Hard Chemical-Mechanical Polishing (CMP) Pad Market

Global Hard Chemical-Mechanical Polishing (CMP) Pad Market Size, Share, By Type (Polyurethane CMP Pads, and Non-polyurethane CMP Pads), By Wafer Size (200mm Wafer, 300mm Wafer, and Others) By Application (Memory Devices, Logic Devices, MEMS Devices, and Others), By End-User (Semiconductor Industry, Electronics Industry, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4762

Published

May 25, 2026

Pages

314 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

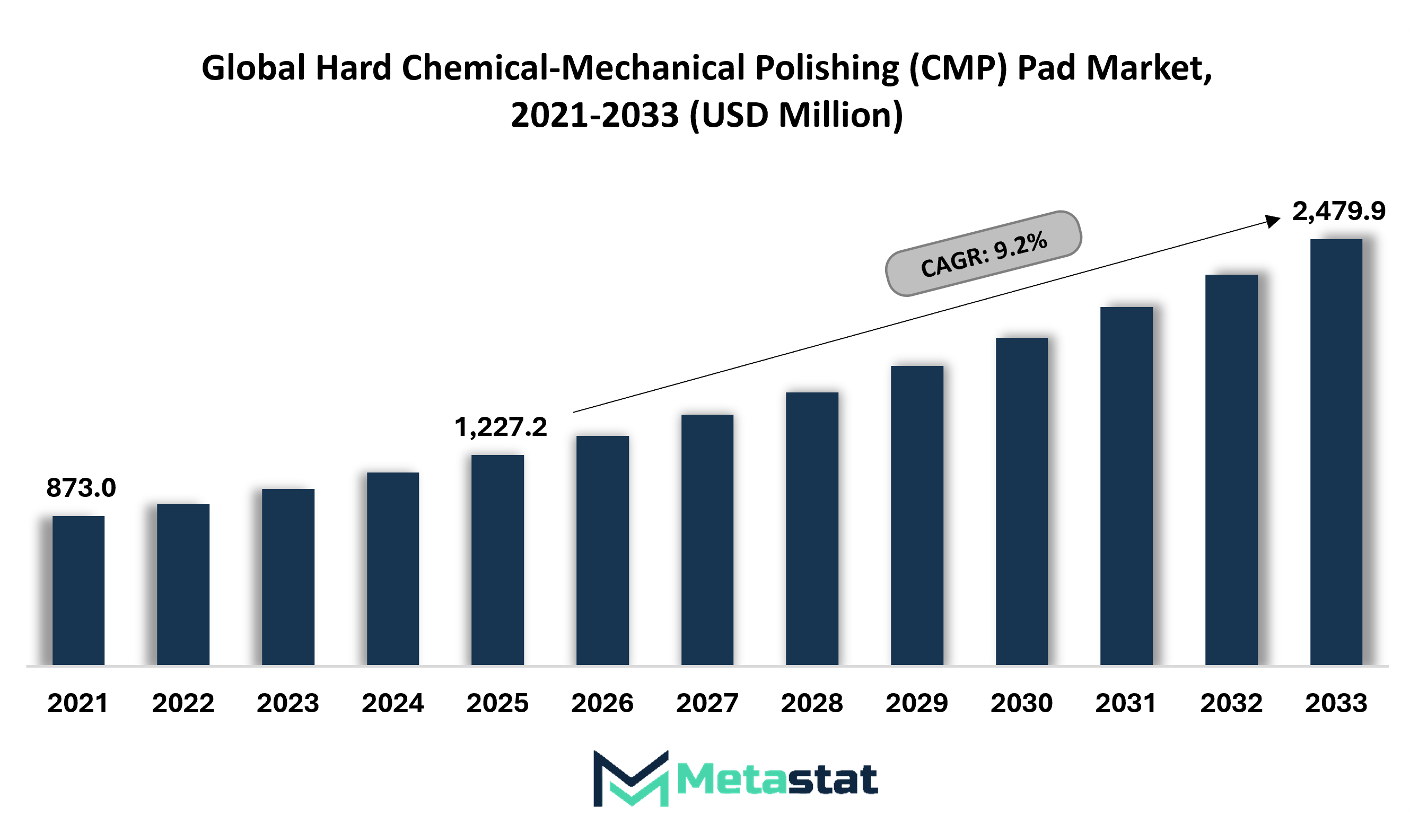

Global Hard Chemical-Mechanical Polishing (CMP) Pad market size is valued at USD 1,227.2 million in 2025 and projected to grow at a CAGR of 9.2% during the forecast period, reaching USD 2,479.9 million by 2033.

