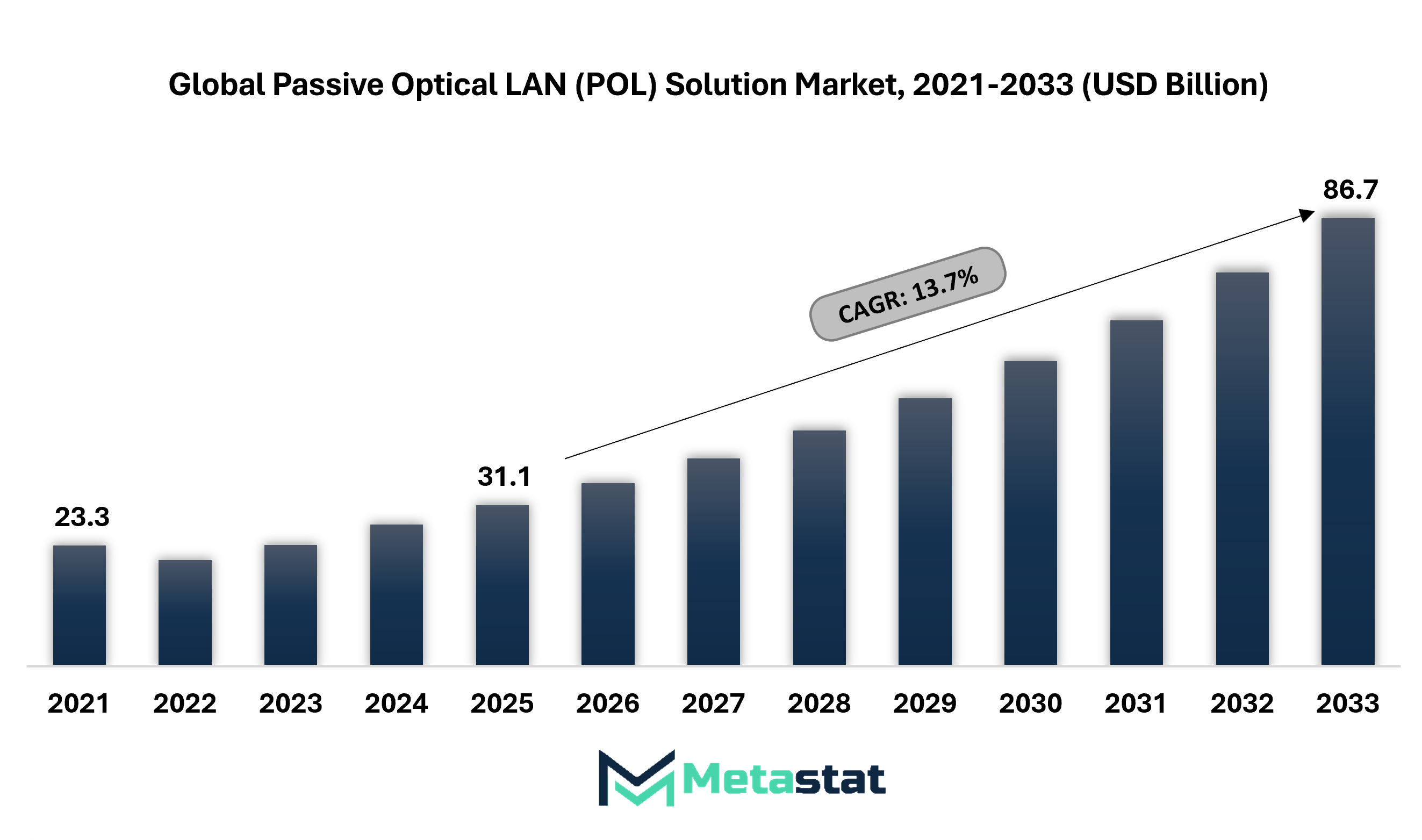

The global Passive Optical LAN (POL) Solution market size is valued at USD 31.1 billion in 2025 and is projected to grow from USD 35.3 billion in 2026 to USD 86.7 billion by 2033.

