Global Modular Heat Exchanger Market Size, Share, By Type of Modular Heat Exchanger (Shell Heat Exchangers, Tube Heat Exchangers, Plate Heat Exchangers, Air-Cooled Heat Exchangers, Double-Pipe Heat Exchangers, and Finned Tube Heat Exchangers), By Material of Construction (Stainless Steel, Carbon Steel, Copper, Titanium, and Nickel Alloys), By Application Industries (Chemical Processing, HVAC Systems, Power Generation, Food Processing, Beverage Processing, Oil, and Gas), By End-User (Residential, Commercial, Industrial, Institutional, and Marine), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4626

Published

April 15, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

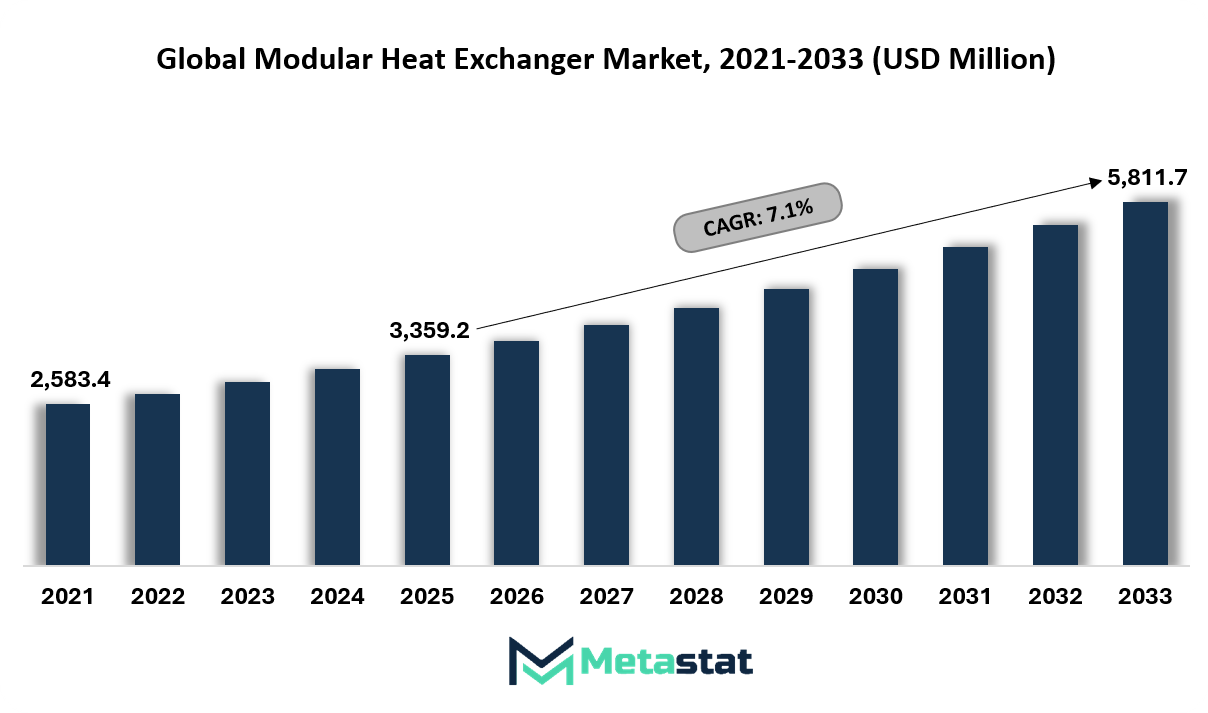

Global Modular Heat Exchanger market size is valued at USD 3,359.2 million in 2025 and projected to grow at a CAGR of 7.1% during the forecast period, reaching USD 5,811.7 million by 2033.