Global Hard Chemical-Mechanical Polishing (CMP) Pad Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

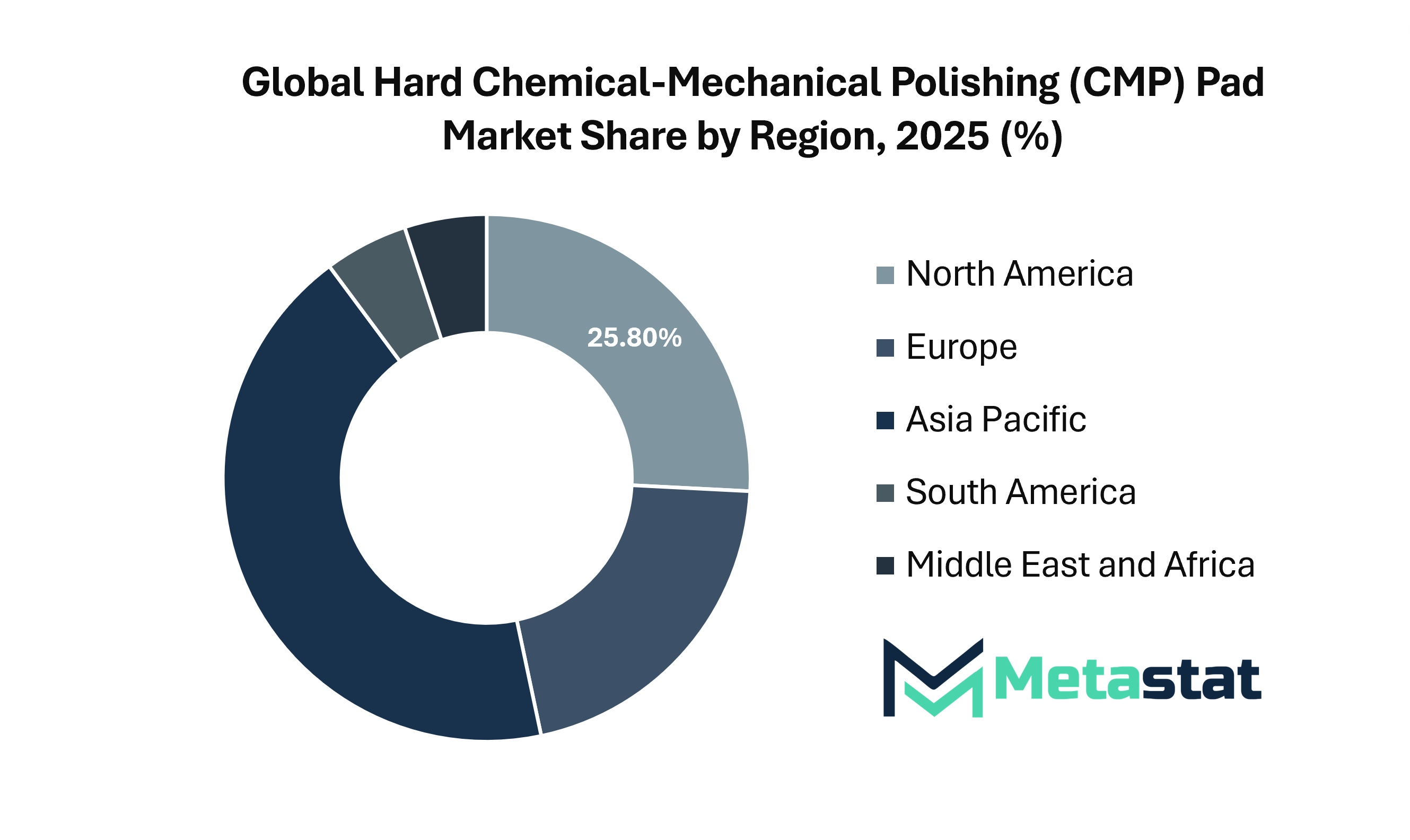

North America holds 25.8% in 2025 with US leading the market share in 2025.

