Global Frozen Potato Products Market Size, Share, By Product Type (French Fries, Tikki, Potato Wedges, Potato Bites, Smileys, Hash Brown, and Others), By Distribution Channel (Business to Business, Supermarkets and Hypermarkets, Convenience Stores, Department Stores, Online, and Others), By End Use (Food Services, Retail, Quick Service Restaurants, and Households), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4560

Published

February 19, 2026

Pages

309 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

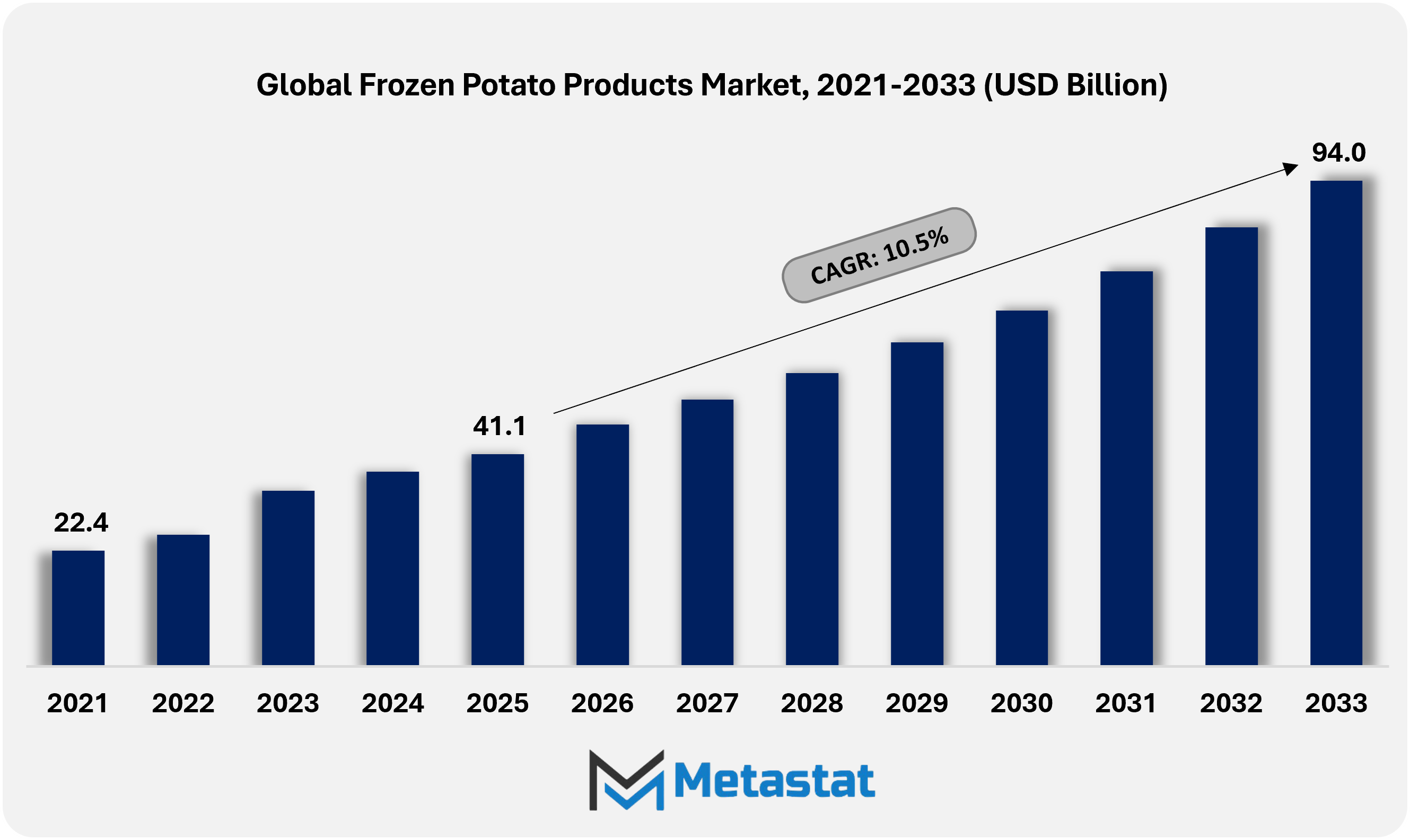

The Global Frozen Potato Products market size was valued at USD 41.1 billion in 2025. The market is projected to grow from USD 46.8 billion in 2026 to USD 94.01 billion by 2033, exhibiting a CAGR of 10.5% during the forecast period. Moreover, the Global Frozen Potato Products market was 27,813.5 kilotons in 2025 and expected to reach 65,321.2 kilotons by 2033.