Global Modular Heat Exchanger Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

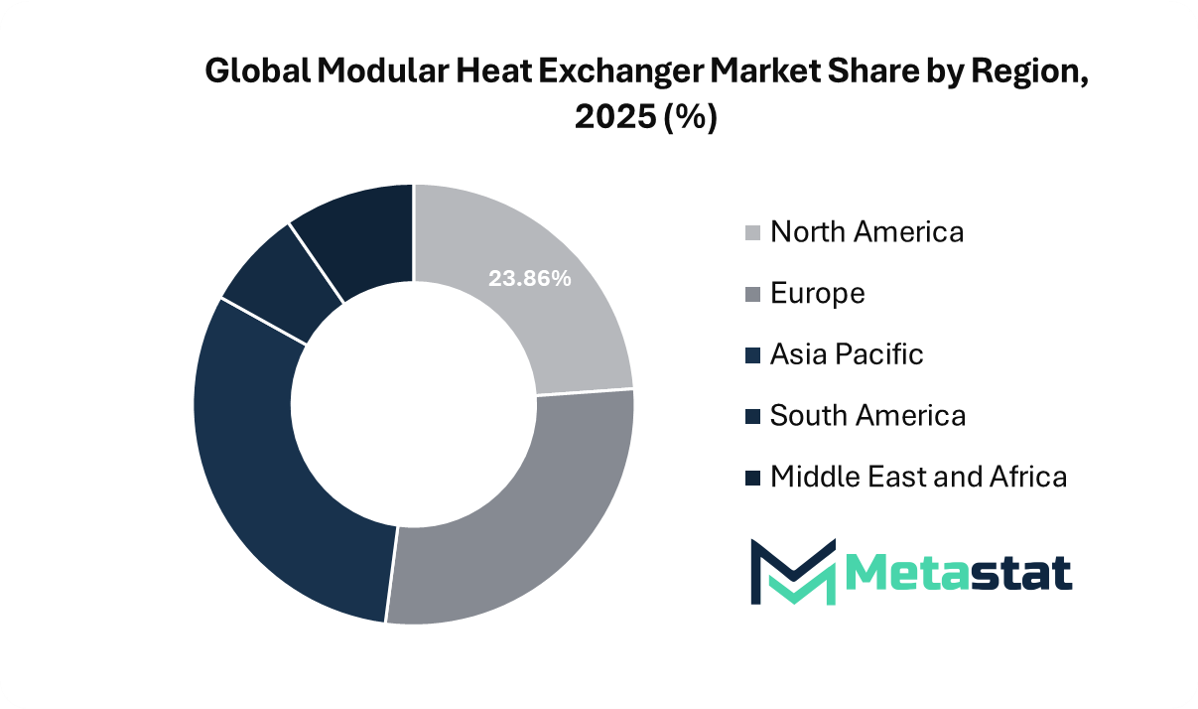

North America holds 23.9% in 2025 with US leading the market share in 2025.

Shell and Tube Heat Exchangers segment account for a market share of 32.0% in 2025.

Key trends driving growth: Increasing demand for energy-efficient thermal management systems in industrial and commercial applications accelerates adoption of modular heat exchangers, along with growth in decentralized and flexible industrial infrastructure drives preference for scalable and easy-to-install modular systems.

Opportunities include expansion of renewable energy and waste heat recovery applications creates strong demand for adaptable and high-efficiency modular heat exchange solutions

Key insight: Rising demand for compact, scalable thermal systems aligned with energy efficiency regulations is accelerating adoption of modular heat exchangers across industrial and infrastructure applications.

The Global Modular Heat Exchanger market is witnessing steady growth, propelled by increased demand for efficient thermal management systems across industrial, commercial, and infrastructure applications. Modular configurations are gaining wider acceptance owing to installation flexibility, scalable capacity, and reduced downtime during maintenance or system upgrades. These systems allow operators to add or replace modules without interrupting broader operations, which supports continuous process efficiency across thermal-intensive environments.

