Water & Wastewater Treatment Systems for Utilities Market

Water & Wastewater Treatment Systems for Utilities Market Size, Share, By Treatment Type (Oil & Water Separation, Suspended Solids Removal, Dissolved Solids Removal, Biological Treatment, Nutrient & Metals Recovery, Disinfection & Oxidation, and Other Types), By Process and Technology (Conventional Filtration, Membrane Systems, Biological Processes, Advanced Oxidation Processes, Ozonation, and Nutrient Removal), By End-User (Municipal and Industrial), Industry Analysis, Growth, Trends, and Forec

Report ID

MSI-4570

Published

March 22, 2026

Pages

317 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Leading Country

Report Details

Comprehensive Market Analysis And Insights

Market Overview

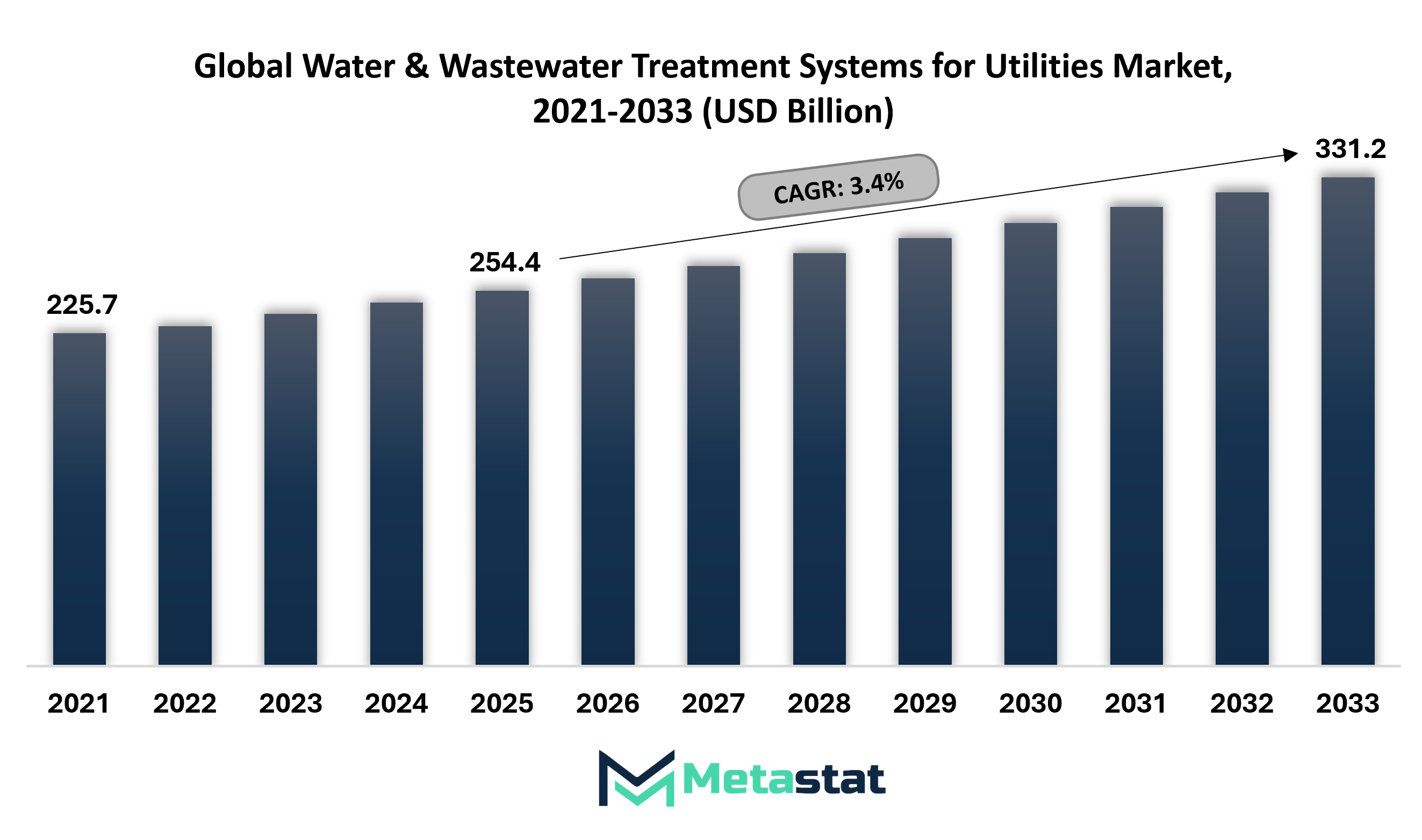

The Global Water & Wastewater Treatment Systems for Utilities market size was valued at USD 254.4 billion in 2025. The market is projected to grow from USD 262.7 billion in 2026 to USD 331.2 billion by 2033, exhibiting a CAGR of 3.4% during the forecast period.

