LFP Cathode Material Market Size, Share, By Type (Nano-LFP Cathode Material and Common-LFP Cathode Material), By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, Power Tools, and Others), By End User (Automotive, Electronics, Energy Sector, Industrial, and Aerospace), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4743

Published

May 19, 2026

Pages

316 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

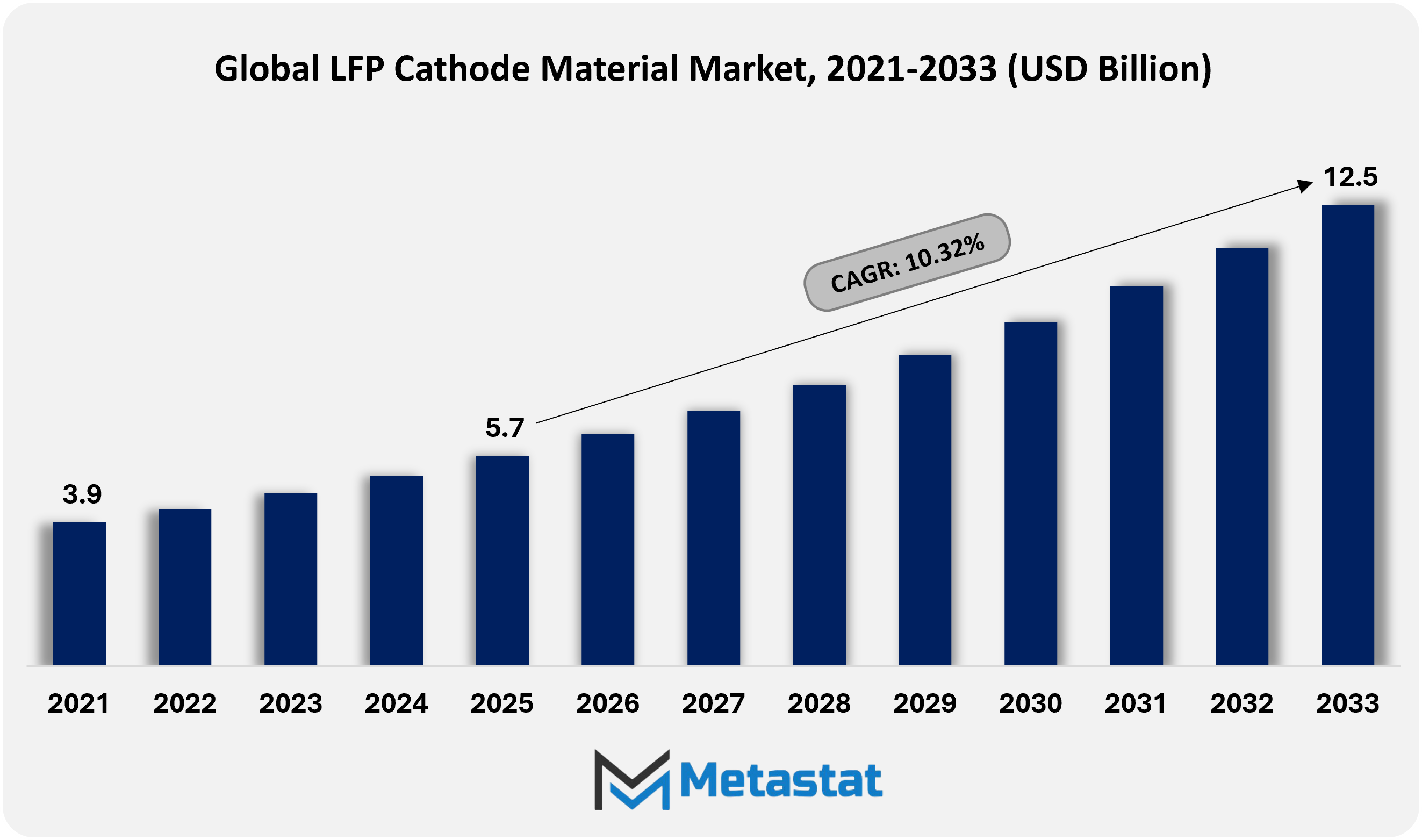

Global LFP Cathode Material market size is valued at USD 5.7 billion in 2025 and projected to grow at a CAGR of 10.3% during the forecast period, reaching USD 12.5 billion by 2033.

