Global Gum Rosin Market Size, Share, By Product (X, WW, WG, N, M, K, and Other Products), By Type (Fractionated Gum Rosin and Standard Gum Rosin), By Source (Longleaf Pine and Slash Pine), By Application (Paper Sizing, Adhesives, Rubber, Tire industries, Paints, Varnishes, Printing Inks, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4692

Published

April 29, 2026

Pages

314 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

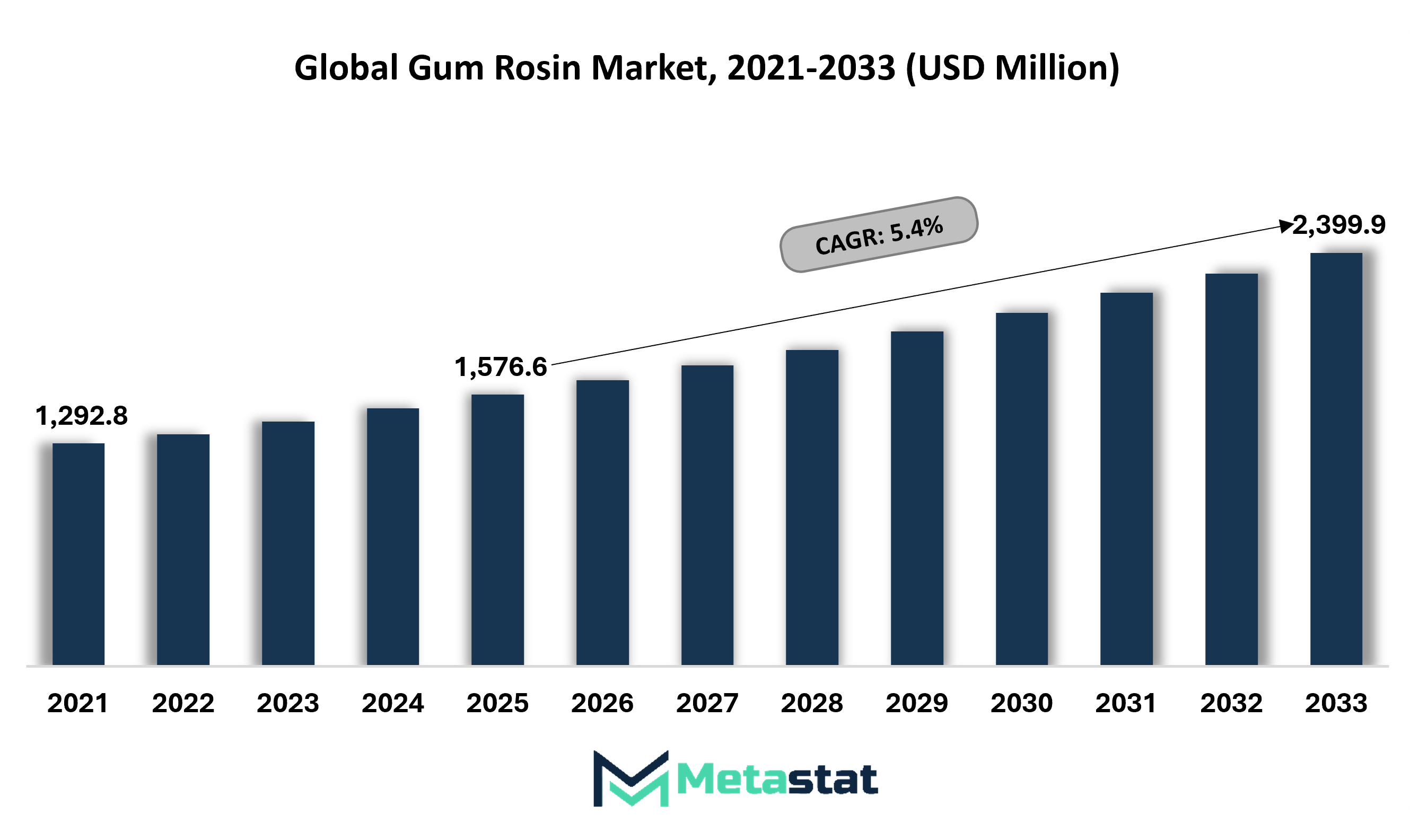

Global Gum Rosin market size is valued at USD 1,576.6 million in 2025 and projected to grow at a CAGR of 5.4% during the forecast period, reaching USD 2,399.9 million by 2033.

