North America Steel Fabrication Market Size and Share, By Service Type (Cutting, Welding, Machining, Bending, and Others), By Material Type (Carbon Steel, Alloy Steel, Stainless Steel, and Others), By End-User Industry (Construction, Automotive, Aerospace, Energy, Manufacturing, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4565

Published

February 24, 2026

Pages

311 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

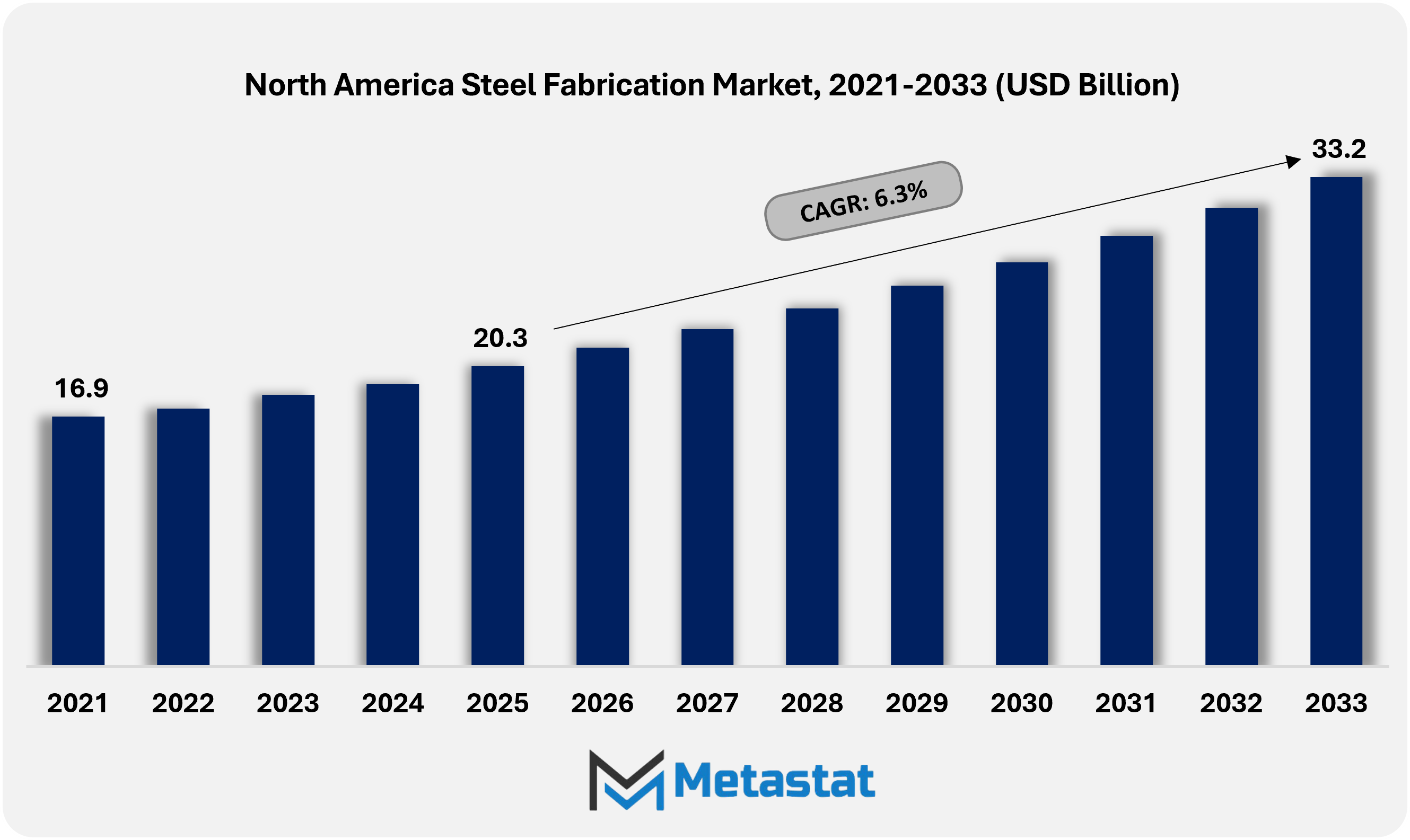

The North America Steel Fabrication market size was valued at USD 20.3 billion in 2025. The market is projected to grow from USD 21.6 billion in 2026 to USD 33.2 billion by 2033, exhibiting a CAGR of 6.3% during the forecast period.

