Cement Plant Equipment Market Size, Share, By Equipment Type (Crushing Equipment, Raw Mills, Rotary Kilns, Preheaters, Cement Mills, Coolers, Cyclones, Conveyors, Bucket Elevators, Silos, Storage Systems, and Others), By Process Stage (Quarry Crushing, Primary Crushing, Raw Meal Preparation, Pyroprocessing, Clinkerization, Cement, Blending, Storage, Packaging, Utilities, and Environmental Systems), By Technology Level (Manual Systems, Mechanical Systems, Semi-automated Equipment, Fully Automated, and IoT-enabled Systems), By End-User Industry (Integrated Cement Plants, Grinding Units, Ready-Mix Concrete Producers, Mining Contractors, and Construction Contractors), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4584

Published

April 9, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

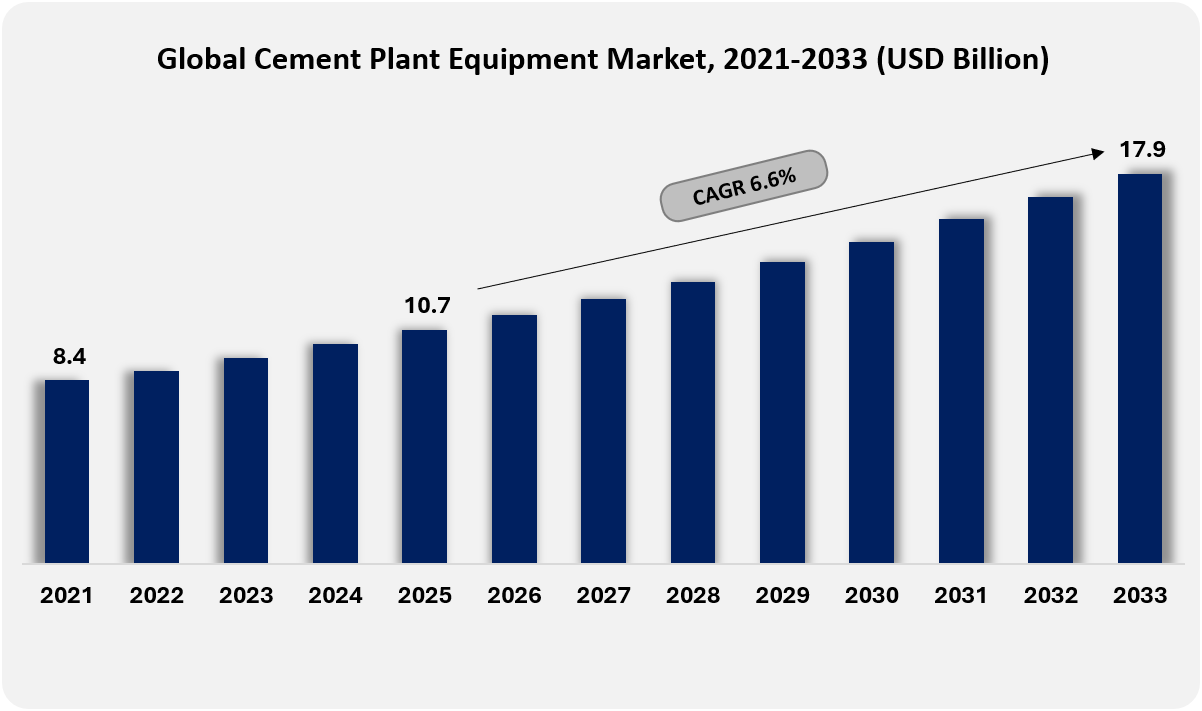

The Global Cement Plant Equipment market size was valued at USD 10.7 billion in 2025 and projected to grow at a CAGR of 6.6% during the forecast period, reaching USD 17.9 billion by 2033.

Global Cement Plant Equipment Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Cement Plant Equipment market valued at USD 10.7 billion in 2025, growing at a CAGR of 6.6% through 2033, with potential to exceed USD 17.9 billion.

