Medical Beds Market Size, Share, By Product Type (Electric Medical Beds, Semi-Electric Medical Beds, and Manual Medical Beds), By Usages (Acute Care Beds, Psychiatric Care Beds, Long-term Care Beds, Bariatric Beds, and Others), By Application (Intensive Care Beds, and Non-intensive Care Beds), By End Users (Hospitals, Elderly Care Facilities, Nursing Homes, Home Care Settings, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4742

Published

May 19, 2026

Pages

315 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

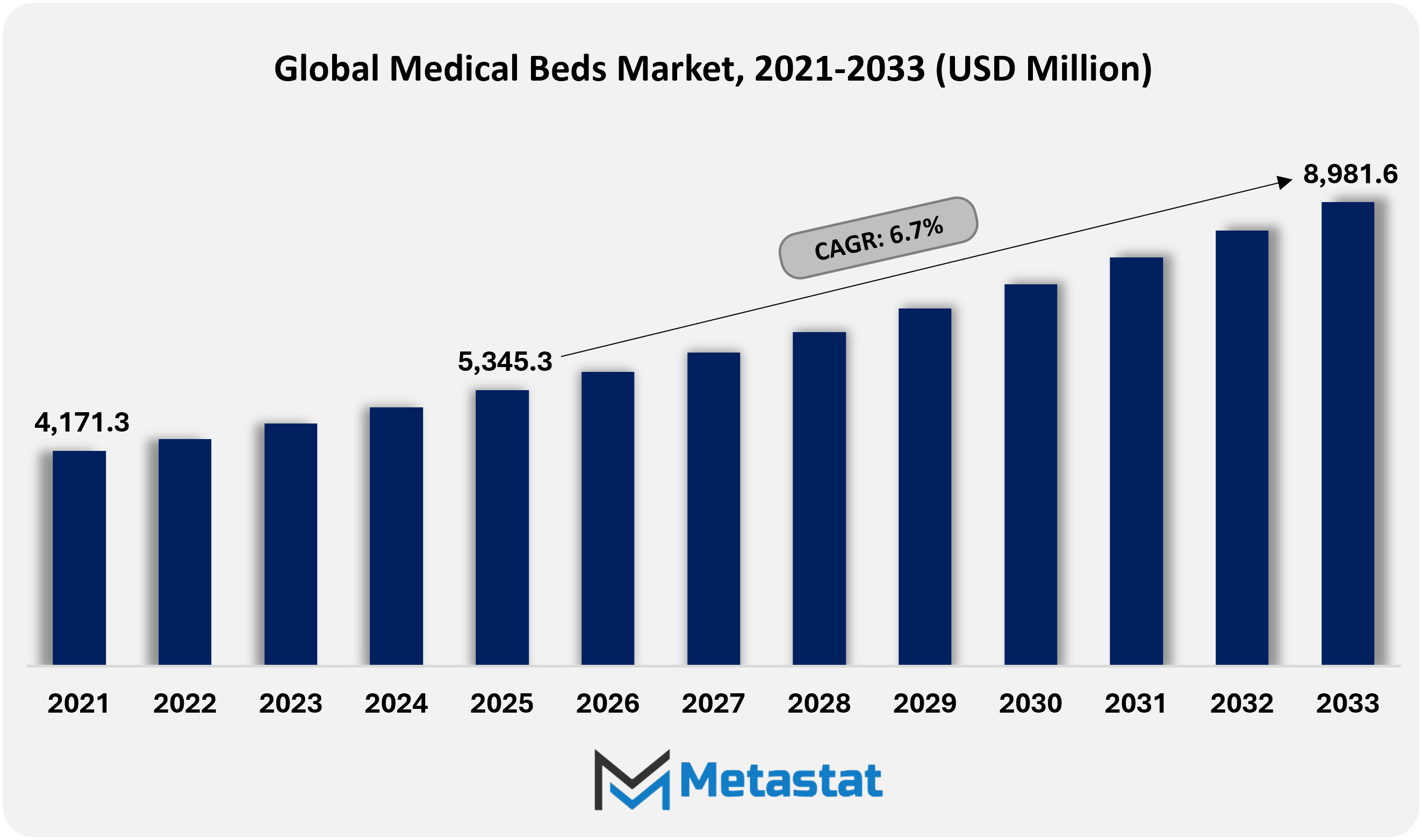

Global Medical Beds market size is valued at USD 5,345.3 million in 2025 and projected to grow at a CAGR of 6.7% during the forecast period, reaching USD 8,981.6 million by 2033.