Global Frozen Potato Products Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Frozen Potato Products market was valued at USD 41.1 billion in 2025 and is projected to reach USD 94.01 billion by 2033, registering a CAGR of 10.5% during 2026-2033.

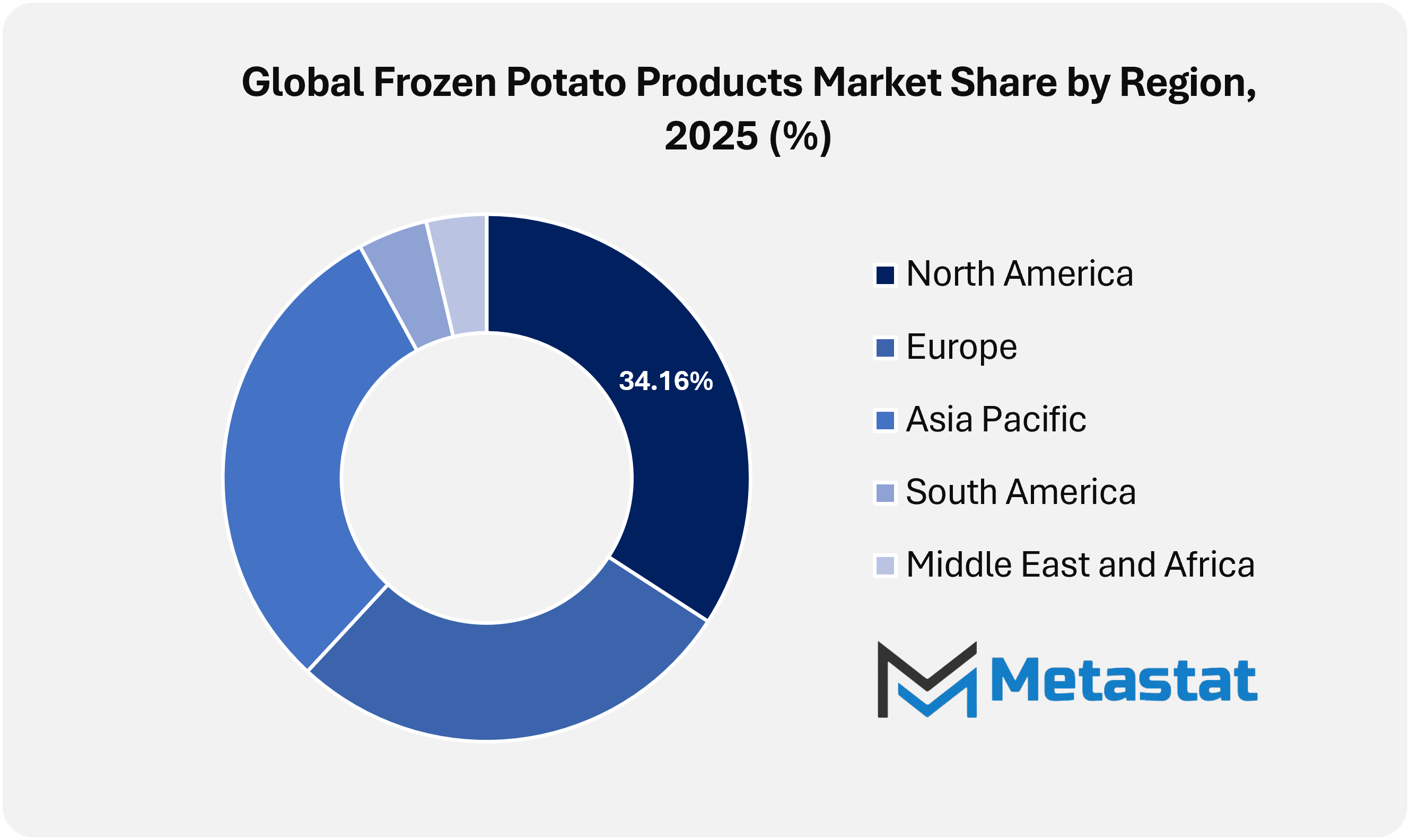

North America holds 34.2% in 2025, with the U.S. leading regional share in 2026.

French Fries segment accounts for a market share of 59.5% in 2025, supported by menu standardization across foodservice and continued process innovation.

Key trends driving growth: Rising consumption of quick-service restaurant meals across urban and semi-urban regions and increasing preference for convenient, long-shelf-life food products among working populations.

Key opportunities include growing demand for premium, seasoned, and value-added frozen potato variants.

Key insight: Urban eating habits coupled with food service expansion are driving demand for frozen potatoes, while supply volatility and cost pressures shape strategic opportunities.

The global frozen potato products market will expand far beyond traditional consumption narratives and operational boundaries within the processed food industry. In the coming years, industry participants will focus on redefining product purpose, channel relevance and consumption moments rather than reinforcing familiar supply-demand cycles. Frozen potato offerings will increasingly play a multifunctional role in foodservice innovation, private-label experimentation and culinary personalization, shaping the landscape driven by application diversity rather than volume expansion.

Product development will shift toward experiential differentiation. Manufacturers will offer formats engineered for regional cooking techniques, appliance compatibility and texture retention in different preparation environments. The frozen potato variants will be designed to perform consistently within cloud kitchens, institutional catering, premium dine-in concepts and emerging hybrid food models. Such developments will allow processors to align portfolios with localized culinary expectations while maintaining centralized production efficiency.

Market Dynamics

Growth Drivers:

Increasing consumption of quick-service restaurant food in urban and semi-urban areas

The growth of quick service restaurants will increase demand for standardized frozen potato varieties, owing to consistent quality and rapid preparation. Urbanization and the commercialization of peri-urban areas will accelerate outlet penetration, while bulk purchase agreements will gain traction. Food service establishments will focus on supply chain reliability and develop closer ties with frozen potato manufacturers.