Global LFP Cathode Material Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global LFP Cathode Material market valued at USD 5.7 billion in 2025, growing at a CAGR of 10.3% through 2033, with potential to exceed USD 12.5 billion.

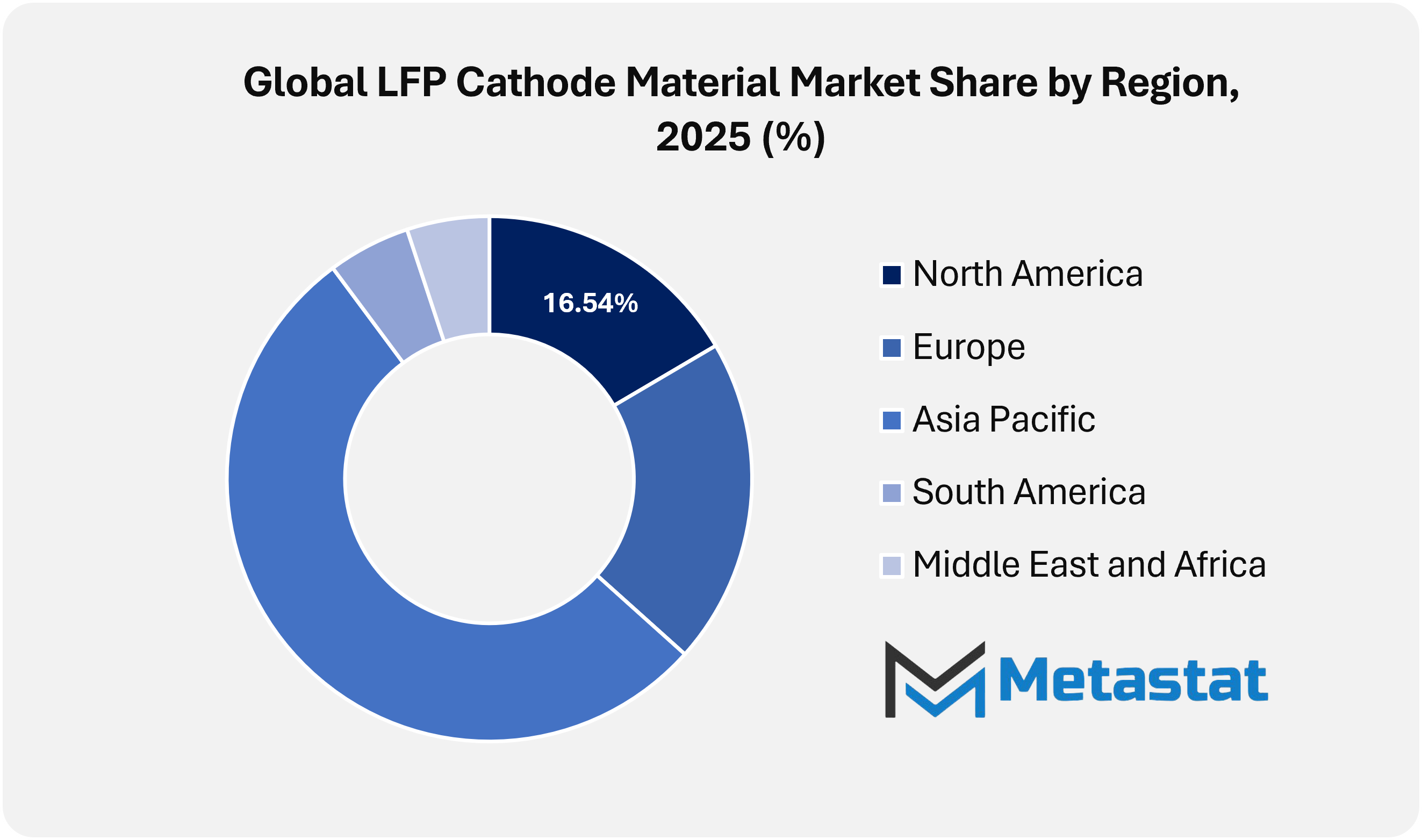

North America accounts for 16.5% of the market in 2025, with the United States holding the leading share within the region.