Global Passive Optical LAN (POL) Solution Market - Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Passive Optical LAN (POL) Solution market valued at USD 31.1 billion in 2025, growing at a CAGR of 13.7% by 2033, with potential to exceed USD 86.7 billion.

North America holds 28.3% share in 2025, with the US leading within the region.

Hospitality segment accounts for 18.7% share in 2025, propelled by hotel and resort network upgrades supporting smart rooms and high-speed guest connectivity.

Key trend driving growth: Increased demand for high-bandwidth, future-proof LAN infrastructure across large sites (campuses, hotels, hospitals, airports).

Opportunities include rising adoption of smart buildings and loT-heavy environments creates strong opportunities for POL as a scalable, fiber-deep digital backbone.

Key insight: The global Passive Optical LAN (POL) solutions market is witnessing a steady shift toward fiber-based network architectures as organizations prioritize long-term efficiency and scalable connectivity.

The global Passive Optical LAN (POL) solutions market within enterprise networking and optical communications will experience growth beyond current deployment patterns, moving toward digital infrastructure designed for long-term utility rather than short-term technology upgrades. The market will be shaped by architectural thinking that considers connectivity as a silent backbone supporting automation, spatial intelligence, and adaptive building ecosystems. Optical LAN frameworks will no longer be planned solely for data transfer requirements, and will support how the environment senses, responds, and self-regulates.

Future implementations will closely align with intelligent campuses, large-scale public infrastructure, and hyperconnected industrial spaces where centralized controls will be operated with minimal physical intervention. Decision-makers will increasingly view optical LAN layouts as foundational infrastructure, positioned to support future software layers rather than isolated networking initiatives. Such a shift will encourage longer planning cycles, deeper integration with building design, and closer collaboration among network engineers, city planners, and systems architects.

Market Dynamics

Growth Drivers:

Increasing demand for high-bandwidth, future-proof LAN infrastructure across large sites (campuses, resorts, hospitals, airports).

Large-scale facilities will continue to move towards networked systems that aid growing data loads, linked offerings, and virtual operations. Fiber-based LAN architecture supports long-term bandwidth scaling, stable connectivity, and simplified network layout. Planning for future-equipped infrastructure across campuses, health care centres, and transportation hubs will force persistent adoption.

Lower total cost of ownership (TCO) and energy savings versus traditional copper-based, multi-switch Ethernet LANs.

Operational planning increasingly favors network models that minimize power use and equipment volume. Fiber-centric LAN deployments will reduce cabling requirements, reduce active components, and cut cooling requirements across access layers. Extended lifecycle, cost efficiency and sustainability goals will influence procurement decisions in enterprise and public infrastructure projects.

Restraints and Challenges:

High upfront investment and perceived migration complexity from legacy Ethernet architectures.

Initial transition planning often highlights capital expenditure concerns associated with fiber rollout and system redesign. Network modernization projects will face hiccups where existing copper layouts remain functional. Budget cycles and short-term return expectations will slow the pace of decision-making despite long-term efficiency gains.

Limited in-house expertise and conservative IT preference for familiar copper/Ethernet switching technologies.

Technical teams often rely on established skill sets focused on traditional Ethernet systems. Training lag and change management challenges will restrict rapid progress toward optical LAN adoption. Comfort with known technologies continues to shape infrastructure choices in risk-averse organizational environments.

Opportunities:

Adoption of smart buildings and IoT-heavy environments creates strong opportunities for POL as a scalable, fiber-deep digital backbone.

The development of smart infrastructure will require sensors, automation platforms, and networks capable of supporting real-time analytics. Fiber-based LAN frameworks will align with intelligent building design by offering scalability, stability, and simplified expansion. Urban development and digital convenience planning will open avenues for sustained growth for the global Passive Optical LAN (POL) solutions market.

Market Segmentation Analysis

The global Passive Optical LAN (POL) Solution market is mainly classified based on Type, End User and Region.