Global Water & Wastewater Treatment Systems for Utilities market valued at USD 254.4 billion in 2025, growing at a CAGR of 3.4% through 2033, with potential to exceed USD 331.2 billion.

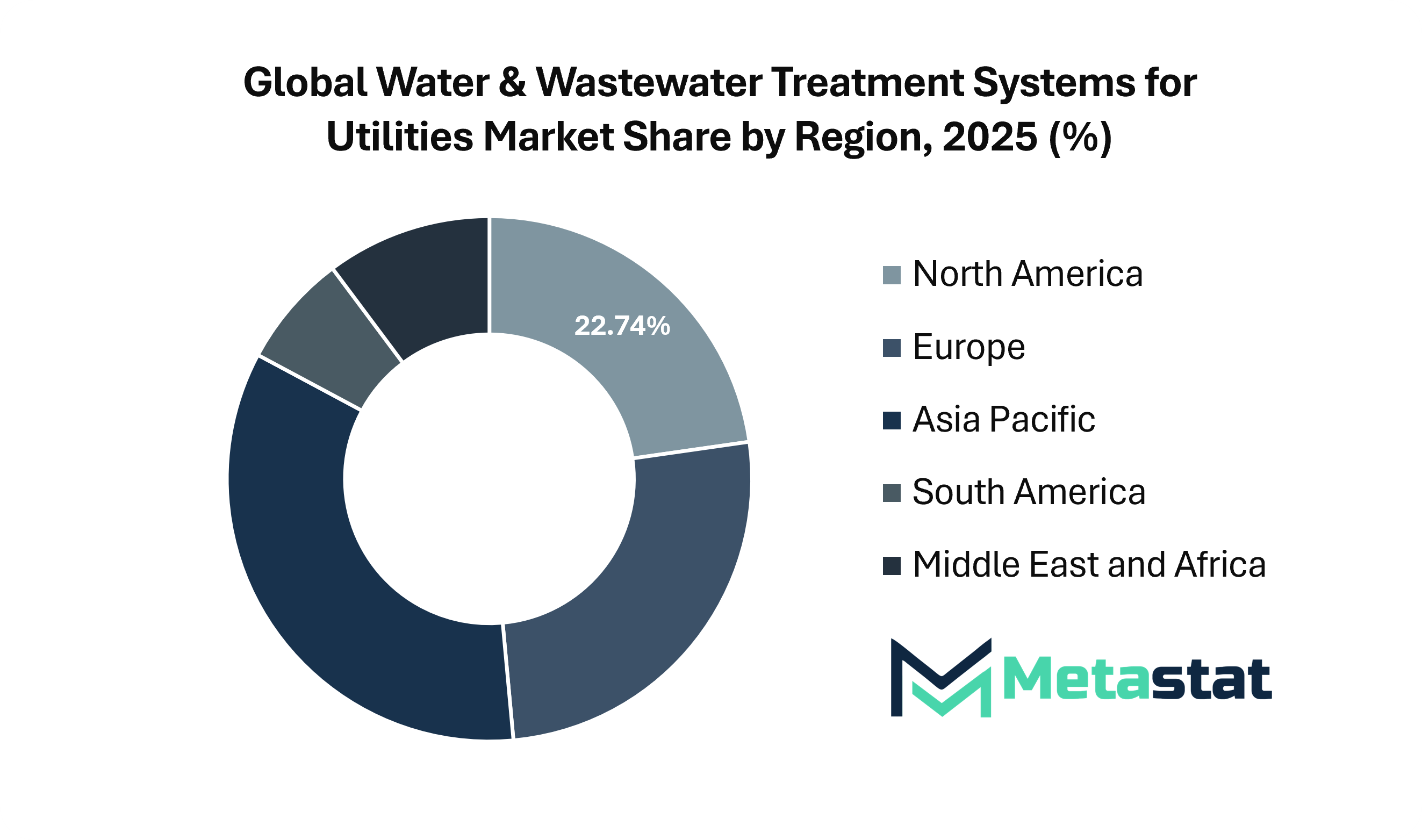

North America holds 22.7% in 2025 with US leading the market share in 2026.