The Global Modular Heat Exchanger market is also benefiting from the shift toward energy optimization and emission control across process industries. Power generation, chemical processing, and HVAC applications are increasingly integrating modular heat exchangers to improve heat recovery efficiency and reduce system-level energy losses. Their design adaptability supports varied temperature ranges, pressure conditions, and fluid compatibility requirements, strengthening product relevance across complex industrial setups.

Market Dynamics

Growth Drivers:

Increasing demand for energy-efficient thermal management systems in industrial and commercial applications accelerates adoption of modular heat exchangers.

Rising focus on energy efficiency across manufacturing sites, commercial buildings, and infrastructure facilities is propelling adoption of modular heat exchangers. End users are prioritizing systems that improve heat transfer performance while lowering operating costs and supporting consistent thermal control. Modular configurations strengthen long-term energy management strategies through scalable deployment, easier maintenance access, and stable operation across varying load conditions.

Growth in decentralized and flexible industrial infrastructure drives preference for scalable and easy-to-install modular systems

The shift toward decentralized production units and flexible industrial infrastructure is strengthening demand for modular heat exchangers across established and emerging markets. Facilities operating in remote, compact, or rapidly expanding environments prefer systems with simplified installation and scalable design. Modular units support phased capacity expansion without major redesign, which improves operational continuity and aligns with evolving production requirements.

Restraints and Challenges:

High initial capital investment and engineering customization requirements limit adoption among small-scale operators

High upfront investment associated with engineering customization, application-specific design, and advanced material selection remains a key restraint for the Global Modular Heat Exchanger market. Small and mid-sized operators often face budget limitations when evaluating installation of modular thermal systems. Extended engineering timelines and integration planning also increase project complexity, which will delay purchasing decisions among cost-sensitive end users.

Maintenance complexity and integration challenges with legacy systems restrict seamless deployment

Maintenance complexity and integration challenges with legacy systems continue to limit wider deployment of modular heat exchangers across older industrial facilities. Compatibility issues with installed equipment often require added engineering intervention, which increases implementation complexity and service requirements. Skilled technical support is also essential for inspection, module replacement, and system balancing, leading to higher lifecycle service costs in facilities dependent on conventional heat exchange infrastructure.

Opportunities:

Expansion of renewable energy and waste heat recovery applications creates strong demand for adaptable and high-efficiency modular heat exchange solutions

Expansion of renewable energy projects and waste heat recovery systems is creating strong growth opportunities for the Global Modular Heat Exchanger market. Industrial operators are increasingly adopting modular solutions to capture and reuse excess thermal energy with higher efficiency. Flexible configurations support a wide range of applications across solar, biomass, district energy, and industrial heat recovery systems, aligning with sustainability goals and emission reduction initiatives.

Market Segmentation Analysis

The Global Modular Heat Exchanger market is classified based on Type of Modular Heat Exchanger, Material of Construction, Application Industries, and End-User.

By Type of Modular Heat Exchanger, the market is further segmented into:

Shell and Tube Heat Exchangers

Shell and Tube Heat Exchangers segment is valued at USD 1,148.4 million in 2026 and is projected to reach USD 1,804.5 million by 2033, at a CAGR of 6.7% during the forecast period.

Shell and tube heat exchangers will remain a leading segment in the Global Modular Heat Exchanger market owing to their strong thermal efficiency, high-pressure tolerance, and broad industrial applicability. These systems are widely preferred across chemical processing, oil and gas, and power generation environments where operational durability remains essential.

Plate Heat Exchangers

Plate Heat Exchangers segment is valued at USD 1,002.2 million in 2026 and is projected to reach USD 1,722.6 million by 2033, at a CAGR of 8% during the forecast period.

Plate heat exchangers are gaining traction in the Global Modular Heat Exchanger market owing to rising preference for compact, energy-efficient thermal systems across industrial and commercial applications. Advanced plate geometry, improved gasket technologies, and better flow distribution are supporting stronger performance in space-constrained installations. Increased focus on lowering energy consumption is further encouraging adoption of solutions that deliver high heat transfer efficiency within a smaller footprint.

