U.S. Heavy Machinery Insurance Market Size, Share, By Type (Hiring Mobile Plant, Heavy Construction Vehicles, Earthmoving, Material Handling, and Others), By End User (Public Work, Railroad, Civil Contracting, Construction, Mining, and Others), By Region (California, Texas, Florida, New York, and Rest of United States), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4558

Published

February 18, 2026

Pages

254 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

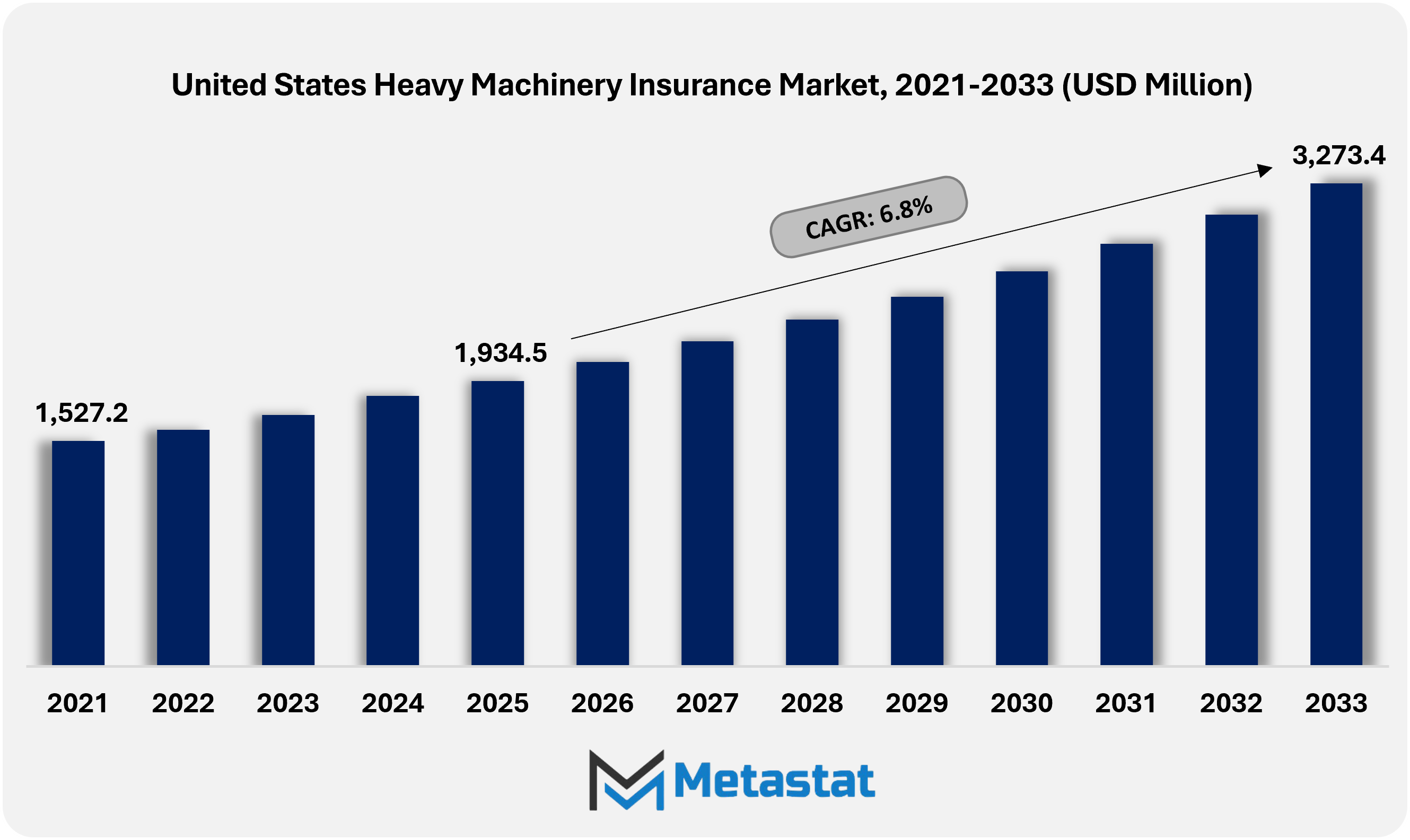

The United States Heavy Machinery Insurance market size was valued at USD 1,934.5 million in 2025. The market is projected to grow from USD 2,062.0 million in 2026 to USD 3,273.4 million by 2033, exhibiting a CAGR of 6.8% during the forecast period.

