Automotive Battery Management System Testing Market Size, Share, By Battery Type (Lithium-ion, Lead-acid, Nickel-based, and Others), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Battery Electric Vehicles, and Others), By Testing Type (Hardware-in-the-Loop (HIL) Test System, Software-in-the-Loop Testing, Functional Testing, Safety Testing, Fault Injection Testing, and Others), By End User (Automotive OEMs, Tier-1 BMS Suppliers, Battery Pack Integrators, Cell manufacturers, Module Manufacturers, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4578

Published

April 8, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

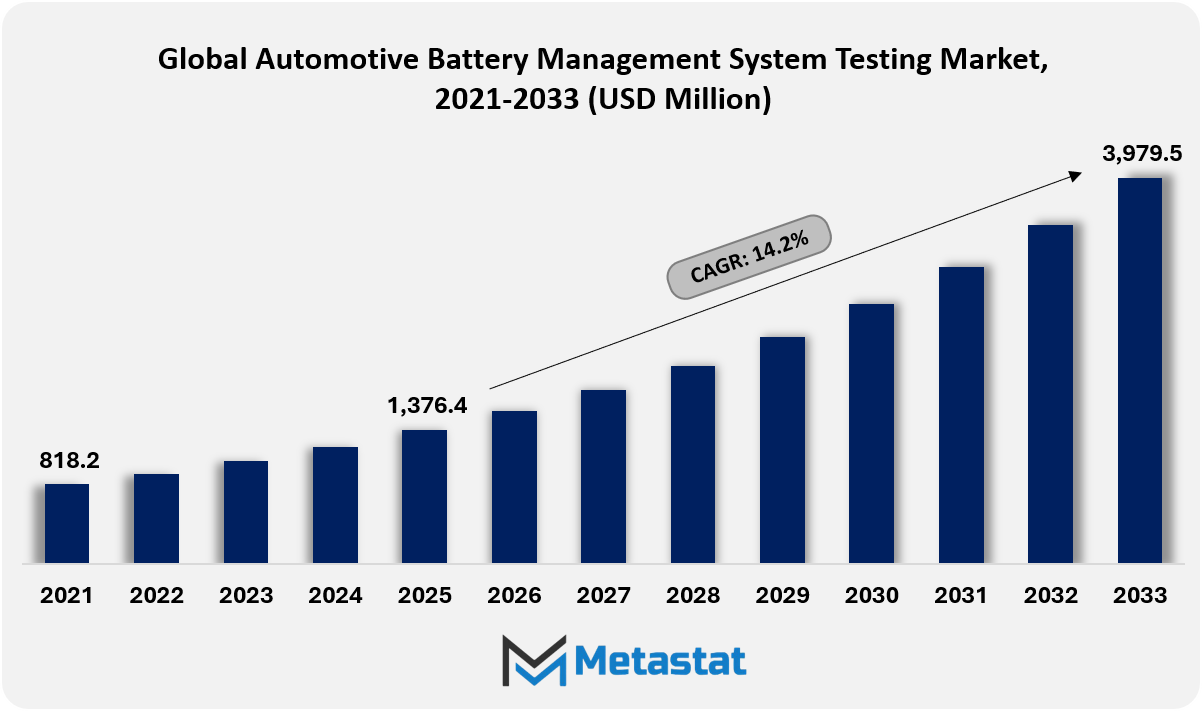

The global automotive battery management system testing market was valued at USD 1,376.4 million in 2025. The market is projected to grow from USD 1,570.4 million in 2026 to USD 3,979.5 million by 2033, registering a CAGR of 14.2% during 2026-2033.

Global Automotive Battery Management System Testing Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

The global automotive battery management system testing market was valued at USD 1,376.4 million in 2025 and is projected to reach USD 3,979.5 million by 2033, reflecting a CAGR of 14.2% during 2026-2033.