The North America Steel Fabrication market was valued at USD 20.3 billion in 2025 and is projected to reach USD 33.2 billion by 2033, registering a CAGR of 6.3% during the forecast period.

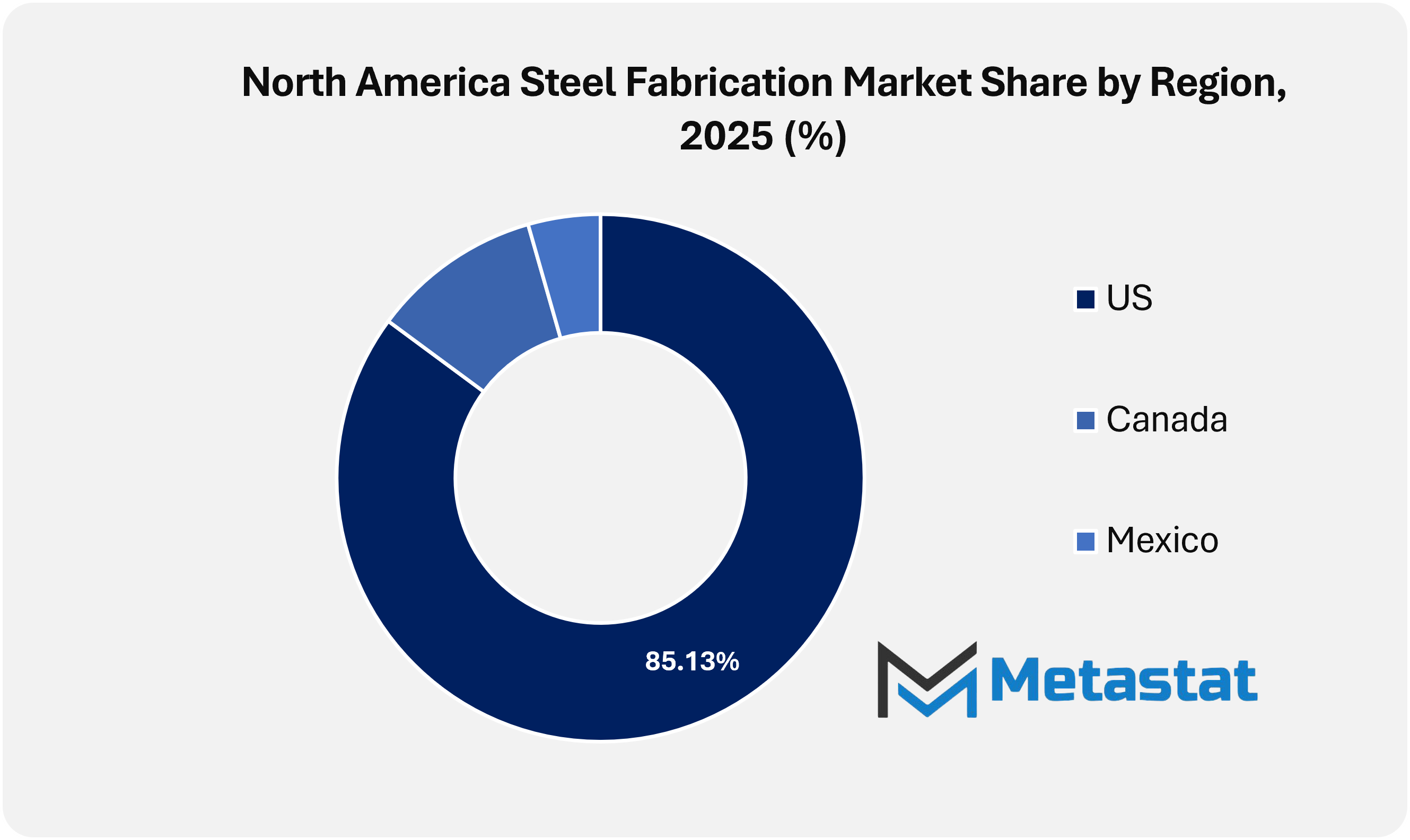

United States accounted for 85.1% share of the North America market in 2025 and remained the leading country market through 2033.

Cutting accounted for a 28.7% market share in 2025.

Key trends driving growth: Large-scale infrastructure renewal across transportation, energy, and public utilities increases demand for fabricated steel components.

Key opportunities include the growing adoption of prefabricated and modular construction methods that elevates demand for precision steel fabrication.

