Canada Skillets and Frying Pans Market By Material Type (Stainless Steel, Carbon Steel, Aluminium, and Other), By Size (Small, Medium, and Large), By Shape (Round, Square, Rectangular, Deep Skillets, Saute Pans, and Others), By End User (Commercial and Residential), Industry Analysis, Size, Share, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-2628

Published

March 7, 2026

Pages

255 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

MARKET OVERVIEW

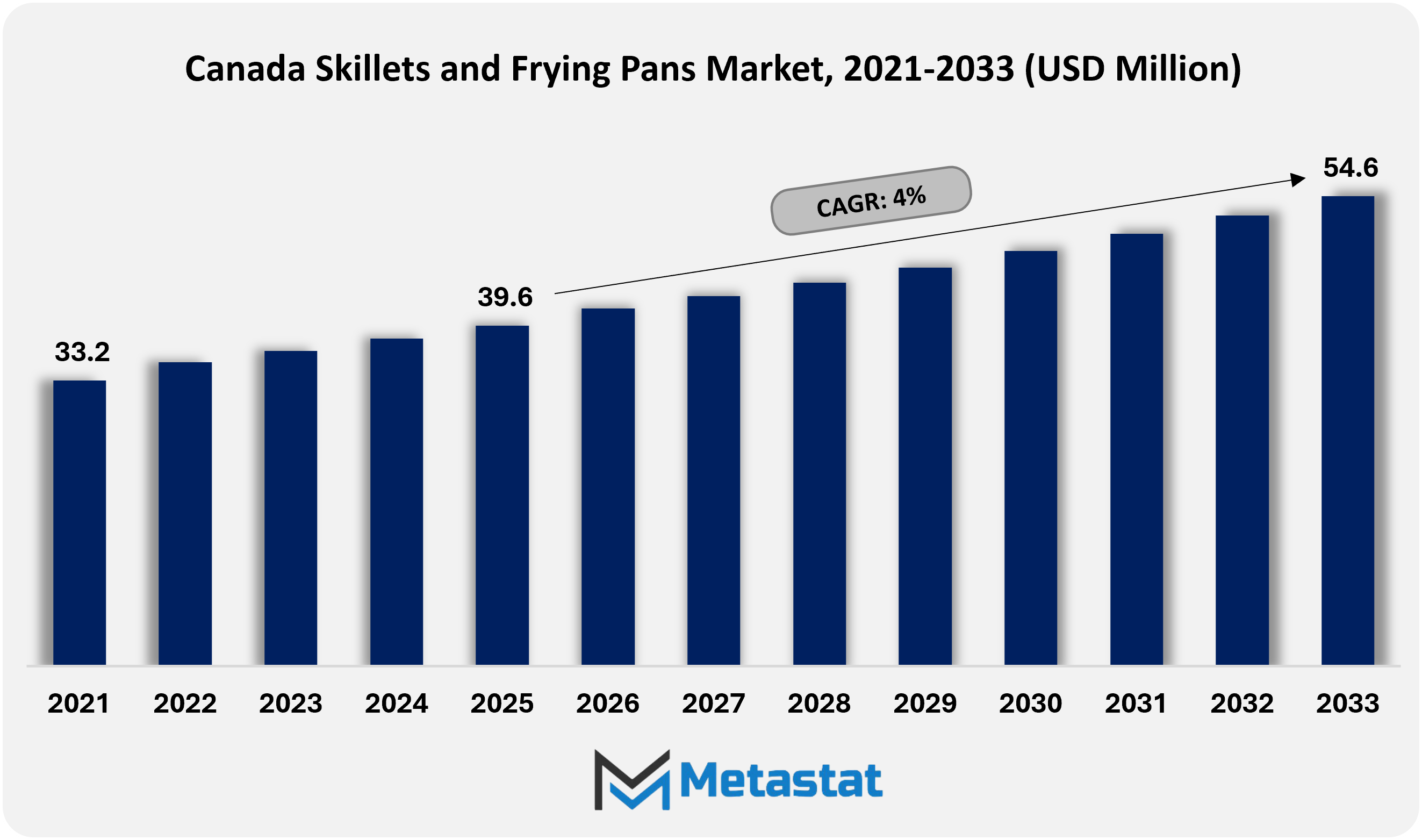

Canada Skillets and Frying Pans market size is valued at USD 39.6 million in 2025 and projected to grow at a CAGR of 4.0% during the forecast period, reaching USD 54.6 million by 2033.