Nano-LFP Cathode Material segment accounts for a market share of 39.5% in 2026.

Key trends driving growth: Rapid EV adoption and large-scale grid storage deployments propel demand for cost-efficient and thermally stable LFP battery chemistry, along with strategic shift toward cobalt-free and low-cost battery chemistries supports accelerated LFP production capacity expansion.

Opportunities include expansion of stationary energy storage projects and entry of global OEMs into LFP platforms create strong long-term commercialization potential.

Key insight: Rapid EV penetration and grid-scale storage expansion position the Global LFP Cathode Material Market for strong volume growth driven by cost efficiency and safety advantages.

The Global LFP Cathode Material Market operates within the lithium-ion battery materials industry, where electrochemical performance, supply security, and cost competitiveness define strategic positioning. Over the forecast period, the market will move beyond capacity additions and volume targets toward stronger sourcing alignment, deeper vertical integration, and improved technology optimization. Producers are increasingly integrating upstream iron phosphate processing with lithium refining to improve margin stability and secure long-term supply agreements with cell manufacturers.

Manufacturers are focusing on particle morphology engineering, surface coating optimization, and nano-structuring techniques to improve ionic conductivity without compromising thermal stability. These advances support next-generation battery architectures designed for high-cycle applications in grid storage, industrial mobility fleets, and two- and three-wheeler electrification across developing economies. The safety profile of LFP chemistry is also supporting broader adoption in stationary energy storage projects, where predictable degradation patterns and operating reliability are prioritized over peak energy density.

Market Dynamics

Growth Drivers:

Rapid EV adoption and large-scale grid storage deployments propel demand for cost-efficient and thermally stable LFP battery chemistry.

Rising electric vehicle penetration across passenger and commercial segments is increasing demand for cost-effective battery systems. Grid-scale energy storage expansion linked to renewable integration is further strengthening reliance on stable battery chemistries. The Global LFP Cathode Material Market is gaining traction owing to strong safety performance, long cycle life, and improved cost predictability supporting mass electrification targets.

Strategic shift toward cobalt-free and low-cost battery chemistries supports accelerated LFP production capacity expansion.

Battery manufacturers are shifting toward cobalt-free formulations to reduce exposure to ethical sourcing concerns and volatile metal prices. Production facilities are expanding across multiple regions to strengthen supply continuity. The Global LFP Cathode Material Market is benefiting from localization strategies, vertical integration initiatives, and process improvements that enhance yield efficiency and material consistency.

Restraints and Challenges:

Lower energy density compared to NMC and NCA chemistries limits adoption in long-range premium EV segments.

Lower energy density remains a key limitation for LFP chemistry in high-performance electric vehicles requiring extended driving range. Premium automakers focused on compact battery packs and higher mileage will continue favoring alternative chemistries. The Global LFP Cathode Material Market will witness slower penetration in luxury EV segments despite ongoing improvements in cell-to-pack architecture and structural battery design.

Price volatility of lithium carbonate and supply chain concentration in key raw material processing regions impacts margin stability.

Volatility in lithium carbonate pricing creates uncertainty in production planning and long-term contracting. Concentration of raw material processing in selected geographies increases exposure to trade policy shifts and logistical bottlenecks. Participants in the Global LFP Cathode Material Market are therefore prioritizing upstream partnerships, localization, and recycling integration to improve margin stability and material security.

Opportunities:

Expansion of stationary energy storage projects and entry of global OEMs into LFP platforms create strong long-term commercialization potential.

