Metal Forgings for Oil and Gas Market Size, Share, By Type (Open-Die Forgings, Closed-Die Forgings, Seamless Rolled Ring Forgings, and Upset Forgings), By Products (Flanges, Fittings, Shafts, Blocks, Hubs, and Others), By Application (Downhole Forgings, Subsea Forgings, and Surface Forgings), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4611

Published

April 14, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

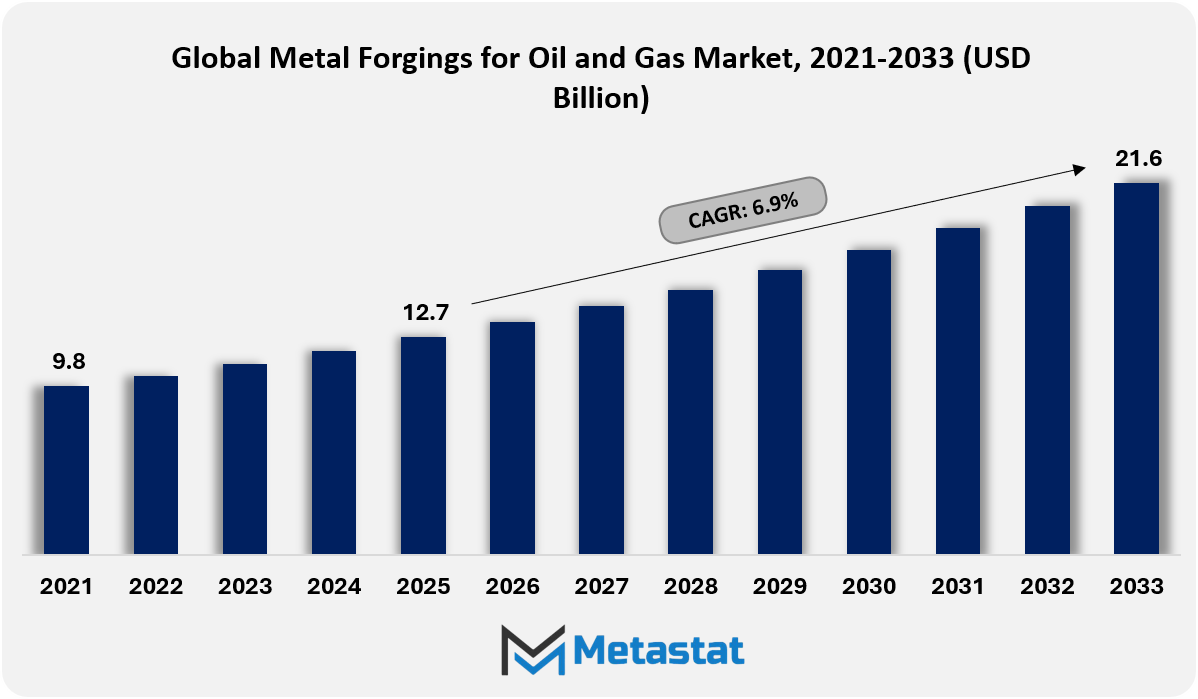

The Global Metal Forgings for Oil and Gas market size was valued at USD 12.7 billion in 2025 and projected to grow at a CAGR of 6.9% during the forecast period, reaching USD 21.6 billion by 2033.

Global Metal Forgings for Oil and Gas Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