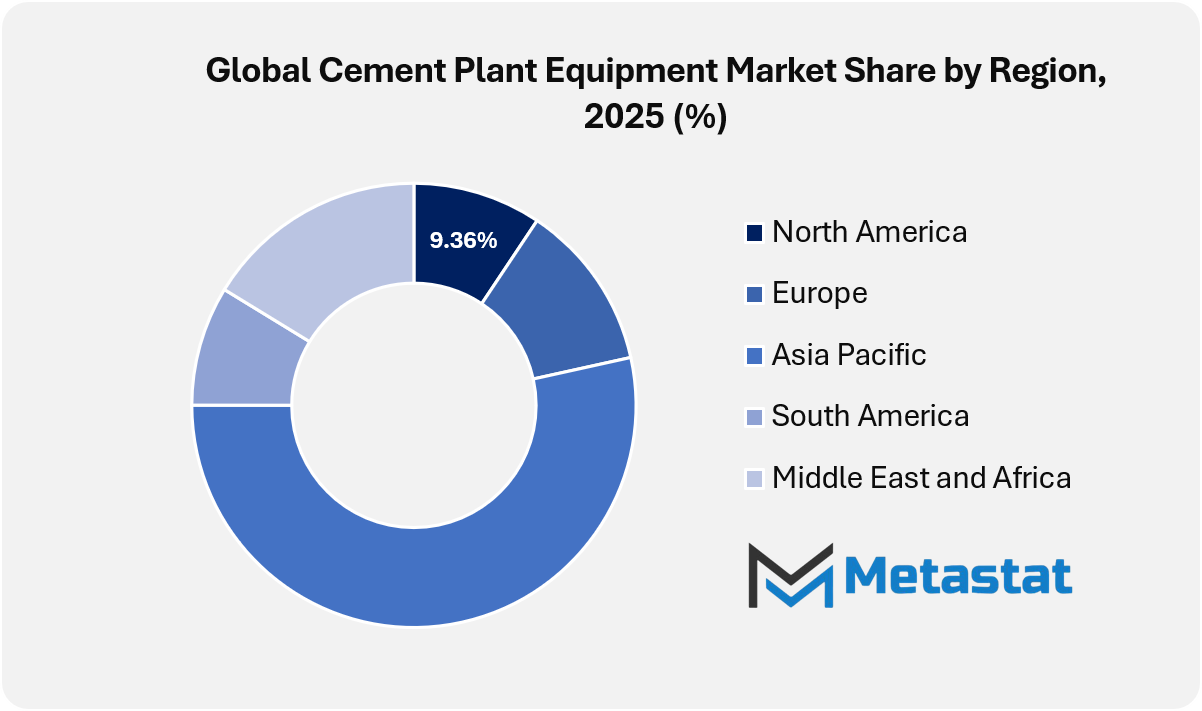

North America held 9.4% in 2025, with the United States leading regional share.

Crushing Equipment (Primary and Secondary Crushers) accounted for 12.1% market share in 2025.

Key trends driving growth: Cement capacity additions and modernization programs across infrastructure and urban development projects; Rising adoption of automation and energy-efficient machinery improving plant productivity.

Opportunities include decarbonization-driven retrofit demand across pyro lines, grinding efficiency, digital optimization, and emissions abatement systems.

Key insight: Technological advancement and sustainability-driven upgrades are reshaping demand patterns in the global cement plant equipment market.

The global cement plant equipment market within the heavy industrial manufacturing industry is projected to grow beyond the traditional boundaries that have historically been limited to kilns, mills and crushers. Future market activity is set to focus on the integrated production ecosystem where equipment expands its role into operational intelligence, emissions governance and lifecycle accountability in cement facilities. Equipment suppliers are anticipated to offer solutions spanning physical machinery and embedded systems that support plant-wide coordination and compliance expectations.

In the coming years, cement plant equipment is projected to participate directly in digital production environments through embedded sensors, adaptive control systems, and plant simulation frameworks. These developments are set to blur the line between mechanical assets and decision-support infrastructure. Instrument platforms are expected to support predictable output planning, fuel mixture adjustments, and process stability without relying on manual recalibration cycles. Such capabilities are expected to shift procurement discussions toward long-term operational alignment rather than transactional machinery replacement.

Market Dynamics

Growth Drivers:

Cement capacity additions and modernization programs across infrastructure and urban development projects.

Cement capacity additions and modernization applications throughout infrastructure and concrete development tasks drive sustained device demand. National delivery corridors, smart towns, and business parks encourage better clinker and grinding capacities. Modernization programs prioritize productivity improvement, process stability, and automation enhancements, propelling replacement demand across kilns, mills, material handling systems, and control platforms.