Global Medical Beds Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Medical Beds market valued at USD 5,345.3 million in 2025, growing at a CAGR of 6.7% through 2033, with potential to exceed USD 8,981.6 million.

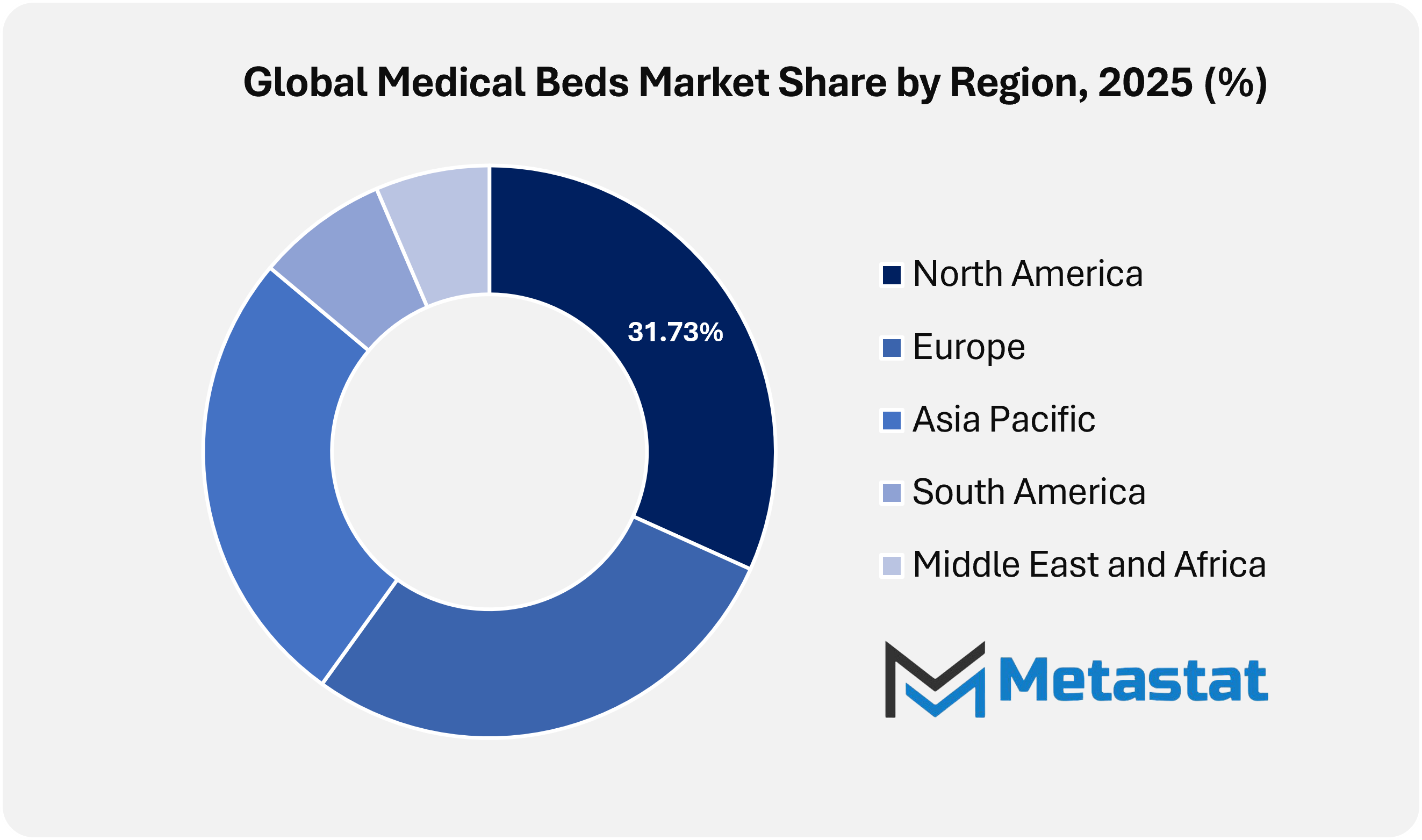

North America holds 31.7% in 2025 with US leading the market share in 2025.

Electric Medical Beds segment account for a market share of 48.8% in 2025.

