Automotive Display System Market By Display Type (Instrument Cluster Display, Center Stack Display, Head-Up Display (HUD), Rear Seat Entertainment Display, and Other), By Technology (Liquid Crystal Display (LCD), Thin-Film Transistor (TFT) LCD, OLED Display, Micro LED Display, and Projection Display), By Size (Small Displays (Up to 5 inches), Medium Displays (6 to 10 inches), and Large Displays (Above 10 inches)), By Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles, and Luxury Vehicles), Industry Analysis, Size, Share, Growth, Trends, and Forecast, 2025-2032

Report ID

MSI-4261

Published

February 10, 2026

Pages

255 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Global Automotive Display System Market- Comprehensive Data-Driven Market Analysis & Strategic Outlook

The global automotive display system market has evolved from a specialty niche of simple dashboards to an amazingly complex center of in-car communications, navigation, and entertainment. In its first phase, car displays were mere analog gauges that indicated speed, fuel, and temperature. The late 1980s saw the very first giant leap with digital odometers and simple LCD panels being seen in luxury vehicles. These early developments were precursors to the future integration of visual data with the act of driving, paving the way for what would become more sophisticated infotainment systems.

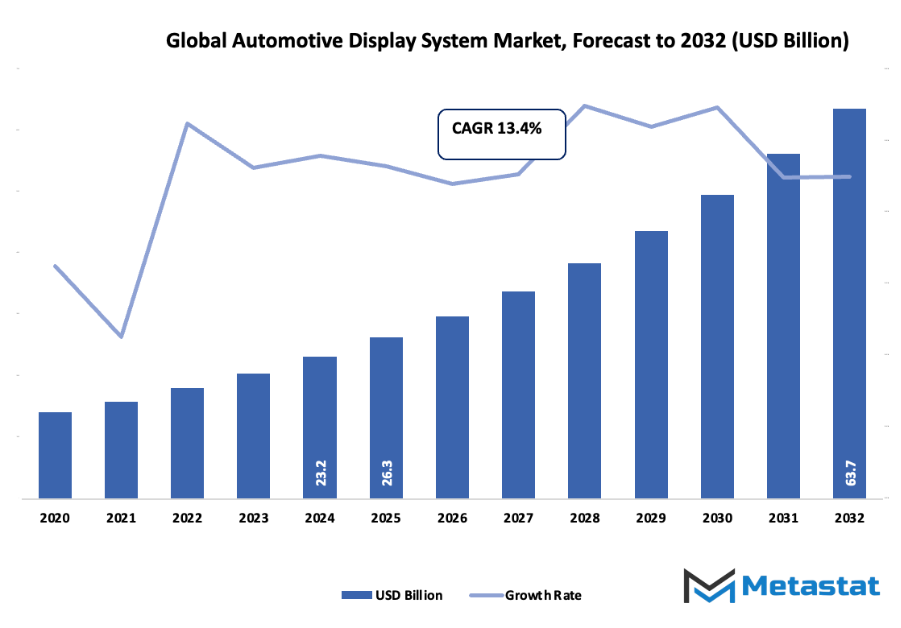

Global automotive display system market worth around USD 26.3 Billion in the year 2025 at a growth rate of around 13.4% during the period from 2032, with a potential to reach beyond USD 63.7 Billion.

Instrument Cluster Display maintains nearly 28.6% market share, promoting innovation and broadened uses through ambitious research.

Driving trends: Growing need for innovative infotainment and connected car technology., Growing use of electric and autonomous vehicles with advanced display interfaces.

Opportunities are: Growing application of smart, customized, and AI-based Automotive Display Systems.

Key point: The industry is on track to grow exponentially in value over the next decade, which supports vigorous growth prospects.