Rising adoption of automation and energy-efficient machinery is improving operational productivity across cement plants.

Large-scale infrastructure expansion across transportation, housing, and smart city programs supports clinker and cement capacity growth. Modernization initiatives focus on replacing aging mechanical systems with advanced furnaces, mills and material handling units. Such developments strengthen plant throughput, reduce operational inefficiencies, and position the global cement plant equipment market for continued capital inflows.

Restraints and Challenges:

Regulatory compliance costs and fuel transition complexity impacting capex timing

Regulatory and cost pressures are accelerating upgrades for energy efficiency, alternative fuels, and emissions control, while limiting investment flexibility. Compliance requirements increase capex intensity and extend approval cycles. Smaller manufacturers face financing constraints, slowing equipment replacement decisions. Cost volatility across raw materials and logistics influences procurement timing and project execution.

Maintenance complexity and unplanned downtime risk for legacy assets and mixed-technology plants

Maintenance complexity and unplanned downtime danger for legacy property and mixed-technology plants create operational constraints. Aging machinery mixed with various generations complicates spare element management and skilled labor availability. Downtime exposure increases operational threat, discouraging aggressive expansion plans and favoring cautious, phased device investment techniques.

Opportunities:

Decarbonization-driven retrofit demand across pyro lines, grinding efficiency, digital optimization, and emissions abatement systems

Decarbonization-driven retrofit demand across pyro lines, grinding efficiency, digital optimization, and emissions abatement systems creates long-term opportunity pathways. Carbon reduction objectives accelerate the adoption of opportunity fuels systems, green grinding answers, and advanced tracking gear. Retrofit hobby helps incremental device call for whilst enabling compliance, performance development, and sustainability-aligned production fashions.

Market Segmentation Analysis

The Global Cement Plant Equipment market is classified based on Equipment Type, Process Stage, Technology Level, and End-User Industry.

By Equipment Type, the market is further segmented into:

Crushing Equipment (Primary & Secondary Crushers)

Crushing Equipment (Primary & Secondary Crushers) segment is estimated at USD 1.4 billion in 2026 and is projected to reach USD 2 billion by 2033, at a CAGR of 5.3% during the forecast period.

Crushing equipment supports early-stage material reduction through controlled size management and consistent throughput. Modernization programs and capacity expansion are projected to propel demand. Advanced wear-resistant materials and energy-efficient drive systems will strengthen operational continuity while supporting cost control and output stability in large-scale cement production facilities.

Raw Mills

Raw Mills segment is estimated at USD 1.6 billion in 2026 and is projected to reach USD 2.3 billion by 2033, at a CAGR of 5.5% during the forecast period.

Raw mills enable the preparation of uniform raw meal through precise grinding and mixing. Adoption of vertical roller configurations supporting low power usage will influence market growth. Process optimization, digital condition monitoring, and high drying efficiency will improve material uniformity, supporting stable kiln feed quality and predictable downstream processing performance.

Rotary Kilns and Preheaters

Rotary Kilns and Preheaters segment is estimated at USD 3.2 billion in 2026 and is projected to reach USD 5.2 billion by 2033, at a CAGR of 7.4% during the forecast period.

Rotary kilns and preheaters form the thermal backbone of cement manufacturing. Future installations will focus on heat recovery, alternative fuel compatibility and emissions control integration. The engineering upgrades will support higher clinker production while meeting strict environmental criteria, strengthening long-term operational reliability and thermal efficiency in the production lines.

Cement Mills (Ball Mills/Vertical Roller Mills)

Cement Mills (Ball Mills/Vertical Roller Mills) segment is estimated at USD 2.3 billion in 2026 and is projected to reach USD 3.4 billion by 2033, at a CAGR of 6.0%% during the forecast period.

Cement mills control the fineness and performance consistency of the final product. Market momentum will favor vertical roller mills due to their lower energy consumption and compact layout. Predictive maintenance systems and automated process controls will increase throughput accuracy while supporting product standardization across different cement grades.

Coolers & Cyclones

Coolers & Cyclones segment is estimated at USD 1.1 billion in 2026 and is projected to reach USD 1.6 billion by 2033, at a CAGR of 5.5% during the forecast period.