Key trends driving growth: Rising hospitalization rates and aging population base accelerate demand for advanced motorized and ICU-configured medical beds, along with expansion of home healthcare and post-acute care services propels adoption of compact and multifunctional adjustable beds.

Opportunities include integration of smart monitoring features such as weight sensors, fall detection, and remote adjustment systems creates strong innovation-led growth avenues.

Key insight: Rising geriatric population and expanding healthcare infrastructure are accelerating demand in the Global Medical Beds market.

Global Medical Beds market forms an important part of the broader medical equipment industry, where patient care efficiency, safety requirements, and healthcare infrastructure expansion continue to shape demand. Over the forecast period, procurement will increasingly extend beyond conventional hospitals to rehabilitation centers, elderly care facilities, nursing homes, and home care settings. Medical beds are evolving from basic patient support systems into advanced care platforms equipped with adjustable positioning, caregiver support functions, and compatibility with monitoring solutions. Manufacturers are focusing on product designs that improve patient comfort, operational efficiency, and clinical functionality across acute and long-term care environments.

Urban hospital expansion across emerging economies is increasing demand for modular, easy-to-install, and hygiene-focused medical bed systems. At the same time, aging populations across Europe and East Asia are supporting procurement of long-term care beds designed for comfort, mobility support, and fall prevention. Competition is moving beyond basic mechanical durability toward patient safety, caregiver ease of use, and clinically efficient design. Features such as pressure relief support, ergonomic adjustment, and improved patient handling are becoming increasingly important in purchasing decisions across tertiary hospitals and specialized care facilities.

Market Dynamics

Growth Drivers:

Rising hospitalization rates and aging population base accelerate demand for advanced motorized and ICU-configured medical beds.

Rising patient admissions across multispecialty hospitals, trauma centers, and long-term care facilities are strengthening procurement demand in the Global Medical Beds market. A growing elderly population is increasing the need for bed systems equipped with motorized positioning, pressure relief support, and ICU-compatible configurations. Healthcare providers are prioritizing products that improve patient comfort, reduce caregiver burden, and support safer treatment delivery. These trends are encouraging manufacturers to develop ergonomic and clinically advanced bed solutions.

Expansion of home healthcare and post-acute care services propels adoption of compact and multifunctional adjustable beds.

Expansion of home healthcare and post-acute recovery services is increasing demand for compact, adjustable, and multifunctional medical beds across residential settings. Patients recovering at home require bed systems that are easy to operate, space-efficient, and supportive for both users and caregivers. This trend is encouraging development of lightweight frames, simple control mechanisms, and practical caregiver-assist features. Wider availability through medical equipment rental providers and community healthcare networks is further supporting segment growth.

Restraints and Challenges:

High procurement and maintenance costs of fully electric and ICU beds constrain adoption among small healthcare facilities.

High acquisition costs associated with fully electric and ICU-configured medical beds continue to limit adoption among small hospitals, regional clinics, and budget-sensitive healthcare facilities. Ongoing expenses related to maintenance, spare parts replacement, and technical servicing further increase total ownership cost. These financial constraints often encourage smaller institutions to retain conventional or lower-cost alternatives for longer periods. As a result, adoption of advanced bed systems remains slower across cost-sensitive care environments.

Budgetary pressures in public healthcare systems delay replacement cycles of existing manual bed inventories.

Budget limitations across public healthcare systems continue to extend replacement cycles for manual and aging bed inventories. Many government-supported hospitals and community care centers operate under restricted capital budgets, which slows modernization plans and delays procurement of advanced bed systems. Large-scale upgrades are often implemented in phases rather than through immediate replacement programs. This financial pressure remains a key restraint across several public-sector healthcare markets.

Opportunities:

Integration of smart monitoring features such as weight sensors, fall detection, and remote adjustment systems creates strong innovation-led growth avenues.

Integration of smart monitoring technologies such as weight sensors, fall detection systems, and remote adjustment features is creating a strong innovation opportunity in the Global Medical Beds market. These capabilities improve patient safety, strengthen caregiver response, and support more efficient workflow across hospitals and long-term care facilities. Healthcare providers are showing rising interest in connected bed systems that combine patient support with functional monitoring. Continued investment in connected healthcare infrastructure will create fresh growth opportunities for manufacturers offering advanced bed solutions.

Market Segmentation Analysis

The Global Medical Beds market is classified based on Product Type, Usages, Application, and End Users.