Canada Skillets and Frying Pans market has quietly emerged as a culinary canvas, reflecting the diverse and evolving tastes of a nation that takes its food seriously. In the mosaic of the culinary industry, these essential kitchen tools are not mere utensils; they are the unsung heroes, silently sizzling away in Canadian kitchens, bringing to life the symphony of flavors that define Canadian cuisine.

The Skillets and Frying Pans market in Canada mirrors the dynamic culinary landscape of the country. With an array of materials, sizes, and styles, these kitchen essentials cater to the diverse cooking preferences that span from the coastal provinces to the heartland. From the bustling urban kitchens of Toronto to the cozy cabins in the rugged landscapes of British Columbia, these pans play a vital role in shaping the gastronomic identity of the nation.

One of the distinctive features of the Canadian Skillets and Frying Pans market is its focus on durability and functionality. The Canadian consumer, known for their practical approach to purchases, values products that withstand the test of time. Skillets and frying pans crafted from robust materials, such as cast iron or stainless steel, find favor among Canadian households. The market has responded to this demand by offering a spectrum of choices, ensuring that every kitchen, from the amateur cook to the seasoned chef, can find the perfect pan for their culinary adventures.

The multicultural tapestry of Canada also influences the Skillets and Frying Pans market. As the nation embraces a rich blend of culinary traditions from around the globe, these kitchen essentials need to adapt. The market witnesses a constant influx of innovative designs and features, each catering to a specific cooking style or cultural preference. This dynamic interplay of tradition and innovation fosters a vibrant marketplace where consumers can explore and experiment with various cooking techniques.

Local artisans and manufacturers also play a crucial role in shaping the Skillets and Frying Pans market in Canada. Many businesses, small and large, are committed to producing high-quality, Canadian-made kitchenware. This focus on local craftsmanship not only supports the national economy but also resonates with consumers who appreciate the authenticity and ethical considerations associated with domestically produced goods.

Furthermore, sustainability is an emerging theme in the Canadian Skillets and Frying Pans market. As environmental consciousness takes center stage, consumers are seeking products that align with their values. Manufacturers are responding by incorporating eco-friendly materials and production methods, appealing to a growing segment of environmentally conscious Canadians who want to minimize their ecological footprint even in the kitchen.

The Skillets and Frying Pans market in Canada is more than a market; it's a reflection of a nation's culinary journey. With a focus on durability, adaptability, local craftsmanship, and sustainability, these kitchen essentials continue to evolve, serving as the backbone of Canadian kitchens. As the culinary landscape of the country continues to unfold, the Skillets and Frying Pans market will undoubtedly remain a canvas where flavors and traditions converge in the spirit of Canadian gastronomy.

GROWTH FACTORS

The Canadian market for skillets and frying pans exhibits various factors that influence its dynamics. One significant driver in this culinary landscape is the growing interest in home cooking. As more individuals find joy and satisfaction in preparing meals at home, the demand for cooking utensils, such as skillets and frying pans, experiences a notable uptick.

Health consciousness plays a pivotal role in shaping consumer preferences, with a particular focus on non-stick technology. Consumers today are increasingly mindful of the impact of their cooking methods on health. Consequently, the market witnesses a surge in demand for cooking utensils that align with health-conscious choices, thus propelling the popularity of non-stick technology in skillets and frying pans.

However, this thriving market is not without its challenges. Market saturation emerges as a prominent restraint, where the plethora of available products saturates consumer choices. As a result, businesses face the task of differentiating their offerings to stand out in a crowded marketplace.

Price sensitivity also poses a challenge in the Canadian skillets and frying pans market. Consumers, while valuing quality, are often sensitive to pricing. Striking a balance between providing high-quality products and maintaining competitive prices becomes crucial for manufacturers in this domain.

As environmental consciousness grows, consumers increasingly seek kitchenware that aligns with their commitment to sustainability. Manufacturers can tap into this demand by developing and promoting eco-friendly alternatives in the skillets and frying pans market.