By End User, the market is further segmented into:

Hospitality

Hospitality segment was valued at USD 6.6 billion in 2026 and is projected to reach USD 16.1 billion by 2033, at a CAGR of 13.7% during the forecast period.

The hospitality sector will see the increasing adoption of fiber-based LAN solutions for supporting smart rooms, high-speed networking, and digital guest services. Hotels and resorts will benefit from the easier management of networks, minimized cabling, and future scalability for supporting digital experience applications within the overall Passive Optical LAN solutions market.

Healthcare

Healthcare segment was valued at USD 8.7 billion in 2026 and is projected to reach USD 23.0 billion by 2033, at a CAGR of 14.9% during the forecast period.

Healthcare institutions will be dependent on sophisticated optical LAN infrastructures that can handle real-time access to data as well as ensure reliable communication. Hospitals and healthcare institutions will focus on ensuring a stable bandwidth and minimizing latency to optimize efficiency, as well as develop a platform for technology-based healthcare service provision.

Education

Education segment was valued at USD 5.4 billion in 2026 and is projected to reach USD 13.4 billion by 2033, at a CAGR of 13.8% during the forecast period.

Universities, K-12 school districts, and multi-building campuses are adopting POL to support high-density Wi-Fi, unified communications, security and surveillance, and cloud-first learning platforms. Campus network refresh cycles are increasingly aligned with smart classroom upgrades, digital administration, and centralized IT operations, owing to the need for scalable bandwidth, simplified cabling, and long lifecycle infrastructure.

Government

Government segment was valued at USD 4.2 billion in 2026 and is projected to reach USD 9.9 billion by 2033, at a CAGR of 13.1% during the forecast period.

Government infrastructure is moving more towards optical LAN solutions that can help establish secure communications, smart city initiatives, and the digitization of public services. The management and administrative buildings, data centres, and public facilities within these will seek reliable network systems that can be used for long-term planning and developing digital governance requirements.

Others

Others segment was valued at USD 10.2 billion in 2026 and is projected to reach USD 23.4 billion by 2033, at a CAGR of 12.7% during the forecast period.

Optical LAN systems will assist commercial spaces, transportation hubs, and enterprise campuses to meet high data demand and automation requirements. Centralized control, energy efficiency, and simplified maintenance will support future-ready operations across applications beyond traditional target environments.

By Type, the market is divided into:

GPON

GPON segment is projected to reach USD 45.4 Billion by 2033, at a CAGR of 13% during the forecast period.

GPON technology will remain among the priorities owing to its high bandwidth capacity and efficient delivery of data. Enterprises will move toward GPON to support their ever-expanding digital workload, centrally designed infrastructure, and a scalable network design in line with long-term connectivity plans.

EPON

EPON segment is projected to reach USD 40.5 Billion by 2033, at a CAGR of 14.5% during the forecast period.

The Ethernet passive optical network technology will grab attention owing to its flexibility and compatibility with Ethernet. Organizations will select EPON to integrate existing Ethernet environments with optical access systems for cost control and phased upgrades, aligned with future data transmission and performance requirements.

By Region:

Based on geography, the global Passive Optical LAN (POL) Solution market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Passive Optical LAN (POL) Solution Market is set to expand at a CAGR of 13.7% within the forecast period, reaching a market size (TAM) of USD 26.1 billion by the end of 2033.

In North America, large-scale modernization of enterprise and government campuses and data-intensive centers will accelerate adoption of POL solutions across public and private sectors.

North America is likely to see continued demand, with hyperscale data centers and smart industrial buildings shifting toward fiber-centric LAN frameworks for performance and scalability.

Asia Pacific will present strong opportunities, with rapid urban infrastructure projects integrating POL solutions into smart cities, airports, and major transportation hubs.

The expansion of digitalization in education, healthcare, and manufacturing will open avenues for POL deployment in cost-sensitive but high-growth economies in the Asia-Pacific region.

