Gas Compressors Market Size, Share, By Compressor Type (Centrifugal Gas Compressors, Reciprocating Gas Compressors, Screw Gas Compressors, and Others), By Lubrication Type (Oil-free Compressors and Oil-lubricated Compressors), By Pressure Rating (Low Pressure, Medium Pressure, and High Pressure), By End‑Use Industry (Oil, Gas, Petrochemicals, Chemical Processing, Power Generation, Industrial Manufacturing, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4745

Published

May 20, 2026

Pages

316 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

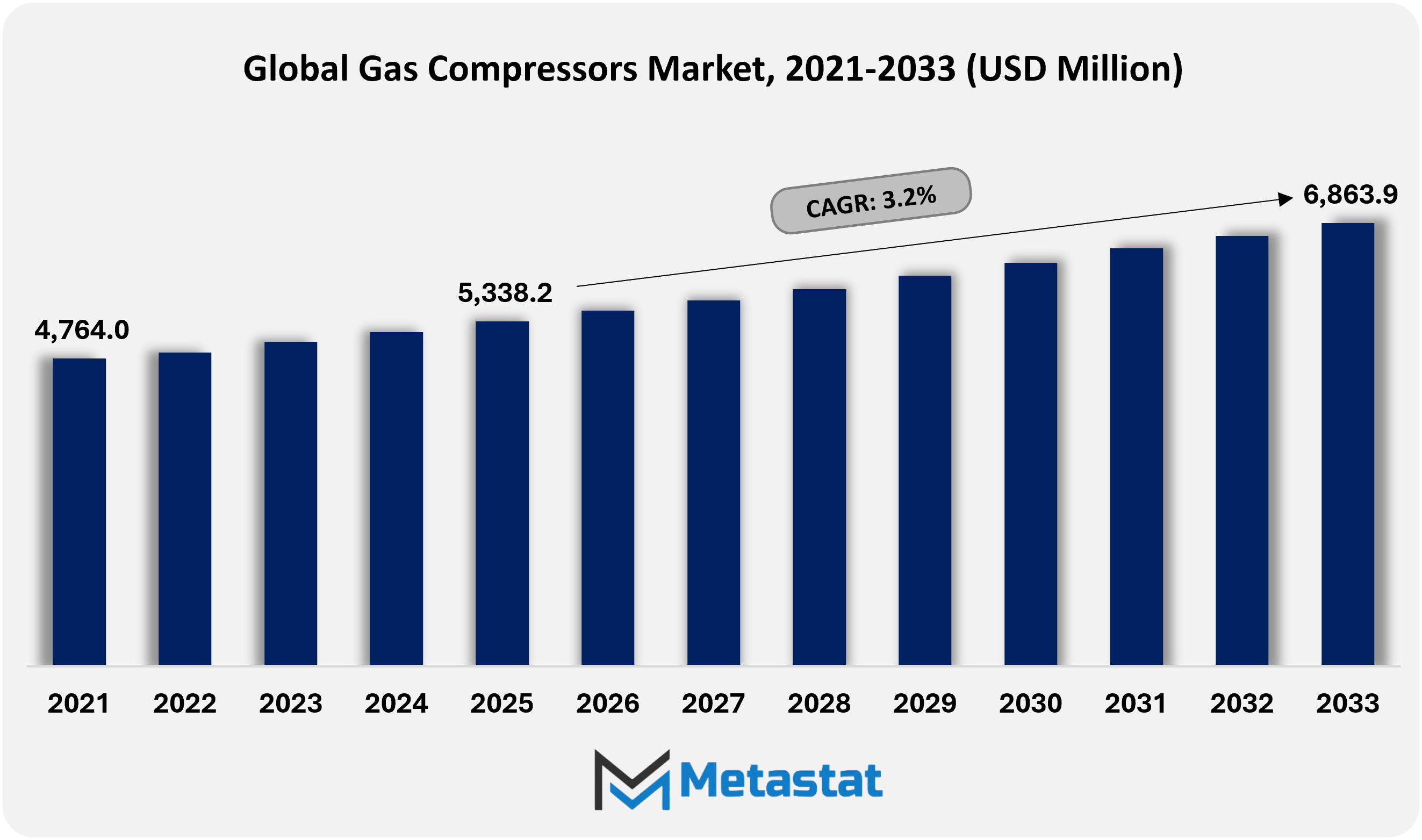

Global Gas Compressors market size is valued at USD 5,338.2 million in 2025 and projected to grow at a CAGR of 3.2% during the forecast period, reaching USD 6,863.9 million by 2033.