United States Heavy Machinery Insurance Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

The United States Heavy Machinery Insurance market was valued at USD 1,934.5 million in 2025, growing at a CAGR of 6.8% through 2033, reaching USD 3,273.4 million by 2033.

Hiring Mobile Plant segment accounts for an estimated 11.7% share in 2025, owing to increased equipment rental penetration and short-duration project deployments.

Key trends driving growth: Rising infrastructure and construction investments increase demand for insured heavy machinery fleets.

Key opportunities include integration of IoT and telematics enables usage-based and predictive maintenance insurance models.

Key insight: The United States heavy machinery insurance market is being shaped by infrastructure expansion and equipment financing trends, moving toward data-driven and customized insurance solutions.

The United States heavy machinery insurance market within the insurance industry will move beyond traditional risk transfer and bring itself closer to operational decision making in construction, mining, agriculture and infrastructure activity. Rather than being limited to loss reimbursement, coverage structures will increasingly align with how equipment will be financed, deployed, moved and retired. The change will place insurers in an advisory role that will influence fleet planning, contract negotiations and long-term capital allocation.

Policy design will become more adaptive and scenario oriented. Insurers will design contracts that respond to fluctuating usage patterns, seasonal idle periods and cross-state project dynamics. Premium structures will move toward usage-sensitive frameworks supported by machine telemetry, inspection history and predictive maintenance records. Underwriting decisions will rely on forward-looking exposure modeling that estimates stress, fatigue and operational variations before claims materialize.

Market Dynamics

Growth Drivers

Rising infrastructure and construction investments increase demand for insured heavy machinery fleets.

Large-scale public infrastructure programs and private construction expansion will continue to increase operational risk exposure. Higher project values will require structured risk transfer solutions, driving strong demand in the United States heavy machinery insurance market. Forward-looking contractors will prioritize comprehensive coverage to support long-term project sustainability and regulatory alignment.

Growing leasing and rental market for heavy equipment drives insurance uptake for asset protection.

Equipment leasing and rental activities will expand due to cost optimization strategies in the construction and industrial sectors. Ownership risk concentration will shift toward rental firms, increasing the need for tailored insurance structures. This trend will encourage standardized policies that protect high-value machinery in different operating environments.

Restraints and Challenges

High premium costs deter small contractors and individual operators.

Premium pricing structure will continue to be a limiting factor for small-scale operators with limited financial capacity. Limited bargaining power and low risk pooling will drive up insurance costs, limiting widespread participation. This restriction will slow down entry rates into price-sensitive sectors despite growing awareness of operational risk exposure.

Complex claim settlement processes reduce customer satisfaction and renewal rates.

Lengthy documentation requirements and delayed claim resolution will undermine confidence among policyholders. Operational downtime associated with unresolved claims will increase financial stress. Without a streamlined settlement framework, retention levels will face pressure, impacting the long-term growth sustainability of the United States heavy machinery insurance market.

Opportunities

Integration of IoT and telematics enables usage-based and predictive maintenance insurance models

The adoption of advanced telematics will reshape underwriting accuracy through real-time equipment performance data. Predictive maintenance insights will reduce loss frequency and improve premium calibration. Future-focused insurers will leverage data-driven models to provide flexible, usage-based coverage structures aligned with emerging machinery usage patterns.

Market Segmentation Analysis

The United States Heavy Machinery Insurance market is mainly classified based on Type, End User, and Region.

