Polyether Polyols for Polyurethane Market Size, Share, and Industry Analysis, By Type (PO-Based Polyols and Natural Oil-Based Polyols), By Application (Flexible Foams, Rigid Foams, Adhesives, and Others (Coatings, Sealants, Elastomers)), By End-Use Industry (Automotive, Construction, Consumer Goods, Electronics, Appliances, Footwear, Apparel, and Others (Aerospace, Marine, Industrial, Medical, and Packaging)), Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4540

Published

February 4, 2026

Pages

310 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

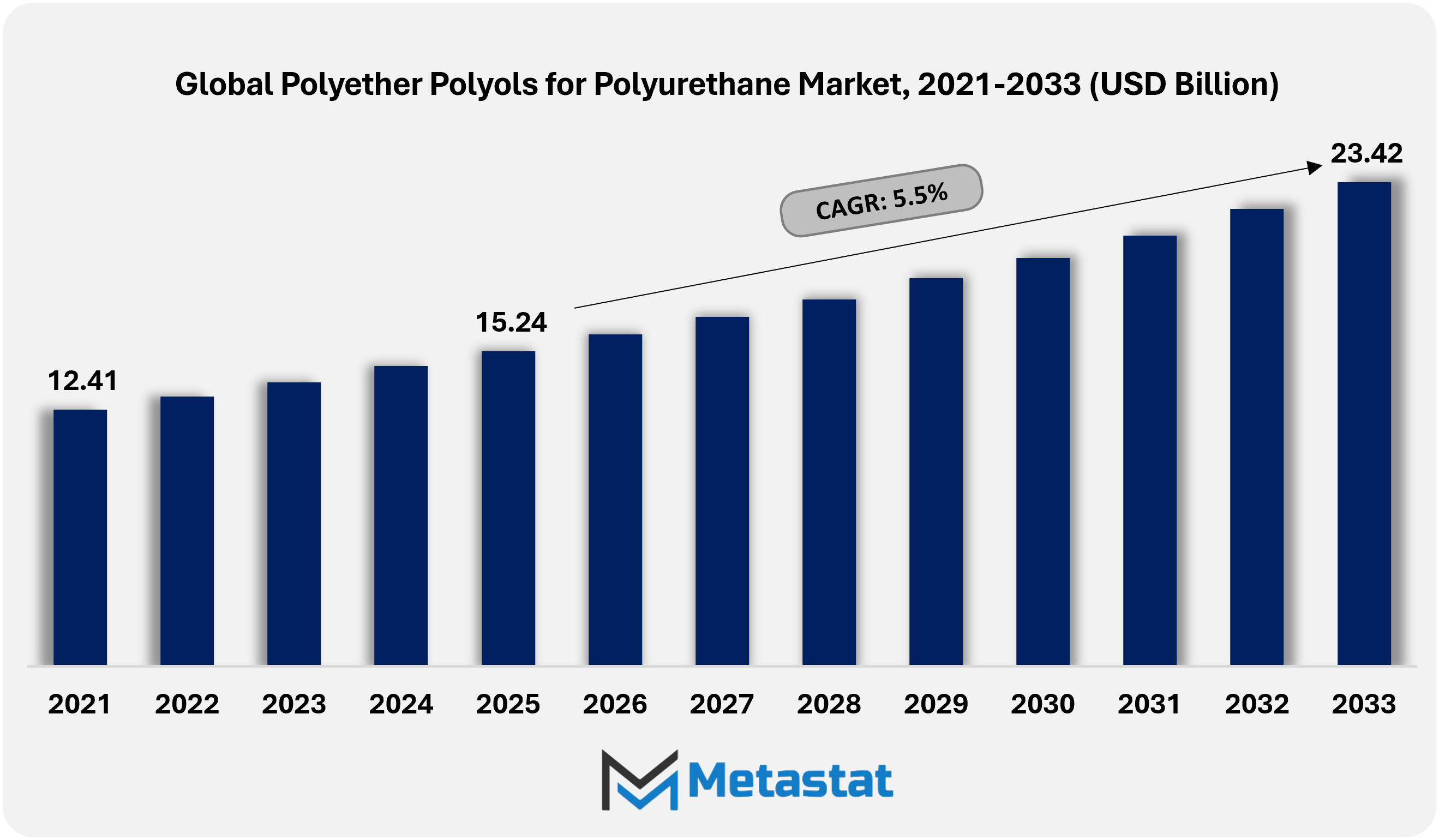

The global Polyether Polyols for Polyurethane market was valued at USD 15.2 billion in 2025 and is projected to reach USD 23.4 billion by 2033, registering a CAGR of 5.5% during 2026-2033.

