Global Oil and Gas Engines Market Size, Share, By Engine Type (Gas Engines, Diesel Engines, and Dual-Fuel Engines), By Fuel Type (Diesel, Natural Gas, Propane, and Others), By Power Output (Low Power (<500 HP), Medium Power (500-2000 HP), and High Power (>2000 HP), By End-User (Oil Exploration Companies, Oilfield Services, Gas Processing Plants, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4596

Published

April 10, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

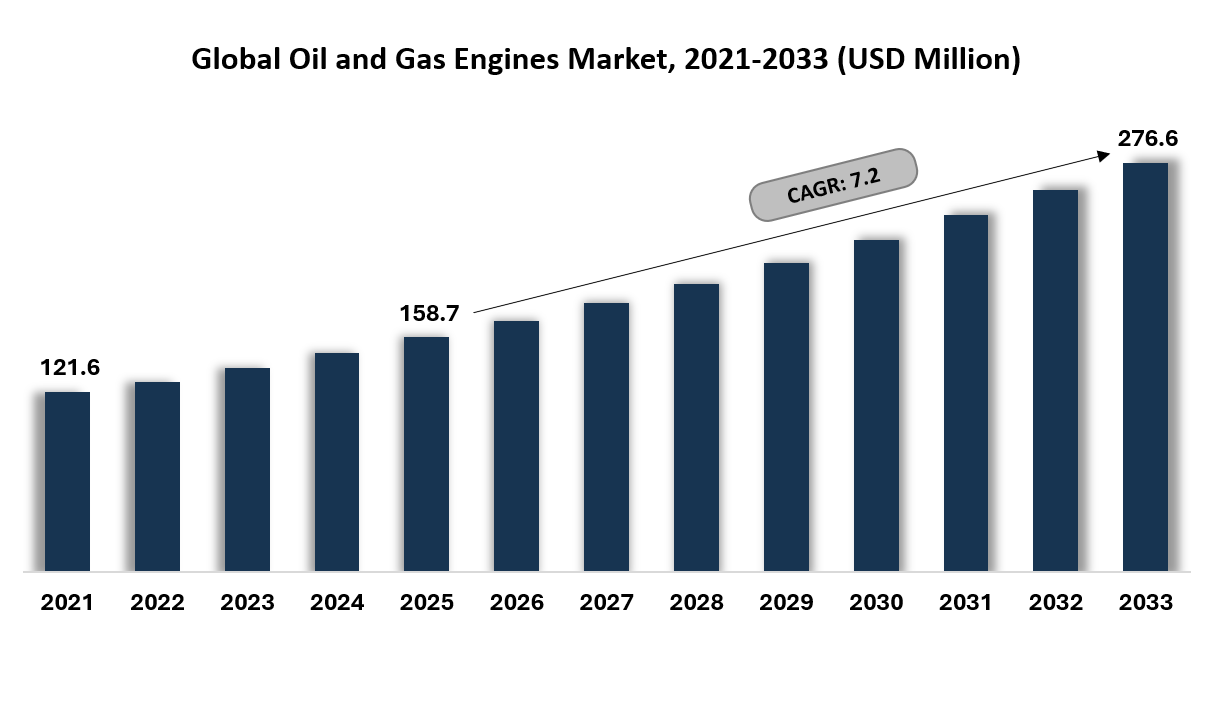

Global Oil and Gas Engines market size is valued at USD 158.7 million in 2025 and projected to grow at a CAGR of 7.2% during the forecast period, reaching USD 276.6 million by 2033.