Growing preference for convenient, long-lasting food products among the working population

Working populations will favor food solutions that support time efficiency and predictable storage life. Frozen potato products will suit busy schedules with easy preparation and reduced food wastage. Home freezers will become essential storage assets, reinforcing regular consumption patterns in metropolitan and developing employment clusters.

Restraints and Challenges:

Volatility in raw potato prices is driven by climate variability and uncertainties in agricultural yield

Climate variability disrupts crop stability, increasing raw potato price volatility. Yield uncertainty linked to rainfall and temperature swings complicates procurement planning. Rising input costs compress processing margins, requiring tighter pricing discipline and supply planning.

Higher costs of cold chain storage and transport affect profitability

Capital outlay for cold chain infrastructure is needed for storage, energy, and cold chain logistics. Transportation costs for long-distance routes are going to increase, further squeezing margins. Smaller players will face barriers to entry because of the lack of efficient cold chain infrastructure.

Opportunities:

Increasing demand for high-quality, seasoned, and value-added frozen potato varieties

There is a preference shift for differentiated products that include spice blends, specialty cuts, and texture profiles. Premium positioning allows for greater value capture. Innovation for products will focus on culinary and sensory attributes, such as use in home meal occasions and foodservice.

Market Segmentation Analysis

The Global Frozen Potato Products market is mainly classified based on Product Type, Distribution Channel, and End Use.

By Product Type, the market is further segmented into:

French Fries

French Fries segment is valued at USD 27.8 billion in 2026 and is projected to reach USD 56.3 billion by 2033, at a CAGR of 10.6% during the forecast period.

French fries will retain their dominant position due to strong acceptance in food service and home consumption. Demand will increase through menu standardization within quick service restaurants and an increasing preference for uniform tastes and textures. Improved freezing technologies will support longer shelf life, less oil absorption and consistent quality during mass preparation.