Global Gas Compressors Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Gas Compressors market valued at USD 5,338.2 million in 2025, growing at a CAGR of 3.2% through 2033, with potential to exceed USD 6,863.9 million.

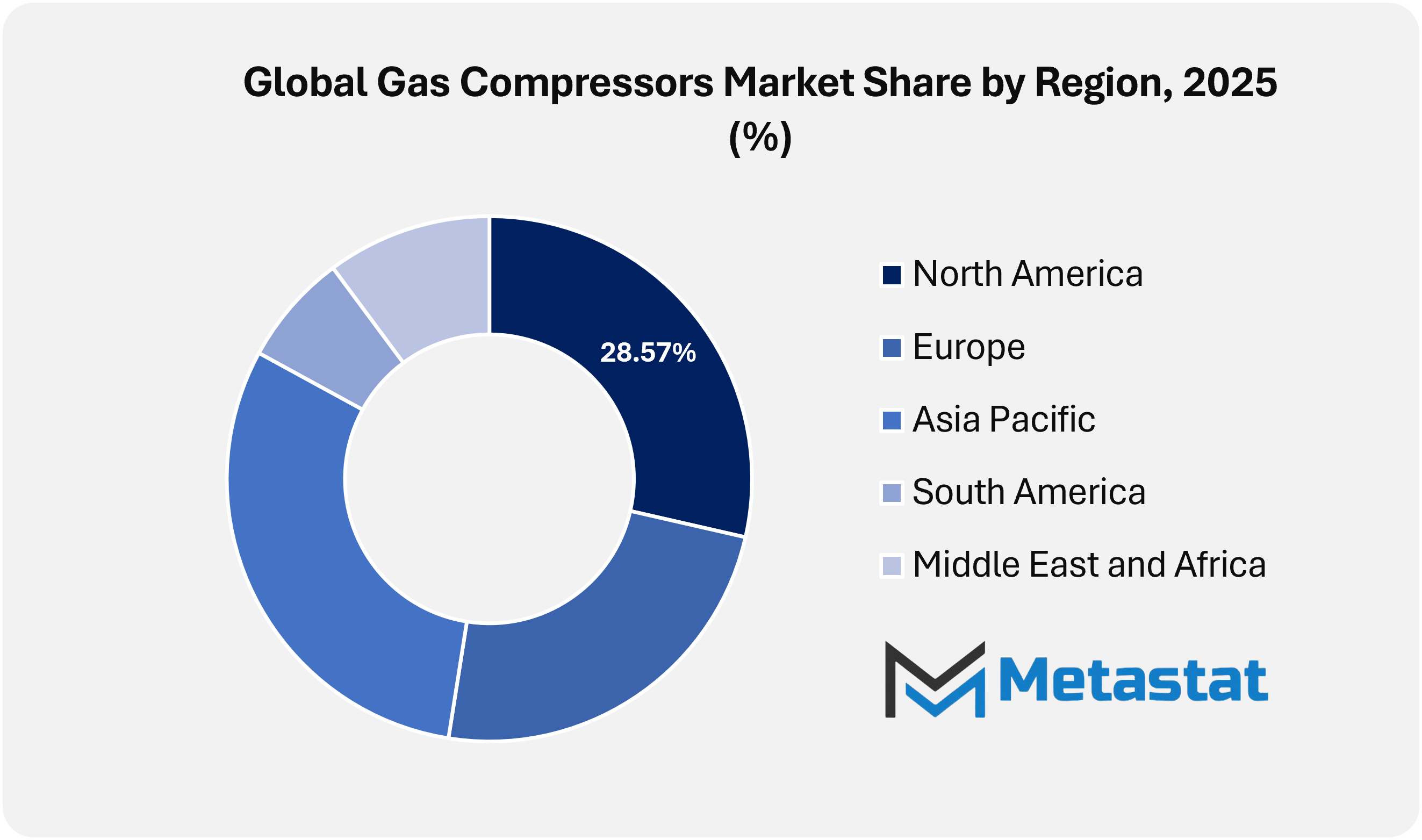

North America held a 28.6% market share in 2025, with the U.S. leading the regional market.

Centrifugal Gas Compressors segment accounted for a market share of 38.6% in 2025.