Utility-scale renewable energy projects require durable battery systems capable of supporting extended operating cycles. The entry of major automotive OEMs into LFP-based platforms is also validating the chemistry across mass-market vehicle categories. The Global LFP Cathode Material Market will witness sustained commercialization momentum supported by policy incentives, electrification programs, and infrastructure modernization.

Market Segmentation Analysis

The Global LFP Cathode Material market is classified based on Type, Application, End User.

By Type, the market is further segmented into:

Nano-LFP Cathode Material

Nano-LFP Cathode Material segment is valued at USD 2.5 billion in 2026 and is projected to reach USD 5.7 billion by 2033, at a CAGR of 12.6% during the forecast period.

Nano-LFP Cathode Material will witness stronger adoption owing to improved conductivity, faster ion transfer, and better thermal stability. Advanced battery manufacturers are increasingly using nano-structured particles to improve charging efficiency and lifecycle performance. Future production strategies will focus on cost control, uniform particle distribution, and scalable synthesis methods to support expanding electrification demand.

Common-LFP Cathode Material

Common-LFP Cathode Material segment is valued at USD 3.8 billion in 2026 and is projected to reach USD 6.8 billion by 2033, at a CAGR of 8.7% during the forecast period.

Common-LFP Cathode Material will maintain steady demand owing to affordability and reliable electrochemical performance. Large-scale battery plants will continue using conventional formulations for applications requiring durability and safety. Manufacturing optimization, localized supply chains, and material recycling initiatives will strengthen long-term viability across mid-range electric mobility and stationary storage applications.

By Application, the market is divided into:

Electric Vehicles

Electric Vehicles segment is projected to reach USD 6.6 billion by 2033, at a CAGR of 12% during the forecast period.

Electric Vehicles will remain the leading application in the Global LFP Cathode Material Market owing to safety benefits, long cycle life, and lower dependence on expensive metals. Automotive battery systems are increasingly adopting LFP chemistry to support mass-market electrification goals. Expansion of charging infrastructure, fleet electrification programs, and government-backed emission reduction policies will continue to accelerate material consumption.

Energy Storage Systems

Energy Storage Systems segment is projected to reach USD 3.1 billion by 2033, at a CAGR of 11.6% during the forecast period.

Energy Storage Systems will expand material consumption in the Global LFP Cathode Material Market through grid balancing, renewable integration, and backup power applications. Utility-scale storage installations increasingly rely on LFP chemistry owing to thermal safety and long lifecycle performance. Rising renewable capacity additions and the growth of decentralized energy networks will support steady procurement of cathode materials over the forecast period.

Consumer Electronics

Consumer Electronics segment is projected to reach USD 1.4 billion by 2033, at a CAGR of 6.5% during the forecast period.

Consumer Electronics will generate moderate growth in the Global LFP Cathode Material Market, particularly in devices where battery longevity and operational safety are important. Manufacturers are evaluating LFP integration in portable devices where thermal control and recharge stability remain critical. Cost-effective battery modules designed for extended usage cycles will gradually support adoption across selected electronics categories.

Power Tools

Power Tools segment is projected to reach USD 0.8 billion by 2033, at a CAGR of 6.6% during the forecast period.

Power Tools will create targeted opportunities in the Global LFP Cathode Material Market through demand for durable and fast-charging battery packs. Industrial-grade tools benefit from improved thermal resistance and reliable discharge performance. Growth in construction activity and professional equipment upgrades will sustain cathode material demand in high-drain operating environments.

Others

Others segment is projected to reach USD 0.5 billion by 2033, at a CAGR of 3.7% during the forecast period.

Other applications include marine systems, backup mobility devices, and small-scale transport solutions. Specialized battery modules designed for safety and reliability will incorporate LFP chemistry in these use cases. Product diversification strategies and niche electrification programs will gradually broaden the application scope of the market.

By End User, the market is further divided into:

Automotive

Automotive segment is projected to reach USD 7.0 billion by 2033.