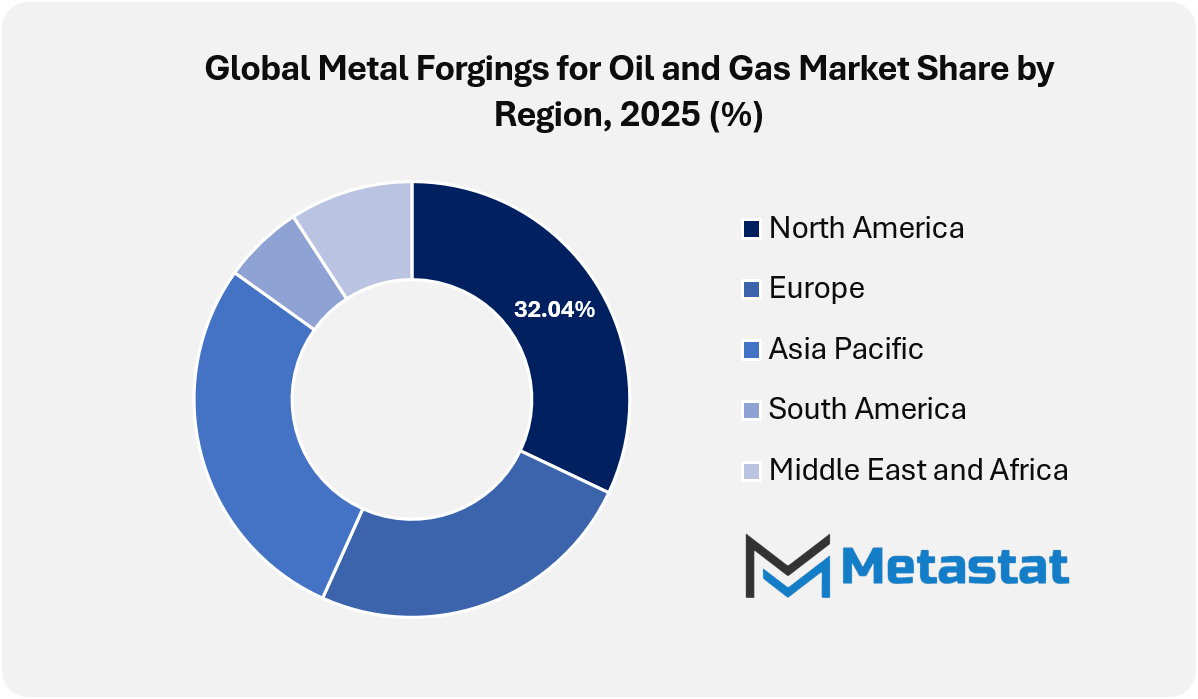

North America held 32.0% of the global market in 2025, with the U.S. leading regional demand.

The Open-Die Forgings segment accounted for 27.4% of the market in 2025.

Key trends driving growth include ongoing investments in oil and gas exploration, production, and pipeline infrastructure, along with rising demand for high-strength and durable components that support operational safety and reliability.

Opportunities include rising demand for corrosion-resistant and high-performance alloy forgings in deepwater and unconventional projects.

Key insight: Rising upstream investment and pipeline expansion continue to anchor demand for high-strength metal forgings across oil and gas infrastructure.

The Global Metal Forgings for Oil and Gas market and its industry ecosystem are entering a phase where technical specialization, operational resilience, and commercial relevance are gaining greater importance beyond conventional supply-side narratives. Over the coming years, forged components designed for drilling systems, pressure control equipment, and subsea infrastructure are expected to attract stronger demand owing to their role in supporting complex extraction environments, including ultra-deepwater and high-temperature fields. Demand patterns are likely to align with engineering requirements related to durability, fatigue resistance, and precision tolerances, encouraging manufacturers to adopt advanced metallurgical practices.

Future development in the Global Metal Forgings for Oil and Gas market is expected to remain closely linked with digital manufacturing frameworks. Smart forging lines, predictive quality monitoring, and data-driven defect reduction strategies are projected to influence procurement decisions among upstream operators and equipment manufacturers. This shift is likely to reshape supplier evaluation, with traceability, simulation-backed design validation, and lifecycle performance data gaining priority over volume-led contracts.

Market Dynamics

Growth Drivers:

Ongoing investments in oil and gas exploration, production, and pipeline infrastructure.

Sustained capital flows toward offshore fields, shale reserves, and cross-border pipeline networks continue to support expansion in the Global Metal Forgings for Oil and Gas market. Infrastructure modernization and capacity additions across producing regions are driving consistent demand for forged components designed for high-pressure operating environments and extended service cycles.

