Spine Navigation Systems Market Size, Share, By Type (Optical Navigation Systems, Electromagnetic Navigation Systems, Robotic-Assisted Navigation Systems, and Others), By Application (Spinal Fusion Surgery, Deformity Correction, Trauma Surgery, and Others), By Price Range (Premium, Mid-Range, Budget, and Others), By End-user (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4703

Published

April 30, 2026

Pages

315 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

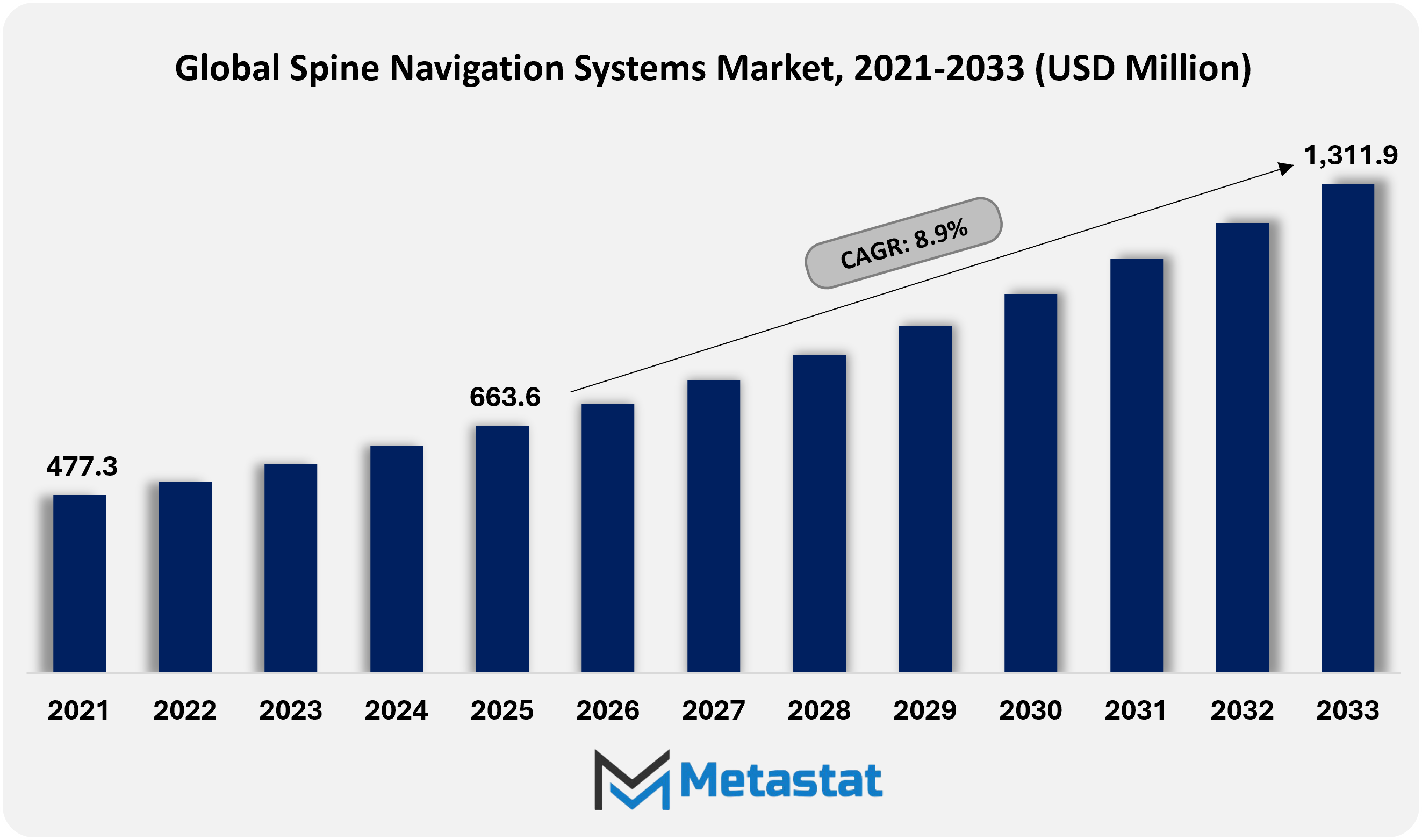

The Global Spine Navigation Systems market is valued at USD 663.6 million in 2025 and projected to grow at a CAGR of 8.9% during the forecast period, reaching USD 1,311.9 million by 2033.