With car interiors becoming digitized in the early 2000s, makers began incorporating color screens for media functions and navigation. It was as much about functionality as it was about aesthetics. The increasing ability of smartphones across these decades reshaped consumer expectations and compelled automakers to provide interactive and intuitive user interfaces. The automotive display system market around the world slowly kept up with some consumer demands in terms of connectivity, touch control, and customization. Displays ceased being data tools but increasingly became part of tools of engagement and control. The previous decade experienced the advent of high-definition displays, OLED and AMOLED technology, and head-up displays revolutionize the driving experience. The increasing focus on automotive safety has provided a key driver of change, as drivers became reliant on visual screens, 360-degree surveillance, and augmented reality overlays to assist. Governments in the big economic blocs created standards for safer user interfaces, indirectly driving the adoption of smart display systems. The situation today is one of an automaker hovering at the crossroads of design, data, and automation. Car companies are trying out curved panels, multi-screen designs, and voice-controlled screens to design frictionless human-machine interaction.

Near future displays will transcend from dashboards to windshields, side panels, and even steering wheels, redefining how information is utilized within cars. From humble beginnings in analog meters to present-day digital communities, the global automotive display system market will continue to redefine the vocabulary of mobility, transforming cars into intelligent companions and not merely transport devices.

Market Segments

The global automotive display system market is mainly classified based on Display Type, Technology, Size, Vehicle Type.

By Display Type is further segmented into:

Instrument Cluster Display: The glglobabal aautomotive ddisplay ssystem market will experience cutting-edge instrument cluster displays with higher-definition, customizable, and digital readings of automotive information. These will include real-time navigation, driving data, and safety messages, with a futuristic driving experience that is safer and more convenient.

Center Stack Display: Center stack displays will more and more become interactive and intuitive with touch, gesture, and voice input potential. Total Automotive Display System global market will power multimedia, connectivity, and vehicle control technology, thereby making vehicles more user-orientated and overall providing more driver engagement.

Head-Up Display (HUD): HUDs will become more advanced by projecting vital driving data onto the windshield in a way that permits drivers to continue looking at the road. The global automotive display system market will witness HUDs providing augmented reality capabilities that enhance navigation, warning alerts, and overall driving efficiency.

Rear Seat Entertainment Display: Demand for rear seat entertainment displays will increase, particularly in luxury cars, with streaming and high-resolution screens along with interactive features. The global market for Automotive Display System will see a focus on high-end passenger experience with a blend of entertainment and connectivity as well as individual content choice.

Other: Other display formats will be flexible, bent, and multifunctional screens embedded in numerous automobile components. The Automotive Display System industry in the global world will be witnessing developments bringing smooth interaction, rich graphics, and flexible content according to the vehicle and passengers' requirements.

By Technology the market is divided into:

Liquid Crystal Display (LCD): LCD technology will continue to be sought after in the global automotive display system market because it is affordable and dependable. More sophisticated displays will provide better brightness, resolution, and power efficiency, keeping old-fashioned LCDs up to date with newer technology.

Thin-Film Transistor (TFT) LCD: TFT LCDs will continue to deliver sharp pictures and quicker response times, enabling enhanced graphics and touch functionality. The market will benefit from TFT LCDs in center stacks and instrument clusters, improving driver interaction and display readability.

OLED Display: OLED displays will be the leader in high-end applications in the market, providing improved color, contrast, and flexibility. The displays will have transparent and curved screens, making vehicles look more futuristic while providing improved visual performance.

MicroLED Display: MicroLED will be an energy-efficient, high-brightness technology in the market. MicroLED displays will be long-lived and ultra-sharp in images and will be suitable for exterior as well as interior automobile use.

Projection Display: Projection displays will provide interactive and customizable visual experiences, such as AR navigation overlays. The global automotive display system market will embrace projection displays to enhance safety and driver assist and facilitate entertainment and dynamic info display.

By Size the market is further divided into:

Small Displays (Up to 5 inches): Small displays will be used for essential vehicle information and secondary controls. The global automotive display system market will see these compact displays in digital clusters and auxiliary screens, providing clear visuals without distracting the driver.

Medium Displays (6 to 10 inches): Medium displays will become standard for center stacks and infotainment systems. The market will focus on touch, connectivity, and content integration, offering a balance between usability, visibility, and advanced functionality.

Large Displays (Above 10 inches): Large displays will define luxury and electric vehicle interiors, providing immersive interaction and multi-functional use. The market will emphasize high-resolution visuals, multiple content layers, and seamless integration with vehicle systems.