In the Middle East, Africa, and South America, POL adoption will progress selectively, shaped by infrastructure readiness and project-led investment cycles. The Middle East will remain the lead adoption pocket, owing to smart government facilities and high-capacity requirements across hospitality and aviation. Africa and South America will advance through targeted campus, public sector, and enterprise modernization deployments, supported by expanding fiber footprints in dense urban nodes.

Competitive Landscape and Strategic Insights

The market for Global Passive Optical LAN (POL) Solution has been receiving increased attention as a network solution positioned to accommodate high data requirements while maintaining efficient operations. The adoption of POL solutions is increasing in both commercial buildings and healthcare institutions that require high levels of reliable connectivity. POL solutions use fiber-based infrastructure that will help to alleviate the issue of complex cabling and maintenance costs. With increasing dependency on digital services, Passive Optical LAN Solution is set to remain a popular option for any environment that demands high performance alongside efficient network management.

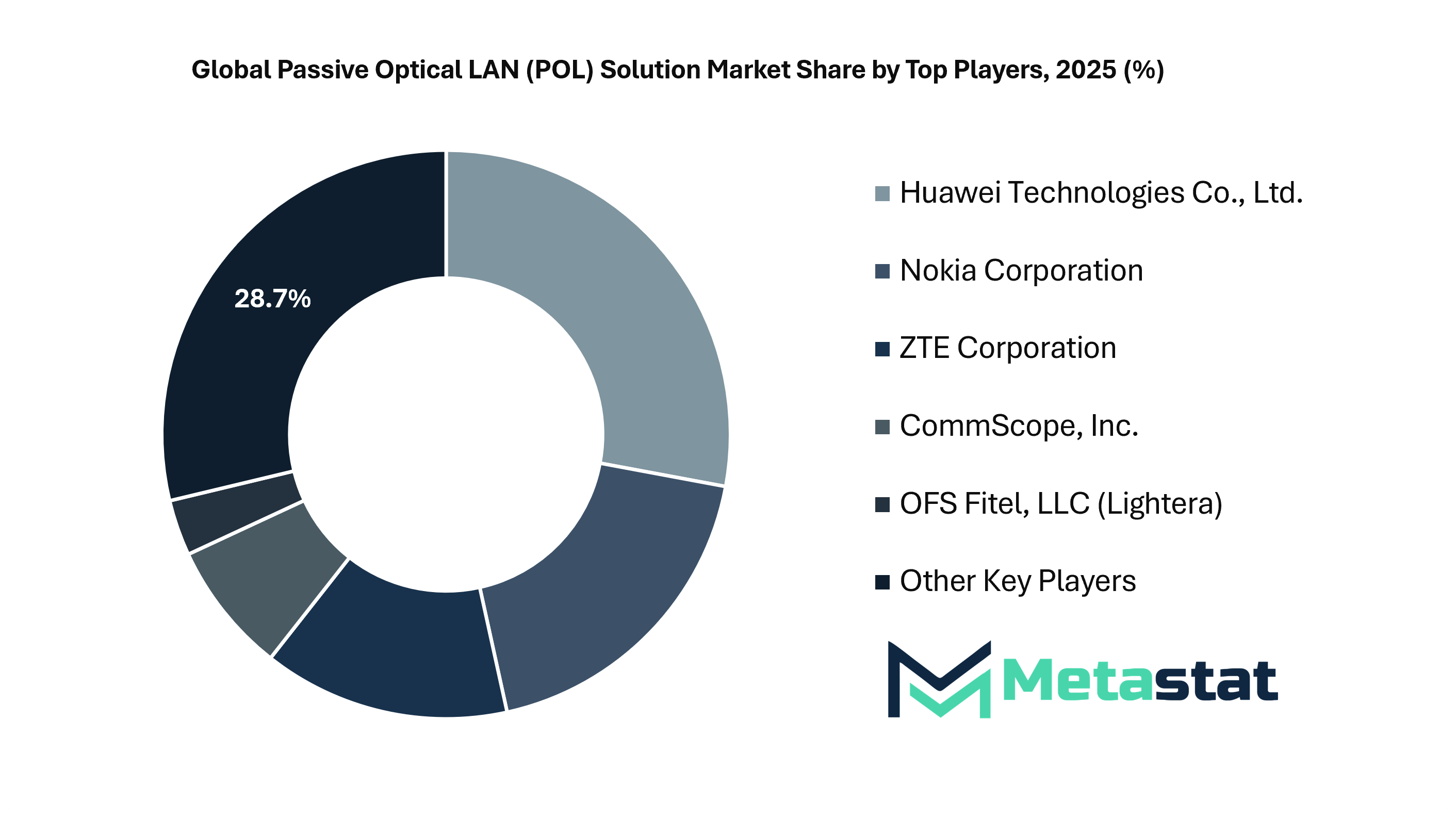

The market is largely influenced by the technological advancements brought along by established tech firms specializing in optical solutions. Huawei Technologies Co., Ltd., Nokia, and ZTE Corporation are some of the key players that have contributed to the development of POL solutions with the help of integrated systems that are suitable for large-scale implementations. The innovation, research, optimization, and adaptability to the latest information technologies will help in the further implementation of POL solutions across various geographies. Suppliers are, in most cases, preferred for implementations that require a high level of dependability, security, and longevity.

Along with these global giants, many niche and medium-sized companies contribute strongly to the market by catering to specific networking needs. Adtran, Inc., Zyxel Communications, EdgeCore Networks Corporation, FS.Com Inc., and Tellabs Access, LLC are known for delivering flexible POL components and access solutions that can be tailored to suit a variety of customer needs. CommScope, Inc., Corning Incorporated, Prysmian Group, and OFS Fitel, LLC (Lightera) strengthen the ecosystem through high-quality fiber, cabling and connectivity solutions that form the backbone of POL networks.

Regional players and diverse technology companies further expand the competitive landscape of the global Passive Optical LAN (POL) Solutions market. Tejas Networks Limited, TP-Link Systems Inc., and Zone Technologies, Inc. focuses on cost-effective and scalable solutions suitable for emerging and developed markets. These companies often meet the needs of enterprises seeking reliable POL deployment without excessive changes to the infrastructure. Through continued product development and strategic partnerships, all these industry players will collectively influence how POL solutions are implemented and adopted around the world in the years to come.