Key trends driving market growth include natural gas pipeline and LNG infrastructure expansion, along with rising industrial process throughput requirements across refining, petrochemicals, chemicals, and power generation.

Opportunities include electrified and low-emission compression packages with digital condition monitoring for hydrogen, CCUS, and renewable gas value chains.

Key insight: Rising energy demand and industrial expansion are strengthening the growth trajectory of the Global Gas Compressors market despite efficiency and emissions-related challenges.

The Global Gas Compressors market within the industrial equipment and energy systems industry is expanding beyond conventional oil and gas applications and moving toward a broader role across diversified gas handling environments. While upstream exploration, gas transmission, and pipeline operations continue to shape a major share of installed demand, the market is increasingly gaining relevance across hydrogen infrastructure, biogas upgrading facilities, carbon capture networks, and distributed industrial systems. Manufacturers are focusing on compressor platforms capable of handling variable gas compositions, fluctuating pressure conditions, and stricter emissions requirements, supporting wider deployment across evolving energy and industrial value chains.

Urban gas distribution networks are increasingly adopting compact and low-noise compression systems integrated with digital monitoring capabilities. New installations are being designed with embedded sensors, remote diagnostics, and predictive maintenance functions to improve uptime and operational visibility. Procurement priorities are gradually shifting from initial equipment cost toward lifecycle efficiency, service reliability, and performance transparency. Industrial decarbonization initiatives are also encouraging the adoption of electrically driven and oil-free compressor systems aligned with tightening environmental and operating standards.

Market Dynamics

Growth Drivers:

Natural gas pipeline and LNG build-out, including compressor stations and midstream expansions.

Expansion of natural gas pipelines, LNG terminals, and related midstream infrastructure continues to support demand across the Global Gas Compressors market. New compressor stations across transmission and gathering systems are required to maintain gas flow, pressure stability, and long-distance transport efficiency. Ongoing investment in gas export facilities, storage systems, and cross-border energy corridors is supporting demand for advanced compressor technologies designed for continuous and high-pressure operation.

Industrial process throughput needs across refining, petrochemicals, chemicals, and power generation

Rising throughput requirements across refining, petrochemicals, chemicals, and power generation are supporting compressor demand across industrial processing environments. Gas compressors play an important role in pressure control, gas transfer, and continuous process operation across production facilities handling large-scale volumes. Industrial operators are increasingly investing in reliable and energy-efficient systems that support process optimization, equipment stability, and long-duration performance across heavy-duty operating conditions.

Restraints and Challenges:

High capital cost, complex installation, and maintenance intensity across lifecycle operations

High capital cost, installation complexity, and maintenance intensity remain key challenges across the Global Gas Compressors market. Large compressor systems often require detailed engineering, foundation preparation, precision alignment, and integration with supporting equipment, which increases project timelines and upfront investment requirements. In addition, ongoing servicing needs, spare parts availability, and dependence on skilled technical personnel raise total lifecycle cost and influence purchasing decisions across end-use industries.

Energy-efficiency and emissions compliance requirements, including noise, vibration, and methane management

Energy-efficiency standards and emissions compliance requirements are placing increasing pressure on compressor manufacturers and end users. Regulations linked to methane leakage, vibration control, acoustic performance, and emissions reduction are encouraging the use of advanced sealing systems, low-loss components, and monitoring technologies. Compliance with these requirements is increasing development costs and accelerating the shift toward compressor systems designed for higher efficiency, lower emissions, and improved operational control.

Opportunities:

Electrified and low-emission compression packages with digital condition monitoring for hydrogen, CCUS, and renewable gas value chains

Electrified and low-emission compression packages integrated with digital condition monitoring present a strong opportunity across hydrogen, CCUS, and renewable gas applications. Operators are showing rising interest in compressor systems that support cleaner operation, remote diagnostics, predictive maintenance, and improved asset reliability. These capabilities are becoming increasingly important across emerging energy networks where uptime, emissions performance, and data-based asset management are critical to project viability and long-term system efficiency.

Market Segmentation Analysis

The Global Gas Compressors market is classified based on Compressor Type, Lubrication Type, Pressure Rating, and End‑Use Industry.

By Compressor Type, the market is further segmented into:

Centrifugal Gas Compressors

Centrifugal Gas Compressors segment is valued at USD 2,124.6 million in 2026 and is projected to reach USD 2,705.1 million by 2033, at a CAGR of 3.5% during the forecast period.