Global Spine Navigation Systems Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

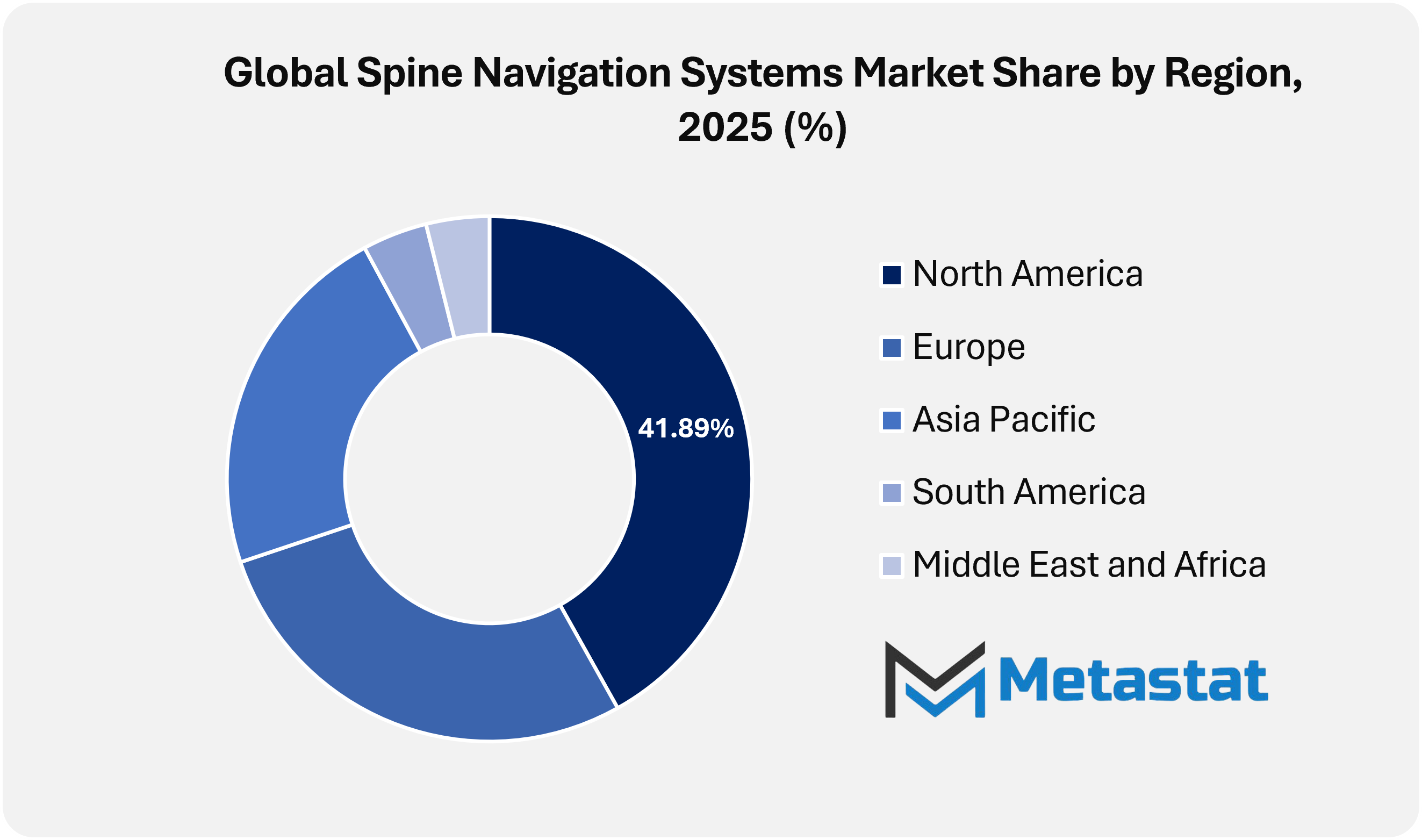

North America holds 41.9% of the global market in 2025, with the U.S. leading the regional market.

Optical Navigation Systems segment accounts for a market share of 41.6% in 2025.

Key trends driving growth: Rising volume of minimally invasive spine procedures and preference for higher placement accuracy propels navigation adoption along with increasing focus on radiation reduction and reproducible surgical workflows supports navigation use across complex cases.

Opportunities include AI-assisted planning combined with robotic-assisted spine platforms creates a strong upgrade cycle for integrated navigation suites.

Key insight: Rising precision demands in spinal surgeries accelerate adoption of advanced navigation technologies across global healthcare systems.

The Global Spine Navigation Systems market within the medical device and surgical imaging industry will move beyond conventional operating room boundaries and penetrate deeper into connected healthcare ecosystems. Over the coming years, surgical navigation platforms will expand their presence in hybrid operating suites where robotics, augmented visualization, and intraoperative imaging function in a synchronized digital environment. Hospitals will increasingly align these systems with enterprise information platforms, enabling procedural metrics, implant positioning data, and surgical performance analytics to flow directly into longitudinal patient records.

Advanced interoperability standards will shape how navigation technologies communicate with robotic arms, C-arm imaging systems, and AI-driven planning software. Instead of functioning as standalone guidance tools, these systems will increasingly operate as command centers that coordinate spatial mapping, predictive modeling, and instrument tracking in real time. Academic medical centers will also adopt them for surgical education and simulation, enabling residents to rehearse complex deformity correction procedures through virtual reconstructions derived from patient-specific scans.

Market Dynamics

Growth Drivers:

Rising volume of minimally invasive spine procedures and preference for higher placement accuracy propels navigation adoption.