The Canadian market for skillets and frying pans reflects a dynamic interplay of factors. From the rise in home cooking enthusiasm to the challenges posed by market saturation and price sensitivity, the landscape is ever evolving. However, the prospect of introducing eco-friendly and sustainable products opens a promising avenue for growth in this culinary domain.

MARKET SEGMENTATION

By Material Type

The Canadian market for skillets and frying pans can be classified based on the material used in their construction. This categorization plays a crucial role in understanding the diverse options available to consumers.

One key factor in this segmentation is the material type, which influences the characteristics and performance of these kitchen essentials. Stainless steel, known for its durability and resistance to corrosion, stands out as a popular choice among consumers seeking long-lasting cookware. Carbon steel, another option, is favored for its even heating and versatility in various cooking methods.

Aluminium is a lightweight material that offers efficient heat conduction, making it a preferred option for those who prioritize quick and even cooking. Additionally, the market includes pans made from other materials, providing a range of choices to cater to different preferences and cooking styles.

By delving into the material segmentation, consumers can make informed decisions based on their specific needs and preferences. This approach not only simplifies the decision-making process but also ensures that individuals find the right skillet or frying pan that aligns with their cooking requirements.

By Size

In the Canadian market for skillets and frying pans, the categorization is based on size, aiming to capture the diverse preferences of consumers. The small-sized pans, measuring less than 8 inches, recorded a value of 8.39 USD Million in 2023. Moving on to the medium sized category, spanning from 8 to 12 inches, it demonstrated substantial market presence with a valuation of 27.7 USD Million in the same year. As for the larger pans, exceeding 12 inches, their segment attained a value of 13.4 USD Million in 2023.

This segmentation by size not only reflects the varied culinary needs of the populace but also mirrors the dynamic market demand for skillets and frying pans. The small-sized pans, perhaps catering to individual or specific cooking requirements, secured a noteworthy position in terms of market valuation. On the other hand, the medium-sized category emerged as a significant player, indicating a considerable consumer base seeking versatility in their kitchenware. Meanwhile, the larger pans, suitable for more extensive cooking applications, contributed substantially to the overall market value.

The differentiation by size serves as a practical approach for both manufacturers and consumers. It allows producers to tailor their offerings to specific dimensions, meeting the nuanced preferences of individuals. Simultaneously, consumers benefit from a market that acknowledges the diversity in cooking styles and needs, providing them with a comprehensive range of skillet and frying pan options. This market analysis sheds light on the nuanced dynamics of the Canadian culinary equipment landscape, emphasizing the importance of understanding consumer preferences in shaping product offerings and market strategies.

By Shape In examining the Canada Skillets and Frying Pans Market, it is crucial to explore the various shapes that contribute to its diversity. These shapes include Round, Square or Rectangular, Deep Skillets/Saute Pans, and Others. This segmentation sheds light on the different preferences and functionalities that consumers seek in their cookware.

The round shape appeals to those who favor traditional designs, providing a classic and versatile option for various cooking needs. On the other hand, the square or rectangular skillets cater to individuals who prioritize efficient space utilization, fitting well into modern kitchen layouts.

Deep skillets and sauté pans attract a specific audience interested in preparing dishes that require more liquid or ingredients. The depth of these pans accommodates a range of cooking styles, adding versatility to the culinary experience. The category labeled as Others encompasses diverse shapes that cater to unique cooking demands, reflecting the dynamic nature of consumer preferences.

By understanding these shape-based differentiations, manufacturers and consumers alike can make informed choices based on both practicality and personal preferences. This market segmentation not only enhances the shopping experience for consumers but also allows businesses to tailor their products to meet the evolving needs of the culinary landscape in Canada.

By End User

In the Canada Skillets and Frying Pans market, we observe a distinct categorization based on end users. Firstly, the Commercial segment takes center stage, boasting a noteworthy valuation of 15 USD Million in the year 2023. This signifies a considerable economic presence, highlighting the demand and utilization of skillets and frying pans within commercial establishments.