Centrifugal gas compressors will maintain strong adoption across large-scale processing facilities, transmission systems, and energy infrastructure projects owing to their suitability for continuous operation and high-flow applications. Their role is particularly important across gas pipelines, LNG facilities, and major industrial processing sites where stable performance and operational efficiency remain essential. Continued improvements in aerodynamic design, digital monitoring, and predictive maintenance are supporting their long-term relevance across the Global Gas Compressors market.

Reciprocating Gas Compressors

Reciprocating Gas Compressors segment is valued at USD 1,758.2 million in 2026 and is projected to reach USD 2,080.4 million by 2033, at a CAGR of 2.4% during the forecast period.

Reciprocating gas compressors will remain important across applications requiring high pressure, precise gas handling, and controlled flow conditions. These systems are widely used across gas storage, refining, chemical processing, and upstream operations where pressure intensity and process control are critical. Ongoing improvements in component durability, sealing performance, and emissions management are supporting their continued use across demanding industrial environments.

Screw Gas Compressors segment is valued at USD 1,233.7 million in 2026 and is projected to reach USD 1,606.8 million by 2033, at a CAGR of 3.8% during the forecast period.

Screw gas compressors are gaining wider acceptance across mid-scale industrial applications owing to their compact structure, stable performance, and suitability for continuous-duty operation. Their use is expanding across manufacturing plants, distributed processing facilities, and industrial systems where space efficiency and ease of operation are important. Advancements in rotor design, energy optimization, and package integration are improving their competitiveness across the Global Gas Compressors market.

Others

Others segment is valued at USD 387 million in 2026 and is projected to reach USD 471.5 million by 2033, at a CAGR of 2.9% during the forecast period.

Other compressor technologies, including diaphragm and scroll systems, are serving specialized applications that require contamination control, precision gas handling, or compact installation formats. These systems are increasingly used across laboratories, medical gas environments, research facilities, and niche industrial processes. Their role remains smaller in value terms, though their importance is increasing across highly specialized operating settings.

By Lubrication Type, the market is divided into:

Oil-free Compressors

Oil-free Compressors segment is projected to reach USD 2,228 million by 2033, at a CAGR of 4.8% during the forecast period.

Oil-free compressors will witness stronger growth across industries where gas purity, contamination control, and regulatory compliance are critical. Food processing, pharmaceuticals, electronics, and selected medical applications continue to support demand for oil-free systems that deliver clean and controlled compression. Advances in coatings, sealing technology, and efficiency enhancement are improving the performance profile of this segment across the Global Gas Compressors market.

Oil-lubricated Compressors

Oil-lubricated Compressors segment is projected to reach USD 4,635.9 million by 2033, at a CAGR of 2.5% during the forecast period.

Oil-lubricated compressors continue to hold a strong position across heavy industrial applications owing to durability, cost efficiency, and suitability for demanding operating conditions. These systems remain widely used across petrochemicals, fabrication, manufacturing, and energy processing environments where long operating hours and mechanical reliability are priorities. Improvements in lubricant management, filtration systems, and maintenance performance continue to strengthen the segment’s installed base.

By Pressure Rating, the market is further divided into:

Low Pressure

Low Pressure segment is projected to reach USD 1,615.8 million by 2033.

Low-pressure compressors are widely used across ventilation systems, packaging operations, light industrial processes, and selected utility applications where moderate compression is sufficient for stable performance. Their adoption is supported by the expansion of small and medium-scale production environments requiring reliable and energy-efficient gas handling solutions. Motor efficiency, package simplicity, and operating cost remain important purchasing considerations across this segment.

Medium Pressure

Medium Pressure segment is projected to reach USD 2,965.9 million by 2033.

Medium-pressure compressors play a central role across industrial gas distribution, processing facilities, and transmission-related applications where balanced pressure capability and consistent performance are required. They are increasingly deployed across infrastructure modernization projects, industrial plants, and utility-linked installations. The segment benefits from growing interest in remote monitoring, operational reliability, and efficient package design across mixed industrial environments.

High Pressure

High Pressure segment is projected to reach USD 2,282.2 million by 2033.