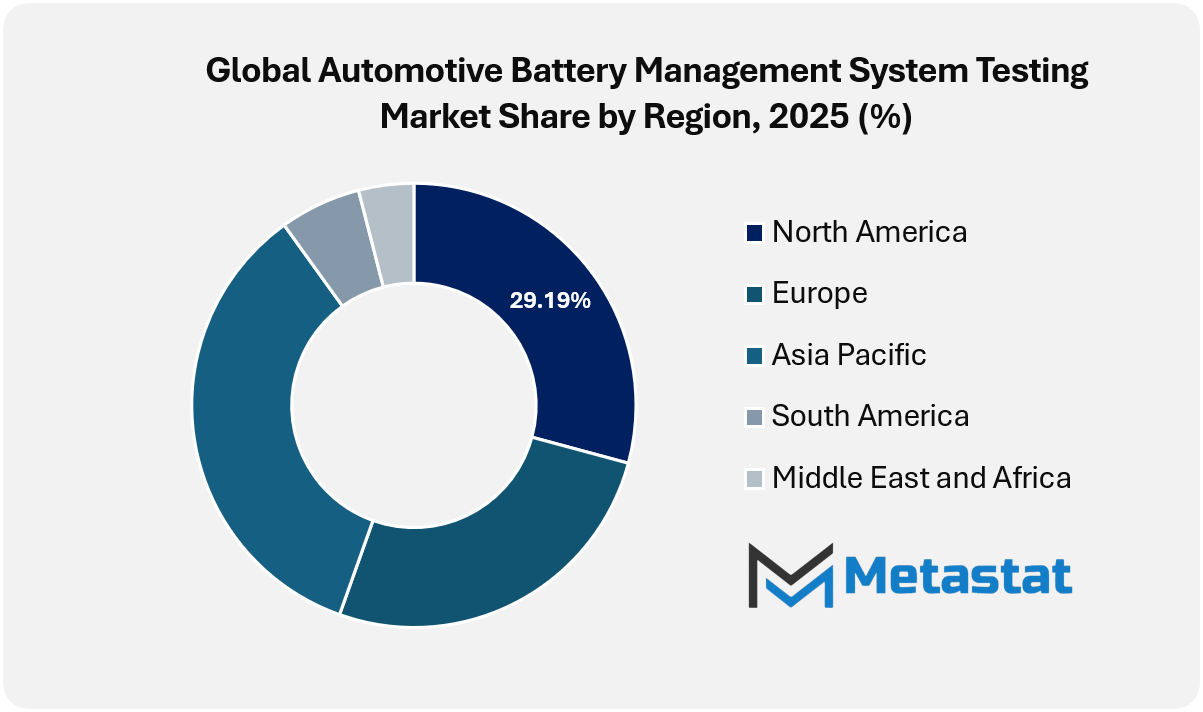

North America accounted for 29.2% of the market in 2025, led by the United States.

Lithium-ion segment accounted for a market share of 79.6% in 2025.

Key trends driving growth include rapid growth of electric and hybrid vehicles, increasing the need for robust BMS validation, and stringent automotive safety and regulatory standards, driving comprehensive battery testing.

Opportunities include the rising adoption of next-generation batteries, creating demand for advanced and automated BMS testing solutions.

Key insight: The global automotive battery management system testing market is propelled by electric vehicle expansion and tightening regulations, while advanced battery innovation sustains long-term testing opportunities amid cost and standardization challenges.

The global automotive battery management system testing market within the automotive testing and verification industry will move beyond traditional verification boundaries and shape how electric mobility platforms will be engineered, audited and certified at the system level. Future activity will extend beyond cell balancing accuracy and voltage monitoring assurance and will expand into behavior prediction under non-ideal operating conditions shaped by autonomous driving, bidirectional charging, and software-defined vehicle architectures.

The test framework will increasingly address cross-domain interactions where battery intelligence will communicate with thermal controls, power electronics and vehicle operating systems in real time. The simulation environment will expand to replicate extreme edge cases such as asynchronous sensor drift, cyber-induced signal noise, and long-term degradation patterns that emerge after years of mixed-duty cycles. Verification protocols will evolve toward probabilistic modeling rather than deterministic pass or fail logic, enabling manufacturers to estimate the probability of failure rather than merely confirm functional compliance.

Market Dynamics

Growth Drivers:

Rapid growth of electric and hybrid vehicles increasing the need for robust BMS validation.

Rapid growth of electric and hybrid mobility will accelerate technical expectations across the global automotive battery management system testing market. Future automobile structures depend upon battery tracking to ensure efficiency, durability, and safety. Comprehensive validation processes will improve performance consistency across operating conditions and usage patterns.

Stringent automotive safety and regulatory standards driving comprehensive battery testing.

Tightening safety frameworks and regulatory oversight are raising test rigor across automotive battery systems. Forward-looking compliance requirements will call for rigorous verification across thermal management, fault detection, and lifecycle durability. Structured testing protocols will strengthen manufacturer credibility while supporting market access across regulated automotive markets.

