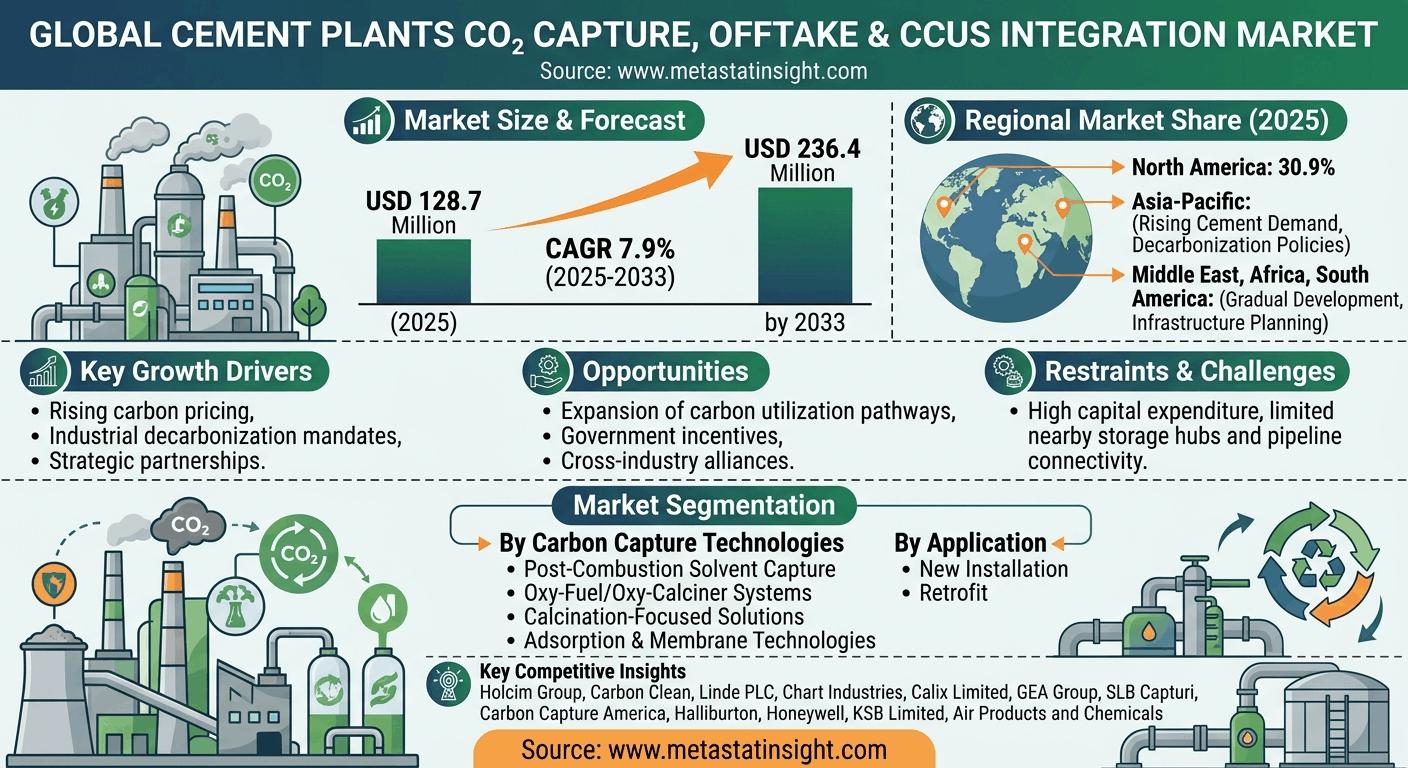

The global Cement Plants CO2 Capture, Offtake & CCUS Integration Market is witnessing a transformative shift as heavy industries pivot toward aggressive sustainability goals. According to the latest strategic analysis from MetaStat Insight, the market is valued at USD 128.7 million in 2025 and is projected to surge at a CAGR of 7.9%, reaching a valuation of USD 236.4 million by 2033.

As the cement industry faces mounting pressure to address emissions from both fuel combustion and clinker production, the integration of Carbon Capture, Utilization, and Storage (CCUS) has emerged as a critical pathway. The report highlights that cement facilities are evolving from standalone manufacturing sites into integral nodes within regional carbon management networks.

Key Market Drivers and Trends

The growth of the market is primarily fueled by:

-

Stringent Carbon Pricing: Rising carbon pricing frameworks and industrial decarbonization mandates are accelerating the deployment of CO2 capture systems across cement manufacturing facilities.

-

Strategic Alliances: Partnerships between cement producers, energy firms, and infrastructure developers are expanding CO2 transport networks and industrial-scale storage projects.

-

Utilization Pathways: The expansion of carbon utilization-converting captured CO2 into synthetic fuels, chemicals, and building materials-is creating lucrative commercial offtake potential.

Technological and Segment Insights

The market is characterized by diverse capture technologies tailored for cement kilns:

-

Post-Combustion Solvent Capture: Holding a dominant 66.4% market share in 2025, this segment is valued at USD 92.2 million in 2026. It remains the leading choice due to its efficiency in separating CO2 from flue gas streams.

-

Oxy-Fuel/Oxy-Calciner Systems: Expected to grow at a high CAGR of 8.5%, these systems are gaining traction for facilities pursuing advanced kiln redesigns.

-

Retrofit vs. New Installation: While the Retrofit segment is vital for modernizing existing plants (projected to reach USD 142.1 million by 2033), the New Installation segment is growing rapidly at a 10.1% CAGR, as future infrastructure is designed with integrated carbon management from the outset.

Regional Outlook

-

North America: Leads the market with a 30.9% share in 2025, driven by the U.S. and supportive tax incentives.

-

Asia-Pacific: Represents a high-growth region due to rising cement demand and government-backed decarbonization roadmaps in major economies.

-

Middle East, Africa, and South America: Witnessing gradual development as infrastructure planning begins to support long-term sequestration and offtake pathways.

Competitive Landscape

Competitive Landscape

Key industry players are driving innovation through specialized technology and gas processing solutions. Prominent companies profiled in the report include Holcim Group, Carbon Clean, Linde PLC, Chart Industries Inc., Calix Limited, GEA Group Aktiengesellschaft, SLB Capturi, Carbon Capture America, Inc., Halliburton Energy Services, Inc., Honeywell International Inc., KSB Limited, and Air Products and Chemicals, Inc.

“The transition to CCUS integration is no longer optional for the heavy industry,” notes the MetaStat Insight analysis. “The coordination between engineering teams, infrastructure partners, and regulatory authorities will define the next phase of global cement sector emissions reduction.”

About MetaStat Insight

MetaStat Insight is a leading global market research firm providing comprehensive data-driven analysis and strategic outlooks across diverse industries. We empower businesses with actionable insights to navigate complex market dynamics and achieve sustainable growth.