By Type, the market is further segmented into:

Hiring Mobile Plant

Hiring Mobile Plant segment is valued at USD 240.8 million in 2026 and is projected to reach USD 400.3 million by 2033, at a CAGR of 7.5% during the forecast period.

With the steady increase in the use of rental-based equipment in construction and infrastructure projects, renting mobile plant coverage will gain relevance. Insurers will design policies addressing short-term deployment risk, operator variability and location-specific risk. Digital monitoring and usage-based premiums will strengthen underwriting accuracy in the years to come.

Heavy Construction Vehicles

Heavy Construction Vehicles segment is valued at USD 372.1 million in 2026 and is projected to reach USD 574.8 million by 2033, at a CAGR of 6.4% during the forecast period.

Heavy construction vehicle insurance will focus on protecting high-value assets used in long-term projects. Future policy structures will emphasize damage mitigation, third-party liability and downtime protection. Advanced analytics will support better valuation methods, supporting consistent project timelines and financial forecasting for fleet operators.

Earthmoving

Earthmoving segment is valued at USD 910.2 million in 2026 and is projected to reach USD 1,446.8 million by 2033, at a CAGR of 6.8% during the forecast period.

Earthmoving equipment coverage will expand with the increase in land development and transportation projects. The insurance offering will prioritize protection against mechanical failure, environmental risks and operational hazards. The long-term outlook indicates greater reliance on condition tracking tools, enabling insurers to refine premium structures and loss prevention strategies.

Material Handling

Material Handling segment is valued at USD 456.9 million in 2026 and is projected to reach USD 726.7 million by 2033, at a CAGR of 6.9% during the forecast period.

Material handling machinery insurance will adapt to increasing warehouse automation and industrial logistics demand. Policies will increasingly reflect the risks associated with continuous operations and enclosed environments. Insurers will integrate security compliance metrics into coverage terms, supporting lower incident frequency and better asset lifecycle management.

Others

Others segment is valued at USD 82.0 million in 2026 and is projected to reach USD 124.7 million by 2033, at a CAGR of 6.2% during the forecast period.

The remaining machinery categories will require flexible insurance structures due to different usage patterns and asset configurations. Future coverage will rely on modular policy design, allowing tailored protection. Market participants will emphasize customization to specific equipment requirements without increasing administrative complexity.

By End User, the market is divided into:

Public works and railroads

Public Work & Railroad segment is projected to reach USD 762.7 million by 2033, at a CAGR of 6.4% during the forecast period.

Continued government investment will strengthen public works and insurance for rail operations. Coverage models will focus largely on asset protection, regulatory alignment and public safety accountability. Long-range planning will support resilience against operational disruption and aging infrastructure challenges.

Civil contracting and construction

Civil Contracting & Construction segment is projected to reach USD 1,597.4 million by 2033, at a CAGR of 6.9% during the forecast period.

Civil contracting and construction coverage will grow with urban expansion and smart city initiatives. Insurers will support contractors through comprehensive risk solutions addressing project delays, equipment damage and workforce safety. Technology-driven assessment will increase transparency in multi-site operations.

Mining

Mining segment is projected to reach USD 730 million by 2033, at a CAGR of 7.8% during the forecast period.

Mining sector insurance will continue to be important due to high operational risks and remote site risks. Future policies will emphasize equipment durability, environmental compliance and accident mitigation. Insurers will apply scenario-based modeling to address fluctuating commodity cycles and operating intensity.

Other

Others segment is projected to reach USD 183.3 million by 2033, at a CAGR of 4.6% during the forecast period.

Additional end-user categories will require customized insurance solutions reflecting diverse industry activities. Forward-looking insurers will balance breadth of coverage with cost efficiency. Strategic underwriting will support emerging sectors without compromising portfolio stability.