Key insight: North America steel fabrication growth advances through infrastructure modernization and industrial expansion while efficiency-driven fabrication models unlock future value amid cost and labor challenges.

The North America steel fabrication market within the industrial manufacturing industry will move beyond traditional supply narratives and enter a phase shaped by structural recalibration rather than volume expansion. Construction companies across the region will increasingly align operations with complex project execution encompassing transportation corridors, energy transition facilities, advanced manufacturing plants and defense-related infrastructure. Contract portfolios shift toward longer-cycle projects, demanding precision engineering, digital coordination and higher accountability throughout the construction phases.

The operational focus will be shifted towards a modular fabrication model where pre-engineered steel assemblies will be produced offsite and integrated at project locations with minimal disruption. Such methods would be suitable for dense urban redevelopment areas and remote industrial establishments, providing predictability in scheduling and quality control. Fabricators will adopt advanced simulation tools, digital twins and automated cutting systems to meet the demands of modern structural designs. Workforce strategies will also evolve with companies investing in multi-skilled technicians capable of operating hybrid manual-digital fabrication environments.

Market Dynamics

Growth Drivers:

Large-scale infrastructure renewal across transportation, energy, and public utilities increases demand for fabricated steel components.

Large-scale infrastructure renewal across transportation corridors, power grids, and public utility networks will propel long-term requirements within the North America steel fabrication market. Government-backed spending programs will prioritize bridges, transit systems, and transmission assets, supporting repeat orders for fabricated steel products designed for durability, code compliance, and extended service life.

Expansion of commercial construction, data centers, and industrial facilities strengthens steady consumption of structural steel.

Expansion of industrial real estate, hyperscale data centers, logistics hubs, and advanced manufacturing facilities will support steady consumption patterns in the North America steel fabrication market. Future-focused development strategies will favor structural steel owing to strength, scalability, and fast installation cycles, supporting sustained construction activity across urban and industrial zones.

Restraints and Challenges:

Volatile steel prices and fluctuating raw material supply margins create cost uncertainty for fabricators.

Volatile steel pricing trends and volatile raw material supply margins will continue to create financial uncertainty for fabricators operating in the North America steel fabrication market. Forward-looking procurement planning will remain complex, as fluctuations in input costs will put pressure on contract pricing, profitability forecasts and long-term investment decisions in manufacturing operations.

Skilled labor shortages and rising wage pressure slow project timelines and capacity utilization.

Shortage of skilled labor coupled with rising wage pressure will limit operational efficiency in the North America steel fabrication market. Manufacturing facilities will face challenges maintaining optimal capacity utilization, while limited availability of certified welders, machinists and structural manufacturing specialists will result in extended project timelines.

Opportunities:

Growing adoption of prefabricated and modular construction methods elevates demand for precision steel fabrication.

The adoption of prefabricated and modular construction technologies will increase the demand for precision-engineered steel solutions in the North American steel fabrication market. Future building models will emphasize off-site construction, dimensional accuracy and short construction cycles, establishing advanced manufacturing capabilities as a key competitive advantage.

Market Segmentation Analysis

The North America Steel Fabrication market is segmented by Service Type, Material Type, and End-User Industry.

By Service Type, the market is further segmented into:

Cutting

Cutting segment is valued at USD 6.2 billion in 2026 and is projected to reach USD 9.8 billion by 2033, at a CAGR of 6.8% during the forecast period.

Cutting services will advance through automation, laser-based systems and data-controlled processes that will support higher accuracy and lower material loss. Demand will increase from infrastructure and transportation projects requiring similar outputs. In future operations, priority will be given to speed, stability and integration with digital production lines to meet evolving industrial specifications.

Welding

Welding segment is valued at USD 6.5 billion in 2026 and is projected to reach USD 10.3 billion by 2033, at a CAGR of 6.3% during the forecast period.

Welding services will experience transformation through robotic systems and advanced joining technologies that support strength and durability. Adoption will increase in areas requiring structural integrity under high stress. Future-focused facilities will emphasize precise controls, reduced defects, and compliance with safety regulations that support long-term performance requirements.

Machining

Machining segment is valued at USD 4.1 billion in 2026 and is projected to reach USD 6.6 billion by 2033, at a CAGR of 7.0% during the forecast period.

Machining services will gain relevance through computer-guided tools supporting complex geometries and tight tolerances. Industrial customers will be looking for components optimized for advanced manufacturing needs. Future demand will focus on efficiency, repeatability and scalability, enabling manufacturing units to support evolving design standards and production volumes.

