Cement Plants CO₂ Capture, Offtake & CCUS Integration Market Size, Share, By Carbon Capture Technologies (Post-Combustion Solvent Capture, Oxy-Fuel Systems, Oxy-Calciner Systems, Calcination-Focused Solutions, Adsorption Technologies, and Membrane Technologies), By Application (New Installation and Retrofit), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4650

Published

April 21, 2026

Pages

313 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

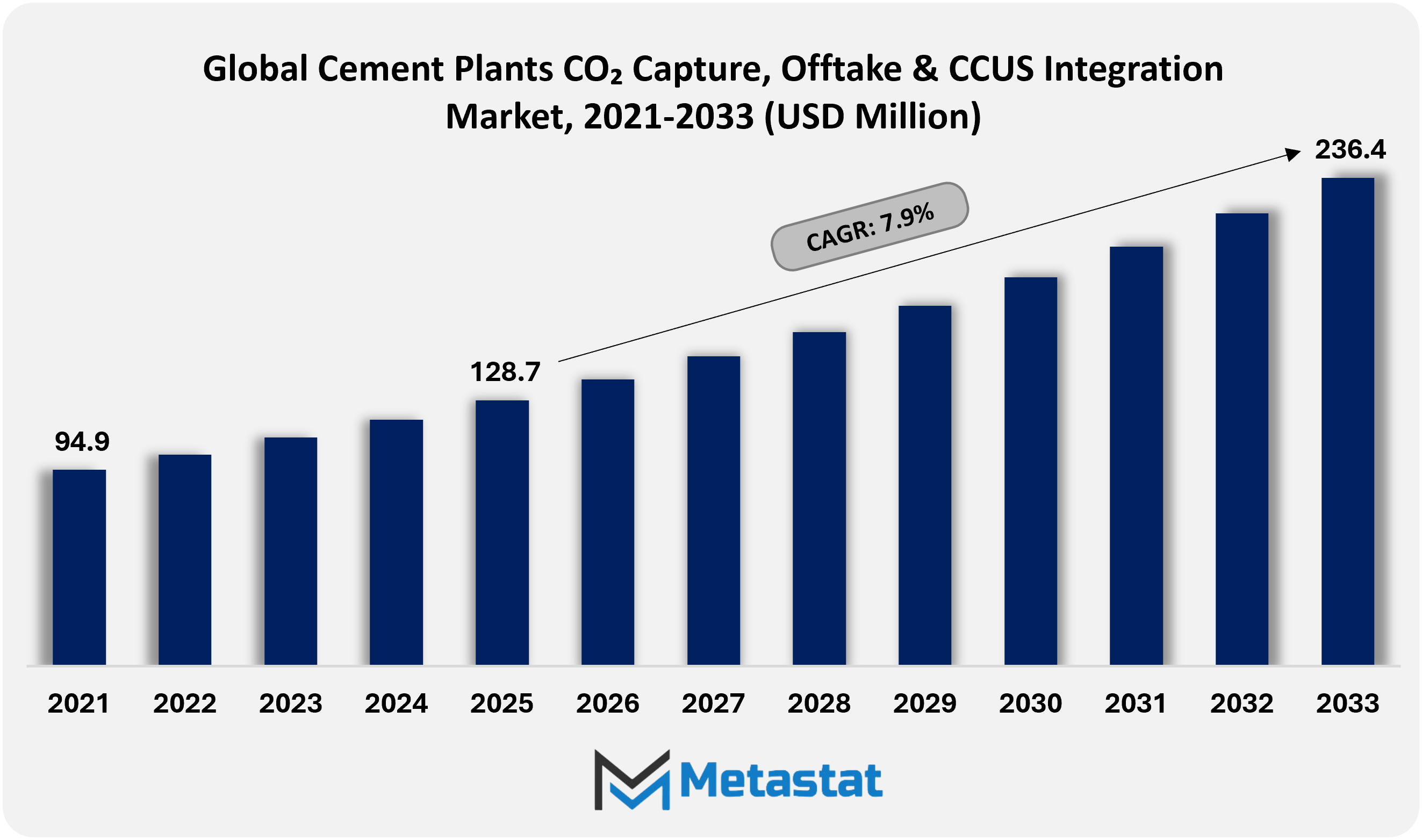

Global Cement Plants CO₂ Capture, Offtake & CCUS Integration market size is valued at USD 128.7 million in 2025 and projected to grow at a CAGR of 7.9% during the forecast period, reaching USD 236.4 million by 2033.