On the residential front, the Residential segment emerges as a significant player, showcasing a valued market worth of 34.4 USD Million in the same year. This underscores the prevalence and consumer preference for these culinary tools in domestic settings. The substantial valuation suggests a robust market engagement within households, emphasizing the relevance of skillets and frying pans in daily cooking activities.

This segmentation provides valuable insights into the dual dynamics of the market, where commercial enterprises and residential households contribute distinctively to the overall economic landscape. The Commercial and Residential segments, with their respective market values, encapsulate the diverse ways in which skillets and frying pans have become integral components in both professional kitchens and home kitchens across Canada.

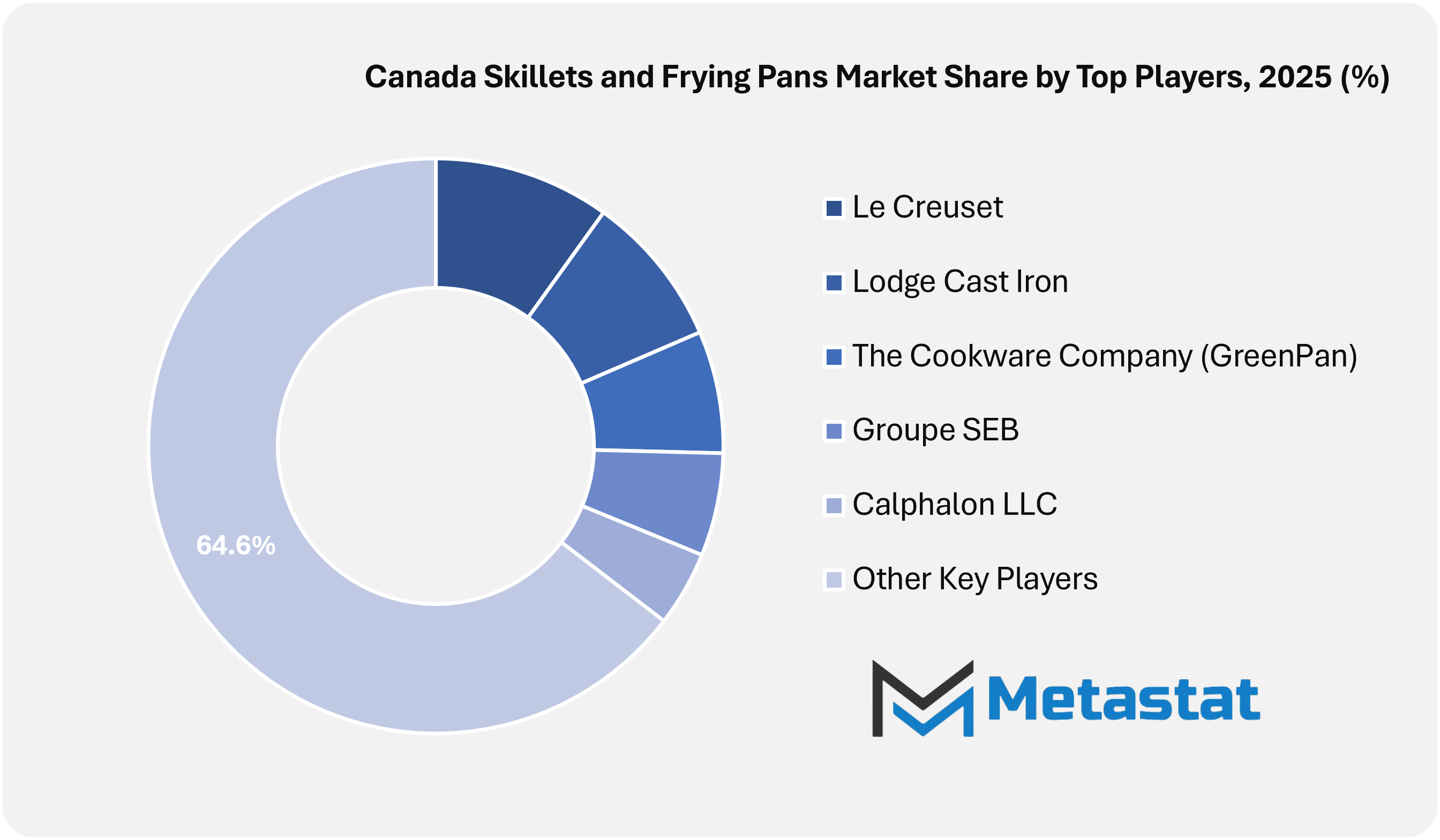

COMPETITIVE PLAYERS

The Skillets and Frying Pans market in Canada boasts a variety of competitive players contributing to the industry's vibrancy. Among these key participants are Lodge Cast Iron, Le Creuset, Groupe SEB, Conair LLC (Cuisinart), Calphalon LLC, The Cookware Company (GreenPan), Zwilling J.A. Henckels LLC, Paderno S.p.A., Tramontina Africa (Pty) Ltd, and Meyer Manufacturing Company Limited.

Lodge Cast Iron is recognized for its durable cast iron cookware, catering to those who appreciate robust kitchen tools. Le Creuset, on the other hand, stands out for its colorful and high-quality enamel-coated cast iron pans, adding a touch of style to cooking. Groupe SEB brings its expertise with a diverse range of cookware, emphasizing functionality and innovation.

Conair LLC, operating under the Cuisinart brand, offers a blend of performance and aesthetics in its skillets and frying pans. Calphalon LLC is known for its precision engineering, providing reliable and efficient cooking solutions. The Cookware Company, renowned for its GreenPan line, prioritizes eco friendly options without compromising on performance.

Zwilling J.A. Henckels LLC is a notable player, combining traditional craftsmanship with modern technology for top-notch culinary experiences. Paderno S.p.A. brings Italian craftsmanship to the Canadian market, showcasing elegance and functionality in its cookware. Tramontina Africa (Pty) Ltd and Meyer Manufacturing Company Limited round out the competitive landscape, each contributing unique strengths to the market.