Demand for high-strength and durable components to ensure operational safety and reliability.

Operational hazard discount remains a central priority across upstream and midstream sectors, growing choice for solid elements supplying superior fatigue resistance and cargo tolerance. High-strength forgings improve equipment stability under extreme temperatures and pressures, strengthening operator confidence in uninterrupted production and long-term asset integrity.

Restraints and Challenges:

Volatility in crude oil prices affecting capital expenditure in oil and gas projects.

Fluctuating crude benchmarks introduce uncertainty within assignment planning and procurement schedules. Budget revisions and deferred investments regularly disrupt order volumes for solid products. Market participants face planning challenges during prolonged price volatility, limiting short-term visibility for suppliers tied to exploration and production spending cycles.

Stringent quality standards and certification requirements increasing production complexity.

Compliance with global material standards and inspection protocols increases manufacturing complexity for forging suppliers. Advanced checking out, documentation, and traceability necessities increase operational costs. Smaller producers face entry barriers, while larger manufacturers allocate significant resources to maintain approvals required across critical oil and gas applications.

Opportunities:

Rising demand for corrosion-resistant and high-performance alloy forgings in deepwater and unconventional projects.

Growth in deepwater drilling and unconventional resource development is encouraging the adoption of alloy forgings engineered for corrosive, high-pressure environments. Specialized materials support longer equipment life under harsh operating conditions. This performance-driven trend is strengthening long-term prospects for the Global Metal Forgings for Oil and Gas market.

Market Segmentation Analysis

The Global Metal Forgings for Oil and Gas market is segmented by Type, Product, and Application.

By Type, the market is further segmented into:

Open-Die Forgings

Open-Die Forgings segment is estimated at USD 3.7 billion in 2026 and is projected to reach USD 5.5 billion by 2033, at a CAGR of 5.8% during the forecast period.

Open-Die Forgings will support large-scale oil and gas equipment manufacturing through flexible shaping capabilities and strong structural performance. Production processes enable customized dimensions for heavy components used in drilling and processing systems. Adoption is expected to rise with infrastructure expansion, where adaptability and grain integrity remain important procurement considerations.

Closed-Die Forgings

Closed-Die Forgings segment is estimated at USD 3.2 billion in 2026 and is projected to reach USD 5 billion by 2033, at a CAGR of 6.5% during the forecast period.

Closed-Die Forgings are expected to gain momentum owing to demand for high-precision components with consistent geometry. Controlled tooling improves mechanical performance in critical oilfield equipment. Future deployment will remain strong in volume-production settings that require repeatability, reduced material waste, and improved surface finish, supporting efficiency goals across energy-sector supply chains.

Seamless Rolled Ring Forgings

Seamless Rolled Ring Forgings segment is estimated at USD 5.2 billion in 2026 and is projected to reach USD 8.8 billion by 2033, at a CAGR of 7.7% during the forecast period.

Seamless Rolled Ring Forgings will play a vital role in pressure-intensive oil and gas applications. Their circular grain flow improves fatigue resistance in valves, bearings, and connectors. Market preference is expected to strengthen owing to their reliability under rotational stress, supporting longer service life across offshore and onshore installations.

Upset Forgings

Upset Forgings segment is estimated at USD 1.4 billion in 2026 and is projected to reach USD 2.4 billion by 2033, at a CAGR of 7.9% during the forecast period.

Upset Forgings address the requirement for localized strength enhancement in oil and gas components. Axial force concentration improves load-bearing capacity in fasteners and connectors. Utilization is expected to increase with more complex drilling operations, where compact components must withstand high tensile and compressive forces over extended operating cycles.

By Products, the market is divided into:

Flanges

Flanges segment is projected to reach USD 6.7 billion by 2033, at a CAGR of 6.4% during the forecast period.

Flanges remain essential connection components in pipelines and processing units. Forged construction supports leak resistance under high-pressure and high-temperature conditions. Future demand will align with pipeline network expansion, refinery upgrades, and compliance-driven replacement cycles, reinforcing the importance of dimensional accuracy and metallurgical consistency.