Bending

Bending segment is valued at USD 2.5 billion in 2026 and is projected to reach USD 3.4 billion by 2033, at a CAGR of 4.9% during the forecast period.

Bending services will expand with higher capacity equipment supporting flexible design requirements. Infrastructure and industrial projects will increase the demand for precision formed components. Future operations will prioritize programmable systems that enable faster turnaround, less waste, and consistent output supporting larger construction and manufacturing infrastructure.

Others

Others segment is valued at USD 2.3 billion in 2026 and is projected to reach USD 3.2 billion by 2033, at a CAGR of 5.1% during the forecast period.

Other services will include surface treatment, assembly and finishing activities supporting value-added manufacturing. Demand will increase from customers seeking integrated solutions. Future growth will depend on service bundling, quality assurance and customization while supporting streamlined procurement and better project coordination.

By Material Type, the market is divided into:

Carbon Steel

Carbon Steel segment is projected to reach USD 14.6 billion by 2033, at a CAGR of 6.1% during the forecast period.

The use of carbon steel will remain strong due to cost efficiency and structural reliability. Construction and industrial applications will sustain demand. Future adoption will focus on improved coatings and processing technologies that support durability, corrosion resistance and extended lifecycle performance in large-scale projects.

Alloy Steel

Alloy Steel segment is projected to reach USD 8.8 billion by 2033, at a CAGR of 7.0% during the forecast period.

Demand for alloy steel will increase through applications requiring increased strength and thermal resistance. Automotive and industrial equipment manufacturing will drive growth. Future material developments will support lighter structures, improved performance and compatibility with advanced manufacturing technologies meeting strict engineering standards.

Stainless Steel

Stainless Steel segment is projected to reach USD 7.0 billion by 2033, at a CAGR of 6.7% during the forecast period.

Adoption of stainless steel will expand due to corrosion resistance and hygiene benefits. Energy and aerospace applications will support usage growth. Future demand will be consistent with sustainability goals, recycling standards and performance reliability supporting long-term operational efficiency in critical industries.

Others

Others segment is projected to reach USD 2.7 billion by 2033, at a CAGR of 4.4% during the forecast period.

Other material categories will include specialty metals supporting specific applications. Demand will emerge from innovation-driven sectors requiring tailored assets. Future material adoption will focus on adaptability, performance optimization and alignment with emerging regulatory and environmental expectations.

By End-User Industry, the market is further divided into:

Construction

Construction segment is projected to reach USD 12.7 billion by 2033 with a share of 37.6% in 2025.

Construction will remain a primary demand driver through infrastructure upgrades and urban growth. Steel fabrication will support the structural framework and modular design. Future activity will focus on speed, accuracy and sustainability supporting large public and private development initiatives.

Automotive

Automotive segment is projected to reach USD 7.4 billion by 2033 with a share of 22.2% in 2025.

Automotive demand will increase through lightweight design trends and electric vehicle production. Fabricated steel components will support safety and efficiency standards. Manufacturing of the future will focus on precision parts, scalable output, and integration with automated assembly environments.

Aerospace

Aerospace segment is projected to reach USD 5.3 billion by 2033 with a share of 15.5% in 2025.

Aerospace demand will depend on high-performance manufactured components supporting safety-critical applications. Precision and quality of materials will remain central. Future growth will be in line with advanced design requirements, strict compliance norms and increased production efficiency across supply chains.

Energy

Energy segment is projected to reach USD 3.9 billion by 2033 with a share of 11.8% in 2025.

Demand for the energy sector will increase through renewable projects and grid expansion. Steel construction will support the structural and equipment requirements. Future focus will be on sustainability, environmental resistance and reliability supporting long-term energy infrastructure development.

Manufacturing

Manufacturing segment is projected to reach USD 2.8 billion by 2033 with a share of 8.5% in 2025.

Industrial automation and capacity expansion will strengthen manufacturing demand. Fabricated steel components will enable machinery and facility upgrades. Future requirements will emphasize customization, efficiency, and compatibility with smart manufacturing systems.

Others

Others segment is projected to reach USD 1.1 billion by 2033 with a share of 4.5% in 2025.

Other end-user industries will contribute through specialized tools and emerging applications. Technological diversification will increase demand. Future partnerships will depend on flexible manufacturing capabilities supporting emerging industrial use cases and performance expectations.