Global Gum Rosin Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

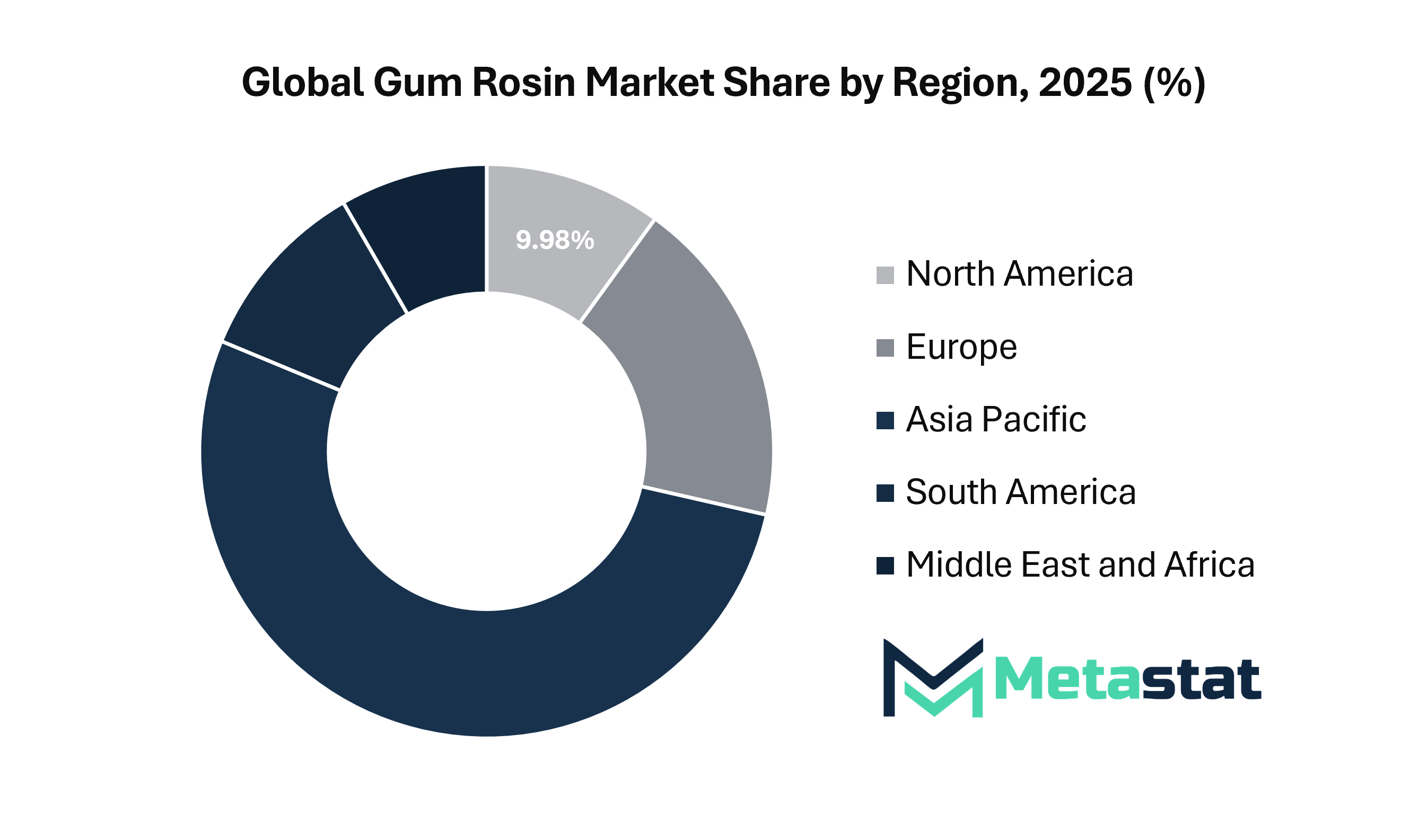

North America holds 10.0% in 2025 with US leading the market share in 2025.