Coolers and cyclones support heat exchange and material separation with high efficiency. Technology development will focus on stepped forward air distribution and thermal restoration. Enhanced designs will lessen energy loss, stabilize clinker quality, and aid compliance objectives related to gas efficiency and emission reduction tasks.

Others (Conveyors & Bucket Elevators, Silos & Storage Systems) segment is estimated at USD 1.9 billion in 2026 and is projected to reach USD 3.4 billion by 2033, at a CAGR of 8.2% during the forecast period.

Auxiliary material handling and storage systems support uninterrupted material flow and inventory control. Future investments will emphasize dirt suppression, structural sturdiness, and automation compatibility. Efficient logistics float will assist plant protection, lessen material loss, and improve coordination across interconnected manufacturing levels.

By Process Stage, the market is divided into:

Quarry and Primary Crushing

Quarry and Primary Crushing segment is projected to reach USD 2.1 billion by 2033, at a CAGR of 4.9% during the forecast period.

Quarry and primary crushing operations begin the production flow through controlled extraction and size reduction. The equipment upgrades will target fuel efficiency and output stability. Integration of monitoring tools will support predictive planning, reduce downtime risk and align raw material supply with long-term capacity strategies.

Raw Meal Preparation

Raw Meal Preparation segment is projected to reach USD 3 billion by 2033, at a CAGR of 6.2% during the forecast period.

Raw meal preparation focuses on precise proportions and grinding of raw inputs. Technological advancements will support real-time quality adjustment and moisture control. Improved system responsiveness will strengthen feed stability, enhance furnace performance, and reduce material variability in continuous production cycles.

Pyroprocessing and Clinkerization

Pyroprocessing and Clinkerization segment is projected to reach USD 5.5 billion by 2033, at a CAGR of 6.9% during the forecast period.

Pyroprocessing and clinkerization determine the quality of cement through controlled thermal changes. Future systems will adopt advanced burners, alternative fuel management and emissions mitigation modules. Operational precision will support energy optimization while maintaining clinker integrity under increasing stability expectations.

Cement Grinding and Blending

Cement Grinding and Blending segment is projected to reach USD 3.8 billion by 2033, at a CAGR of 6.2% during the forecast period.

Cement grinding and blending finalizes product characteristics through controlled fineness and composition, supported by grinding and mixing systems. Equipment development will prioritize low-energy grinding technologies and automated quality control. Continuity of the process will improve packaging readiness and market adaptability to regional demand patterns.

Storage and Packaging

Storage and Packaging segment is projected to reach USD 1.7 billion by 2033, at a CAGR of 7.3% during the forecast period.

Storage and packaging systems maintain product quality and support distribution efficiency. Future facilities will adopt automated packing lines, real-time inventory tracking, and dust-free handling solutions. Operational reliability will strengthen supply chain response and reduce product degradation during transit.

Utilities and Environmental Systems

Utilities and Environmental Systems segment is projected to reach USD 1.8 billion by 2033, at a CAGR of 9% during the forecast period.

Utilities and environmental systems maintain plant functionality and regulatory alignment. Investment focus will include waste heat recovery, water optimization, and emission filtration. Integrated management platforms will support compliance assurance while improving resource utilization efficiency across production infrastructure.

By Technology Level, the market is further divided into:

Manual/Mechanical Systems

Manual/Mechanical Systems segment is projected to reach USD 6.5 billion by 2033.

Manual and mechanical systems continue to serve cost-sensitive operations and small-scale facilities. Gradual upgrades will increase durability and safety performance. Market presence will be supported by simplicity, low capital requirements and ease of maintenance within traditional operational structures.

Semi-automated Equipment

Semi-automated Equipment segment is projected to reach USD 6.6 billion by 2033.

Semi-automated equipment balances operational control with improved efficiency. Adoption will expand through modular automation and sensor integration. Flexible upgrade paths will allow incremental modernization in medium-sized cement manufacturing units while maintaining workforce participation and process transparency.

Fully Automated/IoT-enabled Systems

Fully Automated/IoT-enabled Systems segment is projected to reach USD 4.8 billion by 2033.