Competitive Landscape and Strategic Insights

The North America steel fabrication market continues to hold a strong position across production, infrastructure upgrades, energy projects, and manufacturing activity. Steel fabrication supports buildings, bridges, industrial facilities, and transportation networks, reinforcing regional economic development. Increasing investments in business areas and public infrastructure will pressure fabricators to scale operations, adopt modern-day production technology and attention on quicker shipping timelines. The increasing emphasis on sustainability, safety standards and efficient fabric utilization in industries will even benefit the marketplace growth.

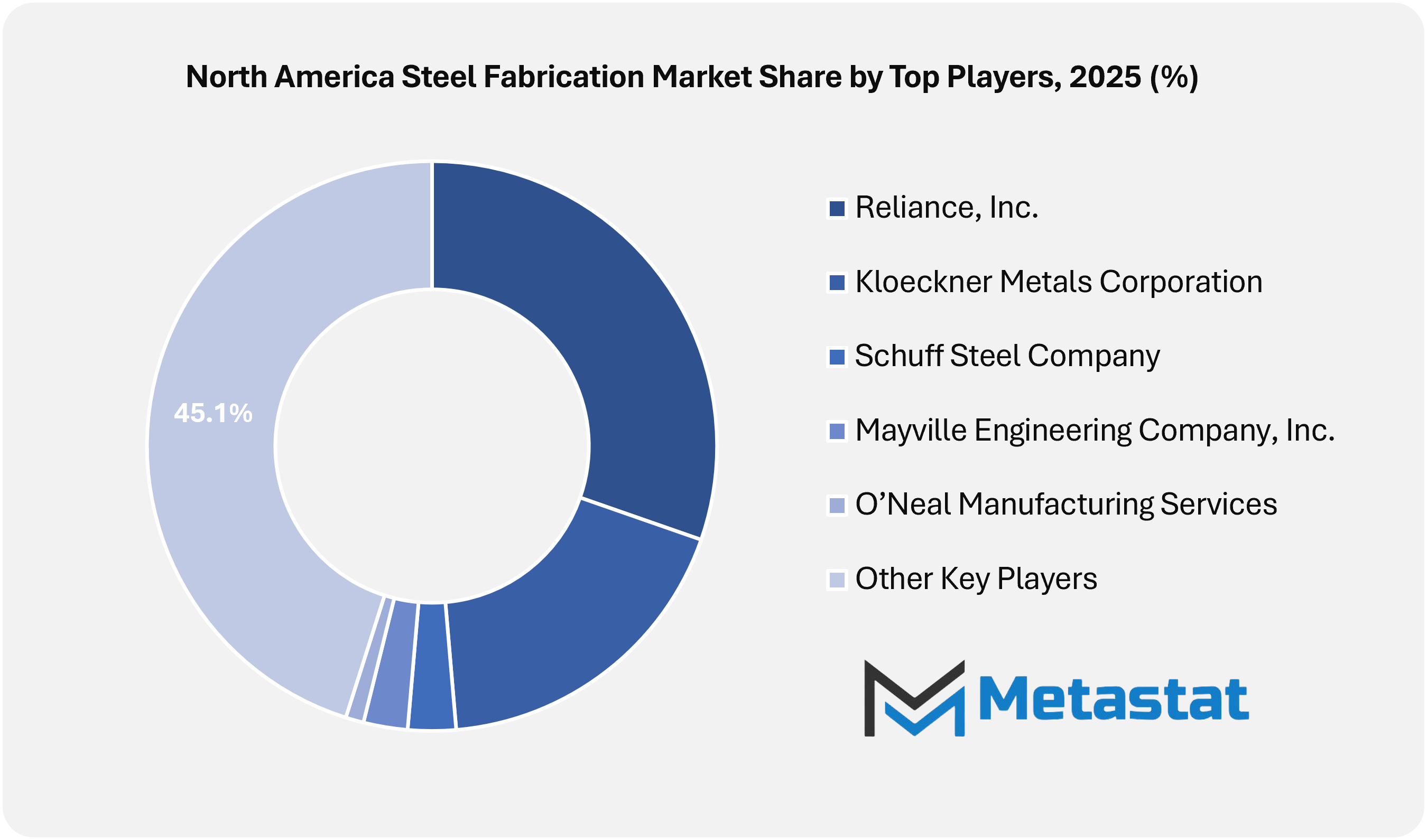

Industry players across North America will focus on improving manufacturing accuracy and reducing waste through automation and digital planning tools. Companies including O’Neal Manufacturing Services, Mayville Engineering Company, Inc., Kapco Metal Stamping, and Standard Iron & Wire Works, LLC will support their positions by supplying customized fabrication solutions tailored to project needs. EVS Metals, Inc., Global Fabrication II, LLC, and FabTech US will maintain to amplify talents in cutting, welding and forming to serve numerous give up users. Operational efficiency and consistent quality will stay the key elements shaping competitive advantage.