By Region, the market is further divided into:

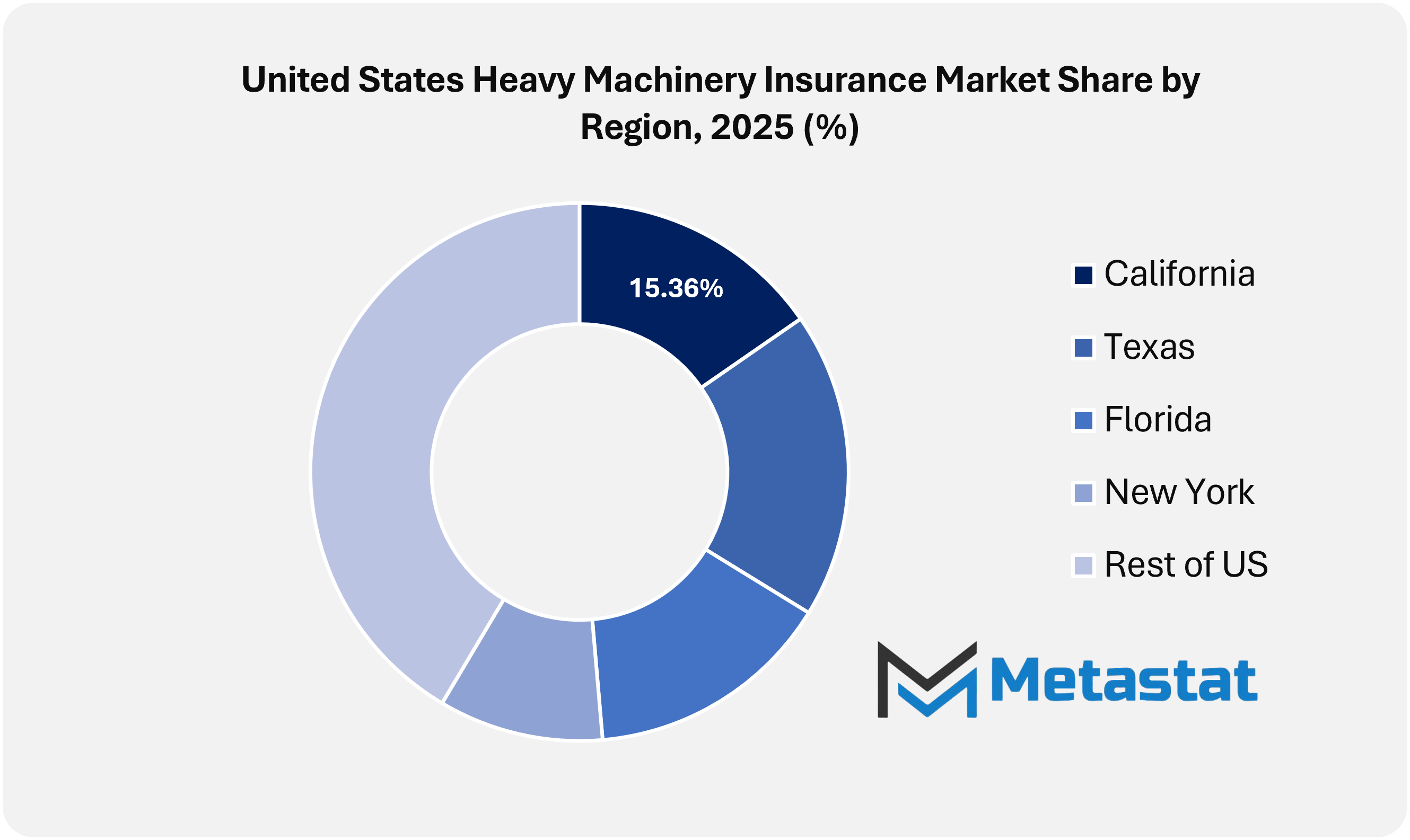

California

California segment is projected to reach USD 492.6 million by 2033 with a share of 15.4% in 2025.

California will continue to impact insurance demand through infrastructure renewal and environmental regulation. Policies will increasingly integrate climate risk considerations. Insurers will adopt stringent compliance standards while supporting large-scale public and private development initiatives.

