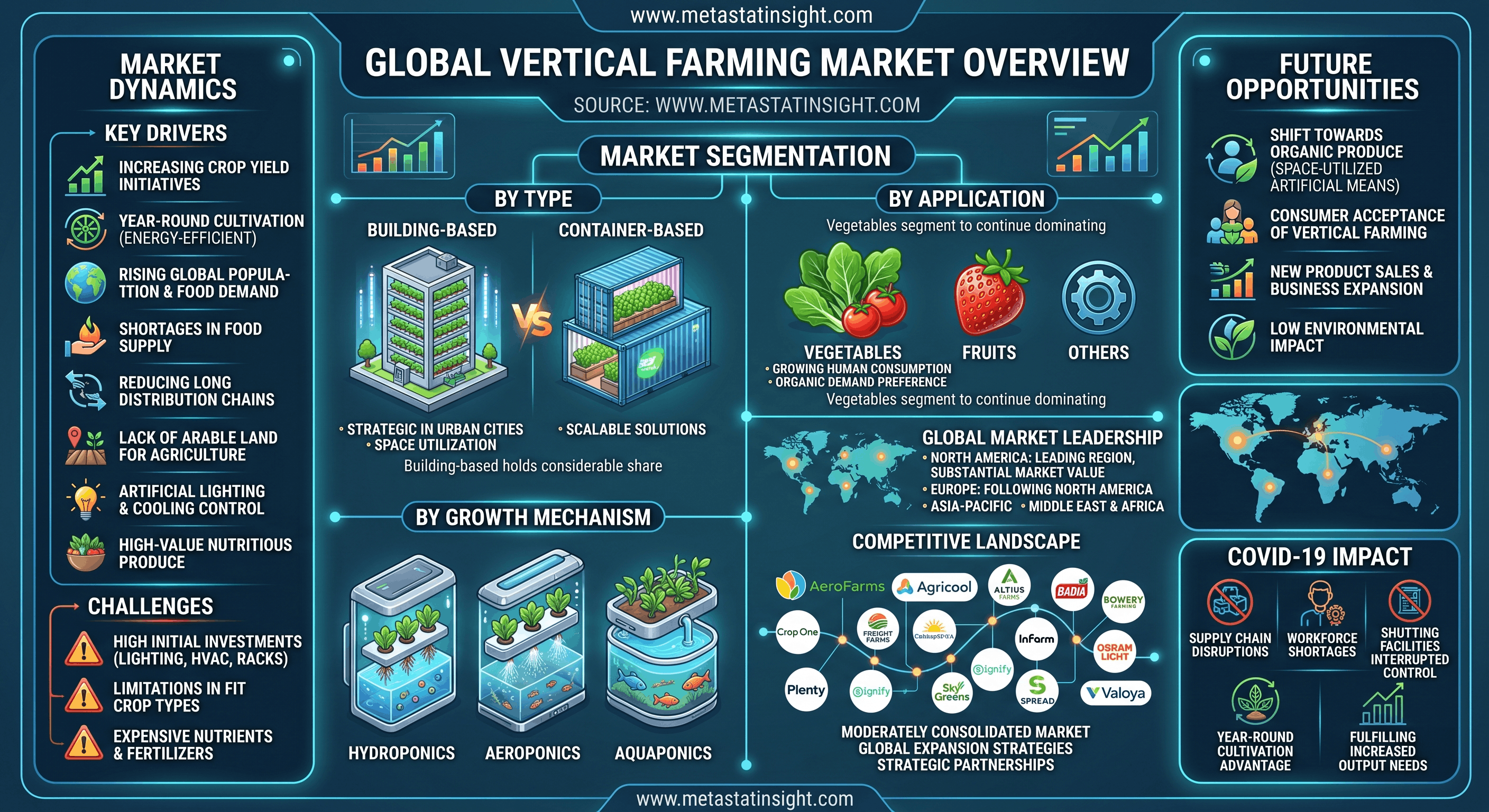

MetaStat Insight has released its comprehensive market assessment of the Global Vertical Farming Market. The study outlines how the agricultural sector is shifting from traditional land-dependent practices toward indoor, climate-controlled environments. Driven by a rising global population and diminishing arable land, vertical farming offers a strategic pathway to secure year-round crop production directly within urban centers.

Strategic Optimization of Controlled Environments

Vertical farming restructures agricultural cultivation into vertically stacked layers inside indoor spaces and buildings. By utilizing artificial lighting and cooling systems, this approach guarantees high-yield, year-round production of conventional crops, insulating them from external weather limitations.

Urbanization and global supply chain vulnerabilities are compelling corporations to seek innovative answers. Establishing vertical farms near city centers helps companies bypass the heavy capital expenditures associated with long distribution chains, offering an immediate remedy to localized food shortages.

Structural Breakdown of the Industry

The MetaStat Insight study categorizes the market landscape into three vital structural segments:

-

By Type: Split into Building-based and Container-based frameworks. Building-based facilities hold a prominent market share due to their multi-story architecture, which dramatically expands cultivation surface areas near dense consumer populations.

-

By Application: Divided into Vegetables, Fruits, and Others. The vegetables segment maintains absolute market dominance, propelled by baseline human dietary needs and a clear consumer preference shifting toward indoor-grown organic produce.

-

By Growth Mechanism: Classified into Hydroponics, Aeroponics, and Aquaponics, representing the foundational soilless systems used to sustain stacked growth.

Navigating Capital Headwinds and Market Opportunities

The initial setup of an indoor farm requires significant capital for heavy-duty HVAC frameworks, specialized shelving, and complex artificial lighting. Ongoing spending on specialized mineral nutrients and organic fertilizers can elevate consumer pricing, presenting a temporary barrier to mainstream market expansion. Furthermore, the market faces biological constraints regarding the specific types of crops currently compatible with stacked farming.

However, a cultural shift provides a lucrative landscape for industry vendors. Modern consumers are increasingly open to food grown via space-utilized artificial methods, valuing its minimal environmental impact. This growing acceptance unlocks critical avenues for product sales and business growth.

Regional Footprint and Competitive Outlook

Geographically, the market covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. North America leads the industry with a substantial share of overall market value, closely followed by Europe.

The competitive landscape is moderately consolidated, with expansive global players capitalizing on high-demand regions. High entry costs deter new competitors, allowing established companies to strengthen their presence via geographic facility expansions and strategic corporate partnerships. Key participants profiled include AeroFarms, LLC, Agricool, Altius Farms, Badia Farms, Bowery Farming, Crop One, Freight Farms, Heliospectra, InFarm, Osram Licht, Plenty, Signify, Sky Greens, SPREAD, and Valoya.