The global Polyether Polyols for Polyurethane market volume was 4,821.6 kilotons in 2024 and expected to grow at a CAGR of 2.2% within forecast period.

Global Polyether Polyols for Polyurethane Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Polyether Polyols for Polyurethane market valued at USD 15.2 billion in 2025, growing at a CAGR of around 5.5% through 2033, with potential to exceed USD 23.4 billion.

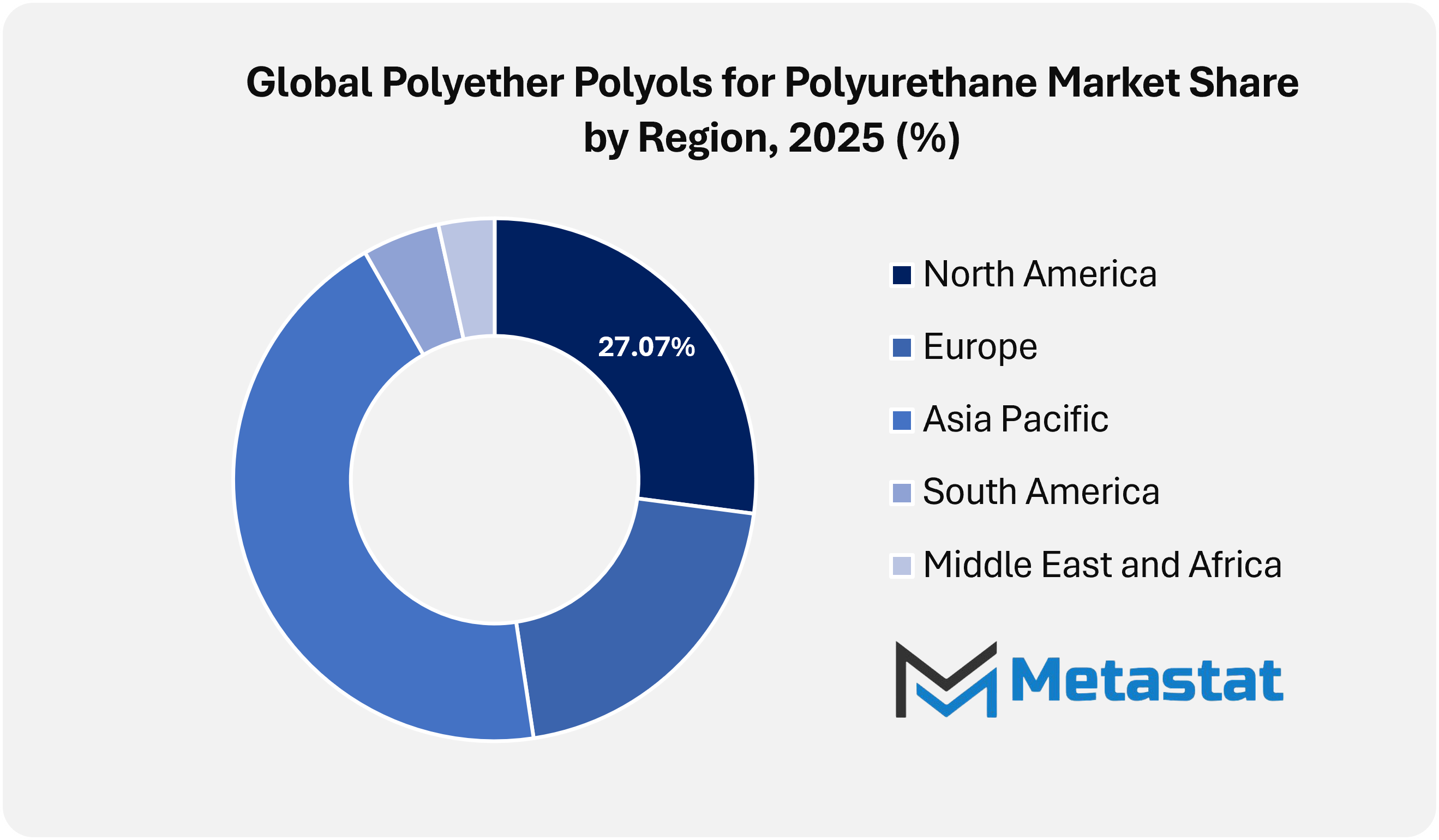

North America held 27.1% share in 2025, led by the United States within the region.