Global Cement Plants CO₂ Capture, Offtake & CCUS Integration Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

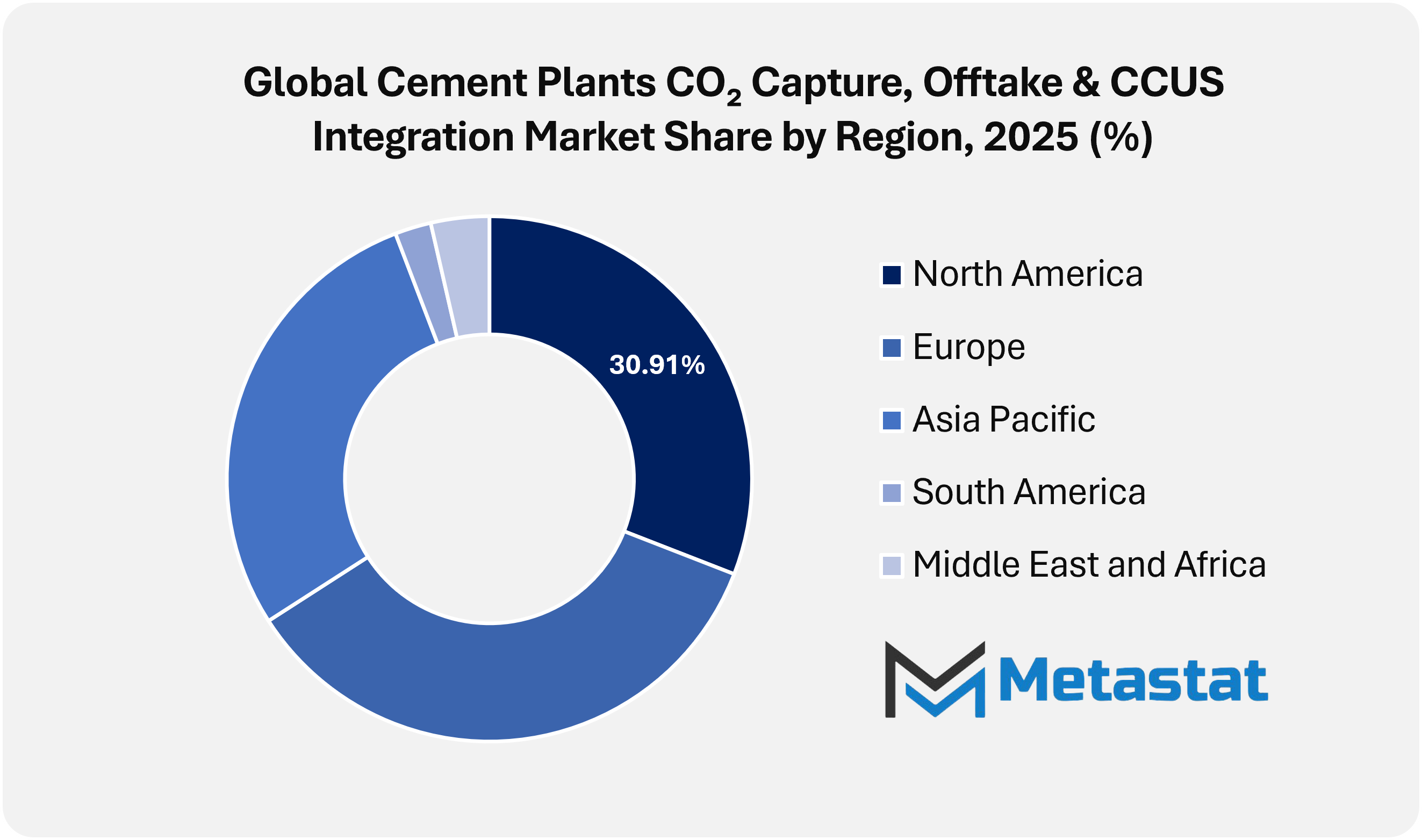

North America holds 30.9% in 2025 with US leading the market share in 2025.