Tikki

Tikki segment is valued at USD 3.2 billion in 2026 and is projected to reach USD 6.3 billion by 2033, at a CAGR of 10.2% during the forecast period.

Tikki will gain prominence due to regional familiarity and growing interest in convenient snack formats. Increasing acceptance and institutional catering among urban families will support growth. Manufacturers will emphasize spice balance, size consistency and pan-ready formats. Frozen Tikki will increasingly serve modern retail and food service menus looking for culturally aligned offerings.

Potato Wedges

Potato Wedges segment is valued at USD 8.0 billion in 2026 and is projected to reach USD 16.5 billion by 2033, at a CAGR of 11.0% during the forecast period.

Potato wedges will continue to expand due to their premium positioning and versatility across all meal formats. Demand will benefit from preference for bold cuts and rustic textures. The advanced spice profile and oven-friendly preparation will appeal to homes and cafes. Food service operators will adopt wedges for menu differentiation and portion control benefits.

Potato Bites

Potato Bites segment is valued at USD 3.1 billion in 2026 and is projected to reach USD 6.2 billion by 2033, at a CAGR of 10.3% during the forecast period.

Growth in Potato Bites will be driven by demand for compact, shareable snacks suitable for rapid consumption. The smaller format will appeal to younger consumers and quick service outlets. The superior coating technology will ensure crispness after reheating. Retail packaging innovations will support impulse buying and freezer-to-table convenience.

Smileys

Smileys segment is valued at USD 2.4 billion in 2026 and is projected to reach USD 4.5 billion by 2033, at a CAGR of 9.4% during the forecast period.

Smileys will maintain relevance through strong appeal among younger age groups and family-oriented families. Visual familiarity will encourage repeat purchases within retail channels. Manufacturers will focus on consistent size, mild seasoning and safe ingredient profiles. Expansion into school catering and casual dining formats will drive steady demand.

Other

Others segment is valued at USD 2.3 billion in 2026 and is projected to reach USD 4.2 billion by 2033, at a CAGR of 8.9% during the forecast period.

Other frozen potato formats will experience gradual expansion driven by experimentation and specific preferences. Hash browns, stuffed variants and specialty cuts will address rising taste expectations. Limited-edition launches and regional flavors will support brand visibility. Product diversity will enable suppliers to respond effectively to local consumption patterns.

By Distribution Channel, the market is divided into:

Business to Business

Business to Business segment is projected to reach USD 37.2 billion by 2033, at a CAGR of 10.1% during the forecast period.

Business to business delivery will remain central due to bulk purchasing from food service chains, institutional kitchens and catering operators. Long-term supply contracts will ensure stability in quantities. The emphasis on standardized quality, predictable pricing and logistics reliability will strengthen supplier relationships within the commercial food preparation ecosystem.

Supermarkets and Hypermarkets

Supermarkets and Hypermarkets segment is projected to reach USD 28.5 billion by 2033, at a CAGR of 10.9% during the forecast period.

Supermarkets and hypermarkets will increase retail penetration through wider freezer space and higher consumer footfall. Private-label expansions and promotional bundling will encourage test purchases. Better packaging clarity and cooking guidance will influence purchasing decisions. The growth of organized retail in emerging economies will further strengthen the importance of the channel.

Convenience Stores

Convenience Stores segment is projected to reach USD 6.6 billion by 2033, at a CAGR of 9.7% during the forecast period.

Convenience stores will support incremental growth through accessibility and offering smaller packs. Urban density and extended operating hours will help drive purchases of frozen snacks. Compact freezers and quick checkout formats will increase visibility. Manufacturers will design packaging sizes to suit the needs of limited storage capacity and rapid consumption.

Department Stores

Department Stores segment is projected to reach USD 5.2 billion by 2033, at a CAGR of 10.6% during the forecast period.

Department stores will contribute selectively through curated frozen food sections targeting quality-focused consumers. Premium positioning and branded assortment will influence purchasing behaviour. Strategic placement near ready-to-cook categories will boost cross-category sales. Growth will depend on store modernization and advanced cold storage infrastructure.