Texas

Texas segment is projected to reach USD 610.5 million by 2033 with a share of 18.4% in 2025.

Texas will maintain strong insurance demand due to energy projects and transportation expansion. Coverage frameworks will emphasize asset concentration and regional risk factors. Future growth will encourage competitive pricing supported by advanced risk assessment methods.

Florida

Florida segment is projected to reach USD 510.7 million by 2033 with a share of 14.9% in 2025.

Florida's market approach will focus on climate risk and urban growth. Insurance structures will prioritize flexible planning and quick claims response. Long-term strategies will support continuity for machinery deployed in high-risk environments.

New York

New York segment is projected to reach USD 304.4 million by 2033 with a share of 9.9% in 2025.

New York will increase demand through urban redevelopment and transit modernization. Insurers will focus on tighter operating settings and regulatory oversight. The policy innovation will support efficient risk management in limited construction scenarios.

Rest of US

Rest of US segment is projected to reach USD 1,355.2 million by 2033 with a share of 41.5% in 2025.

The remaining areas will contribute to stable growth through regional infrastructure and industrial projects. Insurance demand will reflect localized economic preferences. Balanced coverage solutions will support sustainable machinery use in different geographical conditions.

Competitive Landscape and Strategic Insights

The United States heavy machinery insurance market supports industries that rely on large equipment across construction, manufacturing, agriculture, and infrastructure. Companies that use heavy equipment constantly risk financial losses from accidents, damage, downtime, and lawsuits. Insurance is a key protection, letting them operate confidently while handling risks related to expensive equipment and safety rules. Insurers have changed what they offer to meet the need for specific plans that reflect actual work conditions, not just general policies.

Insurance companies in this market concentrate on creating coverage that matches the worth, use, and environment of heavy machines. Plans usually cover physical damage, liability to others, worker safety, and project-specific risks. Insurers also team up with clients to look at how they operate, how they maintain their gear, and how well they follow rules. This helps companies lower their risk of surprise losses and keep things running during tough times, like equipment failures or site mishaps.