By Vehicle Type the global automotive display system market is divided as:

Passenger Cars: Passenger cars will adopt advanced displays for navigation, infotainment, and driver assistance. The global automotive display system market will drive improvements in safety, connectivity, and user experience, making modern vehicles more intuitive and responsive.

Commercial Vehicles: Commercial vehicles will integrate rugged and functional displays for fleet management, navigation, and monitoring. The market will provide durable solutions with practical features to enhance efficiency, reliability, and operational safety.

Electric Vehicles: Electric vehicles will rely on futuristic displays to manage energy consumption, navigation, and system monitoring. The market will see growth in interactive and high-tech displays that complement the digital and sustainable nature of electric vehicles.

Luxury Vehicles: Luxury vehicles will push the global automotive display system market toward premium and customizable solutions. Advanced displays will provide immersive experiences, connectivity, and aesthetic appeal, offering passengers and drivers a sophisticated and futuristic environment.

Forecast Period

2025-2032

Market Size in 2025

$26.3Billion

Market Size by 2032

$63.7Billion

Growth Rate from 2025 to 2032

13.4%

Base Year

2024

Regions Covered

North America, Europe, Asia-Pacific, South America, Middle East & Africa

By Region:

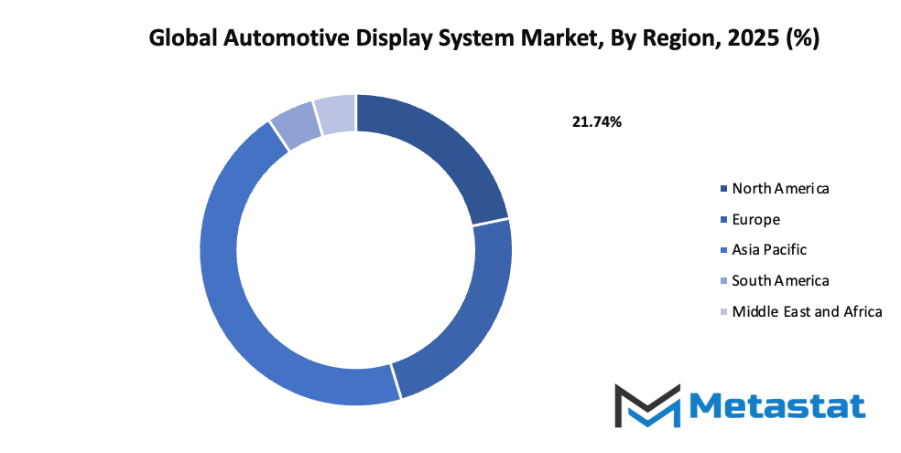

Based on geography, the global automotive display system market is divided into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

North America is further divided into the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and the Rest of Europe.

Asia-Pacific is segmented into India, China, Japan, South Korea, and the Rest of Asia-Pacific.

The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and the Rest of the Middle East & Africa.

Growth Drivers

Growing demand for advanced infotainment and connected vehicle technologies: Growing demand for advanced infotainment and connected vehicle technologies will drive the expansion of the global automotive display system market. Vehicle manufacturers are focusing on enhancing the user experience through high-resolution screens, interactive interfaces, and real-time information delivery, which will make driving safer and more engaging.

Increasing adoption of electric and autonomous vehicles requiring sophisticated display interfaces: Increasing adoption of electric and autonomous vehicles requiring sophisticated display interfaces will support the market’s growth. These vehicles depend on clear, intuitive displays for navigation, system monitoring, and passenger interaction, which will create a strong demand for innovative display solutions that integrate smoothly with emerging vehicle technologies.

Challenges and Opportunities

High cost of advanced display technologies: High cost of advanced display technologies will pose a challenge for the global automotive display system market. The investment required for high-quality screens, touch-sensitive panels, and adaptive lighting solutions may limit adoption by certain vehicle segments, making affordability a key factor for market players to address in the coming years.

Complexity in integration with existing vehicle systems: Complexity in integration with existing vehicle systems presents another challenge. Automotive Display Systems need to work seamlessly with various onboard electronics, sensors, and software platforms. Ensuring compatibility and smooth operation will require careful engineering, testing, and updates, which will be critical to achieving widespread acceptance.