Polyurethane CMP Pads segment account for a market share of 84.3% in 2025.

Key trends driving growth: Expansion of advanced semiconductor fabrication and wafer processing capacity, Increased adoption of AI, HPC, memory, and advanced packaging devices

Opportunities include chlorine-free, low-defect, and third-generation semiconductor pad innovation for SiC and GaN polishing.

Key insight: The Hard Chemical-Mechanical Polishing (CMP) Pad Market is positioned for steady expansion owing to rising wafer complexity and increasing demand for precision planarization materials.

The Hard Chemical-Mechanical Polishing (CMP) Pad Market plays a critical role in semiconductor manufacturing, where surface flatness and defect reduction remain essential for advanced chip production. CMP pads are widely used during wafer polishing processes to ensure smooth surfaces for subsequent lithography, deposition, and interconnect formation stages. Growing investments in logic chips, memory devices, automotive electronics, and high-performance computing continue to reinforce demand across semiconductor fabrication facilities worldwide.

Rapid technology migration toward smaller nodes, heterogeneous integration, and higher layer counts is increasing the need for consistent polishing performance. Manufacturers in the Hard Chemical-Mechanical Polishing (CMP) Pad Market are focusing on pad life improvement, uniform slurry distribution, lower scratch rates, and stable material removal rates. These improvements are helping fabs improve yields, reduce downtime, and optimize manufacturing economics.

New fabrication plants, node migration programs, wafer output expansion, and regional supply chain investments are creating strong demand for polishing consumables. Capacity additions across foundry, logic, memory, and specialty chip production lines are supporting recurring pad replacement cycles. The Global Hard Chemical-Mechanical Polishing (CMP) Pad Market is gaining momentum from sustained semiconductor manufacturing scale-up.

Increased adoption of AI, HPC, memory, and advanced packaging devices

AI servers, high-performance computing systems, memory upgrades, chiplet integration, and dense packaging formats require advanced surface planarity. Rising complexity across multilayer device structures is increasing the need for precision polishing solutions. The Global Hard Chemical-Mechanical Polishing (CMP) Pad Market benefits from premium pad demand linked with next-generation semiconductor device manufacturing.

Restraints and Challenges:

High process qualification requirements and fab-specific customization

Lengthy validation cycles, strict contamination controls, recipe-matching requirements, and fab-specific tuning slow commercial adoption. Qualification failure risks increase supplier workload and development costs. The Global Hard Chemical-Mechanical Polishing (CMP) Pad Market faces prolonged sales timelines where approval requirements remain stringent across advanced semiconductor manufacturing environments.

Raw material sensitivity, defect-control challenges, and cost pressure

Polymer inputs, additives, logistics variability, and purity standards influence product consistency. Scratch prevention, particle control, yield protection, and margin pressure create challenging operating conditions for suppliers. The Global Hard Chemical-Mechanical Polishing (CMP) Pad Market faces pricing pressure as buyers seek higher performance within limited procurement budgets.

Opportunities:

Chlorine-free, low-defect, and third-generation semiconductor pad innovation for SiC and GaN polishing

Wide bandgap materials such as SiC and GaN require durable CMP pads with stable removal rates, low defectivity, and strong process compatibility. Chlorine-free chemistry alignment supports cleaner processing goals and tighter semiconductor manufacturing standards. The Global Hard Chemical-Mechanical Polishing (CMP) Pad Market holds strong growth potential through specialized pad launches for power electronics and compound semiconductor applications.

Market Segmentation Analysis

The Global Hard Chemical-Mechanical Polishing (CMP) Pad market is classified / based on Type, Wafer Size, Application, and End-User.

By Type, the market is further segmented into:

Polyurethane CMP Pads

Polyurethane CMP Pads segment is valued at USD 1,128.8 million in 2026 and is projected to reach USD 2,126.3 million by 2033, at a CAGR of 9.5% during the forecast period.