Global Oil and Gas Engines Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

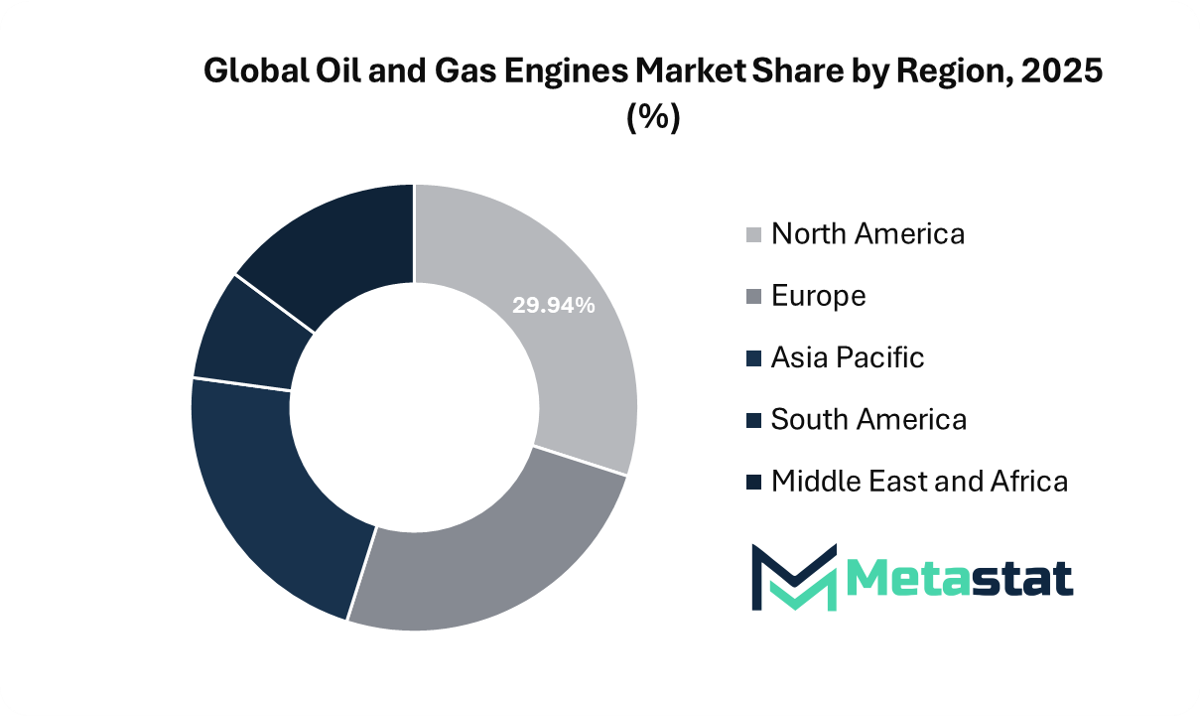

North America holds 29.9% in 2025 with US leading the market share.

Gas Engines segment accounts for a market share of 38.5% in 2025.

Key trends driving growth: Expansion of Natural Gas Compression and Pipeline Infrastructure, along with Rising Power Demand Across Drilling, Production, and Remote Oilfield Operations.

Opportunities include Adoption of Dual-Fuel, Low-Emission, and Digitalized Engine Systems Across Oil and Gas Operations.

Key insight: Rising industrial energy demand and modernization of upstream operations continue to strengthen adoption of high-efficiency engines across global oil and gas production sites.

The Global Oil and Gas Engines market represents a critical part of energy infrastructure supporting drilling, exploration, production, and midstream transportation activities. These engines provide reliable mechanical power for pumps, compressors, generators, and drilling rigs operating across remote oilfields and offshore production facilities. Rising need for dependable power solutions across upstream and midstream operations continues to support growth in the Global Oil and Gas Engines market.

Growth in the Oil and Gas Engines market remains closely linked to rising oil and gas production activities, pipeline development projects, and increasing power requirements across industrial economies. Operators rely on high-performance engines capable of operating under demanding conditions, including high temperatures, remote locations, and continuous heavy-duty workloads. Such operating requirements are supporting adoption of advanced gas engines and dual-fuel systems that improve efficiency and reduce fuel consumption.

Market Dynamics

Growth Drivers:

Expansion of Natural Gas Compression and Pipeline Infrastructure.

Expansion of natural gas transportation networks across major producing regions continues to strengthen the Global Oil and Gas Engines market. Compression stations depend on high-performance engines to maintain pressure across pipelines and ensure efficient transmission of natural gas over long distances. Ongoing pipeline construction and network modernization are creating sustained demand for reliable gas engine solutions.