Fittings

Fittings segment is projected to reach USD 5.6 billion by 2033, at a CAGR of 6.8% during the forecast period.

Forged fittings will support directional flow control and structural continuity within oil and gas systems. High-strength metallurgy will reduce the risk of failure under fluctuating pressure. Future growth will reflect increased adoption of complex pipeline layouts, where durability, corrosion resistance, and long-term performance will influence purchasing strategies.

Shafts

Shafts segment is projected to reach USD 2.2 billion by 2033, at a CAGR of 7.3% during the forecast period.

Shafts enable torque transmission in drilling rigs, pumps, and compressors. Uniform grain flow improves fatigue resistance under continuous rotation. Future requirements will emphasize precise balancing and material stability, supporting automation-led equipment design and higher operational efficiency across upstream and midstream applications.

Blocks

Blocks segment is projected to reach USD 2.5 billion by 2033, at a CAGR of 6.5% during the forecast period.

Blocks serve as core components in heavy oil and gas machinery. Solid structural integrity will support machining into customized forms. Future relevance will expand with modular tool design trends, where high-load tolerances and machining flexibility will support faster deployment and less maintenance downtime.

Hubs

Hubs segment is projected to reach USD 1.9 billion by 2033, at a CAGR of 7.8% during the forecast period.

Hubs connect rotating elements within energy equipment assemblies. Higher mechanical strength reduces wear under cyclic stress. Adoption is expected to increase with the modernization of drilling systems, where compact yet robust components support higher power density and extended operating reliability.

Others

Others segment is projected to reach USD 2.8 billion by 2033, at a CAGR of 7.8% during the forecast period.

Other forged products meet specialized oil and gas requirements, including connectors, couplings, and custom-engineered components. Tailored production supports project-specific specifications. Requirement for these products is expected to increase with unconventional exploration activity, encouraging innovation in forging techniques and alloy selection for specific operating challenges.

By Application, the market is further divided into:

Downhole Forgings

Downhole Forgings segment is projected to reach USD 6.6 billion by 2033.

Downhole forgings must withstand extreme pressures, temperatures, and corrosive environments during drilling operations. High structural strength reduces failure risk at critical depths. Growth will be supported by deep-well development, which places greater emphasis on metallurgical precision and performance assurance under prolonged exposure conditions.

Subsea Forgings

Subsea Forgings segment is projected to reach USD 5.2 billion by 2033.

Subsea forgings will support offshore infrastructure through exceptional resistance to pressure and corrosion. Structural reliability will continue to be important for underwater installations. Future growth will follow offshore energy investments, where long service intervals and minimal maintenance access will increase the value of high-integrity forged components.

Surface Forgings

Surface Forgings segment is projected to reach USD 9.8 billion by 2033.

Surface forgings contribute to processing units, storage systems, and transportation infrastructure. Forged durability will support continuous operation under variable loads. Future expansion will align with refinery upgrades and onshore facility development, driving demand for standardized components that meet increasing safety and efficiency requirements.

By Region:

Based on geography, the Global Metal Forgings for Oil and Gas market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

North America Metal Forgings for Oil and Gas Market is set to expand at a CAGR of 6.9% within the forecast period, reaching a market size (TAM) of USD 6.4 billion by the end of 2033.

In North America, sustained investment in shale exploration and unconventional drilling supports steady demand for high-strength metal forgings used in critical oil and gas equipment.

North America also maintains stringent safety and performance standards across upstream and midstream operations, encouraging adoption of precision-engineered metal forgings.

In Asia-Pacific, expanding refining capacity and cross-border pipeline projects are creating strong opportunities for steel forgings used in valves, flanges, and pressure equipment.

Asia-Pacific offers strong growth potential through rising offshore exploration activity and increasing domestic energy consumption across emerging economies.

Across the Middle East, Africa, and South America, large-scale oilfield development, infrastructure upgrades, and national energy security initiatives sustain long-term demand for durable steel forgings in oil and gas operations.