Air-Cooled Heat Exchangers

Air-Cooled Heat Exchangers segment is valued at USD 673.0 million in 2026 and is projected to reach USD 1,128.6 million by 2033, at a CAGR of 7.7% during the forecast period.

Air-cooled heat exchangers are witnessing broader adoption in the Global Modular Heat Exchanger market, particularly across regions facing water stress and stricter resource management priorities. Industries operating in water-constrained environments are increasingly favoring air-based cooling solutions that reduce dependence on water-intensive thermal systems. Integration of smart monitoring features is improving operational control, reliability, and maintenance planning in outdoor and heavy-duty applications.

Double-Pipe Heat Exchangers

Double-Pipe Heat Exchangers segment is valued at USD 388.9 million in 2026 and is projected to reach USD 543.4 million by 2033, at a CAGR of 4.9% during the forecast period.

Double-pipe heat exchangers continue to hold relevance in the Global Modular Heat Exchanger market, supported by simple design architecture and suitability for smaller-scale or specialized industrial operations. Their modular nature supports customization across applications requiring controlled heat transfer and straightforward maintenance access. Ongoing design improvements are enhancing thermal efficiency and system reliability, which supports use across niche process environments.

Finned Tube Heat Exchangers

Finned Tube Heat Exchangers segment is valued at USD 381.8 million in 2026 and is projected to reach USD 612.6 million by 2033, at a CAGR of 7% during the forecast period.

Finned tube heat exchangers are witnessing increased adoption in the Global Modular Heat Exchanger market owing to their strong heat dissipation performance and suitability for gas-to-liquid heat transfer applications. Industries focused on thermal optimization are increasingly deploying finned designs to improve system efficiency across demanding operating conditions. Advancements in fin configuration and material integration are also supporting better thermal output and long-term operating stability.

By Material of Construction, the market is divided into:

Stainless Steel

Stainless Steel segment is projected to reach USD 2,126.3 million by 2033, at a CAGR of 8% during the forecast period.

Stainless steel remains the preferred material category in the Global Modular Heat Exchanger market owing to strong corrosion resistance, mechanical durability, and suitability for hygienic and process-intensive applications. Increased demand from food processing, pharmaceuticals, and chemical industries is supporting segment expansion. Improved fabrication techniques and stronger cost efficiency in production are also widening stainless steel usage across sectors requiring long service life and dependable thermal performance.

Carbon Steel

Carbon Steel segment is projected to reach USD 1,591.2 million by 2033, at a CAGR of 5.5% during the forecast period.

Carbon steel continues to hold a significant share in the Global Modular Heat Exchanger market owing to its cost efficiency, structural strength, and suitability for heavy industrial duty. End users across large-scale processing and energy operations prefer carbon steel for applications that require robust mechanical performance. Ongoing improvement in protective coatings and surface treatment technologies is also strengthening corrosion resistance and operating lifespan.

Copper

Copper segment is projected to reach USD 683.1 million by 2033, at a CAGR of 6.5% during the forecast period.

Copper maintains an important position in the Global Modular Heat Exchanger market owing to its high thermal conductivity and suitability for HVAC, refrigeration, and selected commercial thermal systems. Strong heat transfer efficiency supports continued demand across applications where compact and responsive thermal performance remains important. Material innovation and hybrid construction approaches are also improving durability in environments where corrosion resistance requires greater attention.

Titanium

Titanium segment is projected to reach USD 741.0 million by 2033, at a CAGR of 8.1% during the forecast period.

Titanium is gaining wider acceptance across applications involving aggressive chemical media, saline exposure, and highly corrosive operating environments. Exceptional resistance to corrosion positions titanium as a premium material choice in demanding industrial settings. Broader adoption will strengthen further with ongoing efforts focused on improving fabrication efficiency and reducing material processing cost.

Nickel Alloys

Nickel Alloys segment is projected to reach USD 670.1 million by 2033, at a CAGR of 8.1% during the forecast period.