Rising Power Demand Across Drilling, Production, and Remote Oilfield Operations

Oil and gas extraction sites often operate in remote locations with limited access to grid-connected power. The Global Oil and Gas Engines market benefits from rising need for dependable engine systems capable of supporting drilling rigs, pumping units, and processing equipment. These engines provide the mechanical and electrical power required for uninterrupted field operations.

Restraints and Challenges:

Stringent Emission Compliance and Decarbonization Pressure on Combustion-Based Assets

Environmental regulations are becoming stricter across the energy and industrial sectors, creating compliance pressure for combustion-based equipment. The Global Oil and Gas Engines market is facing growing need to reduce carbon emissions and improve combustion efficiency. Meeting these requirements often involves additional investment in emission-control systems, engine redesign, and monitoring technologies.

High Maintenance, Fuel Efficiency, and Lifecycle Cost Challenges in Aging Engine Fleets

Many oilfield operations continue to rely on aging engine fleets that require frequent maintenance to sustain performance. The Global Oil and Gas Engines market faces challenges related to higher fuel consumption, increased servicing needs, and rising lifecycle costs associated with older equipment. Operators often face difficult replacement decisions when balancing capital spending against long-term operating efficiency.

Opportunities:

Adoption of Dual-Fuel, Low-Emission, and Digitalized Engine Systems Across Oil and Gas Operations

Advancements in engine design are creating strong opportunities across the Global Oil and Gas Engines market. Dual-fuel engines capable of operating on diesel and natural gas offer improved efficiency, lower emissions, and greater operational flexibility. Increasing adoption of digital monitoring and low-emission engine platforms is helping operators improve field performance while supporting environmental compliance goals.

Market Segmentation Analysis

The Global Oil and Gas Engines market is classified based on Engine Type, Fuel Type, Power Output, and End-User.

By Engine Type, the market is further segmented into:

Gas Engines

Gas Engines segment is valued at USD 65.5 million in 2026 and is projected to reach USD 109.3 million by 2033, at a CAGR of 7.6% during the forecast period.

Rising power demand across production fields will support wider use of gas-based engine systems. Gas engines enable efficient fuel utilization across drilling, compression, and pipeline operations while aligning with growing natural gas availability in key hydrocarbon-producing regions. Adoption of gas engines is supported by cleaner combustion profiles, stable output, and compatibility with existing gas infrastructure.

Diesel Engines

Diesel Engines segment is valued at USD 71.9 million in 2026 and is projected to reach USD 104.2 million by 2033, at a CAGR of 5.4% during the forecast period.

Diesel engines will retain strong relevance across heavy-duty drilling, transport, and pumping operations. Field operators require durable engine systems capable of delivering dependable performance under harsh environmental conditions and long operating cycles. Diesel engines remain important for remote operations where fuel flexibility, reliability, and established service networks support continued deployment.

Dual-Fuel Engines

Dual-Fuel Engines segment is valued at USD 32.5 million in 2026 and is projected to reach USD 63.2 million by 2033, at a CAGR of 9.9% during the forecast period.

Dual-fuel engines allow operators to switch between diesel and gaseous fuels based on site conditions and fuel availability. These systems support fuel cost optimization, improved combustion control, and greater operational continuity across diverse field environments. Demand for dual-fuel engines is increasing as operators prioritize efficiency, flexibility, and lower-emission operation.

By Fuel Type, the market is divided into:

Diesel

Diesel segment is projected to reach USD 101.1 million by 2033, at a CAGR of 5.2% during the forecast period.

Diesel remains a dependable fuel source for engines operating across drilling rigs, pumping systems, and field transport fleets. High energy density supports long operating hours and reliable performance in demanding applications. Diesel use remains significant across remote sites where alternative fuel infrastructure is limited.

Natural Gas

Natural Gas segment is projected to reach USD 117.7 million by 2033, at a CAGR of 8.3% during the forecast period.