PO-based polyols segment accounts for 82.4% share in 2025, propelled by ongoing R & D and expanding polyurethane applications.

Key trends driving growth: Growing demand for flexible and rigid polyurethane foams in furniture, bedding, automotive seating, and building insulation is boosting consumption of polyether polyols for polyurethane.

Opportunities include development and commercialization of bio-based or low-carbon polyether polyols such as those derived from natural oils or recycled carbon sources and premium growth opportunities in sustainable polyurethane applications.

Key insight: Increased demand for lightweight, durable, and energy-efficient materials is propelling the global polyether polyols for polyurethane market across construction, automotive, and consumer applications.

The polyether polyols for polyurethane market within the global chemicals and materials industry expands beyond traditional boundaries as innovation, regulation and end-use expectations continue to change in the coming years. Instead of adhering to established production models or conventional application narratives, the market is defined by advanced material engineering, refined molecular architectures, and close integration with the downstream manufacturing ecosystem.

Providers will focus on formulating polyether polyols on the molecular level to fulfil relatively precise overall performance necessities in forecast period. The approach enables polyurethane formulations to achieve an optimal balance of flexibility, elasticity, thermal stability, and durability without dependence on standardized grades. As industries increasingly require materials tailored to precise engineering specifications, formulation science is shifting toward a collaborative development framework involving both manufacturers and end users.

Market Dynamics

Growth Drivers:

Rising polyurethane foam usage across construction, automotive, and furniture industries, propelled by insulation performance and lightweighting priorities.

Polyurethane foam usage in furniture, bedding, automotive seating, and building insulation will sustain polyether polyol consumption patterns across core applications. Manufacturing cycles prioritize polyether polyols owing to consistent processing and repeatable performance, supporting insulation standards across residential and commercial infrastructure projects.

Increasing use of polyether polyols in flexible and rigid polyurethane applications driven by durability, chemical stability, and cost efficiency.

Energy performance and lightweighting priorities in the automotive sector will boost adoption of advanced polyurethane insulation and structural additives. Regulatory alignment with thermal efficiency and fuel optimization dreams helps the expanded use of polyether polyols, as manufacturers prioritize decreased material weight while retaining energy, safety, and long-time period sturdiness benchmarks.

Restraints and Challenges:

Volatility in propylene oxide and related petrochemical feedstock pricing will remain a cost-side challenge.

Volatility in propylene oxide and related petrochemical feedstock pricing will continue to be a value-facet venture. Fluctuating input costs affect the predictability of manufacturing, limiting margin sustainability. Strategic sourcing and supply chain changes will become important as producers attempt to stabilize pricing pressures with persistent manufacturing and contractual duties.

Stringent environmental regulations related to emissions and chemical processing limiting manufacturing flexibility.

Environmental and regulatory pressures related to VOC emissions, petro-based feedstock dependence, and polyurethane system compliance will constrain manufacturing flexibility. Compliance necessities increase improvement timelines and value burdens, requiring non-stop development efforts. Regulatory variation will shape the destiny materials' attractiveness in many regional markets.

Opportunities:

Growing adoption of bio-based and low-VOC polyether polyols to meet sustainability targets and regulatory compliance.

Development and commercialization of bio-based or low-carbon polyether polyols derived from natural oils or recycled carbon resources will open avenues for premium growth. Sustainable polyurethane applications will acquire priority in the construction and mobility sectors, helping logo differentiation, regulatory alignment, and long-term fabric innovation within performance-targeted price chains.

Market Segmentation Analysis

The global Polyether Polyols for Polyurethane market is segmented by Type, Application, and End-Use Industry.