Polyurethane CMP pad demand will remain strong owing to high durability, stable polishing rates, and surface uniformity during advanced chip fabrication. Manufacturers will focus on pore structure optimization, hardness control, slurry interaction, and longer operating cycles. The Global Hard Chemical-Mechanical Polishing (CMP) Pad Market will receive continued support from semiconductor capacity expansion and advanced wafer processing requirements.

Non-polyurethane CMP Pads

Non-polyurethane CMP Pads segment is valued at USD 210.0 million in 2026 and is projected to reach USD 353.6 million by 2033, at a CAGR of 7.7% during the forecast period.

Non-polyurethane CMP pad adoption will rise through specialized polishing requirements where softer contact, reduced defect levels, and material compatibility are important. Research activity will improve composite pad structures, alternative polymer blends, and process-specific surface properties. Future supply trends will create wider options for niche wafer processes across specialty semiconductor production lines.

200mm Wafer segment is projected to reach USD 549.3 million by 2033, at a CAGR of 6.2% during the forecast period.

200mm wafer usage will remain relevant across mature node production, power devices, sensors, and industrial chips. Existing fabrication plants continue to operate with cost-focused strategies, creating steady polishing pad requirements. Replacement demand, process consistency, and affordable technology upgrades will support long-term consumption across established semiconductor manufacturing facilities.

300mm Wafer

300mm Wafer segment is projected to reach USD 1,754.0 million by 2033, at a CAGR of 10.5% during the forecast period.

300mm wafer production will lead future volume demand owing to higher chip output, better process efficiency, and broader use in advanced fabs. Advanced semiconductor facilities continue to increase dependence on precision polishing consumables for logic, memory, and advanced packaging applications. Pad suppliers will invest in defect control, uniform pressure response, longer service life, and improved polishing consistency.

Others

Others segment is projected to reach USD 176.6 million by 2033, at a CAGR of 7.7% during the forecast period.

Other wafer sizes will retain value across research centers, pilot lines, specialty devices, and legacy manufacturing systems. Demand levels will remain moderate, while technical customization can create profitable opportunities for CMP pad producers. Flexible production planning will help suppliers address varied customer process requirements across low-volume and specialized semiconductor applications.

By Application, the market is further divided into:

Memory Devices

Memory Devices segment is projected to reach USD 899.5 million by 2033.

Memory device fabrication is projected to generate notable CMP pad demand owing to rising storage requirements in data centers, mobile products, and artificial intelligence hardware. Multilayer memory architectures require flat wafer surfaces, reliable process control, and low-defect polishing performance. Future pad development will target precision finishing, lower scratch generation, and improved compatibility with high-volume memory manufacturing.

Logic Devices

Logic Devices segment is projected to reach USD 1,134.8 million by 2033.

Logic device manufacturing will create sustained demand through processor growth in computing, automotive electronics, AI accelerators, and connected equipment. Smaller process nodes require stronger planarization accuracy across multiple polishing stages. Suppliers will emphasize material consistency, thermal stability, and repeatable performance for complex chip structures.

MEMS Devices segment is projected to reach USD 236.6 million by 2033.

MEMS device output will expand with increasing sensor integration across vehicles, healthcare tools, industrial systems, and smart products. CMP pads play an important role in surface preparation, wafer thinning, and dimensional control. Producers will design tailored pad solutions suited for delicate structures, varied substrate materials, and precision MEMS manufacturing needs.

Others

Others segment is projected to reach USD 209.1 million by 2033.

Other applications will include compound semiconductors, photonics, research devices, and emerging electronic components. Demand will rise through innovation pipelines, prototype activity, and specialty wafer processing. Pad manufacturers will benefit from custom formulations, rapid delivery models, and technical collaboration with fabrication teams seeking process optimization.

By End-User, the Global Hard Chemical-Mechanical Polishing (CMP) Pad market is divided as:

Semiconductor Industry

Semiconductor Industry segment is projected to grow at a CAGR of 9.7% during the forecast period.