X segment account for a market share of 10.5% in 2025.

Key trends driving growth: Expanding demand from adhesives and sealants industry propels consumption of gum rosin as a key tackifier, along with increased use in printing inks and coatings supports market growth driven by packaging and publishing sectors.

Opportunities include rising preference for bio-based and sustainable materials creates growth avenues for gum rosin in green chemical formulations.

Key insight: Rising shift toward bio-based and sustainable materials is steadily increasing global demand for gum rosin across adhesives, packaging, and industrial applications.

The Global Gum Rosin market is witnessing steady expansion, supported by rising demand across adhesives, rubber processing, coatings, printing inks, and paper sizing applications. Derived from pine resin, gum rosin plays an important role in industrial value chains where binding, tackifying, stabilizing, and film-forming properties remain critical. Industrial consumption patterns are shifting toward bio-based raw materials, strengthening the position of gum rosin in sustainable manufacturing processes. Producers are focusing on refined extraction methods, improved grade consistency, and better processing efficiency to meet evolving performance requirements across downstream industries.

The Global Gum Rosin market is also influenced by supply-side dynamics linked to forestry resources, climatic conditions, and regional resin harvesting practices. Countries with strong pine resin production capabilities are shaping global supply trends, while consumption continues to rise across major manufacturing hubs. The market is gradually moving toward higher-value applications, where product purity, color consistency, and formulation precision determine usability. Rising focus on performance-grade materials is encouraging investments in processing infrastructure, quality control systems, and long-term supply chain stability.

Market Dynamics

Growth Drivers:

Expanding demand from adhesives and sealants industry propels consumption of gum rosin as a key tackifier.

Strong expansion in adhesives and sealants production is increasing reliance on gum rosin owing to its effective tackifying performance and compatibility with diverse formulations. Future industrial activity across construction, packaging, woodworking, and automotive applications will support stable consumption patterns. Continued product integration in pressure-sensitive adhesives, hot-melt adhesives, and sealant formulations will strengthen long-term demand across the Global Gum Rosin Market.

Increased use in printing inks and coatings supports market growth driven by packaging and publishing sectors.

Rising packaging production, labeling activity, and commercial printing volumes are increasing the requirement for high-quality printing inks and surface coatings, where gum rosin supports adhesion, gloss, drying performance, and pigment dispersion. Continuous innovation in flexible packaging, corrugated packaging, and label printing will expand application scope. Increased use of rosin-based resins in ink and coating formulations will create sustained growth momentum across commercial printing segments.

Restraints and Challenges:

Price volatility of raw pine resin impacts cost stability and supply consistency.

Fluctuating availability and pricing of pine resin create uncertainty in production planning, procurement cycles, and margin management. Variations linked to climatic conditions, forestry output, labor availability, and harvesting intensity affect overall supply chains, leading to unstable pricing structures. Long-term stability in the Global Gum Rosin Market will depend on improved sourcing strategies, sustainable forestry practices, and stronger raw material management systems.

Availability of synthetic substitutes limits dependency on natural gum rosin in industrial applications.

Growing adoption of synthetic alternatives with controlled properties limits reliance on natural gum rosin across several industrial applications. Petroleum-based tackifiers, synthetic resins, and modified polymers offer uniform performance, scalable production, and predictable formulation behavior, creating competitive pressure. Sustained relevance in the Global Gum Rosin Market will depend on differentiation through quality consistency, renewable origin, functional performance, and environmental benefits.

Opportunities:

Rising preference for bio-based and sustainable materials creates growth avenues for gum rosin in green chemical formulations.

Increasing regulatory focus on sustainability, lower-emission materials, and environmental safety supports the transition toward bio-based materials in industrial manufacturing. Gum rosin aligns with green chemistry initiatives owing to its renewable origin, broad functional utility, and lower dependence on fossil-based inputs. Future product development in green coatings, adhesives, tackifier resins, and specialty formulations will unlock significant expansion opportunities in the Global Gum Rosin Market.

Market Segmentation Analysis

The Global Gum Rosin market is classified based on Product, Type, Source, and Application.