These players collectively contribute to the rich tapestry of the Skillets and Frying Pans industry in Canada, offering consumers a diverse array of options to suit their culinary preferences and needs. The market is dynamic, with each participant bringing its distinct offerings, ensuring a competitive and innovative landscape for Canadian consumers seeking high-quality cookware.

Skillets and Frying Pans Market Key Segments:

By Material Type

Stainless Steel

Carbon Steel

Aluminium

Others (Cast Iron, Ceramic, Copper)

By Size

Small (Less than 8 inches)

Medium (8-12 inches)

Large (More than 12 inches)

By Shape

Round

Square or Rectangular

Deep Skillets/Saute Pans

Others

By End User

Commercial

Residential

Key Canada Skillets and Frying Pans Industry Players

Lodge Cast Iron

Le Creuset

Groupe SEB

Conair LLC (Cuisinart)

Calphalon LLC

The Cookware Company (GreenPan)

Zwilling J.A. Henckels LLC

Paderno S.p.A.

Tramontina Africa (Pty) Ltd

Meyer Manufacturing Company Limited

Canadian Tire Corporation

SharkNinja

Atlantic Promotions

HexClad Cookware

Made In

SCANPAN

Swiss Diamond International

de Buyer

Mauviel 1830

Fissler GmbH

CRISTEL

Cuisinox

Victoria Cookware

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 4.0% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Thousand Units

Segmentation

By Material Type, Size, Shape, and Region

By Material Type

Stainless Steel

Aluminium

Others (Cast Iron, Ceramic, Copper)

By Size

Small (Less than 8 inches)

Medium (8-12 inches)

Large (More than 12 inches)

By Shape

Round

Square or Rectangular

Deep Skillets/Saute Pans

Others

WHAT REPORT PROVIDES

Full in-depth analysis of the parent Industry

Important changes in market and its dynamics

Segmentation details of the market

Former, on-going, and projected market analysis in terms of volume and value

Australia Cat Litter Market Size, Share, Trends, 2033

Australia Cat Litter market size is valued at USD 361.1 million in 2025 and is projected to reach USD 671.8 million in 2033, at a CAGR of 7.3% from 2026 to 2033