High-pressure compressors are essential across exploration, gas reinjection, hydrogen systems, chemical synthesis, and specialized industrial applications that require intense compression capability. Their importance is rising across advanced energy and process industries where safety, pressure integrity, and thermal stability are critical. Engineering improvements linked to materials, sealing performance, and system control are supporting the premium positioning of this segment.

By End-Use Industry, the Global Gas Compressors market is divided as:

Oil and Gas

Oil and Gas segment is projected to grow at a CAGR of 2.5% during the forecast period.

Oil and gas remain a major end-use segment for gas compressors owing to continued requirements across upstream extraction, midstream transport, storage, LNG infrastructure, and downstream processing. Compressor systems remain essential for maintaining flow, pressure control, and gas movement across multiple stages of the value chain. Ongoing pipeline development, LNG investment, and digital asset management adoption continue to support long-term segment demand.

Petrochemicals & Chemical Processing

Petrochemicals & Chemical Processing segment is projected to grow at a CAGR of 4.4% during the forecast period.

Petrochemical and chemical processing facilities continue to rely on gas compressors for feedstock handling, process pressure management, and continuous production operations. Capacity additions across bulk chemicals, specialty chemicals, and polymer production are supporting equipment demand across this segment. Procurement trends are increasingly shaped by efficiency improvement, process optimization, and emissions-control priorities.

Power Generation

Power Generation segment is projected to grow at a CAGR of 2.3% during the forecast period.

Power generation applications require gas compressors across turbine support systems, fuel handling processes, and selected plant operations where stable gas movement is necessary for efficient output. Rising deployment across gas-fired and hybrid power systems is supporting demand for reliable compression equipment. Segment growth is also linked to efficiency improvement initiatives and efforts to align plant operations with lower-emission generation frameworks.

Industrial Manufacturing

Industrial Manufacturing segment is projected to grow at a CAGR of 3.8% during the forecast period.

Industrial manufacturing facilities use gas compressors across material handling, pneumatic systems, automation platforms, and process support operations. Growth across automotive, metals, electronics, and general manufacturing is sustaining equipment replacement and capacity expansion activity. Smart factory integration, energy management focus, and equipment reliability remain central factors influencing purchasing decisions across this segment.

Others

Others segment is projected to grow at a CAGR of 4.4% during the forecast period.

Other end-use industries, including healthcare, mining, environmental services, and research applications, are contributing to incremental demand for gas compressors across specialized operating environments. These applications often require customized solutions suited to specific gas compositions, pressure requirements, and safety standards. The widening use of compressors across niche sectors is gradually expanding the market’s application base.

By Region:

Based on geography, the Global Gas Compressors market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Gas Compressors Market is set to expand at a CAGR of 3.2% within the forecast period, reaching a market size (TAM) of USD 1,805.9 million by the end of 2033.

North America drives the Gas Compressors market through increasing shale fuel exploration and growing LNG export infrastructure investments.

Strong modernization of pipeline networks throughout North America supports regular demand inside the Gas Compressors market.

Asia Pacific gives fundamental opportunities for the Gas Compressors market owing to rapid industrialization and developing natural gasoline consumption throughout electricity and manufacturing sectors.

Expanding city gas distribution initiatives across Asia Pacific create new opportunities inside the Gas Compressors market.

Across the Middle East, Africa, and South America, the Gas Compressors market profits momentum from upstream oil and gas growth, gasoline monetization projects, and increasing go-border pipeline trends.

Competitive Landscape and Strategic Insights

The Global Gas Compressors market remains highly important across industries that depend on gas movement, storage, and pressure management. Compressors are widely used across oil and gas, power generation, chemicals, manufacturing, LNG infrastructure, and specialized industrial applications. Market growth is supported by energy demand, industrial expansion, infrastructure investment, and the need for higher operating efficiency across gas handling systems. At the same time, emissions standards and digitalization trends are reshaping product development priorities across the competitive landscape.

Large multinational manufacturers continue to account for a significant share of the market through broad product portfolios, strong engineering capabilities, and global service networks. Companies such as Atlas Copco AB, Siemens Energy AG, Burckhardt Compression Holding AG, Ingersoll Rand Inc., Hitachi Ltd., and Kawasaki Heavy Industries, Ltd. maintain established positions across industrial, energy, and process applications. Their competitive strength is supported by technology depth, aftermarket capabilities, and long-standing relationships across major end-use sectors.