Post-Combustion Solvent Capture segment accounts for a market share of 66.4% in 2025.

Key trends driving growth: Rising carbon pricing frameworks and industrial decarbonization mandates accelerate deployment of CO₂ capture and CCUS systems across cement manufacturing facilities and Strategic partnerships between cement producers, energy firms, and infrastructure developers expand CO₂ transport networks and industrial-scale storage projects.

Opportunities include expansion of carbon utilization pathways including synthetic fuels, chemicals, and building materials creates commercial offtake potential for captured CO₂ from cement plants and government incentives, climate finance programs, and cross-industry decarbonization alliances support large demonstration projects and long-term CCUS infrastructure development.

Key insight: Rapid decarbonization pressure across heavy industry positions CO₂ capture, offtake agreements, and CCUS integration at cement plants among central pathways for lowering global cement sector emissions.

The Global Cement Plants CO₂ Capture, Offtake & CCUS Integration Market represents a specialized segment within the broader cement and industrial decarbonization industry, centered on the capture, transport, offtake, utilization, and permanent storage of carbon emissions generated during clinker production. While capture technologies installed at kiln exhaust systems remain the core focus, the wider operating model increasingly depends on coordination among cement producers, energy companies, transport infrastructure providers, carbon utilization partners, and long-term storage operators.

Over the coming years, cement facilities will evolve into integral nodes within regional carbon management networks rather than operating as standalone manufacturing sites. Captured CO₂ streams will be conditioned, compressed, and directed toward pipelines, liquefaction terminals, mineralization units, or sequestration hubs. This transition will increase the importance of monitoring systems capable of tracking CO₂ purity, pressure stability, transport scheduling, and compliance with measurement, reporting, and verification protocols.

Market Dynamics

Growth Drivers:

Rising carbon pricing frameworks and business decarbonization mandates boost up deployment of CO₂ seize and CCUS systems across cement manufacturing facilities.

The Global Cement Plants CO₂ Capture, Offtake & CCUS Integration Market is gaining momentum under increasingly stringent carbon pricing mechanisms and industrial decarbonization mandates introduced by governments and regulatory bodies. These policy measures are encouraging cement manufacturers to adopt capture technologies, modernize kiln systems, and integrate carbon management infrastructure aligned with long-term emission reduction goals.

Strategic partnerships among cement manufacturers, electricity corporations, and infrastructure developers enlarge CO₂ shipping networks and commercial-scale garage projects.

Cement producers are increasingly entering into strategic partnerships with energy companies, logistics operators, and infrastructure developers to establish integrated carbon management networks. Joint investments in pipeline systems, transport terminals, and geological storage assets are strengthening CO₂ transport capacity and supporting coordinated development of capture, transport, and storage solutions across major cement production regions.

Restraints and Challenges:

High capital expenditure for seize units, compression infrastructure, and shipping pipelines limits big-scale adoption among smaller cement producers.

High upfront investment requirements associated with capture equipment, gas compression systems, monitoring technologies, and transport infrastructure remain a major challenge for market expansion. Smaller and mid-sized cement producers often operate under tight margin structures and limited financing access, which can delay modernization plans and restrict wider deployment of CCUS systems across the industry.

Limited availability of nearby CO₂ garage hubs and pipeline connectivity slows integration of seize initiatives with long-term sequestration or usage pathways.