By Product Type, the market is further segmented into:

Electric Medical Beds

Electric Medical Beds segment is valued at USD 2,782.3 million in 2026 and is projected to reach USD 4,851 million by 2033, at a CAGR of 8.3% during the forecast period.

Electric Medical Beds will continue to record strong demand in the Medical Beds market owing to automated positioning, ease of operation, and growing use across hospitals and advanced care settings. Healthcare providers are increasingly prioritizing beds that improve patient comfort, reduce caregiver effort, and support efficient treatment workflows. Product innovation is also strengthening demand through integration of monitoring compatibility and improved adjustment mechanisms. These advantages will keep the segment at the forefront of market revenue generation.

Semi-Electric Medical Beds

Semi-Electric Medical Beds segment is valued at USD 1,695.6 million in 2026 and is projected to reach USD 2,492.4 million by 2033, at a CAGR of 5.7% during the forecast period.

Semi-Electric Medical Beds are attracting demand from healthcare providers seeking a practical balance between functionality and cost efficiency. These beds offer powered head and foot adjustment while maintaining lower cost than fully electric models, making them suitable for secondary hospitals, nursing homes, and regional care centers. Their practical design supports routine patient handling without significantly increasing capital expenditure. Stable procurement from mid-tier institutions will continue to support this segment.

Manual Medical Beds

Manual Medical Beds segment is valued at USD 1,220.4 million in 2026 and is projected to reach USD 1,638.2 million by 2033, at a CAGR of 4.3% during the forecast period.

Manual Medical Beds remain relevant across resource-constrained healthcare settings where affordability, durability, and low maintenance are major purchasing factors. Public hospitals, rural healthcare centers, and basic inpatient facilities continue to rely on these beds for routine patient support. Their mechanical design ensures dependable operation without dependence on electrical systems. Ongoing investment in essential healthcare infrastructure will help sustain demand across cost-sensitive markets.

By Usages, the market is divided into:

Acute Care Beds

Acute Care Beds segment is projected to reach USD 3,286.8 million by 2033, at a CAGR of 5.6% during the forecast period.

Acute Care Beds are witnessing stronger demand across emergency departments, surgical recovery units, and general inpatient settings. Healthcare providers are increasingly seeking bed systems that support patient mobility, pressure management, and improved infection control. Rapid patient turnover in acute care environments is increasing the need for adaptable and durable bed configurations. Product improvements in adjustability, materials, and ease of cleaning are strengthening the segment.

Psychiatric Care Beds

Psychiatric Care Beds segment is projected to reach USD 867.2 million by 2033, at a CAGR of 6% during the forecast period.

Psychiatric Care Beds are designed to support secure treatment environments through reinforced construction, anti-ligature features, and safety-oriented design. Demand is increasing across mental health institutions and specialized care facilities that require controlled inpatient settings. Healthcare providers are prioritizing products that improve supervision while protecting patient dignity and safety. Manufacturers are focusing on durable and specialized designs suited for psychiatric care applications.

Long-term Care Beds

Long-term Care Beds segment is projected to reach USD 2,941.5 million by 2033, at a CAGR of 8.3% during the forecast period.

Long-term Care Beds are gaining traction owing to rising geriatric populations and increasing prevalence of chronic conditions requiring extended care support. These beds are widely used across elderly care facilities, assisted living centers, and long-duration recovery environments where comfort and stability are essential. Features such as adjustable positioning, low-height design, and fall prevention support are strengthening adoption. Rising investment in senior care infrastructure will continue to support segment growth.

Bariatric Beds

Bariatric Beds segment is projected to reach USD 1,208.7 million by 2033, at a CAGR of 7.7% during the forecast period.

Bariatric Beds are recording increasing demand as healthcare systems respond to rising obesity prevalence and the need for specialized patient support infrastructure. These beds are designed with higher weight capacity, wider frames, and reinforced construction to improve safety for both patients and caregivers. Hospitals and specialty care facilities are expanding procurement of bariatric-compatible equipment to meet treatment requirements more effectively.

Others

Others segment is projected to reach USD 677.5 million by 2033, at a CAGR of 5.3% during the forecast period.

Other specialized beds, including pediatric, maternity, and rehabilitation-focused variants, continue to serve targeted clinical requirements across specialty care environments. Demand in this category is supported by healthcare diversification and the need for application-specific patient support systems. Product customization, ergonomic design, and clinical suitability remain central to purchasing decisions. Manufacturers are expanding niche product portfolios to address evolving needs across specialty treatment settings.