Restraints and Challenges:

High testing costs and complexity due to advanced battery chemistries and architectures.

Advanced battery chemistries and complex system architectures increase operational burdens within testing environments. High capital investment, extended validation cycles, and evolving technical parameters will challenge scalability. Cost pressure restricts adoption among smaller manufacturers, influencing overall testing capacity expansion across future automotive ecosystems.

Limited availability of specialized testing infrastructure and skilled professionals.

Specialized laboratories and technically trained professionals remain limited across multiple regions. Future testing needs will exceed contemporary infrastructure readiness, developing bottlenecks in validation timelines. Skill development gaps and uneven technology access will restrain uniform testing quality across emerging automotive manufacturing hubs.

Opportunities:

Rising adoption of next-generation batteries creating demand for advanced and automated BMS testing solutions.

Next-generation batteries will redefine testing priorities within the global automotive battery management system testing market. Automation, virtual simulation, and predictive diagnostics will gain prominence to manage higher power densities. Advanced trying out platforms will allow faster validation cycles whilst supporting innovation throughout destiny electric powered automobile architectures.

Market Segmentation Analysis

The Global Automotive Battery Management System Testing market is classified based on Battery Type, Vehicle Type, Testing Type, and End User.

By Battery Type, the market is further segmented into:

Lithium-ion

Lithium-ion segment was valued at USD 1,250.7 million in 2026 and is projected to reach USD 3,391.3 million by 2033

Lithium-ion battery testing receives priority owing to increased electric mobility and higher energy density requirements. Advanced validation frameworks will focus on thermal stability, charge balancing and lifecycle performance. Future test environments will integrate predictive analytics to support long-term durability expectations in automotive platforms while meeting stringent safety standards.

Lead-acid

Lead-acid segment was valued at USD 170.7 Million in 2026 and is projected to reach USD 287.7 Million by 2033, at a CAGR of 7.7% during the forecast period.

Lead-acid battery testing remains relevant for cost-sensitive automotive applications and auxiliary power systems. Verification activities will emphasize charge retention, vibration resistance and aging behavior. Gradual automation of test processes will improve consistency and fault detection, supporting extended operational reliability within traditional vehicle architectures.

Nickel-based

Nickel-based segment was valued at USD 72 Million in 2026 and is projected to reach USD 131.7 Million by 2033, at a CAGR of 9% during the forecast period.

Nickel-based battery tests address specific automotive uses requiring flexibility under extreme temperature conditions. Testing protocols will expand toward efficacy mapping and degradation tracking. Forward-looking test systems will increase accuracy in performance benchmarking, enabling informed deployment decisions in specific automotive energy storage requirements.

Others

Others segment was valued at USD 77 Million in 2026 and is projected to reach USD 168.7 Million by 2033, at a CAGR of 11.9% during the forecast period.

Other battery chemistries need to undergo targeted testing to evaluate the feasibility of emerging automotive concepts. The emphasis will be on adaptability, safety margins and scalability. The future-oriented test setup will allow rapid evaluation of alternative materials, supporting innovation without compromising regulatory compliance or operational safety standards.

By Vehicle Type, the market is divided into:

Passenger Vehicles

Passenger Vehicles segment is projected to reach USD 1585.8 Million by 2033, at a CAGR of 12.9% during the forecast period.

Passenger vehicle testing will increase owing to increased electrification and heightened consumer safety expectations. Battery management verification will prioritize range accuracy, thermal control, and real-world usage simulation. The test environment will evolve toward scenario-based validation to ensure reliable performance in various driving conditions.

Commercial Vehicles

Commercial Vehicles segment is projected to reach USD 641.5 Million by 2033, at a CAGR of 12.9% during the forecast period.

Commercial vehicle battery testing focuses on load endurance, extended duty cycles, and fleet reliability. The verification system will simulate intensive usage patterns and harsh operating environments. Future testing investments will support uptime optimization and predictive maintenance planning for logistics and public transportation applications.

Battery Electric Vehicles

Battery Electric Vehicles segment is projected to reach USD 1584.2 Million by 2033, at a CAGR of 16.9% during the forecast period.

Battery electric vehicle testing promotes innovation in battery management verification. Focus areas will include fast-charging behavior, energy efficiency and fault tolerance. The advanced testing ecosystem will enable continuous improvement cycles, aligning battery performance with evolving infrastructure and regulatory expectations.

Others

Others segment is projected to reach USD 167.9 Million by 2033, at a CAGR of 9.6% during the forecast period.