By Type, the market is segmented into:

PO-based Polyols

PO-based Polyols segment was valued at USD 13.2 billion in 2026 and is projected to reach USD 19 billion by 2033, at a CAGR of 5.3% during the forecast period.

PO-based polyols continue to attract attention owing to consistent quality, stable processing behaviour, and compatibility with large-scale production systems. Future advances likely emphasize efficiency in manufacturing while supporting evolving industrial standards. The materials remain central where uniform performance and scalable output will be essential.

Natural Oil-based Polyols (NOP)

Natural Oil–based Polyols (NOPs) segment was valued at USD 2.8 billion in 2026 and is projected to reach USD 4.4 billion by 2033, at a CAGR of 6.7% during the forecast period.

Natural oil-based polyols gradually expand as the industry prioritizes resource responsibility and material origin transparency. Ongoing innovations focus on improving mechanical strength and processing reliability. Adoption of natural oil-based polyols strengthens as performance gaps narrow and sustainable material integration becomes a standard manufacturing expectation.

By Application, the market is segmented into:

Flexible Foams

Flexible Foams segment is projected to reach USD 6.3 billion by 2033, at a CAGR of 5.3% during the forecast period.

Flexible foam sees widespread use as comfort, flexibility, and adaptability remain important in seating and cushioning solutions. Future designs focus on extended lifetime and improved recovery properties. The advancements will help evolve consumer expectations around comfort, safety, and long-term usability.

Rigid Foams

Rigid Foams segment is projected to reach USD 12.1 billion by 2033, at a CAGR of 5.8% during the forecast period.

Rigid foam continues to be essential for insulation and structural efficiency, especially as construction standards advance. Future development focuses on thermal performance and dimensional stability. Increasing infrastructure investments will support continued use where strength, insulation value and material stability remain critical.

Adhesives

Adhesive segment is projected to reach USD 1.6 billion by 2033, at a CAGR of 5.4% during the forecast period.

Adhesive applications expand as bonding solutions demand stronger performance on a variety of surfaces. Future formulations will support faster cure and better durability in different conditions. These developments align with the increasing demand for advanced assembly processes and reliable structural bonding.

Others (Coatings, Sealants, Elastomers, etc.)

Others (Coatings, Sealants, Elastomers, etc.) segment is projected to reach USD 3.5 billion by 2033, at a CAGR of 5.2% during the forecast period.

Coatings, sealants, and elastomers evolve with a focus on surface protection and resiliency. Future solutions support resistance against environmental stress and mechanical wear and tear. Adoption will broaden in applications requiring adaptability and sustained long-term performance across specialized industrial use cases.

By End-Use Industry, the market is segmented into:

Automotive

Automotive segment is projected to reach USD 5.8 billion by 2033 with a share of 25.6% in 2025.

Automotive sector expands as lightweight materials support efficiency and design flexibility. Future material development will focus on sustainability and safety compliance. Integration across internal and structural components will increase as manufacturers balance performance expectations with emerging mobility trends.

Construction

Construction segment is projected to reach USD 8.3 billion by 2033 with a share of 34.3% in 2025.

Construction applications continue to expand as insulation efficiency and structural reliability remain priorities. Future construction methods rely on materials that support energy conservation and longevity. The adoption process strengthens as urban development and infrastructure modernization progress globally.

Consumer Goods

Consumer Goods segment is projected to reach USD 4.1 billion by 2033 with a share of 17.8% in 2025.

Manufacturers of consumer goods leverage material flexibility to support design variation and product comfort. Future use will emphasize sustainability and cost efficiency. These materials will remain relevant where everyday products require consistent quality and an adaptable look.

Electronics and Appliances

Electronics & Appliances segment is projected to reach USD 2.5 billion by 2033 with a share of 10.3% in 2025.

The electronics and appliances sector depends on material stability and insulation properties. Future demand will be in line with compact designs and better heat management. These characteristics support continued integration into protective and functional components.

Footwear and Apparel

Footwear & Apparel segment is projected to reach USD 1.7 billion by 2033 with a share of 7.6% in 2025.

Footwear and apparel applications benefit from lightweight and cushioning properties. Future product development focuses on comfort, wear resistance, and design innovation. The increase reflects the growing demand for performance-driven and lifestyle-oriented merchandise.