In several industrial regions, the lack of accessible geological storage hubs, pipeline corridors, and marine transport infrastructure continues to limit project integration. Without coordinated regional carbon transport and storage networks, capture facilities will face delays in connecting with sequestration or utilization destinations, reducing the pace of commercial-scale deployment.

Opportunities

Expansion of carbon utilization pathways along with artificial fuels, chemical compounds, and building substances creates industrial offtake ability for captured CO₂ from cement vegetation.

Growing innovation in carbon utilization applications such as synthetic fuels, specialty chemicals, and carbon-based construction materials is creating new commercial offtake opportunities for captured CO₂ from cement plants. Long-term agreements between cement producers and downstream processing companies will strengthen revenue visibility and improve the business case for carbon capture investments.

Market Segmentation Analysis

The Global Cement Plants CO₂ Capture, Offtake & CCUS Integration market is classified based on Carbon Capture Technologies, and Application.

By Carbon Capture Technologies, the market is further segmented into:

Post-Combustion Solvent Capture

Post-Combustion Solvent Capture segment is valued at USD 92.2 million in 2026 and is projected to reach USD 157.4 million by 2033, at a CAGR of 7.9% during the forecast period.

Post-Combustion Solvent Capture represents the leading technology segment within the Global Cement Plants CO₂ Capture, Offtake & CCUS Integration Market. These systems use chemical absorption processes to separate carbon dioxide from flue gas streams generated during clinker production. Ongoing improvements in solvent regeneration efficiency and process integration are supporting adoption across large-scale cement facilities seeking to lower emissions while maintaining stable plant performance.

Oxy-Fuel/Oxy-Calciner Systems

Oxy-Fuel/Oxy-Calciner Systems segment is valued at USD 24.8 million in 2026 and is projected to reach USD 43.8 million by 2033, at a CAGR of 8.5% during the forecast period.

Oxy-Fuel/Oxy-Calciner Systems are emerging as an important technology pathway for cement decarbonization by creating a controlled combustion environment that produces more concentrated CO₂ streams. These systems improve capture efficiency and support deeper emission reduction potential, particularly in facilities pursuing advanced kiln redesign and long-term CCUS integration strategies.

Calcination-Focused Solutions

Calcination-Focused Solutions segment is valued at USD 12.3 million in 2026 and is projected to reach USD 20.3 million by 2033, at a CAGR of 7.4% during the forecast period.

Calcination-Focused Solutions are gaining relevance in the market owing to their ability to directly address process emissions released during limestone decomposition. By integrating dedicated capture systems near calcination stages, cement plants can isolate a significant share of CO₂ before it mixes with broader flue gas streams, improving the efficiency of carbon management during clinker production.

Adsorption & Membrane Technologies

Adsorption & Membrane Technologies segment is valued at USD 9.6 million in 2026 and is projected to reach USD 14.9 million by 2033, at a CAGR of 6.4% during the forecast period.

Adsorption and membrane technology will introduce compact separation structures in the Cement Plants CO₂ Capture, Offtake & CCUS Integration Market. Solid sorbent substances and selective membrane layers will clear out carbon dioxide from cement plant emissions with minimum chemical consumption. Technological development will encourage scalable installations across large industrial facilities seeking efficient carbon separation solutions.

By Application, the market is divided into:

New Installation

New Installation segment is projected to reach USD 94.3 million by 2033, at a CAGR of 10.1% during the forecast period.

New Installation segment will increase swiftly within the Cement Plants CO₂ Capture, Offtake & CCUS Integration Market via creation of cement flowers designed with included carbon management systems. Future business infrastructure planning will include seize units, shipping pipelines, and storage education for the duration of early design stages.

Retrofit

Retrofit segment is projected to reach USD 142.1 million by 2033, at a CAGR of 6.6% during the forecast period.

Retrofit tasks will stay vital for modernization of existing cement facilities inside the Cement Plants CO₂ Capture, Offtake & CCUS Integration Market. Engineering enhancements will combine seize device into operational kilns without important disruption to cement production cycles. Long-term decarbonization objectives will inspire plant operators to convert traditional centers into low-emission commercial sites.