By Application, the market is further divided into:

Intensive Care Beds

Intensive Care Beds segment is projected to reach USD 3,687 million by 2033.

Intensive Care Beds represent a vital segment within owing to their role in supporting high-dependency and life-support treatment environments. These beds are designed for precise positioning, pressure redistribution, caregiver accessibility, and compatibility with critical care equipment. Hospitals continue to prioritize ICU bed procurement as critical care capacity expands across developed and emerging healthcare systems.

Non-intensive Care Beds

Non-intensive Care Beds segment is projected to reach USD 5,294.7 million by 2033.

Non-Intensive Care Beds account for a significant share of demand across general wards, recovery rooms, and routine inpatient care settings. Healthcare providers in this segment prioritize durability, ease of use, patient comfort, and cost efficiency. Product development continues to focus on adjustable features, safe patient transfer support, and long service life.

By End Users, the Global Medical Beds market is divided as:

Hospitals

Hospitals segment is projected to grow at a CAGR of 5.4% during the forecast period.

Hospitals remain the primary end-user segment in the Global Medical Beds market, supported by rising patient admissions, infrastructure modernization, and replacement demand for aging bed inventories. Large healthcare institutions are increasingly adopting advanced electric and ICU-compatible bed systems to improve treatment efficiency and patient outcomes. Procurement is also supported by government healthcare spending and expansion of multispecialty and tertiary care facilities.

Elderly Care Facilities

Elderly Care Facilities segment is projected to grow at a CAGR of 8.6% during the forecast period.

Elderly Care Facilities are witnessing strong demand owing to expanding aging populations and rising need for assisted living and long-term residential care. Purchasing priorities in this segment include comfort, mobility support, fall prevention, and caregiver convenience. Demand for adjustable and low-height bed systems is increasing across senior care settings.

Nursing Homes

Nursing Homes segment is projected to grow at a CAGR of 8.3% during the forecast period.

Nursing Homes are increasing adoption of durable and low-maintenance medical beds that support daily caregiving activities and resident comfort. Product demand in this segment is driven by the need to reduce caregiver strain, improve patient independence, and support long-duration bed occupancy. Facilities are prioritizing reliable solutions that combine affordability with essential functional features.

Home Care Settings

Home Care Settings segment is projected to grow at a CAGR of 8.1% during the forecast period.

Home Care Settings are emerging as an important demand area in the Medical Beds market, supported by growing preference for home-based treatment, rehabilitation, and elderly support. Compact, foldable, and user-friendly bed systems are becoming increasingly important for residential environments. Demand is also rising for remote-adjustable and caregiver-supportive features that improve convenience and monitoring.

Others

Others segment is projected to grow at a CAGR of 3.8% during the forecast period.

Other end users, including rehabilitation centers and specialty clinics, are contributing to market demand through need for customized bed systems aligned with specific treatment requirements. These facilities value functional adaptability, hygiene support, and efficient patient transfer. Growing specialization across healthcare delivery is widening adoption beyond traditional hospital settings. This trend is creating new opportunities for manufacturers serving focused and niche care applications.

By Region:

Based on geography, the Global Medical Beds market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Medical Beds Market is set to expand at a CAGR of 6.7% within the forecast period, reaching a market size (TAM) of USD 2,580.4 million by the end of 2033.

North America drives the Medical Beds market through rising health center admissions connected to continual diseases and an ageing population stressful superior affected person care infrastructure.

Europe supports the Medical Beds market through established hospital infrastructure, growing elderly care requirements, and rising demand for technologically advanced patient support systems.

Asia Pacific presents primary opportunities for the Medical Beds market owing to increasing medical institution networks and increasing investments in public healthcare infrastructure.

Across the Middle East, Africa, and South America, the Medical Beds market profits momentum from gradual healthcare modernization, rising private health facility investments, and enhancing access to inpatient care services.

Competitive Landscape and Strategic Insights

The global medical beds market is developing steadily, supported by increasing demand for quality healthcare infrastructure across hospitals, clinics, rehabilitation facilities, and home care settings. Aging populations and rising prevalence of chronic diseases are strengthening the need for advanced and adjustable bed systems that improve patient comfort and support clinical care. Hospitals are prioritizing patient safety, infection control, and efficient recovery, which is encouraging adoption of electric and semi-electric medical beds. At the same time, growth in home healthcare services is increasing demand for reliable bed systems that offer both medical support and ease of use in residential environments.