Specialized manufacturers also hold strong positions across high-pressure, oil-free, and precision gas handling applications. Ariel Corporation, Bauer Compressors Inc., HAUG Sauer Kompressoren AG, PDC Machines, Inc., Haskel International, Inc., Maximator GmbH, and RIX Industries are notable participants across niche segments requiring advanced compression performance and application-specific engineering. These players compete through product specialization, operational reliability, and alignment with demanding gas handling requirements across hydrogen, specialty gases, and industrial processing environments.

Regional and diversified players continue to strengthen competition across the broader market. Chart Industries, Inc., GEA Group AG, Kirloskar Pneumatic Company Limited, Shanghai Electric Blower Works Co., Ltd., Enerflex Ltd., Solar Turbines Incorporated, Kaishan Group Co., Ltd., Mattei Group, Gardner Denver (LeROI), GasPro Compression Corp., Euro Gas Systems, and Comptech Equipments Limited contribute to market development through localized supply capabilities, service reach, and targeted industrial offerings. Competitive intensity will remain shaped by efficiency improvement, digital monitoring integration, product reliability, and long-term aftermarket support.

Forecast and Future Outlook

Market size is forecast to rise from USD 5,338.2 million in 2025 to over USD 6,863.9 million by 2033.

Over the forecast period, the Global Gas Compressors market is expected to evolve from a conventional equipment category into a critical enabling component across broader energy, industrial, and low-emission gas infrastructure systems. Future market development will be shaped by application diversification, digital monitoring integration, energy-efficiency priorities, and the ability of manufacturers to address changing gas compositions and operating requirements. Compressor systems aligned with reliability, emissions performance, and intelligent asset management are likely to gain stronger traction across both traditional and emerging end-use environments.

This research report categorizes the Gas Compressors market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Gas Compressors market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Gas Compressors market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 3.2% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Thousand Units

Segmentation

By Compressor Type, Lubrication Type, Pressure Rating, End‑Use Industry, and Region

By Region

North America (By Compressor Type, Lubrication Type, Pressure Rating, End‑Use Industry, and Country)

United States

Canada

Mexico

Europe (By Compressor Type, Lubrication Type, Pressure Rating, End‑Use Industry, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Compressor Type, Lubrication Type, Pressure Rating, End‑Use Industry, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Compressor Type, Lubrication Type, Pressure Rating, End‑Use Industry, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Compressor Type, Lubrication Type, Pressure Rating, End‑Use Industry, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Reciprocating and rotary screw compressor technology landscape

Natural gas compression applications across upstream, midstream, LNG, and storage

OEM-aligned packaged systems, controls, and integration architecture

Service, maintenance contracting, and parts availability trends across installed base

Retrofit, uprate, and energy-efficiency upgrade pathways including electrification

Global energy-sector demand dynamics, regional investment hotspots, and project pipeline signals

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Prepositions of Leading Market Players

Stage Hoist market size is valued at USD 236.3 million in 2025 and is projected to reach USD 395.3 million in 2033, at a CAGR of 6.3% from 2026 to 2033.

Global Taper Lock Bushing market is valued at USD 1,187.8 million in 2025 and is projected to reach USD 1,808.0 million in 2033, at a CAGR of 5.4% from 2026 to 2033

Europe Mini Excavators Market Size, Share, Trends, 2033

Europe Mini Excavators market size is valued at USD 2,162.9 million in 2025 and is projected to reach USD 3,004.1 million in 2033, at a CAGR of 4.2% from 2026 to 2033

Europe Mini Excavators Market, Europe Mini Excavators Market Size, Europe Mini Excavators Market Share, Europe Mini Excavators Market Analysis, Europe Mini Excavators Market Growth, Europe Mini Excavators Market Trends, Europe Mini Excavators Market Research Report, Europe Mini Excavators Market Forecast, Europe Mini Excavators, Europe Mini Excavators Market Research, Europe Mini Excavators Industry, Europe Mini Excavators Industry Report, Europe Mini Excavators Market Data, Europe Mini Excavators Statistics, Europe Mini Excavators Market Statistics, Europe Mini Excavators Industry Trends, Europe Mini Excavators Market Report, Europe Mini Excavators Market Trends, Europe Mini Excavators Market News, Europe Mini Excavators Forecasts, Europe Mini Excavators Market Intelligence Report

Global Switch Actuators market size is valued at USD 18.4 billion in 2025 and is projected to reach USD 30.6 billion in 2033, at a CAGR of 6.6% from 2026 to 2033