Nickel alloys are increasing in importance within the Global Modular Heat Exchanger market owing to their resistance to extreme temperatures, oxidation, and corrosive process environments. Industries operating under high thermal stress and severe chemical conditions rely on these materials for safe and stable performance. Continued alloy development is supporting stronger durability, improved thermal stability, and reliable service life across critical process applications.

By Application Industries, the market is further divided into:

Chemical Processing

Chemical Processing segment is projected to reach USD 1,493.0 million by 2033.

Chemical processing remains a major application area for modular heat exchangers owing to the need for precise temperature control, process consistency, and reliable thermal transfer across complex production lines. Expansion of specialty chemical manufacturing is supporting additional demand across modular system configurations. Flexible plant integration, efficient heat management, and improved operational safety continue to strengthen product relevance within this segment.

HVAC Systems

HVAC Systems segment is projected to reach USD 1,379.7 million by 2033.

HVAC systems represent a significant application segment in the Global Modular Heat Exchanger market, propelled by urbanization, commercial construction growth, and rising demand for energy-efficient building infrastructure. Modular heat exchangers support compact installation, reliable climate control, and improved thermal management across residential, commercial, and institutional spaces. Integration with smart building systems is further strengthening segment outlook.

Power Generation

Power Generation segment is projected to reach USD 1,008.3 million by 2033.

Power generation remains a core application area in the Global Modular Heat Exchanger market, supported by rising electricity demand and continued investment in thermal efficiency improvement. Conventional power plants and renewable energy systems both require dependable heat exchange solutions that improve recovery efficiency and reduce thermal loss. Modular designs are increasingly preferred for their scalability, maintenance convenience, and suitability for evolving plant architectures.

Food and Beverage Processing

Food and Beverage Processing segment is projected to reach USD 890.9 million by 2033.

Food and beverage processing is expanding its use of modular heat exchangers owing to strict hygiene requirements, controlled temperature processing, and rising emphasis on product consistency. Processing facilities are increasingly deploying advanced thermal systems that support sanitation, energy efficiency, and reliable heat transfer performance. Design innovation focused on cleanability and regulatory compliance continues to strengthen growth across this application area.

Oil and Gas

Oil and Gas segment is projected to reach USD 1,039.7 million by 2033.

Oil and gas remain a strong application segment in the Global Modular Heat Exchanger market, supported by complex thermal operations across upstream, midstream, and downstream activities. Exploration, refining, and process treatment environments require dependable thermal management systems capable of operating under demanding conditions. Modular solutions are gaining preference owing to efficient deployment, flexible capacity expansion, and suitability for remote or operationally challenging sites.

By End-User, the Global Modular Heat Exchanger market is divided as:

Residential

Residential segment is projected to grow at a CAGR of 10.3% during the forecast period.

Residential adoption of modular heat exchangers is increasing gradually with rising interest in energy-efficient home systems, compact heating solutions, and sustainable building design. Modular units support space-saving installation and improved thermal performance across modern residential infrastructure.

Commercial

Commercial segment is projected to grow at a CAGR of 8.1% during the forecast period.

Commercial end users are expanding adoption of modular heat exchangers across office buildings, retail centers, hospitality properties, and mixed-use developments. Efficient thermal management has become increasingly important across commercial infrastructure focused on energy performance and occupant comfort.

Industrial

Industrial segment is projected to grow at a CAGR of 5.9% during the forecast period.

Industrial end users continue to represent the leading share of the Global Modular Heat Exchanger market owing to extensive thermal processing requirements across manufacturing, chemicals, energy, and heavy industry. Modular systems support high-capacity operations through scalable design, improved maintenance access, and efficient process integration.

Institutional

Institutional segment is projected to grow at a CAGR of 7.4% during the forecast period.

Institutional adoption is growing steadily across hospitals, educational facilities, public buildings, and utility-linked infrastructure where reliable thermal control remains essential. Modular heat exchangers support operational continuity, efficient space utilization, and long-term system durability across these environments. Energy-saving priorities and infrastructure modernization programs are also supporting segment development.