Expansion of gas extraction projects and pipeline infrastructure is supporting wider use of natural gas as a primary engine fuel. Cleaner combustion characteristics make natural gas suitable for operators seeking lower emission profiles across production and compression activities. Natural gas-fueled engine systems are gaining traction across regions with expanding gas supply networks.

Propane

Propane segment is projected to reach USD 19.7 million by 2033, at a CAGR of 5.6% during the forecast period.

Propane-based fuel solutions are attracting attention in specialized field applications requiring stable combustion and portable fuel supply. Ease of storage and transport supports use across remote production zones and mobile power applications. Propane adoption will grow gradually across smaller operations and distributed energy environments.

Others

Others segment is projected to reach USD 38.2 million by 2033, at a CAGR of 10.8% during the forecast period.

Alternative fuels such as bio-based fuels and synthetic blends are emerging in pilot and limited deployment stages across energy extraction sites. Ongoing engine testing and fuel trials are supporting long-term emission reduction strategies and greater fuel diversification. Alternative fuel options will support future sustainability initiatives across hydrocarbon production infrastructure.

By Power Output, the market is further divided into:

Low Power (<500 HP)

Low Power (<500 HP) segment is projected to reach USD 66.5 million by 2033.

Low-power engines support light operational equipment used in maintenance activity, monitoring stations, and auxiliary systems near production zones. Compact design enables easier deployment across dispersed field locations and smaller installations. Low-power engines remain valuable for secondary operations requiring reliable and consistent power generation.

Medium Power (500–2000 HP)

Medium Power (500-2000 HP) segment is projected to reach USD 126.2 million by 2033.

Medium-power engines play a central role in compressors, pumping systems, and mid-scale drilling activity across oil and gas infrastructure. Balanced output and operational efficiency make these engines suitable for standard field applications without excessive fuel use. Medium-power engines will account for a significant share of installations across mature and developing oilfields.

High Power (>2000 HP)

High Power (>2000 HP) segment is projected to reach USD 83.9 million by 2033.

High-power engines are essential for large-scale extraction activity requiring substantial mechanical output. These engines support major compressors, offshore drilling equipment, and heavy transport systems across complex field environments. Investment in deepwater and large-capacity exploration projects will support demand for engines above 2000 HP.

By End-User, the Global Oil and Gas Engines market is divided as:

Oil Exploration Companies

Oil Exploration Companies segment is projected to grow at a CAGR of 5.8% during the forecast period.

Oil exploration companies continue to invest in reliable power systems for drilling rigs, seismic survey operations, and heavy extraction equipment. Engine performance has a direct effect on field productivity, equipment uptime, and project continuity. Exploration companies remain major adopters of large-scale engine systems supporting upstream expansion.

Oilfield Services

Oilfield Services segment is projected to grow at a CAGR of 7.6% during the forecast period.

Oilfield service providers require mobile and engine-powered equipment across drilling, maintenance, stimulation, and field logistics operations. Reliability and operating efficiency are essential for supporting project timelines and reducing unplanned downtime. Oilfield service companies will expand engine deployment across pumping fleets, fracturing units, and heavy service vehicles.

Gas Processing Plants

Gas Processing Plants segment is projected to grow at a CAGR of 8.8% during the forecast period.

Gas processing plants rely on efficient engine systems for compression, pumping, and plant-level power supply. Stable engine performance supports uninterrupted operations and effective handling of rising natural gas throughput. Gas processing facilities will increase demand for high-efficiency engines as processing capacity expands.

Others

Others segment is projected to grow at a CAGR of 6.2% during the forecast period.

Other end users include pipeline operators, storage terminal operators, and energy logistics companies involved in fuel movement across large networks. Engine-powered systems support compression, pumping, and transportation functions across these infrastructures. End users continue to generate steady demand for durable and application-specific engine technologies.

By Region:

Based on geography, the Global Oil and Gas Engines market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Oil and Gas Engines Market is set to expand at a CAGR of 7.2% within the forecast period, reaching a market size (TAM) of USD 71.1 million by the end of 2033.

Modernization of pipeline compression infrastructure in Canada and the United States helps the deployment of high-efficiency engines inside the North American market.