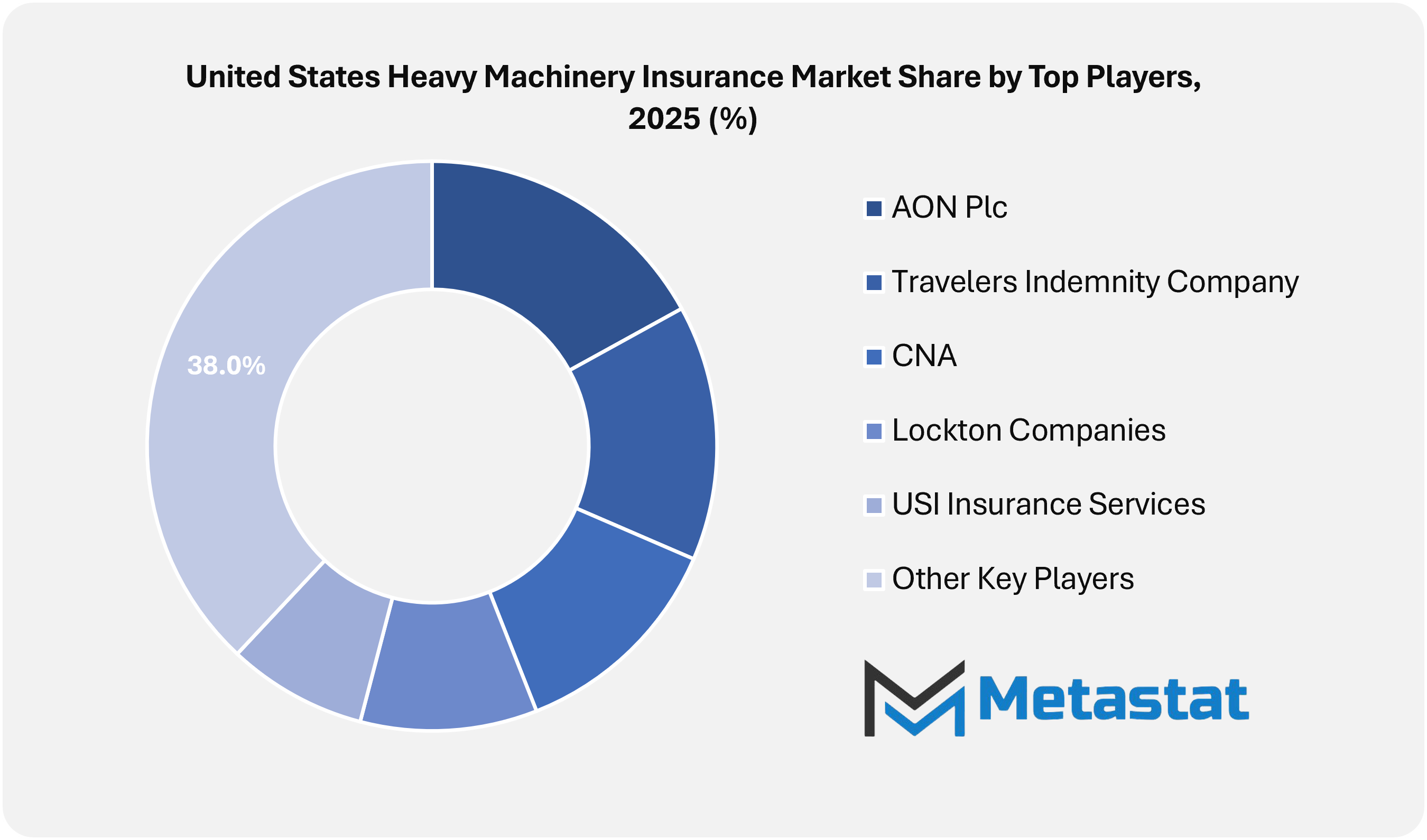

Several established firms shape the competitive landscape of heavy machinery insurance in the United States through broad service networks and industry-focused expertise. HDI United States Insurance Company, Hartford Insurance Group, Inc., Travelers Indemnity Company, CNA, and United Fire & Casualty Company bring strong underwriting capabilities and long-standing market presence. Their experience allows them to design coverage plans that respond to complex claims while supporting businesses during recovery periods. These companies continue to strengthen their position by refining risk assessment models and claim management practices.

Alongside traditional insurers, specialized brokers and advisory firms play a significant role in connecting businesses with suitable insurance solutions. Organizations such as Balsiger Insurance, ALKEME Insurance, USI Insurance Services, Lockton Companies, and Aon plc focus on customized policy placement and ongoing risk guidance. Their involvement will ensure clients receive coverage aligned with operational scale and financial goals rather than standardized packages. This advisory-driven model adds value by helping businesses understand policy terms clearly and avoid coverage gaps.

The United States Heavy Machinery Insurance Market will continue to grow in importance as industries expand operations and invest in advanced equipment. Insurers and brokers operating in this space will likely prioritize flexible coverage, faster claims handling, and proactive risk support to remain competitive. Through collaboration with equipment operators and contractors, these market players will help create a more resilient business environment where financial protection supports long-term growth and operational stability.

Forecast and Future Outlook

Market size is forecast to rise from USD 1,934.5 million in 2025 to over USD 3,273.4 million by 2033.

Regulatory alignment will shape policy language in more precise terms. Insurers will prepare for the tighter safety accountability, emissions oversight and contractual transparency demanded by federal infrastructure programs. Compliance support services will create a blended offering along with coverage that extends beyond indemnity. Over time, the United States heavy machinery insurance market will become integrated with the broader risk governance frameworks adopted by large contractors and public agencies. Insurance will function less like a standalone protection and more like a strategic mechanism that will support operational continuity, financial predictability and asset longevity in complex equipment-intensive projects.