By Region:

Based on geography, the Global Cement Plants CO₂ Capture, Offtake & CCUS Integration market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America is driving market development through supportive tax incentives, funding mechanisms, and expanding CCUS infrastructure across industrial sectors.

Large-scale investment in carbon transport and storage networks is strengthening North America’s position in integrating cement plants with regional CCUS ecosystems.

Asia Pacific presents strong growth potential owing to rising cement demand, expanding industrial capacity, and increasing policy attention toward decarbonization of hard-to-abate sectors.

Government-backed decarbonization roadmaps across major Asia Pacific economies are encouraging wider adoption of CCUS integration in cement manufacturing hubs.

The Middle East, Africa, and South America are witnessing gradual market development as industrial decarbonization initiatives and infrastructure planning begin to support CO₂ capture, offtake, and storage pathways in cement production.

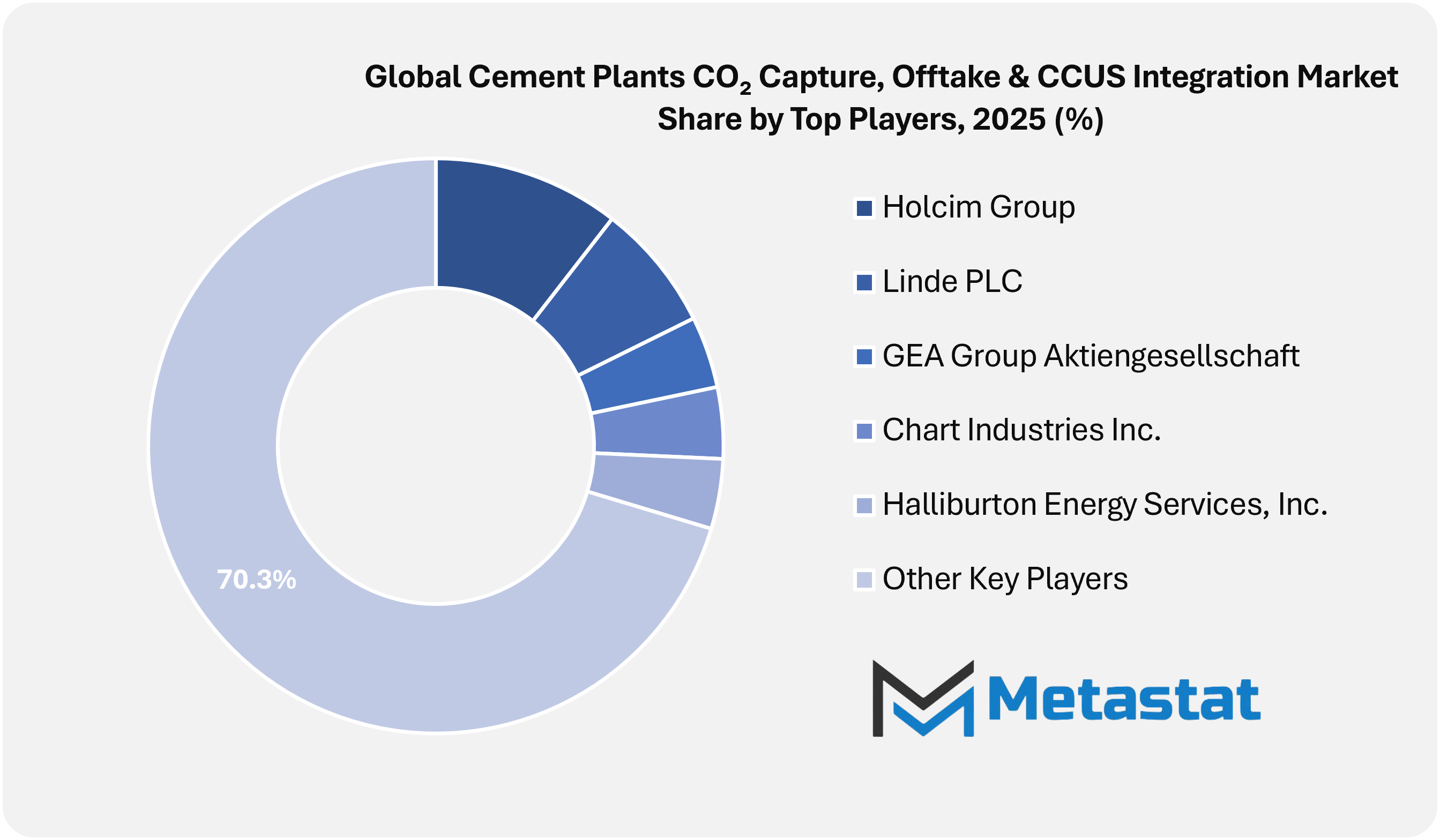

Competitive Landscape and Strategic Insights

The Global Cement Plants CO₂ Capture, Offtake & CCUS Integration Market is gaining strategic importance as the cement industry faces increasing pressure to reduce carbon emissions from both fuel combustion and clinker production processes. With sustainability targets becoming more stringent across global construction and industrial sectors, cement manufacturers are actively evaluating carbon capture, transport, utilization, and storage solutions to lower their environmental footprint while sustaining production efficiency.

Technology providers and engineering companies play a central role in advancing this market. Players such as Holcim Group and Carbon Clean are supporting deployment of capture systems within cement plant operations, while Linde plc and Chart Industries, Inc. provide gas processing, liquefaction, and handling technologies that facilitate efficient CO₂ management. Calix Limited and GEA Group Aktiengesellschaft are also contributing through process technologies designed to improve thermal efficiency and reduce carbon intensity during cement manufacturing.

Energy service companies and industrial technology providers are further strengthening market development. SLB Capturi, Carbon Capture America, Inc., and Halliburton Energy Services, Inc. offer expertise in large-scale capture systems, subsurface storage, and carbon management infrastructure. Honeywell International Inc. and KSB Limited support the market through automation systems, pumps, and plant equipment required for safe and efficient CO₂ handling across integrated industrial environments.