Australia Cat Litter Market, Australia Cat Litter Market Size, Australia Cat Litter Market Share, Australia Cat Litter Market Analysis, Australia Cat Litter Market Growth, Australia Cat Litter Market Trends, Australia Cat Litter Market Research Report, Australia Cat Litter Market Forecast, Australia Cat Litter, Australia Cat Litter Market Research, Australia Cat Litter Industry, Australia Cat Litter Industry Report, Australia Cat Litter Market Data, Australia Cat Litter Statistics, Australia Cat Litter Market Statistics, Australia Cat Litter Industry Trends, Australia Cat Litter Market Report, Australia Cat Litter Market Trends, Australia Cat Litter Market News, Australia Cat Litter Forecasts, Australia Cat Litter Market Intelligence Report

India Naruto Merchandise Market Size, Share, Trends, 2033

India Naruto Merchandise market size is valued at USD 25.3 million in 2025 and is projected to reach USD 61.8 million in 2033, at a CAGR of 11.8% from 2026 to 2033.

India Naruto Merchandise Market, India Naruto Merchandise Market Size, India Naruto Merchandise Market Share, India Naruto Merchandise Market Analysis, India Naruto Merchandise Market Growth, India Naruto Merchandise Market Trends, India Naruto Merchandise Market Research Report, India Naruto Merchandise Market Forecast, India Naruto Merchandise, India Naruto Merchandise Market Research, India Naruto Merchandise Industry, India Naruto Merchandise Industry Report, India Naruto Merchandise Market Data, India Naruto Merchandise Statistics, India Naruto Merchandise Market Statistics, India Naruto Merchandise Industry Trends, India Naruto Merchandise Market Report, India Naruto Merchandise Market Trends, India Naruto Merchandise Market News, India Naruto Merchandise Forecasts, India Naruto Merchandise Market Intelligence Report

UK Pilates Reformer Market Size, Share, Trends, 2033

UK Pilates Reformer market size is valued at USD 141.1 million in 2025 and is projected to reach USD 260.3 million in 2033, at a CAGR of 7.5% from 2026 to 2033.

UK Pilates Reformer Market, UK Pilates Reformer Market Size, UK Pilates Reformer Market Share, UK Pilates Reformer Market Analysis, UK Pilates Reformer Market Growth, UK Pilates Reformer Market Trends, UK Pilates Reformer Market Research Report, UK Pilates Reformer Market Forecast, UK Pilates Reformer, UK Pilates Reformer Market Research, UK Pilates Reformer Industry, UK Pilates Reformer Industry Report, UK Pilates Reformer Market Data, UK Pilates Reformer Statistics, UK Pilates Reformer Market Statistics, UK Pilates Reformer Industry Trends, UK Pilates Reformer Market Report, UK Pilates Reformer Market Trends, UK Pilates Reformer Market News, UK Pilates Reformer Forecasts, UK Pilates Reformer Market Intelligence Report

Global Lab-Grown Diamond Jewelry market size is valued at USD 14.01 billion in 2025 and is projected to reach USD 34.68 billion in 2033, at a CAGR of 12.0% from 2026 to 2033

Global Lab-Grown Diamond Jewelry Market, Global Lab-Grown Diamond Jewelry Market Size, Global Lab-Grown Diamond Jewelry Market Share, Global Lab-Grown Diamond Jewelry Market Analysis, Global Lab-Grown Diamond Jewelry Market Growth, Global Lab-Grown Diamond Jewelry Market Trends, Global Lab-Grown Diamond Jewelry Market Research Report, Global Lab-Grown Diamond Jewelry Market Forecast, Global Lab-Grown Diamond Jewelry, Global Lab-Grown Diamond Jewelry Market Research, Global Lab-Grown Diamond Jewelry Industry, Global Lab-Grown Diamond Jewelry Industry Report, Global Lab-Grown Diamond Jewelry Market Data, Global Lab-Grown Diamond Jewelry Statistics, Global Lab-Grown Diamond Jewelry Market Statistics, Global Lab-Grown Diamond Jewelry Industry Trends, Global Lab-Grown Diamond Jewelry Market Report, Global Lab-Grown Diamond Jewelry Market Trends, Global Lab-Grown Diamond Jewelry Market News, Global Lab-Grown Diamond Jewelry Forecasts, Global Lab-Grown Diamond Jewelry Market Intelligence Report