Modern medical beds now include features such as height adjustment, pressure relief systems, mobility support, and compatibility with monitoring functions. These capabilities help reduce the risk of bedsores, falls, and caregiver strain while improving patient handling efficiency. Manufacturers are also focusing on designs that are easy to clean and maintain, supporting strict hygiene standards across healthcare facilities. Product development is increasingly centered on combining clinical functionality with improved patient comfort and user-friendly design.

Competition in the market remains strong, with global and regional manufacturers investing in product innovation, portfolio expansion, and distribution strengthening. Companies such as Baxter International Inc., Stryker Corporation, LINET spol. s r.o., Arjo AB, and Invacare Corporation maintain strong positions through broad product portfolios and established customer relationships. Other notable participants include Joerns Healthcare LLC, Drive DeVilbiss Healthcare LLC, Paramount Bed Holdings Co., Ltd., Stiegelmeyer GmbH & Co. KG, and Haelvoet bvba. These companies continue to strengthen their presence across both developed and emerging markets.

Additional participants such as Malvestio S.p.A., Favero Health Projects S.p.A., Lojer Oy, Merivaara Corp., Volker GmbH, Burmeier GmbH & Co. KG, wissner-bosserhoff GmbH, Famed Żywiec Sp. z o.o., and Pardo Group are contributing to market expansion through specialized product development and regional reach. Companies including Medline Industries, LP, Amico Corporation, Gendron, Inc., GF Health Products, Inc., Med-Mizer, Inc., Accora Ltd, RotoBed, Transfer Master, Inc., ProBed Medical Technologies Inc., PROMA REHA, s.r.o., Vermeiren N.V., GIVAS S.r.l., Savion Industries Ltd., Narang Medical Limited, Saikang Medical Group, and Direct Supply, Inc. are also strengthening product lines to address varied patient care requirements. Continued investment in design, safety features, and market expansion strategies will support steady growth across the global medical beds market.

Top Player Market Share Graph

Forecast and Future Outlook

Market size is forecast to rise from USD 5,345.3 million in 2025 to over USD 8,981.6 million by 2033.

Sustainability and operational efficiency are becoming increasingly important in the Global Medical Beds market as manufacturers focus on lightweight materials, durable components, and energy-efficient system design. Product development is moving toward smarter and more adaptable bed systems that support patient safety, caregiver efficiency, and broader use across non-acute care environments. Supply chains are also being optimized to improve resilience and ensure consistent product availability across regions. Over the forecast period, competitive differentiation will increasingly depend on product reliability, service capability, and alignment with evolving clinical care requirements.

Medical Beds Market Key Segments:

By Product Type:

Electric Medical Beds

Semi-Electric Medical Beds

Manual Medical Beds

By Usages:

Acute Care Beds

Psychiatric Care Beds

Long-term Care Beds

Bariatric Beds

Others

By Application:

Intensive Care Beds

Non-intensive Care Beds

By End Users:

Hospitals

Elderly Care Facilities

Nursing Homes

Home Care Settings

Others

Key Global Medical Beds Industry Players

Baxter International Inc.

Stryker Corporation

LINET spol. s r.o.

Arjo AB

Invacare Corporation

Joerns Healthcare LLC

Drive DeVilbiss Healthcare LLC

Paramount Bed Holdings Co., Ltd.

Stiegelmeyer GmbH & Co. KG

Haelvoet bvba

Malvestio S.p.A.

Favero Health Projects S.p.A.

Lojer Oy

Merivaara Corp.

Volker GmbH

Burmeier GmbH & Co. KG

wissner-bosserhoff GmbH

Famed Żywiec Sp. z o.o.

Pardo Group

Medline Industries, LP

Amico Corporation

Gendron, Inc.

GF Health Products, Inc.

Med-Mizer, Inc.

Accora Ltd

RotoBed

Transfer Master, Inc.

ProBed Medical Technologies Inc.

PROMA REHA, s.r.o.

Vermeiren N.V.

GIVAS S.r.l.

Savion Industries Ltd.

Narang Medical Limited

Saikang Medical Group

Direct Supply, Inc.