Opportunities

Rising adoption of smart, customizable, and AI-enabled Automotive Display Systems: Rising adoption of smart, customizable, and AI-enabled Automotive Display Systems will offer significant growth potential. These systems will allow users to personalize interfaces, receive predictive information, and interact more efficiently with vehicles. The integration of artificial intelligence and adaptive features will shape the future of the global automotive display system market.

Competitive Landscape & Strategic Insights

The global automotive display system market is positioned to undergo remarkable transformation in the coming years. The industry is a mix of both international industry leaders and emerging regional competitors. Important competitors include LG Display Co., Ltd., Panasonic Corporation, Delphi Technologies, Robert Bosch GmbH, Visteon Corporation, Continental AG, 3M Company, Nippon Seiki Co., Ltd., Magneti Marelli S.p.A, Qualcomm Technologies Inc., Denso Corporation, Alpine Electronics, Inc., Aptiv, Valeo, AU Optronics Corp., Yazaki Corporation, Magna International Inc., and Pioneer Corporation. These companies are expected to drive innovation and shape the standards for next-generation Automotive Display Systems, as vehicles increasingly integrate digital and interactive technologies.

In the future, Automotive Display Systems will no longer serve merely as tools for presenting information; they will become central to vehicle intelligence, safety, and user experience. The push toward electric and autonomous vehicles will accelerate the adoption of advanced displays, including high-resolution digital dashboards, augmented reality head-up displays, and customizable interfaces that respond to driver and passenger preferences. Companies at the forefront will invest heavily in research and development to enhance visibility, reduce energy consumption, and ensure displays can withstand diverse environmental conditions.

Regional players are likely to influence innovation by introducing cost-effective solutions tailored to local markets, ensuring that technological advancements are accessible across a broader range of vehicles. This balance between global leaders and emerging competitors will create a dynamic environment where continuous innovation is necessary to maintain market presence. Partnerships, mergers, and strategic collaborations will shape the competitive landscape, allowing companies to combine expertise in electronics, software, and automotive engineering.

As vehicles become increasingly connected, Automotive Display Systems will serve as the interface linking drivers to intelligent transport systems, navigation aids, and real-time traffic management. The integration of artificial intelligence and machine learning into display systems will make vehicles more responsive to situational awareness, predictive maintenance alerts, and enhanced safety warnings. Future designs will focus on improving user engagement through intuitive interfaces, multi-sensory feedback, and seamless interaction with other in-car technologies.

Market size is forecast to rise from USD 26.3 Billion in 2025 to over USD 63.7 Billion by 2032. Automotive Display System will maintain dominance but face growing competition from emerging formats.

In summary, the global automotive display system market is positioned for significant growth, driven by both established industry leaders and emerging regional competitors. Companies such as LG Display Co., Ltd., Panasonic Corporation, Delphi Technologies, Robert Bosch GmbH, Visteon Corporation, Continental AG, 3M Company, Nippon Seiki Co., Ltd., Magneti Marelli S.p.A, Qualcomm Technologies Inc., Denso Corporation, Alpine Electronics, Inc., Aptiv, Valeo, AU Optronics Corp., Yazaki Corporation, Magna International Inc., and Pioneer Corporation will define the trajectory of innovation. The future will see automotive displays becoming smarter, more interactive, and integral to vehicle operation, reshaping how technology enhances safety, connectivity, and overall driving experience.

Report Coverage

This research report categorizes the global automotive display system market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global automotive display system market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global automotive display system market.