By Product, the market is further segmented into:

X Grade

X segment is valued at USD 174.7 million in 2026 and is projected to reach USD 207.9 million by 2033, at a CAGR of 2.5% during the forecast period.

X Grade in the Gum Rosin Market reflects steady demand driven by industrial consistency, functional reliability, and predictable performance across manufacturing lines. The segment will expand gradually, supported by quality standardization, improved processing methods, and rising preference in specialty formulations where uniformity and stability influence long-term procurement decisions among end-use industries.

WW Grade

WW segment is valued at USD 415.9 million in 2026 and is projected to reach USD 643.9 million by 2033, at a CAGR of 6.4% during the forecast period.

WW Grade holds a strong position in the Gum Rosin Market owing to its superior clarity, color quality, and suitability for premium applications. The segment is set to benefit from rising use in coatings, adhesives, inks, and specialty resin formulations, where high-grade material enhances output performance, durability, and product finish across multiple industrial environments.

WG Grade

WG segment is valued at USD 358.4 million in 2026 and is projected to reach USD 539.2 million by 2033, at a CAGR of 6% during the forecast period.

WG Grade continues to attract attention in the Gum Rosin Market owing to its balanced properties between cost and performance. Manufacturers will increase focus on WG production to meet mid-range industrial demand, particularly across adhesives, rubber processing, paints, and coatings. Cost efficiency combined with acceptable quality will continue to influence purchasing decisions across regional markets.

N Grade

N segment is valued at USD 225.4 million in 2026 and is projected to reach USD 303.1 million by 2033, at a CAGR of 4.3% during the forecast period.

N Grade serves niche applications in the Gum Rosin Market, offering functional value where ultra-high clarity is not a critical requirement. Future demand will remain stable, supported by industries seeking economical solutions without compromising core chemical performance. Adoption will remain relevant across developing economies, where production cost sensitivity strongly influences material selection trends.

M Grade

M segment is valued at USD 171.3 million in 2026 and is projected to reach USD 236 million by 2033, at a CAGR of 4.7% during the forecast period.

M Grade contributes to the Gum Rosin Market through moderate-quality offerings suitable for various industrial uses. Consumption will remain stable owing to adaptability across sectors such as printing inks, coatings, paper sizing, and adhesives. Moderate performance specifications, operational efficiency, and controlled expenditure will support continued use across production units.

K Grade

K segment is valued at USD 138.3 million in 2026 and is projected to reach USD 187.9 million by 2033, at a CAGR of 4.5% during the forecast period.

K Grade in the Gum Rosin Market caters to lower-grade applications, often preferred in cost-driven industries. The segment’s growth potential remains linked with expansion in emerging markets, where affordability remains a major purchasing criterion. Manufacturers will optimize production processes to maintain competitive pricing while ensuring acceptable performance for basic industrial requirements.

Others

Other Products segment is valued at USD 176.0 million in 2026 and is projected to reach USD 281.9 million by 2033, at a CAGR of 7% during the forecast period.

Other product categories in the Gum Rosin Market include customized, modified, and blended variants designed for specific industrial requirements. Innovation and product diversification will support future growth, with manufacturers focusing on tailored solutions that align with evolving application needs across adhesives, coatings, inks, rubber processing, and specialty chemical sectors.

By Type, the market is divided into:

Fractionated Gum Rosin

Fractionated Gum Rosin segment is projected to reach USD 990.2 million by 2033, at a CAGR of 6.5% during the forecast period.

Fractionated Gum Rosin represents a refined segment in the Gum Rosin Market, offering higher purity, controlled composition, and specialized performance properties. Adoption is projected to rise with increased use in high-performance applications, where consistent chemical composition improves formulation efficiency and end-product quality, particularly across advanced adhesive systems, specialty coatings, inks, and modified resin formulations.

Standard Gum Rosin

Standard Gum Rosin segment is projected to reach USD 1,409.7 million by 2033, at a CAGR of 4.7% during the forecast period.

Standard Gum Rosin continues to dominate the Gum Rosin Market owing to broad applicability, cost-effectiveness, and established use across major industrial applications. Industrial reliance on standard grades supports consistent demand, particularly in large-scale production environments where steady supply, manageable pricing, and functional versatility remain vital for operational continuity.