Others (Aerospace, Marine, Industrial, Medical, Packaging, etc.) segment is projected to reach USD 1 billion by 2033 with a share of 4.5% in 2025.

Key industries will undertake substances for tailored performance necessities. Future advancements will emphasize precision, protection requirements, and durability. Adoption will increase where optimized material performance supports complex operating conditions.

By Region:

Based on geography, the global Polyether Polyols for Polyurethane market is divided into North America, Europe, Asia Pacific, South America, and Middle East and Africa.

North America Polyether Polyols for Polyurethane Market is set to expand at a CAGR of 5.5% during 2026-2033, reaching USD 6.3 billion by 2033.

Continued demand for advanced manufacturing standards and high-performance polyurethane applications will propel polyether polyol consumption across North America.

Expanding automotive production focused on lightweight and fuel-efficient components will accelerate the adoption of advanced polyurethane systems in the North America region.

Rapid urban boom throughout the Asia Pacific region will open long-term possibilities for polyether polyols in construction-associated polyurethane products.

Capacity additions and cost-competitive manufacturing position Asia Pacific as a strategic supply hub.

In the Middle East, Africa and South America, polyether polyols represent a modest but strategically important segment, supported by infrastructure-led polyurethane demand, petrochemical advantages in the Middle East and gradual manufacturing modernization, providing long-term potential through local production growth and rising material awareness.