Industrial gas companies and infrastructure specialists will expand their role as cement producers seek reliable partners for CO₂ transport, storage, and utilization. Air Products and Chemicals, Inc. continues to invest in infrastructure capabilities that support long-term carbon movement and industrial reuse. As regulatory pressure intensifies and decarbonization targets strengthen, collaboration between cement manufacturers, technology developers, and infrastructure operators will remain a defining feature of the competitive landscape.

Forecast and Future Outlook

Market size is forecast to rise from USD 128.7 million in 2025 to over USD 236.4 million by 2033.

Digitalization is expected to become increasingly important in supporting emissions accounting, offtake coordination, storage verification, and regulatory compliance. As carbon management becomes more embedded within plant strategy, coordination between engineering teams, infrastructure partners, carbon buyers, and regulatory authorities will shape the next phase of market development.

This research report categorizes the Cement Plants CO₂ Capture, Offtake & CCUS Integration market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Cement Plants CO₂ Capture, Offtake & CCUS Integration market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Cement Plants CO₂ Capture, Offtake & CCUS Integration market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 7.9% from 2026 to 2033

Revenue Unit

USD million

Segmentation

By Carbon Capture Technologies, Application, and Region

By Region

North America (By Carbon Capture Technologies, Application, and Country)

United States

Canada

Mexico

Europe (By Carbon Capture Technologies, Application, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Carbon Capture Technologies, Application, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Carbon Capture Technologies, Application, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Carbon Capture Technologies, Application, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Prepositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Top players operating in the Cement Plants CO₂ Capture, Offtake & CCUS Integration industry include Holcim Group, Carbon Clean, Linde PLC, Chart Industries Inc., Calix Limited, GEA Group Aktiengesellschaft, and SLB Capturi.

Global Cement Plants CO₂ Capture, Offtake & CCUS Integration market is estimated to reach USD 236.4 million by 2033.