Online

Online segment is projected to reach USD 12.9 billion by 2033, at a CAGR of 11.4% during the forecast period.

Online grocery delivery will expand rapidly, supported by platform penetration and direct-to-consumer fulfillment models. Convenience in home delivery and subscription purchase behavior will shape category momentum. Detailed product information and consumer reviews will influence purchase decisions. Temperature-controlled fulfillment will remain critical for product quality maintenance.

Others

Others segment is projected to reach USD 3.6 billion by 2033, at a CAGR of 8.4% during the forecast period.

Others distribution formats will support institutional sales, local distributors and access to specialty food stores. Regional wholesalers will meet the supply shortage in semi-urban areas. Customized supply arrangements will address fluctuations in local demand. Flexible distribution strategies will increase overall market flexibility and reach.

By End Use, the market is further divided into:

Food Services

Food Services segment is projected to reach USD 37.4 billion by 2033 and held a share of 39.3% in 2025.

Food services will represent a major consumption base driven by restaurants, cafes and catering operations. Consistency, speed of preparation and yield efficiency will guide purchasing decisions. Frozen potato products will support menu scalability and cost control. Expansion of organized food formats will drive long-term demand.

Retail

Retail segment is projected to reach USD 19.6 billion by 2033 and held a share of 21.3% in 2025.

Increase in freezer ownership and preference for ready-to-cook foods will increase retail consumption. Promotional pricing and brand familiarity will influence repeat purchases. Nutrition labeling and cooking versatility will gain importance. Retail-driven demand will support volume stability during periods of volatility in food service.

Quick Service Restaurant

Quick Service Restaurants segment is projected to reach USD 28.5 billion by 2033 and held a share of 29.4% in 2025.

Quick service restaurants will continue to shape volume growth through standardized menus and higher transaction frequency. Frozen potato products will enable operational efficiency and uniformity in taste across all stores. Global brand expansion into new territories will strengthen purchasing demand and encourage supplier capacity expansion.

Households

Households segment is projected to reach USD 8.5 billion by 2033 and held a share of 10% in 2025.

Household consumption will continue to grow due to changing food preparation habits and increasing acceptance of frozen foods. Time saving benefits and extended shelf life will attract the working population. Product innovation focused on healthy preparation methods will increase household acceptance across diverse demographics.

By Region:

Based on geography, the Global Frozen Potato Products market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Frozen Potato Products Market is set to expand at a CAGR of 10.5% within the forecast period, reaching a market size (TAM) of USD 34.6 billion by the end of 2033.

In North America, the growing preference for convenient meal formats will accelerate demand for frozen potato offerings at quick-service restaurants.

Higher penetration of cold-chain infrastructure will strengthen large-scale distribution and product sustainability in urban and semi-urban areas in the North American region.

Across the Asia Pacific region, rapid urban population expansion will create continued opportunities for the adoption of frozen potatoes in organized food retail.

The growing influence of Western-style eating habits will open long-term prospects for a diversified frozen potato portfolio in emerging economies across the Asia-Pacific region.

The Middle East, Africa and South America will collectively see sequential market traction driven by food service modernization, infrastructure investment and shifting consumer exposure to packaged frozen foods.