Report Coverage

This research report categorizes the Medical Beds market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Medical Beds market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Medical Beds market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 6.7% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Thousand Units

Segmentation

By Product Type, Usages, Application, End Users, and Region

By Product Type

Electric Medical Beds

Semi-Electric Medical Beds

Manual Medical Beds

By Usages

Acute Care Beds

Psychiatric Care Beds

Long-term Care Beds

Bariatric Beds

Others

By Application

Intensive Care Beds

Non-intensive Care Beds

By End Users

Hospitals

Elderly Care Facilities

Nursing Homes

Home Care Settings

Others

By Region

North America (By Product Type, Usages, Application, End Users, and Country)

United States

Canada

Mexico

Europe (By Product Type, Usages, Application, End Users, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Product Type, Usages, Application, End Users, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Product Type, Usages, Application, End Users, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Product Type, Usages, Application, End Users, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

India Maternal Health Monitoring Market Size, Share, Trends, 2033

India Maternal Health Monitoring market size is valued at USD 416.0 million in 2025 and is projected to reach USD 834.4 million in 2033, at a CAGR of 9.1% from 2026 to 2033

India Maternal Health Monitoring Market, India Maternal Health Monitoring Market Size, India Maternal Health Monitoring Market Share, India Maternal Health Monitoring Market Analysis, India Maternal Health Monitoring Market Growth, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market Research Report, India Maternal Health Monitoring Market Forecast, India Maternal Health Monitoring, India Maternal Health Monitoring Market Research, India Maternal Health Monitoring Industry, India Maternal Health Monitoring Industry Report, India Maternal Health Monitoring Market Data, India Maternal Health Monitoring Statistics, India Maternal Health Monitoring Market Statistics, India Maternal Health Monitoring Industry Trends, India Maternal Health Monitoring Market Report, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market News, India Maternal Health Monitoring Forecasts, India Maternal Health Monitoring Market Intelligence Report

Global Anaerobic Incubators market size is valued at USD 177.5 million in 2025 and is projected to reach USD 323.6 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Global Radiochemical Synthesizers market size is valued at USD 450.5 million in 2025 and is projected to reach USD 746.6 million in 2033, at a CAGR of 6.7% from 2026 to 2033.

Global Radiochemical Synthesizers Market, Global Radiochemical Synthesizers Market Size, Global Radiochemical Synthesizers Market Share, Global Radiochemical Synthesizers Market Analysis, Global Radiochemical Synthesizers Market Growth, Global Radiochemical Synthesizers Market Trends, Global Radiochemical Synthesizers Market Research Report, Global Radiochemical Synthesizers Market Forecast, Global Radiochemical Synthesizers, Global Radiochemical Synthesizers Market Research, Global Radiochemical Synthesizers Industry, Global Radiochemical Synthesizers Industry Report, Global Radiochemical Synthesizers Market Data, Global Radiochemical Synthesizers Statistics, Global Radiochemical Synthesizers Market Statistics, Global Radiochemical Synthesizers Industry Trends, Global Radiochemical Synthesizers Market Report, Global Radiochemical Synthesizers Market Trends, Global Radiochemical Synthesizers Market News, Global Radiochemical Synthesizers Forecasts, Global Radiochemical Synthesizers Market Intelligence Report

Thoracolumbar Posterior Fixation Systems Market Size, Share, Trends, 2033

Global Thoracolumbar Posterior Fixation Systems market size is valued at USD 875.8 million in 2025 and is projected to reach USD 1,526.6 million in 2033, at a CAGR of 7.2% from 2026 to 2033

Thoracolumbar Posterior Fixation Systems Market, Thoracolumbar Posterior Fixation Systems Market Size, Thoracolumbar Posterior Fixation Systems Market Share, Thoracolumbar Posterior Fixation Systems Market Analysis, Thoracolumbar Posterior Fixation Systems Market Growth, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market Research Report, Thoracolumbar Posterior Fixation Systems Market Forecast, Thoracolumbar Posterior Fixation Systems, Thoracolumbar Posterior Fixation Systems Market Research, Thoracolumbar Posterior Fixation Systems Industry, Thoracolumbar Posterior Fixation Systems Industry Report, Thoracolumbar Posterior Fixation Systems Market Data, Thoracolumbar Posterior Fixation Systems Statistics, Thoracolumbar Posterior Fixation Systems Market Statistics, Thoracolumbar Posterior Fixation Systems Industry Trends, Thoracolumbar Posterior Fixation Systems Market Report, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market News, Thoracolumbar Posterior Fixation Systems Forecasts, Thoracolumbar Posterior Fixation Systems Market Intelligence Report