United States Heavy Machinery Insurance Market Key Segments:

By Type:

Hiring Mobile Plant

Heavy Construction Vehicles

Earthmoving

Material Handling

Others

By End User:

Public Work & Railroad

Civil Contracting & Construction

Mining

Others

By Region:

California

Texas

Florida

New York

Rest of United States

Key United States Heavy Machinery Insurance Industry Players

HDI United States Insurance Company

Balsiger Insurance

ALKEME Insurance

Hartford Insurance Group, Inc.

USI Insurance Services

Lockton Companies

AON Plc

Travelers Indemnity Company

United Fire & Casualty Company

CNA

Report Coverage

This research report categorizes the United States Heavy Machinery Insurance market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyzes the key growth drivers, opportunities, and challenges influencing the Heavy Machinery Insurance market. Recent market developments and competitive strategies such as expansion, product and service launch, partnership, merger, and acquisition have been included to outline the competitive landscape.

The report strategically identifies and profiles the key market players and analyzes their core competencies in each sub-segment of the United States Heavy Machinery Insurance market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 6.8% from 2026 to 2033

Revenue Unit

USD Million

Segmentation

By Type, End User and Region

By Type

Hiring Mobile Plant

Heavy Construction Vehicles

Earthmoving

Material Handling

Others

By End User

Public Work & Railroad

Civil Contracting & Construction

Mining

Others

By Region

California

Texas

Florida

New York

Rest of US

WHAT REPORT PROVIDES

Full in-depth analysis of the parent Industry

Important changes in market and its dynamics

Segmentation details of the market

Former, ongoing, and projected market analysis in terms of value

Assessment of niche industry developments

Market share analysis

Key strategies of major players

Emerging segments and regional growth potential

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

The Metastat Insight study indicates that the United States Heavy Machinery Insurance market size was USD 1,934.5 million in 2025.

The United States Heavy Machinery Insurance market is likely to register a CAGR of 6.8% over the forecast period (2026-2033).

Earthmoving is the leading type segment in the United States market.

Rising infrastructure and construction investments increase demand for insured heavy machinery fleets and growing leasing and rental market for heavy equipment drives insurance uptake for asset protection are key driving factors, boosting the market.

United States Heavy Machinery Insurance market is estimated to reach USD 3,273.4 million by 2033.

Top players operating in the Heavy Machinery Insurance industry include HDI United States Insurance Company, Balsiger Insurance, ALKEME Insurance, Hartford Insurance Group, Inc., and USI Insurance Services.

Stage Hoist market size is valued at USD 236.3 million in 2025 and is projected to reach USD 395.3 million in 2033, at a CAGR of 6.3% from 2026 to 2033.

Global Taper Lock Bushing market is valued at USD 1,187.8 million in 2025 and is projected to reach USD 1,808.0 million in 2033, at a CAGR of 5.4% from 2026 to 2033

Europe Mini Excavators Market Size, Share, Trends, 2033

Europe Mini Excavators market size is valued at USD 2,162.9 million in 2025 and is projected to reach USD 3,004.1 million in 2033, at a CAGR of 4.2% from 2026 to 2033

Europe Mini Excavators Market, Europe Mini Excavators Market Size, Europe Mini Excavators Market Share, Europe Mini Excavators Market Analysis, Europe Mini Excavators Market Growth, Europe Mini Excavators Market Trends, Europe Mini Excavators Market Research Report, Europe Mini Excavators Market Forecast, Europe Mini Excavators, Europe Mini Excavators Market Research, Europe Mini Excavators Industry, Europe Mini Excavators Industry Report, Europe Mini Excavators Market Data, Europe Mini Excavators Statistics, Europe Mini Excavators Market Statistics, Europe Mini Excavators Industry Trends, Europe Mini Excavators Market Report, Europe Mini Excavators Market Trends, Europe Mini Excavators Market News, Europe Mini Excavators Forecasts, Europe Mini Excavators Market Intelligence Report

Global Switch Actuators market size is valued at USD 18.4 billion in 2025 and is projected to reach USD 30.6 billion in 2033, at a CAGR of 6.6% from 2026 to 2033