The semiconductor industry will dominate the end-user segment owing to continuous wafer fabrication activity across memory, logic, and specialty chips. Expansion of fabrication plants in Asia-Pacific, North America, and Europe will increase consumable requirements. Growth prospects for the Global Hard Chemical-Mechanical Polishing (CMP) Pad Market remain closely linked with semiconductor capital investment cycles.

Electronics Industry

Electronics Industry segment is projected to grow at a CAGR of 6.8% during the forecast period.

Electronics industry consumption will grow through wider use of sensors, displays, communication hardware, and embedded systems requiring advanced semiconductor components. Increasing device complexity is creating indirect demand for polishing materials used upstream in chip production. Stable consumer electronics, industrial electronics, and connected device demand will support market momentum.

Others

Others segment is projected to grow at a CAGR of 4.2% during the forecast period.

Other end-users will include research institutions, defense manufacturing, healthcare technology producers, and industrial automation firms. Smaller volumes will still offer premium opportunities through specialized processing needs. Suppliers will strengthen future presence by providing technical assistance, custom pad designs, and reliable supply arrangements.

By Region:

Based on geography, the Global Hard Chemical-Mechanical Polishing (CMP) Pad market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America is gaining momentum through semiconductor manufacturing reshoring and government-supported fab investments.

Regional growth is also supported by strong demand for AI processors, automotive chips, and data center semiconductors.

Europe will show steady growth in the Hard Chemical-Mechanical Polishing (CMP) Pad Market owing to rising semiconductor localization efforts, automotive electronics demand, and increasing focus on advanced wafer processing capabilities.

Asia-Pacific offers major opportunities through expanding foundry capacity, memory production, and electronics manufacturing clusters.

China, Taiwan, South Korea, Japan, and India continue strengthening supply chain localization and wafer processing capabilities.

Across the Middle East, Africa, and South America, the Hard Chemical-Mechanical Polishing (CMP) Pad Market is advancing steadily through electronics assembly growth, industrial diversification, and rising participation in the semiconductor ecosystem.

Competitive Landscape and Strategic Insights

The Hard Chemical-Mechanical Polishing (CMP) Pad Market is shaped by companies that support chip manufacturing through continuous product development, process innovation, and supply expansion. Demand is closely tied to semiconductor production, where polishing materials help create flat and smooth wafer surfaces required for advanced devices. Producers in this field focus on pad life, surface consistency, defect control, and process stability. Competition remains active as customers expect strong technical support and reliable output. Many suppliers also work closely with fabrication plants to improve polishing results for changing node sizes and increasingly complex chip designs. Since production requirements are strict, buyers often prefer established suppliers with proven quality performance and long operating histories.

NITTA DuPont Inc. holds a strong position through its experience in precision polishing materials and long-standing presence in electronics manufacturing supply chains. Entegris, Inc. is widely recognized for serving semiconductor customers with process materials, contamination control solutions, and related polishing products. Hubei Dinglong Co., Ltd. has gained attention through expansion in Asia and growing participation in regional semiconductor material sourcing. Fujibo Holdings, Inc. continues to build its position through industrial materials expertise and specialized polishing solutions. IVT Technologies Co., Ltd. and SK enpulse Co., Ltd. are also strengthening their positions through technical enhancements and efforts to meet changing chipmaking requirements. Their ability to respond quickly to customer process needs provides meaningful market advantages.

Pureon AG and 3M bring strong industrial backgrounds that support innovation, materials science, and precision finishing applications. SKC has also expanded its influence through advanced materials capabilities and links to electronics manufacturing networks. Alfa Chemistry serves customers requiring specialty materials, research support, and commercial-grade solutions. FNS TECH Co., Ltd. continues to build its reputation through focused polishing products and regional supply efforts. CMC Materials, Inc., now associated with Entegris following acquisition, remains a relevant reference point in CMP consumables and slurry expertise. These companies help shape pricing trends, product quality expectations, and customer purchasing decisions across multiple regions.

SPS International and Topco Scientific Co., Ltd. add further depth to the competitive landscape by supporting distribution channels, technical service, and customer access across key manufacturing hubs. The market will remain driven by chip demand, new fabrication investments, and movement toward higher-performance electronics. Suppliers that improve pad durability, polishing accuracy, and delivery reliability will gain stronger opportunities over time. Partnerships, regional expansion, and research spending will also influence future positioning among manufacturers.