Growing patient demand for minimally invasive spine interventions will increase procedure volumes across tertiary centers and private hospitals. Surgeons will prioritize improved implant positioning accuracy to reduce revision rates and improve functional recovery outcomes. In response, the Global Spine Navigation Systems market will gain traction through image-guided systems that support precision, consistency, and measurable surgical outcomes.

Increasing focus on radiation reduction and reproducible surgical workflows supports navigation use across complex cases.

Heightened awareness regarding occupational radiation exposure will encourage hospitals to integrate advanced guidance technologies into spine operating rooms. Standardized and reproducible workflows will become increasingly important to quality benchmarks, particularly for deformity correction and multilevel fixation. The Global Spine Navigation Systems market will benefit from demand for solutions that enable structured approaches with controlled imaging exposure.

Restraints and Challenges:

High system acquisition, service, and disposable costs limits uptake in budget-constrained facilities.

Capital expenditure requirements associated with navigation platforms will remain a major hurdle for mid-sized hospitals and public healthcare networks. Ongoing maintenance contracts and recurring disposable costs will add to operational expenditure burdens. These financial pressures will limit rapid penetration of the Global Spine Navigation Systems market across facilities operating under constrained procurement frameworks.

Setup time, learning curve, and workflow integration challenges slows routine utilization across operating teams.

Operating room efficiency depends on seamless integration of imaging, navigation hardware, and surgical instrumentation. Extended setup time and technical training requirements will affect adoption rates among multidisciplinary teams. Without structured implementation programs, routine use in the Global Spine Navigation Systems market will expand gradually despite clear clinical value.

Opportunities:

AI-assisted planning combined with robotic-assisted spine platforms creates a strong upgrade cycle for integrated navigation suites.