Large-scale suppliers and service providers will play a vital role in supporting complex manufacturing requirements. Kloeckner Metals Corporation, Reliance, Inc., Schuff Steel Company and American Structural Corporate will leverage extensive distribution networks and integrated service models to meet growing demand. SteelFab, Inc. and High Steel Structures LLC will be active in structural steel projects involving commercial buildings and large infrastructure works. These companies will benefit from long-term contracts and repeat business driven by reliable performance and technical reliability.

Specialized fabricators will also contribute to speed to market through specialized expertise and flexible production capabilities. Swanton Welding & Machining and Steel, LLC will support areas requiring precision manufacturing and heavy-duty components. Across the market, collaboration with construction firms, engineers and project developers will shape the future growth path. North America steel fabrication will move forward with a strong focus on innovation, workforce skills development and reliable supply chains, supporting sustained demand across multiple industries.

Forecast and Future Outlook

Market size is forecast to rise from USD 20.3 billion in 2025 to over USD 33.2 billion by 2033.

The North America steel fabrication market will largely reflect consolidation among medium-sized players seeking efficiency and technological expansion. Strategic partnerships with engineering firms, logistics providers and construction technology platforms will reshape the competitive landscape. Market participation will reward firms able to translate design intent into executable steel solutions rather than competing on output alone. In the coming years, success in the North America steel fabrication market will depend on execution intelligence, project adaptability and structural expertise rather than detail metrics.

Steel Fabrication Market Key Segments:

By Service Type:

Cutting

Welding

Machining

Bending

Others

By Material Type:

Carbon Steel

Alloy Steel

Stainless Steel

Others

By End-User Industry:

Construction

Automotive

Aerospace

Energy

Manufacturing

Others

Key North America Steel Fabrication Industry Players

This research report categorizes the North America Steel Fabrication market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Steel Fabrication market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Steel Fabrication market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 6.3% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Service Type, Material Type, End-User Industry, and Region

By Service Type

Cutting

Welding

Machining

Bending

Others

By Material Type

Carbon Steel

Alloy Steel

Stainless Steel

Others

By End-User Industry

Construction

Automotive

Aerospace

Energy

Manufacturing

Others

By Region

North America (By Service Type, Material Type, End-User Industry, and Country)

United States

Canada

Mexico

WHAT REPORT PROVIDES

Full in-depth analysis of the parent Industry

Important changes in market and its dynamics

Segmentation details of the market

Former, on-going, and projected market analysis in terms of volume and value

Stage Hoist market size is valued at USD 236.3 million in 2025 and is projected to reach USD 395.3 million in 2033, at a CAGR of 6.3% from 2026 to 2033.

Global Taper Lock Bushing market is valued at USD 1,187.8 million in 2025 and is projected to reach USD 1,808.0 million in 2033, at a CAGR of 5.4% from 2026 to 2033

Europe Mini Excavators Market Size, Share, Trends, 2033

Europe Mini Excavators market size is valued at USD 2,162.9 million in 2025 and is projected to reach USD 3,004.1 million in 2033, at a CAGR of 4.2% from 2026 to 2033

Europe Mini Excavators Market, Europe Mini Excavators Market Size, Europe Mini Excavators Market Share, Europe Mini Excavators Market Analysis, Europe Mini Excavators Market Growth, Europe Mini Excavators Market Trends, Europe Mini Excavators Market Research Report, Europe Mini Excavators Market Forecast, Europe Mini Excavators, Europe Mini Excavators Market Research, Europe Mini Excavators Industry, Europe Mini Excavators Industry Report, Europe Mini Excavators Market Data, Europe Mini Excavators Statistics, Europe Mini Excavators Market Statistics, Europe Mini Excavators Industry Trends, Europe Mini Excavators Market Report, Europe Mini Excavators Market Trends, Europe Mini Excavators Market News, Europe Mini Excavators Forecasts, Europe Mini Excavators Market Intelligence Report

Global Switch Actuators market size is valued at USD 18.4 billion in 2025 and is projected to reach USD 30.6 billion in 2033, at a CAGR of 6.6% from 2026 to 2033