By Source, the market is further divided into:

Longleaf Pine

Longleaf Pine segment is projected to reach USD 1,024 million by 2033.

Longleaf Pine serves as a traditional source in the Gum Rosin Market and is recognized for producing high-quality resin. Future supply trends will depend on sustainable forestry practices, resin yield improvement, and resource management. Growing emphasis on environmental responsibility will influence sourcing strategies across global producers and suppliers.

Slash Pine

Slash Pine segment is projected to reach USD 1,375.8 million by 2033.

Slash Pine contributes significantly to the Gum Rosin Market owing to higher resin yield and efficient harvesting potential. Market growth for Slash Pine-based rosin will strengthen with improved extraction technologies, supporting large-scale production and meeting rising industrial demand without major cost escalation.

By Application, the Global Gum Rosin market is divided as:

Paper Sizing

Paper Sizing segment is projected to grow at a CAGR of 5.7% during the forecast period.

Paper sizing remains an important application area in the Gum Rosin Market, supported by its role in improving paper strength, water resistance, and printability. Future consumption will align with packaging industry expansion, where durability, surface quality, and performance consistency remain critical. Rising use of paper-based materials across several sectors will support continued application growth.

Adhesives

Adhesives segment is projected to grow at a CAGR of 6.2% during the forecast period.

Adhesives remain a major application area in the Gum Rosin Market, supported by expanding construction, packaging, woodworking, footwear, and automotive industries. Rising requirement for strong bonding agents and bio-based formulations will reinforce consumption. Manufacturers are focusing on improving adhesive performance through refined rosin integration and modified rosin derivatives.

Rubber and Tire Industries

Rubber and Tire industries segment is projected to grow at a CAGR of 4.7% during the forecast period.

Rubber and tire industries rely on gum rosin for improving elasticity, processing efficiency, tack, and compound performance. Rising automotive production and replacement tire consumption will support continued use, with manufacturers seeking materials that enhance durability and overall product performance under varying operating conditions.

Paints and Varnishes

Paints and Varnishes segment is projected to grow at a CAGR of 4.4% during the forecast period.

Paints and varnishes benefit from gum rosin through improved gloss, adhesion, film formation, and finish quality. Increasing construction, renovation, and infrastructure activities will support demand, with producers focusing on formulations that enhance surface protection, durability, and aesthetic appeal across residential, commercial, and industrial applications.

Printing Inks

Printing Inks segment is projected to grow at a CAGR of 4.1% during the forecast period.

Printing inks support steady demand in the Gum Rosin Market owing to rosin’s role in improving ink consistency, adhesion, gloss, pigment dispersion, and drying properties. Growth prospects remain linked to packaging, labeling, and publishing industries, where print quality, production efficiency, and material performance continue to influence formulation choices.

Others

Others segment is projected to grow at a CAGR of 6.1% during the forecast period.

Other applications in the Gum Rosin Market include niche industrial uses where specific chemical properties provide functional benefits. Future expansion will emerge from innovation, cross-industry integration, and development of modified rosin products. Increasing research efforts focused on identifying new application areas and improving performance characteristics will support diversification across specialty sectors.

By Region:

Based on geography, the Global Gum Rosin market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

Strong demand from packaging, construction, adhesives, coatings, and printing ink industries supports the Gum Rosin market in North America.

Europe holds a steady position in the Gum Rosin market, supported by established demand from adhesives, printing inks, coatings, paper sizing, rubber processing, and specialty chemical applications.

Asia-Pacific offers strong growth opportunities through considerable raw material availability, expanding industrial demand, and large-scale manufacturing activity.

Across the Middle East, Africa, and South America, the Gum Rosin market is expanding steadily, supported by growing industrialization, improved trade networks, and increasing demand for adhesives, coatings, inks, and rubber processing materials.

Competitive Landscape and Strategic Insights

The Global Gum Rosin Market includes a broad network of producers operating across major resin-producing and industrial regions. Established manufacturers support stable production capacity, while regional players add supply flexibility and local market reach. Together, these companies create a balanced competitive structure where scale, sourcing access, product consistency, and application specialization play important roles in meeting demand from adhesives, inks, coatings, rubber, and paper industries.