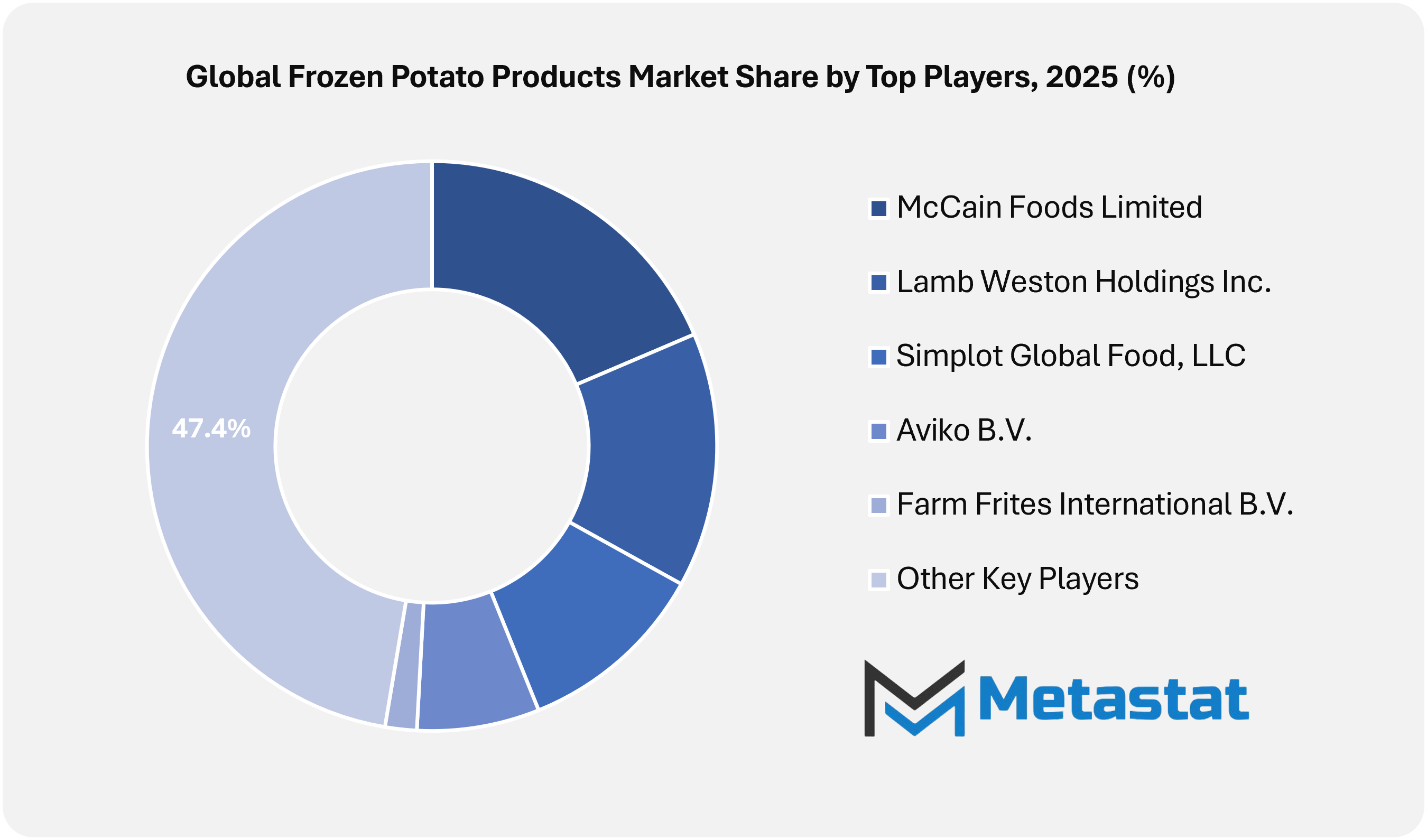

Competitive Landscape and Strategic Insights

The global frozen potato products market is witnessing steady expansion, supported by evolving food habits, wider cold storage access, and rising preference for convenient meal formats. Consumers in urban and semi-urban areas favor frozen potato products for consistent taste, long shelf life, and ease of preparation. Foodservice operators, quick service restaurants, and retail chains support category momentum via expanded menus and private-label offerings. Market participants focus on supply reliability, product quality, and efficient distribution to sustain competitiveness across channels.

Many installed groups hold sturdy positions in manufacturing and processing activities. Lamb Weston Holdings, Inc. and McCain Foods Ltd. Lead through large-scale operations and a diversified product portfolio covering fries, wedges, and specialty potato products. Farm Frites International BV and Avico B.V. Strengthen marketplace presence through partnerships with foodservice brands and local distributors. Simplot Global Foods, LLC and Cavendish Farms Corporation support market expansion by investing in processing capacity and modern freezing technology, which will improve production consistency and reduce waste.