High capital expenditure for capture units, compression infrastructure, and transport pipelines limits large-scale adoption among smaller cement producers will hamper the market growth within the forecast period.

North America region dominates the market.

Rising carbon pricing frameworks and industrial decarbonization mandates accelerate deployment of CO₂ capture and CCUS systems across cement manufacturing facilities and strategic partnerships between cement producers, energy firms, and infrastructure developers expand CO₂ transport networks and industrial-scale storage projects are key driving factors, boosting the market.

The Global Cement Plants CO₂ Capture, Offtake & CCUS Integration market is expected to grow at a CAGR of 7.9% over the forecast period (2026-2033).

The Post-Combustion Solvent Capture is the leading type segment in the Global market.

The Metastat Insights analysis shows that the North America Cement Plants CO₂ Capture, Offtake & CCUS Integration market size is estimated to be USD 73.8 million by 2033.

The Metastat Insights study shows that the Global Cement Plants CO₂ Capture, Offtake & CCUS Integration market size was USD 128.7 million in 2025.

Lubricants Manufacturing market size is valued at USD 151.1 billion in 2025 and projected to reach USD 208.4 billion by 2033, growing at a CAGR of 4.1%.

Vapor Degreasing Solvent market size is valued at USD 1,004.1 million in 2025 and projected to reach USD 1,576.4 million by 2033, growing at a CAGR of 5.8%.

Bangladesh Flavours and Fragrances Market Size, Share, Trends, 2033

Bangladesh Flavours and Fragrances market size is valued at USD 793.9 million in 2025 and is projected to reach USD 1,447.9 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Bangladesh Flavours and Fragrances Market, Bangladesh Flavours and Fragrances Market Size, Bangladesh Flavours and Fragrances Market Share, Bangladesh Flavours and Fragrances Market Analysis, Bangladesh Flavours and Fragrances Market Growth, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market Research Report, Bangladesh Flavours and Fragrances Market Forecast, Bangladesh Flavours and Fragrances, Bangladesh Flavours and Fragrances Market Research, Bangladesh Flavours and Fragrances Industry, Bangladesh Flavours and Fragrances Industry Report, Bangladesh Flavours and Fragrances Market Data, Bangladesh Flavours and Fragrances Statistics, Bangladesh Flavours and Fragrances Market Statistics, Bangladesh Flavours and Fragrances Industry Trends, Bangladesh Flavours and Fragrances Market Report, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market News, Bangladesh Flavours and Fragrances Forecasts, Bangladesh Flavours and Fragrances Market Intelligence Report

Biocatalysis and Enzyme Biocatalysts Market Size, Share, Trends, 2033

Biocatalysis and Enzyme Biocatalysts market size is valued at USD 737.8 million in 2025 and is projected to reach USD 1,221.0 million in 2033, at a CAGR of 6.5% from 2026 to 2033.

Biocatalysis and Enzyme Biocatalysts Market, Biocatalysis and Enzyme Biocatalysts Market Size, Biocatalysis and Enzyme Biocatalysts Market Share, Biocatalysis and Enzyme Biocatalysts Market Analysis, Biocatalysis and Enzyme Biocatalysts Market Growth, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market Research Report, Biocatalysis and Enzyme Biocatalysts Market Forecast, Biocatalysis and Enzyme Biocatalysts, Biocatalysis and Enzyme Biocatalysts Market Research, Biocatalysis and Enzyme Biocatalysts Industry, Biocatalysis and Enzyme Biocatalysts Industry Report, Biocatalysis and Enzyme Biocatalysts Market Data, Biocatalysis and Enzyme Biocatalysts Statistics, Biocatalysis and Enzyme Biocatalysts Market Statistics, Biocatalysis and Enzyme Biocatalysts Industry Trends, Biocatalysis and Enzyme Biocatalysts Market Report, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market News, Biocatalysis and Enzyme Biocatalysts Forecasts, Biocatalysis and Enzyme Biocatalysts Market Intelligence Report