Competitive Landscape and Strategic Insights

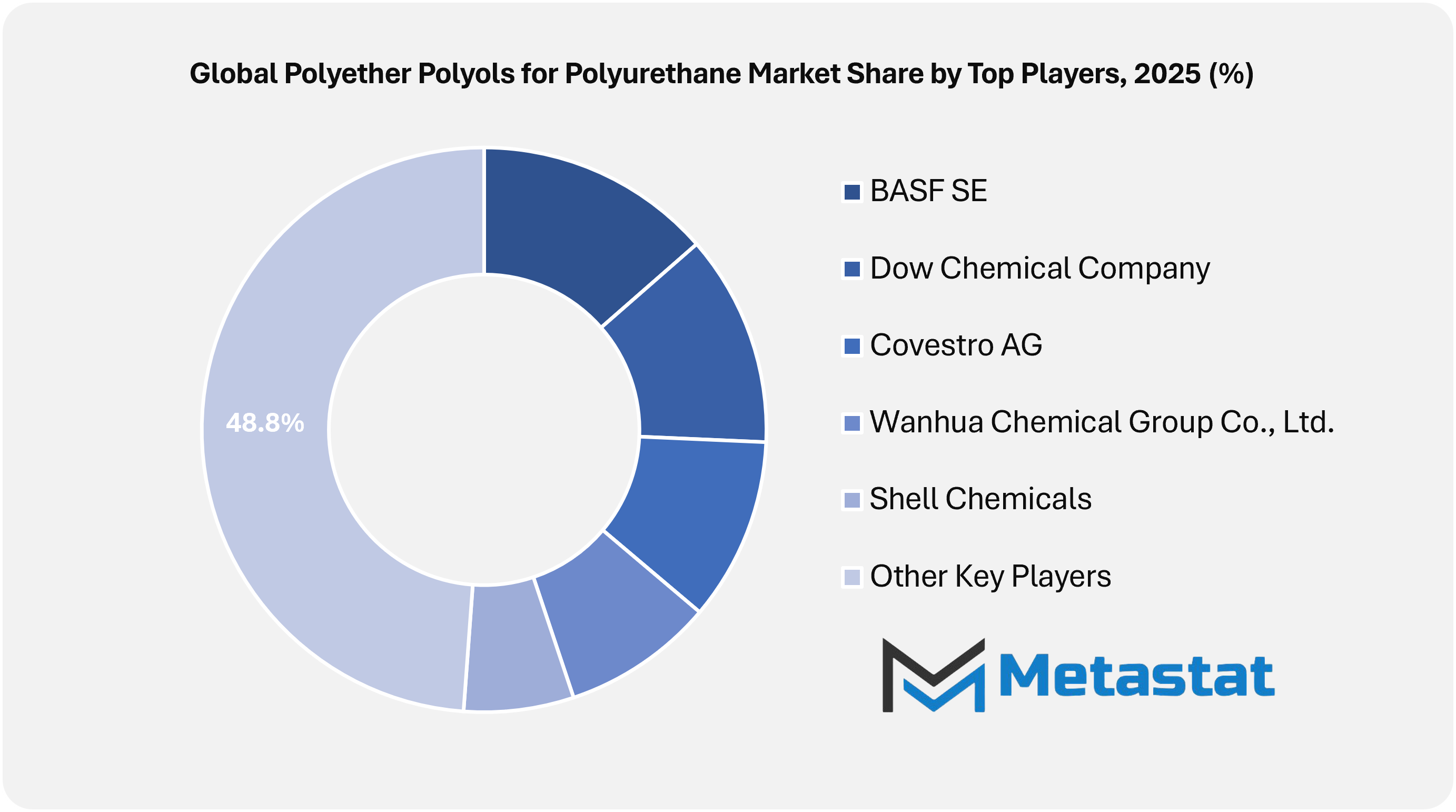

The global Polyether Polyols for Polyurethane market continues to see steady competitive activity, driven by large chemical manufacturers and specialized material producers. The industry is shaped by companies focused on improving product performance, maintaining supply reliability, and meeting changing downstream polyurethane requirements. Players also emphasize quality consistency, technical support, and long-term partnerships with manufacturers across construction, automotive, furniture, and insulation sectors. This balance among scale and specialization will outline how corporations position themselves in the marketplace.

Major industry players including Dow Chemical Company, Covestro AG, BASF SE, and Shell Chemicals maintain strong market positions, supported by global reach, integrated manufacturing assets, and strong R & D capabilities. These companies will continue to invest in process optimization and product refinement to meet demand for durable and sustainable polyurethane materials. Established supply chains and broad customer bases enable rapid response to market shifts while maintaining stable output levels.

Alongside global leaders, numerous local and mid-sized producers play an essential position in shaping opposition. Companies including Yadong Chemical Group, Wanhua Chemical Group Co., Ltd., Shandong INOV Polyurethane Co., Ltd., Jurong Ningwu New Material Co., Ltd., and Chimcomplex S.A. contribute to market diversity by focusing on cost-effective solutions and local demand patterns. Firms such as Sanyo Chemical Industries, Ltd., AGC Chemicals Americas, Inc., Perstorp Holding AB, PCC Group, and Repsol S.A. will reinforce opposition via centered product traces and strategic collaborations, mainly in uniqueness polyols and application-unique formulations.

Key trends across the market includes capacity expansion, technology upgrades, and sustainability-focused initiatives. Saudi Basic Industries Corporation (SABIC) and BASF SE, for instance, strive to align manufacturing techniques with performance and environmental desires, while Covestro AG and Dow Chemical Company focus on innovation to assist high-performance polyurethane systems. At the same time, players together with AGC Chemicals Americas, Inc. and Sanyo Chemical Industries, Ltd. will maintain attention on customized answers for unique commercial wishes.

Overall, the competitive panorama of the Polyether Polyols for Polyurethane market reflects a mix of worldwide leadership and regional strength. As demand from end-users stays stable, organizations will prioritize operational performance, product reliability, and strategic partnerships to keep relevance. This environment will encourage gradual development as opposed to surprising disruption, permitting mounted and emerging players alike to steady their role via regular performance and market-targeted techniques.

Forecast and Future Outlook

Market size is forecast to rise from USD 15.2 billion in 2025 to over USD 23.4 billion by 2033.

Digitization will quietly transform operational and commercial practices. Predictive modeling and data-driven quality control systems enable manufacturers to forecast performance outcomes before physical production begins. The shift reduces physical inefficiencies and shortens development timelines, supporting faster iteration to specific application demands. Looking ahead, the polyether polyols for the polyurethane market will not just expand in volume or geography. It matures into a knowledge-driven segment where innovation, precision chemistry, and responsible production practices will define the competitive position. Its future will be written less by scale and more by the ability to anticipate complex physical requirements in emerging industrial scenarios.