Forecast and Future Outlook

Market size is forecast to rise from USD 1,227.2 million in 2025 to over USD 2,479.9 million by 2033.

The Hard Chemical-Mechanical Polishing (CMP) Pad Market is expected to benefit from increasing semiconductor complexity, advanced packaging expansion, EV power electronics growth, and AI infrastructure demand. Suppliers offering lower defectivity, better uniformity, longer pad life, and sustainability-focused products are likely to gain stronger market share during the forecast period.

Hard Chemical-Mechanical Polishing (CMP) Pad Market Key Segments:

By Type:

Polyurethane CMP Pads

Non-polyurethane CMP Pads

By Wafer Size:

200mm Wafer

300mm Wafer

Others

By Application:

Memory Devices

Logic Devices

MEMS Devices

Others

By End-User:

Semiconductor Industry

Electronics Industry

Others

Key Global Hard Chemical-Mechanical Polishing (CMP) Pad Industry Players

This research report categorizes the Hard Chemical-Mechanical Polishing (CMP) Pad Market based on key segments and regions, forecasts revenue growth, and analyzes trends across each submarket. The report analyzes key growth drivers, opportunities, and challenges influencing the Hard Chemical-Mechanical Polishing (CMP) Pad Market. Recent market developments and competitive strategies such as expansions, product launches, partnerships, mergers, and acquisitions have been included to assess the competitive landscape.

The report strategically identifies and profiles key market players and analyzes their core competencies across each sub-segment of the Hard Chemical-Mechanical Polishing (CMP) Pad Market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 9.2% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Million Units

Segmentation

By Type, Wafer Size, Application, End-User, and Region

By Region

North America (By Type, Wafer Size, Application, End-User, and Country)

United States

Canada

Mexico

Europe (By Type, Wafer Size, Application, End-User, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Type, Wafer Size, Application, End-User, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Type, Wafer Size, Application, End-User, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Type, Wafer Size, Application, End-User, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Prepositions of Leading Market Players

Semiconductor Gas Delivery Cabinet Market Size, Share, Trends, 2033

Semiconductor Gas Delivery Cabinet market size is valued at USD 1,308.2 million in 2025 and is projected to reach USD 2,446.2 million in 2033, at a CAGR of 8.1% from 2026 to 2033.

Semiconductor Gas Delivery Cabinet Market, Semiconductor Gas Delivery Cabinet Market Size, Semiconductor Gas Delivery Cabinet Market Share, Semiconductor Gas Delivery Cabinet Market Analysis, Semiconductor Gas Delivery Cabinet Market Growth, Semiconductor Gas Delivery Cabinet Market Trends, Semiconductor Gas Delivery Cabinet Market Research Report, Semiconductor Gas Delivery Cabinet Market Forecast, Semiconductor Gas Delivery Cabinet, Semiconductor Gas Delivery Cabinet Market Research, Semiconductor Gas Delivery Cabinet Industry, Semiconductor Gas Delivery Cabinet Industry Report, Semiconductor Gas Delivery Cabinet Market Data, Semiconductor Gas Delivery Cabinet Statistics, Semiconductor Gas Delivery Cabinet Market Statistics, Semiconductor Gas Delivery Cabinet Industry Trends, Semiconductor Gas Delivery Cabinet Market Report, Semiconductor Gas Delivery Cabinet Market Trends, Semiconductor Gas Delivery Cabinet Market News, Semiconductor Gas Delivery Cabinet Forecasts, Semiconductor Gas Delivery Cabinet Market Intelligence Report

Global Manual Electronic DIP Switches market size is valued at USD 1,662.9 million in 2025 and is projected to reach USD 2,363.3 million in 2033, at a CAGR of 4.5% from 2026 to 2033

Global Industrial Electronics Repair & Refurbishment Services market size is valued at USD 31.0 billion in 2025 and is projected to reach USD 59.8 billion in 2033, at a CAGR of 7.7% from 2026 to 2033

Global Coaxial Switches market size is valued at USD 179.2 million in 2025 and is projected to reach USD 226.9 million in 2033, at a CAGR of 3.0% from 2026 to 2033