Advancements in artificial intelligence for preoperative trajectory planning are aligning with robotic-assisted execution systems to create integrated digital surgery environments. Hospitals seeking long-term performance gains are expected to invest in unified platforms that connect imaging, navigation, and robotic precision. Such technological convergence will strengthen upgrade cycles in the Global Spine Navigation Systems market and support long-term revenue growth.

Market Segmentation Analysis

The Global Spine Navigation Systems market is classified based on Type, Application, Price Range, and End-user.

By Type, the market is further segmented into:

Optical Navigation Systems

Optical Navigation Systems segment is estimated at USD 300.1 million in 2026 and is projected to reach USD 466.4 million by 2033, at a CAGR of 6.5% during the forecast period.

Optical navigation systems in the Global Spine Navigation Systems market will gain traction through improved camera-based accuracy and real-time instrument tracking during complex spinal procedures. Integration with advanced imaging platforms will enhance surgical precision, reduce intraoperative errors, and support minimally invasive techniques, encouraging adoption across technologically advanced healthcare facilities.

Electromagnetic Navigation Systems

Electromagnetic Navigation Systems segment is estimated at USD 210.3 million in 2026 and is projected to reach USD 342.5 million by 2033, at a CAGR of 7.2% during the forecast period.

Electromagnetic navigation systems in the Global Spine Navigation Systems market will expand owing to their ability to function without a direct line of sight, supporting flexible instrument tracking. Rising demand for adaptable operating room environments and improved workflow efficiency will strengthen adoption of electromagnetic solutions in dynamic surgical settings.

Robotic-Assisted Navigation Systems

Robotic-Assisted Navigation Systems segment is estimated at USD 174.9 million in 2026 and is projected to reach USD 437.3 million by 2033, at a CAGR of 14% during the forecast period.

Robotic-assisted navigation systems in the Global Spine Navigation Systems market are expected to witness strong growth, supported by rising emphasis on automation and data-driven surgery. Advanced robotics integrated with navigation software will improve implant placement accuracy, reduce revision rates, and promote standardized surgical outcomes across high-volume spine centers.

Others

Others segment is estimated at USD 36.7 million in 2026 and is projected to reach USD 65.7 million by 2033, at a CAGR of 8.7% during the forecast period.

Other navigation technologies in the Global Spine Navigation Systems market include hybrid and software-based systems that integrate artificial intelligence and predictive analytics. Continued research investment will support compact, user-friendly solutions designed to improve surgeon confidence and enable precision-driven spinal interventions.

By Application, the market is divided into:

Spinal Fusion Surgery

Spinal Fusion Surgery segment is projected to reach USD 630.8 million by 2033, at a CAGR of 8% during the forecast period.

Spinal fusion surgery applications in the Global Spine Navigation Systems market will expand steadily owing to the rising prevalence of degenerative disc disorders and spinal instability. Navigation-guided fusion techniques will improve screw placement accuracy, reduce complications, and enhance long-term patient outcomes across a wide range of healthcare settings.

Deformity Correction

Deformity Correction segment is projected to reach USD 275.2 million by 2033, at a CAGR of 10.7% during the forecast period.

Deformity correction procedures in the Global Spine Navigation Systems market will benefit from three-dimensional visualization and real-time alignment tracking. Complex scoliosis and kyphosis cases increasingly rely on navigation technologies to achieve balanced spinal reconstruction, supporting safer correction procedures and improved structural stability.

Trauma Surgery

Trauma Surgery segment is projected to reach USD 262.8 million by 2033, at a CAGR of 8.9% during the forecast period.

Trauma surgery applications in the Global Spine Navigation Systems market will grow with the rising incidence of road accidents and sports-related spinal injuries. Navigation systems will support rapid assessment and precise instrument placement, enabling efficient emergency interventions and reducing postoperative complications.

Others

Others segment is projected to reach USD 143.1 million by 2033, at a CAGR of 9.8% during the forecast period.