Other vehicle categories require customized battery testing strategies based on application-specific demands. The validation will assess compatibility with hybrid configurations and low-volume automotive formats. Flexible test platforms will support different design architectures while maintaining the same quality and security outcomes.

By Testing Type, the market is further divided into:

Hardware-in-the-Loop (HIL) Test System

Hardware-in-the-Loop (HIL) Test System segment is projected to reach USD 1281.8 Million by 2033 with a share of 28.6% in 2025.

HIL test systems serve as the cornerstone for real-time battery management validation. Integration of physical components with the simulated environment will increase the accuracy of fault detection. Future systems will support faster prototyping and shorter development timelines without sacrificing depth of validation.

Software-in-the-Loop Testing

Software-in-the-Loop Testing segment is projected to reach USD 672.1 Million by 2033 with a share of 14.6% in 2025.

Software-in-the-loop testing expands owing to increased software complexity in battery management systems. Emphasis will be on algorithm verification, communication logic, and control accuracy. The virtual testing environment will allow early-stage problem solving, improving overall development efficiency.

Functional Testing

Functional Testing segment is projected to reach USD 1091.6 Million by 2033 with a share of 31.2% in 2025.

Functional testing ensures that battery management operations align with design intent under a variety of conditions. Test procedures will check sensing accuracy, response time, and system coordination. A forward-looking approach will include automated workflows to strengthen repeatability and compliance verification.

Safety and Fault Injection Testing

Safety and Fault Injection Testing segment is projected to reach USD 768.8 Million by 2033 with a share of 19.9% in 2025.

Safety and fault injection testing gains importance amid strict automotive safety norms. Controlled fault scenarios will validate system resilience and fail-safe responses. Advanced simulation capabilities will support proactive risk mitigation on future vehicle platforms.

Others

Others segment is projected to reach USD 165.1 Million by 2033 with a share of 5.6% in 2025.

Other test methods complement validation practices established through special evaluations. The focus will be on interoperability, environmental stress and long-term performance trends. The modular test framework will support evolving automotive battery technologies.

By End User, the Global Automotive Battery Management System Testing market is divided as:

Automotive OEMs

Automotive OEMs segment is projected to grow at a CAGR of 13.6% during the forecast period.

Automotive OEMs invest heavily in comprehensive battery management verification to protect brand reliability. In-house testing capabilities will be expanded to reduce development risks. Adopting strategic testing will help in faster product launches while meeting global compliance standards.

Tier-1 BMS Suppliers

Tier-1 BMS Suppliers segment is projected to grow at a CAGR of 15.7% during the forecast period.

Tier-1 BMS suppliers prioritize testing excellence to strengthen partnerships with vehicle manufacturers. Validation processes will emphasize system integration readiness and scalability. Continuous test refinement will support competitive differentiation and long-term contract retention.

Battery Pack Integrators

Battery Pack Integrators segment is projected to grow at a CAGR of 14.2% during the forecast period.

Battery pack integrators rely on robust testing to ensure system compatibility and safety. Verification will include mechanical integrity, electrical balance and thermal interactions. Adoption of advanced testing will support optimization demands on various automotive platforms.

Cell and Module Manufacturers

Cell and Module Manufacturers segment is projected to grow at a CAGR of 15.1% during the forecast period.

Cell and module manufacturers expand testing investments to align product quality with automotive-grade requirements. Focus areas will include sustainability, declining behavior and compliance readiness. Test-driven insights will guide production optimization and technology upgrades.

Others

Others segment is projected to grow at a CAGR of 9.9% during the forecast period.

Other end users adopt battery management testing to support research, validation, and specific automotive programs. Flexible testing solutions will address diverse operational needs. Future demand will encourage widespread access to standardized testing infrastructure within the global automotive battery management system testing market.

By Region:

Based on geography, the Global Automotive Battery Management System Testing market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America automotive battery management system testing market is projected to expand at a CAGR of 14.2% during 2026-2033, reaching USD 1,125.8 million by 2033.

Strong adoption of electric vehicles is rising in North America, pushing automakers to heighten automotive battery management system checking out to meet overall performance and safety expectancies.

North America benefits from stricter vehicle safety policies, supporting sustained investment in advanced automotive battery management system testing frameworks.

Electric vehicle production is unexpectedly expanding in Asia Pacific, creating sizeable opportunities for automotive battery control system testing offerings.