Automotive Display System Market Key Segments:

By Display Type

Instrument Cluster Display

Center Stack Display

Head-Up Display (HUD)

Rear Seat Entertainment Display

Other

By Technology

Liquid Crystal Display (LCD)

Thin-Film Transistor (TFT) LCD

OLED Display

MicroLED Display

Projection Display

By Size

Small Displays (Up to 5 inches)

Medium Displays (6 to 10 inches)

Large Displays (Above 10 inches)

By Vehicle Type

Passenger Cars

Commercial Vehicles

Electric Vehicles

Luxury Vehicles

Key Global Automotive Display System Industry Players

UK Bus & Coach Fleet Leasing, Rental and Finance Market Size, Share, Trends, 2033

UK Bus & Coach Fleet Leasing, Rental and Finance market size is valued at USD 886.4 million in 2025 and is projected to reach USD 1,442.8 million in 2033, at a CAGR of 6.3% from 2026 to 2033

UK Bus & Coach Fleet Leasing, Rental and Finance Market, UK Bus & Coach Fleet Leasing, Rental and Finance Market Size, UK Bus & Coach Fleet Leasing, Rental and Finance Market Share, UK Bus & Coach Fleet Leasing, Rental and Finance Market Analysis, UK Bus & Coach Fleet Leasing, Rental and Finance Market Growth, UK Bus & Coach Fleet Leasing, Rental and Finance Market Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market Research Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Forecast, UK Bus & Coach Fleet Leasing, Rental and Finance, UK Bus & Coach Fleet Leasing, Rental and Finance Market Research, UK Bus & Coach Fleet Leasing, Rental and Finance Industry, UK Bus & Coach Fleet Leasing, Rental and Finance Industry Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Data, UK Bus & Coach Fleet Leasing, Rental and Finance Statistics, UK Bus & Coach Fleet Leasing, Rental and Finance Market Statistics, UK Bus & Coach Fleet Leasing, Rental and Finance Industry Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market News, UK Bus & Coach Fleet Leasing, Rental and Finance Forecasts, UK Bus & Coach Fleet Leasing, Rental and Finance Market Intelligence Report

Inductive Loop Vehicle Detector market size is valued at USD 93.1 million in 2025 and is projected to reach USD 205.5 million in 2033, at a CAGR of 10.4% from 2026 to 2033.

USA EVSE Procurement Market Size, Share, Trends, 2033

USA EVSE Procurement market size is valued at USD 6.6 billion in 2025 and is projected to reach USD 52.1 billion in 2033, at a CAGR of 29.5% from 2026 to 2033.

USA EVSE Procurement Market, USA EVSE Procurement Market Size, USA EVSE Procurement Market Share, USA EVSE Procurement Market Analysis, USA EVSE Procurement Market Growth, USA EVSE Procurement Market Trends, USA EVSE Procurement Market Research Report, USA EVSE Procurement Market Forecast, USA EVSE Procurement, USA EVSE Procurement Market Research, USA EVSE Procurement Industry, USA EVSE Procurement Industry Report, USA EVSE Procurement Market Data, USA EVSE Procurement Statistics, USA EVSE Procurement Market Statistics, USA EVSE Procurement Industry Trends, USA EVSE Procurement Market Report, USA EVSE Procurement Market Trends, USA EVSE Procurement Market News, USA EVSE Procurement Forecasts, USA EVSE Procurement Market Intelligence Report

Heavy Duty Truck Wash Market Size, Share, Trends, 2033

Global Heavy Duty Truck Wash market size is valued at USD 1,240.7 million in 2025 and is projected to reach USD 1,863.2 million in 2033, at a CAGR of 5.0% from 2026 to 2033

Heavy Duty Truck Wash Market, Heavy Duty Truck Wash Market Size, Heavy Duty Truck Wash Market Share, Heavy Duty Truck Wash Market Analysis, Heavy Duty Truck Wash Market Growth, Heavy Duty Truck Wash Market Trends, Heavy Duty Truck Wash Market Research Report, Heavy Duty Truck Wash Market Forecast, Heavy Duty Truck Wash, Heavy Duty Truck Wash Market Research, Heavy Duty Truck Wash Industry, Heavy Duty Truck Wash Industry Report, Heavy Duty Truck Wash Market Data, Heavy Duty Truck Wash Statistics, Heavy Duty Truck Wash Market Statistics, Heavy Duty Truck Wash Industry Trends, Heavy Duty Truck Wash Market Report, Heavy Duty Truck Wash Market Trends, Heavy Duty Truck Wash Market News, Heavy Duty Truck Wash Forecasts, Heavy Duty Truck Wash Market Intelligence Report