Competitive Landscape and Strategic Insights

The Global Metal Forgings for Oil and Gas market plays a critical role in supporting energy infrastructure, where strength, safety, and long service life are essential. Forged components are used across drilling, exploration, transportation, and refining operations, where they must perform under high pressure and extreme temperatures. Demand remains connected to upstream and midstream investments, pipeline expansion, and equipment upgrades across mature and emerging electricity markets. Manufacturers remain focused on consistency, material quality, and delivery reliability to meet stringent industry standards while managing costs and lead times.

Several established companies shape the competitive structure of this market through deep manufacturing expertise and broad product portfolios. Bharat Forge Ltd., ELLWOOD City Forge Group, Scot Forge, FRISA, Farinia Group (Setforge), Ring Mill S.P.A., and Galperti Group supply massive solid rings, flanges, and custom elements utilized in critical oil and gas operations. ULMA Forged Solutions, Special Flanges S.p.A., Metalfar, Vilmar S.p.A., Texas Flange, and Paramount Forge support global projects through a mix of standard and engineered solutions designed for harsh operating conditions.

The Global Metal Forgings for Oil and Gas market plays a constant role in supporting power infrastructure, where electricity, protection, and long service life are essential every day. Forged components guide drilling, exploration, shipping, and refining operations, coping with high strain and extreme temperatures without failure. Demand remains connected to upstream and midstream investments, pipeline expansion, and equipment upgrades across mature and emerging electricity markets. Manufacturers' attention on consistency, fabric quality, and dependable output to meet strict enterprise standards while handling fees and delivery timelines.

Several installed corporations form the aggressive structure of this market through deep production experience and huge product portfolios. Bharat Forge Ltd., ELLWOOD City Forge Group, Scot Forge, FRISA, Farinia Group, Ring Mill S.p.A., and Galperti Group supply large, forged rings, flanges, and custom components used in critical oil and gas operations. ULMA Forged Solutions, Special Flanges S.P.A., Metalfar, Vilmar S.P.A., Texas Flange, and Paramount Forge help international projects through a mix of well-known and engineered solutions designed for harsh field conditions.

Forecast and Future Outlook

Market size is forecast to rise from USD 12.7 billion in 2025 to over USD 21.6 billion by 2033.

Beyond direct oilfield applications, forged products serving this market are expected to gain relevance across adjacent energy segments. Hydrogen transport systems, carbon capture infrastructure, and geothermal installations are likely to adopt similar forging specifications owing to shared pressure and safety requirements. Such convergence is probably to blur conventional enterprise obstacles, positioning forging specialists at the intersection of multiple energy pathways. Over time, the Global Metal Forgings for Oil and Gas market is expected to evolve into a technically anchored segment where engineering credibility, compliance depth, and adaptive manufacturing capabilities define long-term relevance beyond immediate project cycles.

Metal Forgings for Oil and Gas Market Key Segments:

By Type:

Open-Die Forgings

Closed-Die Forgings

Seamless Rolled Ring Forgings

Upset Forgings

By Products:

Flanges

Fittings

Shafts

Blocks

Hubs

Others

By Application:

Downhole Forgings

Subsea Forgings

Surface Forgings

Key Global Metal Forgings for Oil and Gas Industry Players

This research report categorizes the Metal Forgings for Oil and Gas market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Metal Forgings for Oil and Gas market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Metal Forgings for Oil and Gas market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 6.9% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Type, Products, Application, and Region

By Region

North America (By Type, Products, Application, and Country)

United States

Canada

Mexico

Europe (By Type, Products, Application, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Type, Products, Application, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Type, Products, Application, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Type, Products, Application, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share and Revenue

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Concentrated Solar Power Market Size, Share, Trends, 2033

Concentrated Solar Power market size is valued at USD 7.5 billion in 2025 and is projected to reach USD 17.3 billion in 2033, at a CAGR of 11.1% from 2026 to 2033.