Automotive end users will account for significant consumption in the Global LFP Cathode Material Market owing to rising electric vehicle production volumes. Battery cell manufacturing facilities are expanding capacity to meet regulatory emission targets and growing consumer adoption. Strategic investments in localized battery ecosystems will strengthen supply security and long-term procurement stability.

Electronics

Electronics segment is projected to reach USD 1.8 billion by 2033.

Electronics manufacturers in the Global LFP Cathode Material Market are prioritizing battery safety, longer lifecycle, and cost efficiency. Portable equipment, smart devices, and backup systems will adopt LFP-based batteries to reduce overheating risk. Gradual innovation in compact battery pack design will support continued integration across multiple electronics product lines.

Energy Sector

Energy Sector segment is projected to reach USD 2.3 billion by 2033.

Energy Sector participants are increasing their engagement in the Global LFP Cathode Material Market to stabilize renewable power supply and improve grid resilience. Utility operators are deploying LFP-based storage units for peak shaving and load balancing applications. Long-term energy transition programs will continue to support procurement momentum across public and private infrastructure projects.

Industrial

Industrial segment is projected to reach USD 0.9 billion by 2033.

Industrial operations will contribute to the Global LFP Cathode Material Market through adoption in heavy equipment, warehouse automation, and backup systems. Demand for reliable and low-maintenance battery solutions is increasing the integration of LFP chemistry in industrial mobility applications. Expansion of automation and electrified machinery upgrades will further support future material demand.

Aerospace

Aerospace segment is projected to reach USD 0.5 billion by 2033.

Aerospace applications will focus on safety-oriented energy storage solutions for auxiliary systems and lightweight ground operations equipment. Research initiatives are working to improve energy density while maintaining stable thermal performance. Gradual electrification of support vehicles and onboard backup systems will support specialized cathode material development.

By Region:

Based on geography, the Global LFP Cathode Material market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America LFP Cathode Material Market is set to expand at a CAGR of 10.3% within the forecast period, reaching a market size (TAM) of USD 1.8 billion by the end of 2033.

In North America, rising electric vehicle production and domestic battery gigafactory investments are strengthening demand across the LFP Cathode Material Market.

In Europe, decarbonization targets, battery value chain localization, and increasing deployment of energy storage systems are supporting LFP cathode material adoption.

In Asia Pacific, fast expansion of electricity storage systems and cost-centered EV manufacturing is creating large-scale opportunities in the LFP Cathode Material Market.

Across the Middle East, Africa, and South America, rising renewable electricity integration, mining quarter improvement, and early-degree EV adoption are step by step positioning the LFP Cathode Material Market for long-term expansion.

Competitive Landscape and Strategic Insights

The Global LFP Cathode Material Market is expanding steadily as demand for lithium iron phosphate batteries rises across electric vehicles, energy storage systems, and selected electronics applications. LFP chemistry is widely valued for its thermal stability, long cycle life, and cost efficiency compared with several other lithium-ion chemistries. As governments promote cleaner mobility and manufacturers focus on safer battery platforms, production capacity for LFP cathode materials will increase further. The shift toward localized battery supply chains in Asia, Europe, and North America is also supporting investment in processing facilities and raw material sourcing.

China remains the dominant manufacturing base, with companies such as Ronbay Technology Co., Ltd. and Hunan Yuneng New Energy Battery Material Co., Ltd. playing a major role in scaling production. Firms including Shenzhen Dynanonic Co., Ltd. and Jiangsu Lopal Tech Co., Ltd. continue to strengthen supply capabilities through technology upgrades and partnerships with battery manufacturers. Other notable participants such as Guizhou Anda Technology Energy Co., Ltd. and Hubei Wanrun New Energy Technology Co., Ltd. are expanding production lines to meet growing domestic and export demand. Their strategies are focused on improving material performance while maintaining cost competitiveness.