Asia-Pacific gains momentum from large-scale battery production facilities, strengthening localized automotive battery management system testing capabilities.

Across the Middle East, Africa, and South America, gradual electric mobility adoption and improving automotive standards support steady growth in automotive battery management system testing demand.

Competitive Landscape and Strategic Insights

The global automotive battery management system testing market continues to attract sustained interest as electric powered and hybrid vehicles flow towards mainstream adoption. Battery structures sit down at the center of modern automobiles, and performance, safety, and reliability depend on how thoroughly systems are tested prior to deployment. Battery management system testing focuses on validating voltage control, thermal behavior, communication accuracy, fault detection, and overall system response under real-world driving conditions. As automobile architectures come to be more software-pushed, checking out practices will grow in significance to make certain batteries perform safely throughout varied environments and usage styles.

Testing solutions in this market will help manufacturers for the duration of each development and production levels. Hardware-in-the-loop setups, simulation platforms, and automated check benches will assist engineers compare machine conduct without relying most effective on physical avenue assessments. The equipment will permit quicker fault identification, decreased development time, and better compliance with worldwide safety requirements. With stricter emission rules and rising client expectancies for variety and battery life, testing providers will play a vital role in retaining product pleasant at the same time as controlling costs.

A wide variety of era vendors will form aggressive interest inside the market. Key players consist of AVL List GmbH, dSPACE GmbH, eInfochips, NEWARE, DMC Inc., NXP Semiconductors, Keysight Technologies (Scienlab), Rohde & Schwarz, Chroma ATE Inc., Arbin Instruments, Maccor, Inc., HIOKI E.E. Corporation, Hottinger Brüel & Kjær (HBK), Dewesoft d.O.O., OPAL-RT TECHNOLOGIES, Bloomy Controls, Inc., Typhoon HIL, ANSYS, Inc, HORIBA, Ltd, TÜV SÜD, Applus+ IDIADA, UL Solutions, Intertek, and Pickering Interfaces Ltd. These organizations will offer a mix of testing hardware, simulation software, validation offerings, and certification aid tailored to automotive battery structures.

Collaboration between automakers, battery suppliers, and testing companies will boom as vehicle platforms come to be more complex. Testing vendors will cognizance on scalable solutions which can adapt to extraordinary battery chemistries, percent sizes, and software updates. Digital twins, real-time simulation, and cloud-enabled testing environments will further enhance efficiency and accuracy. Such methods will help manufacturers cope with protection concerns early even as meeting regulatory expectancies throughout areas.

Looking ahead, the market will witness steady demand in the electric vehicle space and innovation in battery technology. The testing solutions will mature to support higher energy density, faster charging solutions, and longer lifecycle solutions. The companies that can provide flexible and cost-effective testing solutions will ensure long-term relevance in the market. As the automotive industry further adopts electrification, battery management system testing will continue to be an essential part of this journey.

Forecast and Future Outlook

Market size is forecast to rise from USD 1,376.4 million in 2025 to over USD 3,979.5 million by 2033.

Future testing activity will also integrate data lineage and traceability requirements driven by regulatory audits and second-life battery deployment strategies. The battery performance history will be validated not only for road use but also for re-use in stationary storage and grid-support applications. As battery ownership models move toward leases and energy service agreements, test results will meet engineering needs as well as financial, legal and insurance assessments.

Automotive Battery Management System Testing Market Key Segments:

By Battery Type:

Lithium-ion

Lead-acid

Nickel-based

Others

By Vehicle Type:

Passenger Vehicles

Commercial Vehicles

Battery Electric Vehicles

Others

By Testing Type:

Hardware-in-the-Loop (HIL) Test System

Software-in-the-Loop Testing

Functional Testing

Safety and Fault Injection Testing

Others

By End User:

Automotive OEMs

Tier-1 BMS Suppliers

Battery Pack Integrators

Cell and Module Manufacturers

Others

Key Global Automotive Battery Management System Testing Industry Players

This research report categorizes the Automotive Battery Management System Testing market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Automotive Battery Management System Testing market. Recent market developments and competitive strategies such as expansion, product launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Automotive Battery Management System Testing market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 14.2% from 2026 to 2033

Revenue Unit

USD million

Segmentation

By Battery Type, Vehicle Type, Testing Type, End User, and Region

By Region

North America (By Battery Type, Vehicle Type, Testing Type, End User, and Country)

United States

Canada

Mexico

Europe (By Battery Type, Vehicle Type, Testing Type, End User, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of the Europe