Oil/Water Separation segment accounted for a market share of 7.9% in 2025.

Key trends driving growth: Increasing urbanization and population growth raising demand for reliable water supply and sanitation. Stringent environmental regulations mandating advanced wastewater treatment and reuse.

Opportunities include growing focus on water reuse, desalination, and smart treatment technologies by utilities worldwide.

Key insight: Regulatory pressure and urban water stress will sustain long-term demand for utility-scale water and wastewater treatment systems, while digitalization and reuse strategies will define competitive advantage.

Global water and wastewater treatment systems for the utility market will expand far beyond traditional purification, disposal and compliance-driven operations within the utility industry. Utility operators will repurpose treatment infrastructure into a data-enabled public service platform designed to support urban resilience, climate adaptation and circular water use. The facilities will not only operate to process inflows and outflows but will also act as intelligence centres generating operational insights, predictive alerts and resource recovery metrics for municipalities.

Digital water twins will be embedded in the treatment network, enabling utilities to simulate hydraulic behaviour, energy demand and chemical dosage outcomes prior to field execution. Such systems would reduce test-based operations and encourage policy-backed performance contracts linked to efficiency standards. Treatment plants will increasingly interact with energy grids, stormwater networks and industrial reuse corridors, creating interconnected municipal utility ecosystems rather than separate assets.

Market Dynamics

Growth Drivers:

Increasing urbanization and population growth raising demand for reliable water supply and sanitation.

Increasing urban expansion and population growth will increase pressure on municipal water networks. Utilities will prioritize scalable remedy capability, uninterrupted supply, and expanded sanitation coverage. The forward-searching plan will guide flexible systems designed to satisfy lengthy-time period intake patterns at the same time as shielding public health standards.

Stringent environmental regulations mandating advanced wastewater treatment and reuse.

Stricter environmental regulations will force utilities to undertake superior remediation tactics and reuse practices. Regulatory enforcement will boost investments in nutrient elimination, pollutant control, and satisfactory discharge upgrades. Future compliance will inspire generation upgrades consistent with sustainability goals and ecosystem conservation.

Restraints and Challenges:

High capital investment and long project payback periods limiting new system adoption.

High upfront expenses will lead to the avoidance of the fast deployment of cutting-edge treatment systems. Extended payback periods will venture into price range planning for utilities and public government. Financial challenges will slow down the decision-making process, specifically for projects requiring advanced automation and excessive-spec infrastructure.

Aging infrastructure and operational inefficiencies increasing maintenance costs.

Aging pipelines, remedial devices, and pumping property will lead to frequent breakdowns and elevated maintenance fees. Operational inefficiencies will place stress on the application price range and service reliability. Future device overall performance will depend upon phased modernization techniques addressing asset health, strength efficiency, and manner optimization.

Opportunities:

Growing focus on water reuse, desalination, and smart treatment technologies by utilities worldwide.

A global shift towards reuse, desalination, and digital treatment structures will open new avenues for the worldwide water and wastewater treatment structures for the utilities market. Utilities will undertake clever monitoring, predictive maintenance, and optimize water resources to strengthen resilience against weather stress and supply volatility.

Market Segmentation Analysis

The Global Water & Wastewater Treatment Systems for Utilities market is classified based on Treatment Type, Process and Technology, and End-User.

By Treatment Type the market is further segmented into:

Oil/Water Separation

Oil/Water Separation segment was valued at USD 20.8 Billion in 2026 and is projected to reach USD 25.3 Billion by 2033, at a CAGR of 2.8% during the forecast period.

Oil and water separation systems will be advantaged due to stricter discharge standards and increasing contamination risks. Utilities will prioritize advanced separation methods to guard downstream infrastructure and surface water bodies. Future deployments will emphasize computerized monitoring, low maintenance requirements, and stable performance under fluctuating load conditions.

Suspended Solids Removal

Suspended Solids Removal segment was valued at USD 57.5 Billion in 2026 and is projected to reach USD 71.3 Billion by 2033, at a CAGR of 3.1% during the forecast period.