Forecast and Future Outlook

Market size is forecast to rise from USD 31.1 billion in 2025 to over USD 86.7 billion by 2033.

With advancements in digital working, optical network solutions will come into play for flexible space reconfiguration, whereby designing new space without reshaping basic infrastructure will become possible. These flexible solutions will apply to health facilities, transport infrastructure, and learning environments, where predictability and reliability with minimum changes will become more important than mere network speeds. Here again, value propositions will be more related to predictability rather than speeds. Besides the conventional applications of the technology found within the enterprise setting, there will be its applications within smart governance architecture, where there will be a significant need for standardization and management. In the future, the deployment of optical LANs will represent a paradigm shift in how people think of infrastructure as quiet, sustainable, and beyond the lifespan of various technological generations, ensuring its positioning as a future foundational infrastructure rather than a temporary solution for networking.

Passive Optical LAN (POL) Solution Market Key Segments:

By End User:

Hospitality

Healthcare

Education

Government

Others

By Type:

GPON

EPON

Key Global Passive Optical LAN (POL) Solution Industry Players

This research report categorizes the Passive Optical LAN (POL) Solution market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Passive Optical LAN (POL) Solution market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Passive Optical LAN (POL) Solution market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 13.7% from 2026 to 2033

Revenue Unit

USD Billion

Sales Volume Unit

Units

Segmentation

By End User, Type, and Region

By Region

North America (By End User, Type, and Country)

United States

Canada

Mexico

Europe (By End User, Type, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By End User, Type, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By End User, Type, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By End User, Type, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Market Leaders Landscape

Full Analysis of the Parent Industry

Industry Statistics

Important Changes in Market Flow

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Prepositions (USP) of Leading Market Players

New Zealand Optical Encryption Market Size, Share, Trends, 2033

New Zealand Optical Encryption market size is valued at USD 34.5 million in 2025 and is projected to reach USD 76.9 million in 2033, at a CAGR of 10.3% from 2026 to 2033.