Fully automated and IoT-enabled systems represent future-oriented plant architecture. Adoption will increase through demand for predictive analytics, remote monitoring and integrated decision support. Data-driven operations will strengthen productivity, reduce downtime risks and align cement manufacturing with digital industrial standards.

By End-User Industry, the Global Cement Plant Equipment market is divided as:

Integrated Cement Plants

Integrated Cement Plants segment is projected to grow at a CAGR of 5.9% during the forecast period.

Integrated cement plants drive demand for large-scale equipment through end-to-end production capabilities. Capacity expansion and sustainability mandates will shape procurement strategies. The improved plant layouts will support efficiency, regulatory alignment and long-term competitiveness in regional and global markets.

Grinding Units

Grinding Units segment is projected to grow at a CAGR of 6.2% during the forecast period.

Grinding units support regional cement supply through localized finishing operations. Demand for equipment will increase through infrastructure expansion and urban growth. Energy-efficient mills and automated blending systems will increase output consistency while reducing logistics dependency.

Ready-Mix Concrete Producers

Ready-Mix Concrete Producers segment is projected to grow at a CAGR of 8.1% during the forecast period.

Ready-mix concrete manufacturers influence downstream equipment demand through quality and quantity requirements. Equipment alignment with faster batching and consistent cement supply will strengthen operational synergy. Market growth will follow urban construction trends and infrastructure investment cycles.

Mining & Construction Contractors

Mining & Construction Contractors segment is projected to grow at a CAGR of 9.6% during the forecast period.

Mining and construction contractors support the availability of raw materials and the development of infrastructure. Equipment demand will be in line with project-based expansion and mechanization trends. Durable, mobile-enabled systems will strengthen operational flexibility across diverse site conditions and production timelines.

By Region:

Based on geography, the Global Cement Plant Equipment market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Cement Plant Equipment Market is set to expand at a CAGR of 6.6% within the forecast period, reaching a market size (TAM) of USD 1.3 billion by the end of 2033.

North America sees robust demand for cement plant equipment driven by large-scale infrastructure upgrades and sustained public funding in transportation and concrete redevelopment.

North America benefits from rising adoption of automated and energy-efficient cement manufacturing structures aimed toward enhancing productivity and regulatory compliance.

Asia Pacific provides significant opportunities because of speedy city expansion and continuous increase in residential and industrial creation activities.

Asia Pacific offers excessive potential supported via new cement potential additions and modernization of present vegetation across rising economies.

Across the Middle East, Africa, and South America, the cement plant device marketplace advances step by step through commercial diversification, increasing housing call for, and slow improvements of growing old production facilities.

Competitive Landscape and Strategic Insights

The Global Cement Plant Equipment market is shaped by steady industrial demand and the need for efficient manufacturing systems across production-oriented economies. Cement producers continue to invest in systems that improve output consistency, lowers strength use, and helps extend operational life. Equipment suppliers focus on process reliability and plant integration, addressing grinding, pyroprocessing, material management, and automation needs. Growth in infrastructure projects across growing regions helps sustained hobby in cutting-edge cement plant answers.

Several long-established companies play a central role in providing central plant structures. FLSmidth, thyssenkrupp Polysius, and KHD Humboldt Wedag maintain robust positions because of their expertise in kiln structures, turbines, and complete plant solutions. Loesche, Gebr. Pfeiffer, Christian Pfeiffer, and Claudius Peters assist cement manufacturers through advanced grinding and material processing equipment. Fives FCB and IKN GmbH contribute thermal and clinker cooling technologies that enhance plant efficiency and technique balance.

Material handling and mechanical solutions receive strong support from companies such as AUMUND Group, BEUMER Group, Haver & Boecker, and HASLER Group. These gamers guide bulk delivery, packaging, and weighing operations across the cement plant life. Magotteaux and Schenck Process cognizance on wear-resistant additives and size systems that enhance operational accuracy. Flender and WEG improve plant overall performance via power structures and motors designed for heavy-duty cement applications.

Engineering and heavy machinery suppliers expand the competitive landscape through local manufacturing and project execution strength. Kawasaki Heavy Industries, CITIC Heavy Industries, Jiangsu Pengfei Group, AGICO Cement Machinery Co., Ltd., Ashoka Group, Chanderpur Group, Gmmco Ltd., Elecon Engineering Co., Ltd. and Promac Engineering Industries Ltd. support regional cement producers with tailored equipment and turnkey solutions.