Marine

Marine segment is projected to grow at a CAGR of 5.5% during the forecast period.

Marine applications are gaining traction in the Global Modular Heat Exchanger market with rising shipping activity, vessel modernization, and the need for efficient onboard thermal management systems. Heat exchangers play a vital role across engine cooling, auxiliary systems, and marine process applications. Product development focused on corrosion resistance and stable performance in harsh operating conditions continues to strengthen market potential.

By Region:

Based on geography, the Global Modular Heat Exchanger market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America benefits from a strong industrial base and advanced manufacturing ecosystem, supporting demand for high-performance modular heat exchangers across energy, chemical, and HVAC applications.

Europe is witnessing stable demand in the Modular Heat Exchanger market, supported by industrial modernization, strict energy efficiency regulations, and growing adoption of advanced thermal management systems across manufacturing and infrastructure applications.

Asia Pacific presents strong growth opportunities for the Modular Heat Exchanger market, propelled by rapid industrialization, infrastructure development, and expanding thermal processing capacity.

South America is witnessing steady demand for modular heat exchangers across industrial processing, mining, and infrastructure-linked thermal applications.

Middle East and Africa markets are being supported by energy sector expansion, oil and gas developments, and increased infrastructure investment, which are strengthening adoption of modular heat exchange systems across diversified industrial environments.

Competitive Landscape and Strategic Insights

The Global Modular Heat Exchanger market will continue to gain attention owing to the rising need for flexible and efficient thermal management solutions across industries. These systems are designed to support easy installation, scalable capacity, and operational adaptability, making them suitable for sectors where process requirements evolve over time. Their modular structure allows end users to expand capacity without replacing entire systems, which improves cost efficiency and asset utilization. Adoption will remain strong across chemicals, power generation, food processing, and HVAC applications, where precise temperature control plays a critical role in maintaining product quality and operational stability.

Manufacturers are focusing on improving design efficiency and system durability to meet the requirements of modern industrial environments. Material advancements are supporting equipment to operate under higher pressure and temperature conditions while maintaining stable performance over extended operating cycles. Energy efficiency remains a key priority, with industries aiming to reduce operating costs and align with environmental targets. Integration of digital monitoring and smart control systems is also increasing, enabling operators to track performance, optimize operations, and manage maintenance in a more structured manner.

Competition in the Global Modular Heat Exchanger market remains strong, with several established players shaping industry dynamics through product innovation and strategic expansion. Key players include Alfa Laval AB, APEN Group Co., Ltd., Armstrong International Inc., Boyd Corporation, Chart Industries, Inc., Danfoss A/S, De Dietrich Process Systems, Dongguan Hstars Electric Equipment Co., Ltd. (H.Stars Group), ElringKlinger Engineered Plastics GmbH, Envicool Technology Co., Ltd., EVAPCO, Inc., FUNKE Wärmeaustauscher Apparate GmbH, GEA Group AG, Graphite Technology SARL, Güntner GmbH & Co. KG, Hisaka Works Ltd., Kaori Heat Treatment Co., Ltd., Kelvion Holding GmbH, Mersen S.A., Modine Manufacturing Company, Nexson Group, nVent Electric plc, Rittal GmbH & Co. KG, Shanghai Accessen Group Co., Ltd., SPX FLOW, Inc., SWEP International AB, Thermo Fisher Scientific Inc., Thermowave GmbH, Tranter, Inc., and Vahterus Oy. These companies continue to invest in product development and expand their global presence to strengthen competitive positioning.

Regional demand varies, with Asia Pacific emerging as a high-growth region driven by industrial expansion, infrastructure development, and increasing adoption of modular thermal systems. North America and Europe are focusing on modernization and replacement of existing thermal infrastructure with more efficient and advanced solutions. The Global Modular Heat Exchanger market will progress steadily, supported by continuous innovation, rising energy efficiency requirements, and the need for reliable heat exchange systems across diverse industrial applications.