New Zealand Optical Encryption Market, New Zealand Optical Encryption Market Size, New Zealand Optical Encryption Market Share, New Zealand Optical Encryption Market Analysis, New Zealand Optical Encryption Market Growth, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market Research Report, New Zealand Optical Encryption Market Forecast, New Zealand Optical Encryption, New Zealand Optical Encryption Market Research, New Zealand Optical Encryption Industry, New Zealand Optical Encryption Industry Report, New Zealand Optical Encryption Market Data, New Zealand Optical Encryption Statistics, New Zealand Optical Encryption Market Statistics, New Zealand Optical Encryption Industry Trends, New Zealand Optical Encryption Market Report, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market News, New Zealand Optical Encryption Forecasts, New Zealand Optical Encryption Market Intelligence Report

Generative AI in Analytics Market Size, Share, Trends, 2033

Generative AI in Analytics market size is valued at USD 1.6 billion in 2025 and is projected to reach USD 10.9 billion in 2033, at a CAGR of 26.8% from 2026 to 2033.

Generative AI in Analytics Market, Generative AI in Analytics Market Size, Generative AI in Analytics Market Share, Generative AI in Analytics Market Analysis, Generative AI in Analytics Market Growth, Generative AI in Analytics Market Trends, Generative AI in Analytics Market Research Report, Generative AI in Analytics Market Forecast, Generative AI in Analytics, Generative AI in Analytics Market Research, Generative AI in Analytics Industry, Generative AI in Analytics Industry Report, Generative AI in Analytics Market Data, Generative AI in Analytics Statistics, Generative AI in Analytics Market Statistics, Generative AI in Analytics Industry Trends, Generative AI in Analytics Market Report, Generative AI in Analytics Market Trends, Generative AI in Analytics Market News, Generative AI in Analytics Forecasts, Generative AI in Analytics Market Intelligence Report

Retail Project Management Software market size is valued at USD 1,505.5 million in 2025 and is projected to reach USD 3,524.9 million in 2033, at a CAGR of 11.2% from 2026 to 2033.

UK Immersive Entertainment & Experiential Property Market Size, Share, Trends, 2033

UK Immersive Entertainment & Experiential Property Market size is valued at USD 6.17 billion in 2025 and is projected to reach USD 26.16 billion in 2033, at a CAGR of 19.5% from 2026 to 2033

UK Immersive Entertainment & Experiential Property Market, UK Immersive Entertainment & Experiential Property Market Size, UK Immersive Entertainment & Experiential Property Market Share, UK Immersive Entertainment & Experiential Property Market Analysis, UK Immersive Entertainment & Experiential Property Market Growth, UK Immersive Entertainment & Experiential Property Market Trends, UK Immersive Entertainment & Experiential Property Market Research Report, UK Immersive Entertainment & Experiential Property Market Forecast, UK Immersive Entertainment & Experiential Property, UK Immersive Entertainment & Experiential Property Market Research, UK Immersive Entertainment & Experiential Property Industry, UK Immersive Entertainment & Experiential Property Industry Report, UK Immersive Entertainment & Experiential Property Market Data, UK Immersive Entertainment & Experiential Property Statistics, UK Immersive Entertainment & Experiential Property Market Statistics, UK Immersive Entertainment & Experiential Property Industry Trends, UK Immersive Entertainment & Experiential Property Market Report, UK Immersive Entertainment & Experiential Property Market Trends, UK Immersive Entertainment & Experiential Property Market News, UK Immersive Entertainment & Experiential Property Forecasts, UK Immersive Entertainment & Experiential Property Market Intelligence Report