Additional Chinese producers such as Beijing Pulead Technology Industry Co., Ltd., Fulin Precision Co., Ltd., and Gotion High-Tech Co., Ltd. are investing in research to improve material performance. Companies including Chongqing Terui Battery Materials Co., Ltd. and Xiamen Tungsten New Energy Materials Co., Ltd. are focusing on production efficiency and vertical integration. Meanwhile, China Minmetals New Energy Materials (Hunan) Co., Ltd. and Wanhua Chemical Group Co., Ltd. are strengthening raw material supply linkages. Shandong Fengyuan Chemical Co., Ltd. and Yibin Tianyuan Group Co., Ltd. also contribute to market expansion through material processing expertise.

Outside China, global chemical and advanced materials companies are expanding their presence in the market. BASF SE is developing cathode materials with a focus on sustainability and localized supply in Europe. IBU-tec advanced materials AG and IBUvolt GmbH are building LFP manufacturing capabilities to support European cell manufacturers. Companies such as Aleees and Prayon SA are contributing technical expertise in phosphate-based materials. In North America, firms such as Nano One Materials Corp. and 6K Energy are advancing process innovation to improve cost efficiency and reduce environmental impact.

A broader set of specialty chemical and supply companies also participates in the market ecosystem. Himadri Speciality Chemical Ltd and Allox Group are supporting supply linkages for raw inputs and processing solutions. Distributors and research-focused firms such as Targray Technology International Inc., American Elements, MTI Corporation, MSE Supplies LLC, Ossila Ltd, NEI Corporation, Stanford Advanced Materials, and SkySpring Nanomaterials Inc. support research laboratories and pilot-scale manufacturing worldwide. As battery demand rises across electric mobility and grid storage, these companies will continue to strengthen supply networks and technology standards across the Global LFP Cathode Material Market.

Forecast and Future Outlook

Market size is forecast to rise from USD 5.7 billion in 2025 to over USD 12.5 billion by 2033.

Technological competition with high-nickel chemistries will remain strong, yet LFP is expected to secure a strategic position in entry-level electric vehicles, commercial fleets, and mass-market energy storage. By the end of the forecast period, the Global LFP Cathode Material Market is expected to be defined by disciplined capital deployment, vertical integration, and performance-driven customization aligned with differentiated end-use requirements.

This research report categorizes the LFP Cathode Material market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the LFP Cathode Material market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the LFP Cathode Material market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 10.3% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Kilotons

Segmentation

By Type, Application, End User, and Region

By Type

Nano-LFP Cathode Material

Common-LFP Cathode Material

By Application

Electric Vehicles

Energy Storage Systems

Consumer Electronics

Power Tools

Others

By End User

Automotive

Electronics

Energy Sector

Industrial

Aerospace

By Region

North America (By Type, Application, End User, and Country)

United States

Canada

Mexico

Europe (By Type, Application, End User, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Type, Application, End User, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Type, Application, End User, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Type, Application, End User, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Bangladesh Flavours and Fragrances Market Size, Share, Trends, 2033

Bangladesh Flavours and Fragrances market size is valued at USD 793.9 million in 2025 and is projected to reach USD 1,447.9 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Bangladesh Flavours and Fragrances Market, Bangladesh Flavours and Fragrances Market Size, Bangladesh Flavours and Fragrances Market Share, Bangladesh Flavours and Fragrances Market Analysis, Bangladesh Flavours and Fragrances Market Growth, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market Research Report, Bangladesh Flavours and Fragrances Market Forecast, Bangladesh Flavours and Fragrances, Bangladesh Flavours and Fragrances Market Research, Bangladesh Flavours and Fragrances Industry, Bangladesh Flavours and Fragrances Industry Report, Bangladesh Flavours and Fragrances Market Data, Bangladesh Flavours and Fragrances Statistics, Bangladesh Flavours and Fragrances Market Statistics, Bangladesh Flavours and Fragrances Industry Trends, Bangladesh Flavours and Fragrances Market Report, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market News, Bangladesh Flavours and Fragrances Forecasts, Bangladesh Flavours and Fragrances Market Intelligence Report

Biocatalysis and Enzyme Biocatalysts Market Size, Share, Trends, 2033

Biocatalysis and Enzyme Biocatalysts market size is valued at USD 737.8 million in 2025 and is projected to reach USD 1,221.0 million in 2033, at a CAGR of 6.5% from 2026 to 2033.