Other applications in the Global Spine Navigation Systems market will include tumor resection and minimally invasive decompression procedures. Expanding clinical indications will increase system versatility, encouraging broader procedural use across academic hospitals and specialized spine treatment centers.

By Price Range, the market is further divided into:

Premium

Premium segment is projected to reach USD 560.8 million by 2033.

The premium segment of the Global Spine Navigation Systems market will focus on advanced robotic integration, high-definition imaging compatibility, and artificial intelligence-enabled planning tools. Leading healthcare institutions will invest in premium systems to achieve superior surgical precision and strengthen institutional capabilities.

Mid-Range

Mid-Range segment is projected to reach USD 525.9 million by 2033.

Mid-range offerings in the Global Spine Navigation Systems market will balance affordability with essential navigation capabilities. Regional hospitals seeking technological upgrades will adopt mid-range systems to improve procedural accuracy while maintaining controlled capital expenditure.

Budget

Budget segment is projected to reach USD 193.5 million by 2033.

The budget segment in the Global Spine Navigation Systems market will target emerging economies and smaller healthcare providers. Cost-effective navigation systems with core functionality will support broader accessibility, enabling gradual technology penetration in resource-constrained environments.

Others

Others segment is projected to reach USD 31.6 million by 2033.

Other pricing models in the Global Spine Navigation Systems market will include subscription-based software updates and leasing options. Flexible financing structures will encourage technology adoption among institutions seeking lower upfront investment and scalable operational planning.

By End-user, the Global Spine Navigation Systems market is divided as:

Hospitals

Hospitals segment is projected to grow at a CAGR of 8.2% during the forecast period.

Hospitals in the Global Spine Navigation Systems market will remain the primary adopters owing to high surgical volumes and established multidisciplinary infrastructure. Continued investment in digital operating rooms will support integration of navigation systems into standard spinal care pathways.

Ambulatory Surgical Centers

Ambulatory Surgical Centers segment is projected to grow at a CAGR of 11.4% during the forecast period.

Ambulatory surgical centers in the Global Spine Navigation Systems market will adopt compact and efficient systems to support outpatient spine procedures. Increasing emphasis on shorter recovery times and optimized workflow will support demand for streamlined navigation systems.

Specialty Clinics

Specialty Clinics segment is projected to grow at a CAGR of 9.6% during the forecast period.

Specialty clinics in the Global Spine Navigation Systems market will leverage navigation technologies to deliver focused spine care services. Advanced visualization tools will enhance procedural confidence and strengthen competitive positioning within specialized treatment networks.

Others

Others segment is projected to grow at a CAGR of 7.1% during the forecast period.

Other end users in the Global Spine Navigation Systems market will include research institutions and training centers. Growing emphasis on surgical education and simulation-based learning will support adoption of navigation systems for skill development and procedural refinement.

By Region:

Based on geography, the Global Spine Navigation Systems market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Spine Navigation Systems Market is set to expand at a CAGR of 8.9% within the forecast period, reaching a market size (TAM) of USD 523.7 million by the end of 2033.

In North America, rising volumes of minimally invasive spine procedures and strong hospital investment in advanced image-guided technologies are supporting adoption of spine navigation systems.

In North America, the high prevalence of degenerative spinal disorders and favorable reimbursement structures are accelerating demand for precision-based navigation systems.

In Europe, rising adoption of image-guided spine procedures, strong emphasis on surgical precision, and continued investment in advanced orthopedic and neurosurgical infrastructure are supporting steady demand for spine navigation systems.

In Asia-Pacific, expanding healthcare infrastructure and improving access to robotic-assisted surgery are creating major growth opportunities for spine navigation systems.

In Asia-Pacific, increasing medical tourism and rising investment in tertiary care hospitals are supporting adoption of advanced spinal imaging and navigation systems.