Increasing oil and gas exploration investments in China and India create new operational possibilities in Asia Pacific market.

Large hydrocarbon reserves and ongoing oilfield improvement initiatives throughout the Middle East, Africa, and South America hold to create lengthy-term demand for reliable engine structures, strengthening the Oil and Gas Engines market across these strength-rich regions.

Competitive Landscape and Strategic Insights

The Global Oil and Gas Engines market will remain closely associated with energy production activities across upstream, midstream, and downstream operations. Engines play a critical role in powering drilling rigs, compressors, pumps, and other heavy equipment used across oil and gas fields. Rising exploration activity, increasing power requirements, and ongoing expansion of pipeline infrastructure continue to support demand for reliable industrial engine systems. Companies operating in oil and gas environments require equipment that performs consistently under harsh operating conditions, which is supporting steady adoption of high-performance engines designed for durability, efficiency, and continuous operation.

Technological advancement is shaping how engines are designed and deployed across oil and gas operations. Manufacturers are focusing on improving fuel efficiency, reducing emissions, and strengthening engine reliability. Many operators are also seeking engines capable of running on different fuel sources, including natural gas, associated gas, and diesel, depending on field conditions. Digital monitoring systems, predictive maintenance tools, and remote performance tracking are helping operators manage equipment more efficiently and reduce unplanned downtime. These developments are supporting safer operations and improved cost control across demanding field environments.

The market also reflects strong participation from established engineering companies with deep experience in industrial power systems. Key Global Oil and Gas Engines industry participants include Caterpillar Inc., Cummins Inc., Rolls-Royce plc, Bergen Engines AS, Origin Engines, Scania CV AB, DEUTZ AG, Société Internationale des Moteurs Baudouin, and Guangxi Yuchai Machinery Co., Ltd. Additional participants such as IHI Power Systems Co., Ltd., Kubota Engine America Corporation, and Soar Power Group also support the industry through specialized engine solutions and power technologies designed for heavy industrial applications.

Competition among these companies is centered on engine performance, reliability, and adaptability across diverse operating conditions. Many manufacturers are investing in research and development to introduce engines that comply with stricter environmental standards while maintaining the high output required across oil and gas operations. Partnerships with energy companies, expansion of service networks, and strong after-sales support will shape market competition. As energy projects expand across multiple regions, demand for dependable engine systems will remain steady, creating continued opportunities for companies serving the global oil and gas engines market.

Forecast and Future Outlook

Market size is forecast to rise from USD 158.7 million in 2025 to over USD 276.6 million by 2033.

The Global Oil and Gas Engines market is expected to maintain steady expansion during the forecast period, supported by rising energy demand and ongoing investment in hydrocarbon infrastructure. Oilfield operations require dependable mechanical power for drilling rigs, compressors, pumping systems, and related equipment, which continues to strengthen demand for high-performance engine platforms. Greater focus on fuel flexibility, lower emissions, and digitalized engine management is expected to shape future market development.

This research report categorizes the Oil and Gas Engines market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Oil and Gas Engines market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Oil and Gas Engines market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 7.2% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Units

Segmentation

By Engine Type, Fuel Type, Power Output, End-User, and Region

By Region

North America (By Engine Type, Fuel Type, Power Output, End-User, and Country)

United States

Canada

Mexico

Europe (By Engine Type, Fuel Type, Power Output, End-User, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Engine Type, Fuel Type, Power Output, End-User, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Engine Type, Fuel Type, Power Output, End-User, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Engine Type, Fuel Type, Power Output, End-User, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Oil and Gas Engines Market Trends and Future Outlook

Demand for High-Performance Engines in Upstream, Midstream, and Downstream Operations

Advancements in Engine Efficiency, Durability, and Emission Control Technologies

Power Solutions for Energy Generation and Heavy-Duty Industrial Applications

Engine Deployment Trends Across Mining and Remote Off-Grid Operations

Shift Toward Fuel-Flexible, Digitally Monitored, and Low-Emission Engine Systems

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Asset Integrity Management market size is valued at USD 26.1 billion in 2025 and projected to reach USD 40.6 billion by 2033, growing at a CAGR of 5.7%.