Biocatalysis and Enzyme Biocatalysts Market, Biocatalysis and Enzyme Biocatalysts Market Size, Biocatalysis and Enzyme Biocatalysts Market Share, Biocatalysis and Enzyme Biocatalysts Market Analysis, Biocatalysis and Enzyme Biocatalysts Market Growth, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market Research Report, Biocatalysis and Enzyme Biocatalysts Market Forecast, Biocatalysis and Enzyme Biocatalysts, Biocatalysis and Enzyme Biocatalysts Market Research, Biocatalysis and Enzyme Biocatalysts Industry, Biocatalysis and Enzyme Biocatalysts Industry Report, Biocatalysis and Enzyme Biocatalysts Market Data, Biocatalysis and Enzyme Biocatalysts Statistics, Biocatalysis and Enzyme Biocatalysts Market Statistics, Biocatalysis and Enzyme Biocatalysts Industry Trends, Biocatalysis and Enzyme Biocatalysts Market Report, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market News, Biocatalysis and Enzyme Biocatalysts Forecasts, Biocatalysis and Enzyme Biocatalysts Market Intelligence Report

Malaysia Tyre Pyrolysis Products Market Size, Share, Trends, 2033

Malaysia Tyre Pyrolysis Products market size is valued at USD 205.9 million in 2025 and is projected to reach USD 421.8 million in 2033, at a CAGR of 9.3% from 2026 to 2033.

Malaysia Tyre Pyrolysis Products Market, Malaysia Tyre Pyrolysis Products Market Size, Malaysia Tyre Pyrolysis Products Market Share, Malaysia Tyre Pyrolysis Products Market Analysis, Malaysia Tyre Pyrolysis Products Market Growth, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market Research Report, Malaysia Tyre Pyrolysis Products Market Forecast, Malaysia Tyre Pyrolysis Products, Malaysia Tyre Pyrolysis Products Market Research, Malaysia Tyre Pyrolysis Products Industry, Malaysia Tyre Pyrolysis Products Industry Report, Malaysia Tyre Pyrolysis Products Market Data, Malaysia Tyre Pyrolysis Products Statistics, Malaysia Tyre Pyrolysis Products Market Statistics, Malaysia Tyre Pyrolysis Products Industry Trends, Malaysia Tyre Pyrolysis Products Market Report, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market News, Malaysia Tyre Pyrolysis Products Forecasts, Malaysia Tyre Pyrolysis Products Market Intelligence Report

Near Infrared (NIR) Analyzer Market Size, Share, Trends, 2033

Near Infrared (NIR) Analyzer market size is valued at USD 855.3 million in 2025 and is projected to reach USD 1,813.6 million in 2033, at a CAGR of 9.9% from 2026 to 2033.

Near Infrared (NIR) Analyzer Market, Near Infrared (NIR) Analyzer Market Size, Near Infrared (NIR) Analyzer Market Share, Near Infrared (NIR) Analyzer Market Analysis, Near Infrared (NIR) Analyzer Market Growth, Near Infrared (NIR) Analyzer Market Trends, Near Infrared (NIR) Analyzer Market Research Report, Near Infrared (NIR) Analyzer Market Forecast, Near Infrared (NIR) Analyzer, Near Infrared (NIR) Analyzer Market Research, Near Infrared (NIR) Analyzer Industry, Near Infrared (NIR) Analyzer Industry Report, Near Infrared (NIR) Analyzer Market Data, Near Infrared (NIR) Analyzer Statistics, Near Infrared (NIR) Analyzer Market Statistics, Near Infrared (NIR) Analyzer Industry Trends, Near Infrared (NIR) Analyzer Market Report, Near Infrared (NIR) Analyzer Market Trends, Near Infrared (NIR) Analyzer Market News, Near Infrared (NIR) Analyzer Forecasts, Near Infrared (NIR) Analyzer Market Intelligence Report