Concentrated Solar Power Market, Concentrated Solar Power Market Size, Concentrated Solar Power Market Share, Concentrated Solar Power Market Analysis, Concentrated Solar Power Market Growth, Concentrated Solar Power Market Trends, Concentrated Solar Power Market Research Report, Concentrated Solar Power Market Forecast, Concentrated Solar Power, Concentrated Solar Power Market Research, Concentrated Solar Power Industry, Concentrated Solar Power Industry Report, Concentrated Solar Power Market Data, Concentrated Solar Power Statistics, Concentrated Solar Power Market Statistics, Concentrated Solar Power Industry Trends, Concentrated Solar Power Market Report, Concentrated Solar Power Market Trends, Concentrated Solar Power Market News, Concentrated Solar Power Forecasts, Concentrated Solar Power Market Intelligence Report

Global Leak Detection Software market size is valued at USD 985.8 million in 2025 and is projected to reach USD 1,713.0 million in 2033, at a CAGR of 7.1% from 2026 to 2033

Global Leak Detection Software Market, Global Leak Detection Software Market Size, Global Leak Detection Software Market Share, Global Leak Detection Software Market Analysis, Global Leak Detection Software Market Growth, Global Leak Detection Software Market Trends, Global Leak Detection Software Market Research Report, Global Leak Detection Software Market Forecast, Global Leak Detection Software, Global Leak Detection Software Market Research, Global Leak Detection Software Industry, Global Leak Detection Software Industry Report, Global Leak Detection Software Market Data, Global Leak Detection Software Statistics, Global Leak Detection Software Market Statistics, Global Leak Detection Software Industry Trends, Global Leak Detection Software Market Report, Global Leak Detection Software Market Trends, Global Leak Detection Software Market News, Global Leak Detection Software Forecasts, Global Leak Detection Software Market Intelligence Report

Renewable Energy market size is valued at USD 1,738.8 billion in 2025 and is projected to reach USD 5,698.6 billion in 2033, at a CAGR of 15.8% from 2026 to 2033.

Renewable Energy Market, Renewable Energy Market Size, Renewable Energy Market Share, Renewable Energy Market Analysis, Renewable Energy Market Growth, Renewable Energy Market Trends, Renewable Energy Market Research Report, Renewable Energy Market Forecast, Renewable Energy, Renewable Energy Market Research, Renewable Energy Industry, Renewable Energy Industry Report, Renewable Energy Market Data, Renewable Energy Statistics, Renewable Energy Market Statistics, Renewable Energy Industry Trends, Renewable Energy Market Report, Renewable Energy Market Trends, Renewable Energy Market News, Renewable Energy Forecasts, Renewable Energy Market Intelligence Report

North America Liquid-Cooled BESS Market Size, Share, Trends, 2033

North America Liquid-Cooled BESS market size is valued at USD 3,871.9 million in 2025 and is projected to reach USD 13,920.3 million in 2033, at a CAGR of 17.1% from 2026 to 2033.

North America Liquid-Cooled BESS Market, North America Liquid-Cooled BESS Market Size, North America Liquid-Cooled BESS Market Share, North America Liquid-Cooled BESS Market Analysis, North America Liquid-Cooled BESS Market Growth, North America Liquid-Cooled BESS Market Trends, North America Liquid-Cooled BESS Market Research Report, North America Liquid-Cooled BESS Market Forecast, North America Liquid-Cooled BESS, North America Liquid-Cooled BESS Market Research, North America Liquid-Cooled BESS Industry, North America Liquid-Cooled BESS Industry Report, North America Liquid-Cooled BESS Market Data, North America Liquid-Cooled BESS Statistics, North America Liquid-Cooled BESS Market Statistics, North America Liquid-Cooled BESS Industry Trends, North America Liquid-Cooled BESS Market Report, North America Liquid-Cooled BESS Market Trends, North America Liquid-Cooled BESS Market News, North America Liquid-Cooled BESS Forecasts, North America Liquid-Cooled BESS Market Intelligence Report