Across the Middle East, Africa, and South America, gradual modernization of surgical centers and improving clinical training are supporting steady penetration of spine navigation systems despite budget-sensitive healthcare environments.

Competitive Landscape and Strategic Insights

The Global Spine Navigation Systems market is gaining steady traction as hospitals and specialty care centers continue to prioritize surgical accuracy and patient safety. Spine procedures require a high degree of precision, particularly when placing screws or implants near sensitive nerves and the spinal cord. Navigation systems provide surgeons with real-time, three-dimensional visualization of spinal anatomy during procedures, reducing the risk of error and improving surgical outcomes. As spinal disorders associated with aging, injuries, and lifestyle-related factors continue to increase, demand for advanced surgical guidance technologies will rise. Hospitals and specialty clinics are also investing in digital operating rooms where navigation systems are integrated with imaging and robotic platforms.

Technological advancement plays a critical role in shaping the market. Modern spine navigation systems integrate intraoperative imaging, tracking cameras, and advanced software that guides surgical instruments with high accuracy. Many platforms are designed to work seamlessly with CT scanners and 3D C-arms, allowing surgeons to refine their approach during the procedure itself. This supports lower revision rates and improved recovery outcomes for patients. As awareness of minimally invasive spine surgery continues to rise, adoption of navigation systems will increase, supported by their ability to enable smaller incisions and more controlled instrument placement.

Competition within the industry remains strong, with several established medical device companies and emerging innovators offering specialized solutions. Companies such as Stryker Corporation, Medtronic Plc, Zimmer Biomet, DePuy Synthes, and Smith & Nephew maintain strong positions owing to their broad orthopedic portfolios and extensive global distribution networks. At the same time, players such as Brainlab SE, Globus Medical, NuVasive, Inc., Orthofix Medical Inc., and Alphatec Spine are strengthening their spine-focused platforms through innovation and strategic partnerships. Their systems increasingly combine navigation with robotic assistance, shaping the next phase of market expansion.

In addition, imaging and tracking specialists contribute significantly to market development. Companies such as B. Braun Melsungen AG, GE Healthcare, Ziehm Imaging GmbH, TINAVI Medical Technologies, Perlove Medical, NDI, ClaroNav, PathKeeper Surgical, SI-Bone, Coeur d’Alene Spine and Brain, and Happy Reliable Surgeries Pvt. Ltd. are expanding their presence through focused technology offerings. As healthcare providers continue to prioritize surgical precision and patient safety, the Global Spine Navigation Systems market will move toward deeper integration of navigation, robotics, and real-time imaging, creating a clear pathway for future surgical standards.

Forecast and Future Outlook

Market size is forecast to rise from USD 663.6 million in 2025 to over USD 1,311.9 million by 2033.

Cross-border collaborations among imaging companies and digital health firms are expected to foster integrated surgical ecosystems that blur the boundaries between navigation, robotics, and decision-support algorithms. Through these developments, the Global Spine Navigation Systems market is likely to move beyond hardware sales and position itself at the center of intelligent surgical orchestration, shaping how spinal procedures are planned, executed, and evaluated across healthcare networks worldwide.

Spine Navigation Systems Market Key Segments:

By Type:

Optical Navigation Systems

Electromagnetic Navigation Systems

Robotic-Assisted Navigation Systems

Others

By Application:

Spinal Fusion Surgery

Deformity Correction

Trauma Surgery

Others

By Price Range:

Premium

Mid-Range

Budget

Others

By End-user:

Hospitals

Ambulatory Surgical Centers

Specialty Clinics

Others

Key Global Spine Navigation Systems Industry Players

This research report categorizes the Spine Navigation Systems market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Spine Navigation Systems market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Spine Navigation Systems market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 8.9% from 2026 to 2033

Revenue Unit

USD million

Segmentation

By Type, Application, Price Range, End-user, and Region

By Region

North America (By Type, Application, Price Range, End-user, and Country)