Key Global Gum Rosin industry players represent a mix of long-standing technical expertise and growing participation from emerging resin-producing markets. Companies such as Dérivés Résiniques et Terpéniques (DRT) and Harima Chemicals Group, Inc. bring strong technical capabilities and an extensive product range, supporting their stable market position. Arakawa Chemical Industries, Ltd. and Lawter, Inc. continue to focus on quality, formulation consistency, and application support, which strengthens long-term customer relationships. At the same time, companies including Ambar Florestal Ltda and Pinus Brasil Agro Florestal Ltda highlight the strategic importance of raw material access in pine-rich regions.

Producers based in Brazil and nearby regions, including FLORPINUS Indústria Química and Irani Papel e Embalagem S.A., benefit from natural supply advantages linked to forestry resources. Their operations often align closely with resin extraction and forestry activities, helping maintain cost control and steady output. Grupo Resinas Brasil and similar companies strengthen regional supply chains and improve distribution across local markets. In Europe, Luresa Resinas, S.L. and United Resins, S.A. continue to serve customers with a focus on product reliability, regulatory compliance, and consistent quality standards.

Asian manufacturers maintain a strong role in the Global Gum Rosin Market, supported by rising industrial demand and access to resin-producing resources. Companies such as PT. NASCO, PT. GUM ROSIN INDONESIA, and PT. Naval Overseas play an active role in meeting domestic and export requirements. CV. INDONESIA PINUS and PT Kharisma Satya Jaya contribute through steady production, while Perum Perhutani supports raw material availability. PT Global Sejahtera Perkasa adds further capacity in the region, helping maintain supply balance.

In China, Wuzhou Sun Shine Forestry and Chemicals Co., Ltd. of Guangxi, Forestar Chemical Co., Ltd., and Guilin Songquan Forest Chemical Co., Ltd. continue to expand their presence through large-scale operations. Their output supports both domestic consumption and global trade. Across these participants, steady demand and access to raw materials will shape future market growth, while competition will encourage improvements in operating efficiency, grade consistency, supply reliability, and product quality.

Forecast and Future Outlook

Market size is forecast to rise from USD 1,576.6 million in 2025 to over USD 2,399.9 million by 2033.

The Global Gum Rosin market is projected to maintain steady growth, supported by rising industrial consumption and increasing preference for renewable raw materials. Manufacturers will continue to focus on product quality, grade consistency, supply chain resilience, and application expansion across adhesives, inks, coatings, rubber processing, and paper sizing industries.

This research report categorizes the Gum Rosin market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Gum Rosin market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Gum Rosin market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 5.4% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Kilotons

Segmentation

By Product, Type, Source, Application, and Region

By Region

North America (By Product, Type, Source, Application, and Country)

United States

Canada

Mexico

Europe (By Product, Type, Source, Application, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Product, Type, Source, Application, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Product, Type, Source, Application, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Product, Type, Source, Application, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Bangladesh Flavours and Fragrances Market Size, Share, Trends, 2033

Bangladesh Flavours and Fragrances market size is valued at USD 793.9 million in 2025 and is projected to reach USD 1,447.9 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Bangladesh Flavours and Fragrances Market, Bangladesh Flavours and Fragrances Market Size, Bangladesh Flavours and Fragrances Market Share, Bangladesh Flavours and Fragrances Market Analysis, Bangladesh Flavours and Fragrances Market Growth, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market Research Report, Bangladesh Flavours and Fragrances Market Forecast, Bangladesh Flavours and Fragrances, Bangladesh Flavours and Fragrances Market Research, Bangladesh Flavours and Fragrances Industry, Bangladesh Flavours and Fragrances Industry Report, Bangladesh Flavours and Fragrances Market Data, Bangladesh Flavours and Fragrances Statistics, Bangladesh Flavours and Fragrances Market Statistics, Bangladesh Flavours and Fragrances Industry Trends, Bangladesh Flavours and Fragrances Market Report, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market News, Bangladesh Flavours and Fragrances Forecasts, Bangladesh Flavours and Fragrances Market Intelligence Report

Biocatalysis and Enzyme Biocatalysts Market Size, Share, Trends, 2033

Biocatalysis and Enzyme Biocatalysts market size is valued at USD 737.8 million in 2025 and is projected to reach USD 1,221.0 million in 2033, at a CAGR of 6.5% from 2026 to 2033.