Asia Pacific (By Battery Type, Vehicle Type, Testing Type, End User, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Battery Type, Vehicle Type, Testing Type, End User, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Battery Type, Vehicle Type, Testing Type, End User, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Full In-Depth Analysis of the Parent Industry

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Former, On-Going, and Projected Market Analysis in Terms of Value

Assessment Of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Major Market Players

UK Bus & Coach Fleet Leasing, Rental and Finance Market Size, Share, Trends, 2033

UK Bus & Coach Fleet Leasing, Rental and Finance market size is valued at USD 886.4 million in 2025 and is projected to reach USD 1,442.8 million in 2033, at a CAGR of 6.3% from 2026 to 2033

UK Bus & Coach Fleet Leasing, Rental and Finance Market, UK Bus & Coach Fleet Leasing, Rental and Finance Market Size, UK Bus & Coach Fleet Leasing, Rental and Finance Market Share, UK Bus & Coach Fleet Leasing, Rental and Finance Market Analysis, UK Bus & Coach Fleet Leasing, Rental and Finance Market Growth, UK Bus & Coach Fleet Leasing, Rental and Finance Market Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market Research Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Forecast, UK Bus & Coach Fleet Leasing, Rental and Finance, UK Bus & Coach Fleet Leasing, Rental and Finance Market Research, UK Bus & Coach Fleet Leasing, Rental and Finance Industry, UK Bus & Coach Fleet Leasing, Rental and Finance Industry Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Data, UK Bus & Coach Fleet Leasing, Rental and Finance Statistics, UK Bus & Coach Fleet Leasing, Rental and Finance Market Statistics, UK Bus & Coach Fleet Leasing, Rental and Finance Industry Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market News, UK Bus & Coach Fleet Leasing, Rental and Finance Forecasts, UK Bus & Coach Fleet Leasing, Rental and Finance Market Intelligence Report

Inductive Loop Vehicle Detector market size is valued at USD 93.1 million in 2025 and is projected to reach USD 205.5 million in 2033, at a CAGR of 10.4% from 2026 to 2033.

USA EVSE Procurement Market Size, Share, Trends, 2033

USA EVSE Procurement market size is valued at USD 6.6 billion in 2025 and is projected to reach USD 52.1 billion in 2033, at a CAGR of 29.5% from 2026 to 2033.

USA EVSE Procurement Market, USA EVSE Procurement Market Size, USA EVSE Procurement Market Share, USA EVSE Procurement Market Analysis, USA EVSE Procurement Market Growth, USA EVSE Procurement Market Trends, USA EVSE Procurement Market Research Report, USA EVSE Procurement Market Forecast, USA EVSE Procurement, USA EVSE Procurement Market Research, USA EVSE Procurement Industry, USA EVSE Procurement Industry Report, USA EVSE Procurement Market Data, USA EVSE Procurement Statistics, USA EVSE Procurement Market Statistics, USA EVSE Procurement Industry Trends, USA EVSE Procurement Market Report, USA EVSE Procurement Market Trends, USA EVSE Procurement Market News, USA EVSE Procurement Forecasts, USA EVSE Procurement Market Intelligence Report

Heavy Duty Truck Wash Market Size, Share, Trends, 2033

Global Heavy Duty Truck Wash market size is valued at USD 1,240.7 million in 2025 and is projected to reach USD 1,863.2 million in 2033, at a CAGR of 5.0% from 2026 to 2033

Heavy Duty Truck Wash Market, Heavy Duty Truck Wash Market Size, Heavy Duty Truck Wash Market Share, Heavy Duty Truck Wash Market Analysis, Heavy Duty Truck Wash Market Growth, Heavy Duty Truck Wash Market Trends, Heavy Duty Truck Wash Market Research Report, Heavy Duty Truck Wash Market Forecast, Heavy Duty Truck Wash, Heavy Duty Truck Wash Market Research, Heavy Duty Truck Wash Industry, Heavy Duty Truck Wash Industry Report, Heavy Duty Truck Wash Market Data, Heavy Duty Truck Wash Statistics, Heavy Duty Truck Wash Market Statistics, Heavy Duty Truck Wash Industry Trends, Heavy Duty Truck Wash Market Report, Heavy Duty Truck Wash Market Trends, Heavy Duty Truck Wash Market News, Heavy Duty Truck Wash Forecasts, Heavy Duty Truck Wash Market Intelligence Report