Polyether Polyols for Polyurethane Market Key Segments:

This research report categorizes the Polyether Polyols for Polyurethane market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Polyether Polyols for Polyurethane market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Polyether Polyols for Polyurethane market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 5.5% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Kilotons

Segmentation

By Type, Application, End-Use Industry, and Region

Vapor Degreasing Solvent market size is valued at USD 1,004.1 million in 2025 and projected to reach USD 1,576.4 million by 2033, growing at a CAGR of 5.8%.

Bangladesh Flavours and Fragrances Market Size, Share, Trends, 2033

Bangladesh Flavours and Fragrances market size is valued at USD 793.9 million in 2025 and is projected to reach USD 1,447.9 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Bangladesh Flavours and Fragrances Market, Bangladesh Flavours and Fragrances Market Size, Bangladesh Flavours and Fragrances Market Share, Bangladesh Flavours and Fragrances Market Analysis, Bangladesh Flavours and Fragrances Market Growth, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market Research Report, Bangladesh Flavours and Fragrances Market Forecast, Bangladesh Flavours and Fragrances, Bangladesh Flavours and Fragrances Market Research, Bangladesh Flavours and Fragrances Industry, Bangladesh Flavours and Fragrances Industry Report, Bangladesh Flavours and Fragrances Market Data, Bangladesh Flavours and Fragrances Statistics, Bangladesh Flavours and Fragrances Market Statistics, Bangladesh Flavours and Fragrances Industry Trends, Bangladesh Flavours and Fragrances Market Report, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market News, Bangladesh Flavours and Fragrances Forecasts, Bangladesh Flavours and Fragrances Market Intelligence Report

Biocatalysis and Enzyme Biocatalysts Market Size, Share, Trends, 2033

Biocatalysis and Enzyme Biocatalysts market size is valued at USD 737.8 million in 2025 and is projected to reach USD 1,221.0 million in 2033, at a CAGR of 6.5% from 2026 to 2033.

Biocatalysis and Enzyme Biocatalysts Market, Biocatalysis and Enzyme Biocatalysts Market Size, Biocatalysis and Enzyme Biocatalysts Market Share, Biocatalysis and Enzyme Biocatalysts Market Analysis, Biocatalysis and Enzyme Biocatalysts Market Growth, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market Research Report, Biocatalysis and Enzyme Biocatalysts Market Forecast, Biocatalysis and Enzyme Biocatalysts, Biocatalysis and Enzyme Biocatalysts Market Research, Biocatalysis and Enzyme Biocatalysts Industry, Biocatalysis and Enzyme Biocatalysts Industry Report, Biocatalysis and Enzyme Biocatalysts Market Data, Biocatalysis and Enzyme Biocatalysts Statistics, Biocatalysis and Enzyme Biocatalysts Market Statistics, Biocatalysis and Enzyme Biocatalysts Industry Trends, Biocatalysis and Enzyme Biocatalysts Market Report, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market News, Biocatalysis and Enzyme Biocatalysts Forecasts, Biocatalysis and Enzyme Biocatalysts Market Intelligence Report

Malaysia Tyre Pyrolysis Products Market Size, Share, Trends, 2033

Malaysia Tyre Pyrolysis Products market size is valued at USD 205.9 million in 2025 and is projected to reach USD 421.8 million in 2033, at a CAGR of 9.3% from 2026 to 2033.

Malaysia Tyre Pyrolysis Products Market, Malaysia Tyre Pyrolysis Products Market Size, Malaysia Tyre Pyrolysis Products Market Share, Malaysia Tyre Pyrolysis Products Market Analysis, Malaysia Tyre Pyrolysis Products Market Growth, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market Research Report, Malaysia Tyre Pyrolysis Products Market Forecast, Malaysia Tyre Pyrolysis Products, Malaysia Tyre Pyrolysis Products Market Research, Malaysia Tyre Pyrolysis Products Industry, Malaysia Tyre Pyrolysis Products Industry Report, Malaysia Tyre Pyrolysis Products Market Data, Malaysia Tyre Pyrolysis Products Statistics, Malaysia Tyre Pyrolysis Products Market Statistics, Malaysia Tyre Pyrolysis Products Industry Trends, Malaysia Tyre Pyrolysis Products Market Report, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market News, Malaysia Tyre Pyrolysis Products Forecasts, Malaysia Tyre Pyrolysis Products Market Intelligence Report