Regional players also contribute to competitive balance and local development. Himalaya Food International Ltd. and ISKCON Balaji Foods Pvt. Ltd. focus on driving the adoption of frozen foods in price-sensitive markets. Conagra Brands, Inc. through Alexia Foods and The Kraft Heinz Company under Ore-Ida. Emphasizes premium positioning and retail branding. European producers including 11er Nahrungsmittel GmbH, Agrarfrost GmbH, Pizzoli S.p.A., Ardo NV, and Damaco Group maintain strong export activity supported by quality standards and product innovation.

Global reach is strengthened through companies such as AJC International, Inc., Del Monte International GmbH, Global Fries BV, Landun Xuemei Foods Co., Ltd. and MBRF, which support cross-border trade and private-label manufacturing. The strategic focus throughout the enterprise will be on cost control, sustainable sourcing and growth of cold chain infrastructure. Competitive dynamics suggest continued consolidation, product line expansion, and nearby expansion, shaping a strong outlook for the global frozen potato merchandise marketplace inside the coming years.

Forecast and Future Outlook

Market size is forecast to rise from USD 41.1 billion in 2025 to USD 94.01 billion by 2033.

Retail engagement strategies will shift toward narrative-led branding and selective channel positioning. Frozen potato products will rely less on price-led shelf competition; messaging around cooking versatility, cultural relevance, and eating occasions will influence purchasing behavior. Partnerships with food innovators, appliance brands, and hospitality platforms will strengthen category relevance. Market players will focus on value creation via ecosystem alignment rather than linear expansion, with competitive advantage shaped by adaptability, application insight, and cross-sector collaboration.

Frozen Potato Products Market Key Segments:

By Product Type:

French Fries

Tikki

Potato Wedges

Potato Bites

Smileys

Others

By Distribution Channel:

Business to Business

Supermarkets and Hypermarkets

Convenience Stores

Department Stores

Online

Others

By End Use:

Food Services

Retail

Quick Service Restaurants

Households

Key Global Frozen Potato Products Industry Players

This research report categorizes the Frozen Potato Products market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Frozen Potato Products market. Recent market developments and competitive strategies such as expansion, product launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Frozen Potato Products market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 10.5% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Kilotons

Segmentation

By Product Type, Distribution Channel, End Use, and Region

By Product Type

French Fries

Tikki

Potato Wedges

Potato Bites

Smileys

Others

By Distribution Channel

Business to Business

Supermarkets and Hypermarkets

Convenience Stores

Department Stores

Online

Others

By End Use

Food Services

Retail

Quick Service Restaurants

Households

By Region

North America (By Product Type, Distribution Channel, End Use, and Country)

United States

Canada

Mexico

Europe (By Product Type, Distribution Channel, End Use, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Product Type, Distribution Channel, End Use, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Product Type, Distribution Channel, End Use, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Product Type, Distribution Channel, End Use, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Prepositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

Import Export Trade Statistics Landscape for HS Code 200410 (Value, Volume, Origin Country, Export Country, and Top Suppliers)

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

The Metastat Insights study shows that the Global Frozen Potato Products market size was USD 41.1 billion in 2025.

The Global Frozen Potato Products market is likely to grow at a CAGR of 10.5% over the forecast period (2026-2033).

The Metastat Insights analysis shows that the North America Frozen Potato Products market size is estimated to be USD 34.6 billion by 2033.

French Fries is the leading product type segment in the global market.

Rising consumption of quick service restaurant meals across urban and semi-urban regions, along with increased preference for convenient, long-shelf-life food products among working populations, are key factors supporting the market.

Fluctuating raw potato prices influenced by climate variability and agricultural yield uncertainty will hamper the market growth within the forecast period.

Global Frozen Potato Products market is estimated to reach USD 94.01 billion by 2033.

Top players operating in the Frozen Potato Products industry include Lamb Weston Holdings Inc., McCain Foods Limited, Farm Frites International B.V., Aviko B.V., and Simplot Global Food.

Bulk Milk Coolers (BMC) market size is valued at USD 1,355.7 million in 2025 and projected to reach USD 2,194.3 million by 2033, growing at a CAGR of 6.2%.