Biocatalysis and Enzyme Biocatalysts Market, Biocatalysis and Enzyme Biocatalysts Market Size, Biocatalysis and Enzyme Biocatalysts Market Share, Biocatalysis and Enzyme Biocatalysts Market Analysis, Biocatalysis and Enzyme Biocatalysts Market Growth, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market Research Report, Biocatalysis and Enzyme Biocatalysts Market Forecast, Biocatalysis and Enzyme Biocatalysts, Biocatalysis and Enzyme Biocatalysts Market Research, Biocatalysis and Enzyme Biocatalysts Industry, Biocatalysis and Enzyme Biocatalysts Industry Report, Biocatalysis and Enzyme Biocatalysts Market Data, Biocatalysis and Enzyme Biocatalysts Statistics, Biocatalysis and Enzyme Biocatalysts Market Statistics, Biocatalysis and Enzyme Biocatalysts Industry Trends, Biocatalysis and Enzyme Biocatalysts Market Report, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market News, Biocatalysis and Enzyme Biocatalysts Forecasts, Biocatalysis and Enzyme Biocatalysts Market Intelligence Report

Malaysia Tyre Pyrolysis Products Market Size, Share, Trends, 2033

Malaysia Tyre Pyrolysis Products market size is valued at USD 205.9 million in 2025 and is projected to reach USD 421.8 million in 2033, at a CAGR of 9.3% from 2026 to 2033.

Malaysia Tyre Pyrolysis Products Market, Malaysia Tyre Pyrolysis Products Market Size, Malaysia Tyre Pyrolysis Products Market Share, Malaysia Tyre Pyrolysis Products Market Analysis, Malaysia Tyre Pyrolysis Products Market Growth, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market Research Report, Malaysia Tyre Pyrolysis Products Market Forecast, Malaysia Tyre Pyrolysis Products, Malaysia Tyre Pyrolysis Products Market Research, Malaysia Tyre Pyrolysis Products Industry, Malaysia Tyre Pyrolysis Products Industry Report, Malaysia Tyre Pyrolysis Products Market Data, Malaysia Tyre Pyrolysis Products Statistics, Malaysia Tyre Pyrolysis Products Market Statistics, Malaysia Tyre Pyrolysis Products Industry Trends, Malaysia Tyre Pyrolysis Products Market Report, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market News, Malaysia Tyre Pyrolysis Products Forecasts, Malaysia Tyre Pyrolysis Products Market Intelligence Report

Near Infrared (NIR) Analyzer Market Size, Share, Trends, 2033

Near Infrared (NIR) Analyzer market size is valued at USD 855.3 million in 2025 and is projected to reach USD 1,813.6 million in 2033, at a CAGR of 9.9% from 2026 to 2033.

Near Infrared (NIR) Analyzer Market, Near Infrared (NIR) Analyzer Market Size, Near Infrared (NIR) Analyzer Market Share, Near Infrared (NIR) Analyzer Market Analysis, Near Infrared (NIR) Analyzer Market Growth, Near Infrared (NIR) Analyzer Market Trends, Near Infrared (NIR) Analyzer Market Research Report, Near Infrared (NIR) Analyzer Market Forecast, Near Infrared (NIR) Analyzer, Near Infrared (NIR) Analyzer Market Research, Near Infrared (NIR) Analyzer Industry, Near Infrared (NIR) Analyzer Industry Report, Near Infrared (NIR) Analyzer Market Data, Near Infrared (NIR) Analyzer Statistics, Near Infrared (NIR) Analyzer Market Statistics, Near Infrared (NIR) Analyzer Industry Trends, Near Infrared (NIR) Analyzer Market Report, Near Infrared (NIR) Analyzer Market Trends, Near Infrared (NIR) Analyzer Market News, Near Infrared (NIR) Analyzer Forecasts, Near Infrared (NIR) Analyzer Market Intelligence Report