Energy Harvesting Module Market Size, Share, Trends, 2033

Energy Harvesting Module market size is valued at USD 707.9 billion in 2025 and is projected to reach USD 1,727.8 billion by 2033, growing at a CAGR of 11.8%.

Energy Harvesting Module market, Energy Harvesting Module Market Size, Energy Harvesting Module Market Share, Energy Harvesting Module Market Analysis, Energy Harvesting Module Market Growth, Energy Harvesting Module Market Trends, Energy Harvesting Module Market Research Report, Energy Harvesting Module Market Forecast, Energy Harvesting Module, Energy Harvesting Module Market Research, Energy Harvesting Module Industry, Energy Harvesting Module Industry Report, Energy Harvesting Module Market Data, Energy Harvesting Module Statistics, Energy Harvesting Module Market Statistics, Energy Harvesting Module Industry Trends, Energy Harvesting Module Market Report, Energy Harvesting Module Market Trends, Energy Harvesting Module Market News, Energy Harvesting Module Forecasts, Energy Harvesting Module Market Intelligence Report, Energy Harvesting Module market 2033, Energy Harvesting Module market outlook, Energy Harvesting Module market segmentation, Energy Harvesting Module market drivers, Energy Harvesting Module market restraints, Energy Harvesting Module market opportunities, Energy Harvesting Module market CAGR, Energy Harvesting Module suppliers, Energy Harvesting Module manufacturers, Energy Harvesting Module market by region, North America Energy Harvesting Module market, Asia Pacific Energy Harvesting Module market, Europe Energy Harvesting Module market, Energy Harvesting Module market competitive landscape, Energy Harvesting Module market key players, Photovoltaic and Light Energy Harvesting market, Thermoelectric and Heat Energy Harvesting market, Piezoelectric and Vibration Energy Harvesting market, Industrial IoT and Condition Monitoring market, Smart Buildings and Home Automation market

Concentrated Solar Power Market Size, Share, Trends, 2033

Concentrated Solar Power market size is valued at USD 7.5 billion in 2025 and is projected to reach USD 17.3 billion in 2033, at a CAGR of 11.1% from 2026 to 2033.

Concentrated Solar Power Market, Concentrated Solar Power Market Size, Concentrated Solar Power Market Share, Concentrated Solar Power Market Analysis, Concentrated Solar Power Market Growth, Concentrated Solar Power Market Trends, Concentrated Solar Power Market Research Report, Concentrated Solar Power Market Forecast, Concentrated Solar Power, Concentrated Solar Power Market Research, Concentrated Solar Power Industry, Concentrated Solar Power Industry Report, Concentrated Solar Power Market Data, Concentrated Solar Power Statistics, Concentrated Solar Power Market Statistics, Concentrated Solar Power Industry Trends, Concentrated Solar Power Market Report, Concentrated Solar Power Market Trends, Concentrated Solar Power Market News, Concentrated Solar Power Forecasts, Concentrated Solar Power Market Intelligence Report

Global Leak Detection Software market size is valued at USD 985.8 million in 2025 and is projected to reach USD 1,713.0 million in 2033, at a CAGR of 7.1% from 2026 to 2033

Global Leak Detection Software Market, Global Leak Detection Software Market Size, Global Leak Detection Software Market Share, Global Leak Detection Software Market Analysis, Global Leak Detection Software Market Growth, Global Leak Detection Software Market Trends, Global Leak Detection Software Market Research Report, Global Leak Detection Software Market Forecast, Global Leak Detection Software, Global Leak Detection Software Market Research, Global Leak Detection Software Industry, Global Leak Detection Software Industry Report, Global Leak Detection Software Market Data, Global Leak Detection Software Statistics, Global Leak Detection Software Market Statistics, Global Leak Detection Software Industry Trends, Global Leak Detection Software Market Report, Global Leak Detection Software Market Trends, Global Leak Detection Software Market News, Global Leak Detection Software Forecasts, Global Leak Detection Software Market Intelligence Report