United States

Canada

Mexico

Europe (By Type, Application, Price Range, End-user, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Type, Application, Price Range, End-user, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Type, Application, Price Range, End-user, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Type, Application, Price Range, End-user, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share and Revenue

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

India Maternal Health Monitoring Market Size, Share, Trends, 2033

India Maternal Health Monitoring market size is valued at USD 416.0 million in 2025 and is projected to reach USD 834.4 million in 2033, at a CAGR of 9.1% from 2026 to 2033

India Maternal Health Monitoring Market, India Maternal Health Monitoring Market Size, India Maternal Health Monitoring Market Share, India Maternal Health Monitoring Market Analysis, India Maternal Health Monitoring Market Growth, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market Research Report, India Maternal Health Monitoring Market Forecast, India Maternal Health Monitoring, India Maternal Health Monitoring Market Research, India Maternal Health Monitoring Industry, India Maternal Health Monitoring Industry Report, India Maternal Health Monitoring Market Data, India Maternal Health Monitoring Statistics, India Maternal Health Monitoring Market Statistics, India Maternal Health Monitoring Industry Trends, India Maternal Health Monitoring Market Report, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market News, India Maternal Health Monitoring Forecasts, India Maternal Health Monitoring Market Intelligence Report

Global Anaerobic Incubators market size is valued at USD 177.5 million in 2025 and is projected to reach USD 323.6 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Global Radiochemical Synthesizers market size is valued at USD 450.5 million in 2025 and is projected to reach USD 746.6 million in 2033, at a CAGR of 6.7% from 2026 to 2033.

Global Radiochemical Synthesizers Market, Global Radiochemical Synthesizers Market Size, Global Radiochemical Synthesizers Market Share, Global Radiochemical Synthesizers Market Analysis, Global Radiochemical Synthesizers Market Growth, Global Radiochemical Synthesizers Market Trends, Global Radiochemical Synthesizers Market Research Report, Global Radiochemical Synthesizers Market Forecast, Global Radiochemical Synthesizers, Global Radiochemical Synthesizers Market Research, Global Radiochemical Synthesizers Industry, Global Radiochemical Synthesizers Industry Report, Global Radiochemical Synthesizers Market Data, Global Radiochemical Synthesizers Statistics, Global Radiochemical Synthesizers Market Statistics, Global Radiochemical Synthesizers Industry Trends, Global Radiochemical Synthesizers Market Report, Global Radiochemical Synthesizers Market Trends, Global Radiochemical Synthesizers Market News, Global Radiochemical Synthesizers Forecasts, Global Radiochemical Synthesizers Market Intelligence Report

Thoracolumbar Posterior Fixation Systems Market Size, Share, Trends, 2033

Global Thoracolumbar Posterior Fixation Systems market size is valued at USD 875.8 million in 2025 and is projected to reach USD 1,526.6 million in 2033, at a CAGR of 7.2% from 2026 to 2033

Thoracolumbar Posterior Fixation Systems Market, Thoracolumbar Posterior Fixation Systems Market Size, Thoracolumbar Posterior Fixation Systems Market Share, Thoracolumbar Posterior Fixation Systems Market Analysis, Thoracolumbar Posterior Fixation Systems Market Growth, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market Research Report, Thoracolumbar Posterior Fixation Systems Market Forecast, Thoracolumbar Posterior Fixation Systems, Thoracolumbar Posterior Fixation Systems Market Research, Thoracolumbar Posterior Fixation Systems Industry, Thoracolumbar Posterior Fixation Systems Industry Report, Thoracolumbar Posterior Fixation Systems Market Data, Thoracolumbar Posterior Fixation Systems Statistics, Thoracolumbar Posterior Fixation Systems Market Statistics, Thoracolumbar Posterior Fixation Systems Industry Trends, Thoracolumbar Posterior Fixation Systems Market Report, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market News, Thoracolumbar Posterior Fixation Systems Forecasts, Thoracolumbar Posterior Fixation Systems Market Intelligence Report