Automation and control system providers are increasingly influencing equipment decisions within cement plants. Rockwell Automation, Emerson, Honeywell International Inc., and Yokogawa Electric provide digital control, monitoring, and optimization tools that support stable plant operations. Their systems help producers improve visibility into production stages and manage energy consumption more effectively. Together, these companies define the competitive and solution-driven market structure for the global cement plant equipment.

Forecast and Future Outlook

Market size is forecast to rise from USD 10.7 billion in 2025 to over USD 17.9 billion by 2033.

The global cement plant equipment market is projected to influence financing models, insurance valuations and environmental reporting standards associated with cement assets. Equipment performance data is projected to inform asset valuation, operational risk profiling and cross-border investment decisions. Such expansion beyond physical supply limitations is projected to position cement plant equipment as a strategic industrial backbone supporting transparency, accountability and operational foresight across the cement production value chain.

This research report categorizes the Cement Plant Equipment market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Cement Plant Equipment market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Cement Plant Equipment market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 6.6% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Units

Segmentation

By Equipment Type, Process Stage, Technology Level, End-User Industry, and Region

By Region

North America (By Equipment Type, Process Stage, Technology Level, End-User Industry, and Country)

United States

Canada

Mexico

Europe (By Equipment Type, Process Stage, Technology Level, End-User Industry, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Equipment Type, Process Stage, Technology Level, End-User Industry, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Equipment Type, Process Stage, Technology Level, End-User Industry, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Equipment Type, Process Stage, Technology Level, End-User Industry, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share and Revenue

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

Import Export Trade Statistics

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Global Cement Plant Equipment market is estimated to reach USD 17.9 billion by 2033.

Asia Pacific region dominates the market.

Cement capacity additions and modernization programs across infrastructure and urban development projects and Rising adoption of automation and energy-efficient machinery improving plant productivity are key driving factors, boosting the market.

The Metastat Insights analysis shows that the North America Cement Plant Equipment market size is estimated to be USD 1.3 billion by 2033.

The Rotary Kilns and Preheaters is the leading type segment in the Global market.

The Metastat Insights study shows that the Global Cement Plant Equipment market size was USD 10.7 billion in 2025.

Top players operating in the Cement Plant Equipment industry includes FLSmidth, thyssenkrupp Polysius, KHD Humboldt Wedag, Ammann, Howden, and Kawasaki Heavy Industries.

Regulatory compliance costs and fuel transition complexity impacting capex timing will hamper the market growth within the forecast period.

The Global Cement Plant Equipment market is likely to grow at a CAGR of 6.6% over the forecast period (2026-2033).

Stage Hoist market size is valued at USD 236.3 million in 2025 and is projected to reach USD 395.3 million in 2033, at a CAGR of 6.3% from 2026 to 2033.

Global Taper Lock Bushing market is valued at USD 1,187.8 million in 2025 and is projected to reach USD 1,808.0 million in 2033, at a CAGR of 5.4% from 2026 to 2033

Europe Mini Excavators Market Size, Share, Trends, 2033

Europe Mini Excavators market size is valued at USD 2,162.9 million in 2025 and is projected to reach USD 3,004.1 million in 2033, at a CAGR of 4.2% from 2026 to 2033

Europe Mini Excavators Market, Europe Mini Excavators Market Size, Europe Mini Excavators Market Share, Europe Mini Excavators Market Analysis, Europe Mini Excavators Market Growth, Europe Mini Excavators Market Trends, Europe Mini Excavators Market Research Report, Europe Mini Excavators Market Forecast, Europe Mini Excavators, Europe Mini Excavators Market Research, Europe Mini Excavators Industry, Europe Mini Excavators Industry Report, Europe Mini Excavators Market Data, Europe Mini Excavators Statistics, Europe Mini Excavators Market Statistics, Europe Mini Excavators Industry Trends, Europe Mini Excavators Market Report, Europe Mini Excavators Market Trends, Europe Mini Excavators Market News, Europe Mini Excavators Forecasts, Europe Mini Excavators Market Intelligence Report

Global Switch Actuators market size is valued at USD 18.4 billion in 2025 and is projected to reach USD 30.6 billion in 2033, at a CAGR of 6.6% from 2026 to 2033