Forecast and Future Outlook

Market size is forecast to rise from USD 3,359.2 million in 2025 to over USD 5,811.7 million by 2033.

The Global Modular Heat Exchanger market is expected to maintain steady growth driven by the increasing need for energy optimization, industrial efficiency, and sustainable operations. Future developments are likely to focus on advanced modular configurations that support higher thermal efficiency, compact designs, and seamless integration into digital industrial ecosystems.

This research report categorizes the Modular Heat Exchanger market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Modular Heat Exchanger market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Modular Heat Exchanger market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 7.1% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Units / Thousand Units

Segmentation

By Type of Modular Heat Exchanger, Material of Construction, Application Industries, End-User, and Region

By Region

North America (By Type of Modular Heat Exchanger, Material of Construction, Application Industries, End-User, and Country)

United States

Canada

Mexico

Europe (By Type of Modular Heat Exchanger, Material of Construction, Application Industries, End-User, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Type of Modular Heat Exchanger, Material of Construction, Application Industries, End-User, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Type of Modular Heat Exchanger, Material of Construction, Application Industries, End-User, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Type of Modular Heat Exchanger, Material of Construction, Application Industries, End-User, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Prepositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Global Modular Heat Exchanger market is estimated to reach USD 5,811.7 million by 2033.

Top players operating in the Modular Heat Exchanger industry include Alfa Laval AB, APEN Group Co., Ltd., Armstrong International Inc., Boyd Corporation, and Chart Industries, Inc.

The Metastat Insights analysis shows that the North America Modular Heat Exchanger market size is estimated to be USD 1,378.8 million by 2033.

Increasing demand for energy-efficient thermal management systems in industrial and commercial applications accelerates adoption of modular heat exchangers and growth in decentralized and flexible industrial infrastructure drives preference for scalable and easy-to-install modular systems are key driving factors, boosting the market.

The Shell and Tube Heat Exchangers is the leading type segment in the Global market.

High initial capital investment and engineering customization requirements limit adoption among small-scale operators will hamper the market growth within the forecast period.

Asia Pacific region dominates the market.

The Global Modular Heat Exchanger market is expected to grow at a CAGR of 7.1% over the forecast period (2026-2033).

The Metastat Insights study shows that the Global Modular Heat Exchanger market size was USD 3,359.2 million in 2025.

Stage Hoist market size is valued at USD 236.3 million in 2025 and is projected to reach USD 395.3 million in 2033, at a CAGR of 6.3% from 2026 to 2033.

Global Taper Lock Bushing market is valued at USD 1,187.8 million in 2025 and is projected to reach USD 1,808.0 million in 2033, at a CAGR of 5.4% from 2026 to 2033

Europe Mini Excavators Market Size, Share, Trends, 2033

Europe Mini Excavators market size is valued at USD 2,162.9 million in 2025 and is projected to reach USD 3,004.1 million in 2033, at a CAGR of 4.2% from 2026 to 2033

Europe Mini Excavators Market, Europe Mini Excavators Market Size, Europe Mini Excavators Market Share, Europe Mini Excavators Market Analysis, Europe Mini Excavators Market Growth, Europe Mini Excavators Market Trends, Europe Mini Excavators Market Research Report, Europe Mini Excavators Market Forecast, Europe Mini Excavators, Europe Mini Excavators Market Research, Europe Mini Excavators Industry, Europe Mini Excavators Industry Report, Europe Mini Excavators Market Data, Europe Mini Excavators Statistics, Europe Mini Excavators Market Statistics, Europe Mini Excavators Industry Trends, Europe Mini Excavators Market Report, Europe Mini Excavators Market Trends, Europe Mini Excavators Market News, Europe Mini Excavators Forecasts, Europe Mini Excavators Market Intelligence Report

Global Switch Actuators market size is valued at USD 18.4 billion in 2025 and is projected to reach USD 30.6 billion in 2033, at a CAGR of 6.6% from 2026 to 2033