Removal of suspended solids will stay principal remedy for performance as particulate matter at once affects downstream strategies. Utilities will spend money on advanced rationalization and filtration gadgets to make sure constant water quality. Future systems will focus on better throughput potential, much less chemical dependency, and stepped forward solids control efficiency.

Dissolved Solids Removal

Dissolved Solids Removal segment was valued at USD 47.2 Billion in 2026 and is projected to reach USD 60 Billion by 2033, at a CAGR of 3.5% during the forecast period.

Soluble solids removal technologies will expand in response to salinity management challenges and reuse requirements. Utilities will emphasize solutions capable of addressing complex inorganic loads. Its future adoption will help in long-term water reuse strategies, better mineral balance control, and protection of distribution networks from large-scale damage.

Biological Treatment/Nutrient and Metals Recovery

Biological Treatment/Nutrient and Metals Recovery segment was valued at USD 74.5 Billion in 2026 and is projected to reach USD 96.8 Billion by 2033, at a CAGR of 3.8% during the forecast period.

Biological treatment paired with recovery of nutrients and metals will support circular resource goals. Utilities will adopt systems that convert waste streams into reusable outputs while meeting discharge criteria. Future installations will focus on stable microbial performance, energy optimization, and recovery of valuable by-products for secondary applications.

Disinfection/Oxidation

Disinfection/Oxidation segment was valued at USD 49.9 Billion in 2026 and is projected to reach USD 62.5 Billion by 2033, at a CAGR of 3.3% during the forecast period.

Disinfection and oxidation processes will evolve to detect emerging pathogens and contaminants. Utilities will move to advanced systems providing consistent microbial control without excessive by-product formation. Future approaches will emphasize reliability, low chemical exposure, and compatibility with automated treatment frameworks.

Other Types

Other Types segment was valued at USD 12.9 Billion in 2026 and is projected to reach USD 15.3 Billion by 2033, at a CAGR of 2.5% during the forecast period.

Other types will support specific and area-specific needs where traditional systems show limitations. Utilities will implement hybrid solutions addressing unique water structures. Future integration will allow flexible upgrades, modular expansion, and adaptive operation under different source water conditions.

By Process and Technology the market is divided into:

Conventional Filtration

Conventional Filtration segment is projected to reach USD 86.9 Billion by 2033, at a CAGR of 2.6% during the forecast period.

Conventional filtration will retain relevance due to operational familiarity and cost efficiency. Utilities will modernize existing assets using better media and automation layers. Future filtration setups will focus on improved durability, less downtime, and integration with advanced pretreatment systems.

Membrane Systems (UF, NF, RO, MBR)

Membrane Systems (UF, NF, RO, MBR) segment is projected to reach USD 71.5 Billion by 2033, at a CAGR of 4.2% during the forecast period.

Membrane systems will see increased use due to the demand for high-quality output. The use of membrane systems by utilities will increase for desalination, reuse, and advanced purification. Future membranes will have enhanced resistance to pollution, reduced energy requirements, and longer lifetimes when operated continuously.

Biological Processes (Activated Sludge, MBBR, IFAS, Anaerobic) segment is projected to reach USD 104.5 Billion by 2033, at a CAGR of 3.2% during the forecast period.

Biological processes will drive secondary treatment because of their adaptability and effectiveness. Utilities will optimize process control to achieve maximum biological removal efficiency. Future designs will focus on a smaller size, energy recovery, and stability despite fluctuating conditions that influence the process.

Advanced Oxidation Processes and Ozonation

Advanced Oxidation Processes and Ozonation segment is projected to reach USD 27.5 Billion by 2033, at a CAGR of 3.8% during the forecast period.

Advanced oxidation processes and ozonation will help in the removal of persistent contaminants. Utilities will adopt these processes to ensure quality. Future technologies will be designed to ensure accurate dose control, simplicity of operation, and integration with digital monitoring systems.

Nutrient Removal (Nitrification-Denitrification, Biological Phosphorus Removal) segment is projected to reach USD 40.8 Billion by 2033, at a CAGR of 3.7% during the forecast period.

Nutrient removal will become a more strategic process due to the mandates for protecting ecosystems. Utilities will use advanced biological processes to manage nitrogen and phosphorus in their discharges. Future designs will emphasize efficiency, low chemical use, and meeting long-term environmental objectives.

By End-User the market is further divided into:

Municipal

Municipal segment is projected to reach USD 241.5 Billion by 2033 with a share of 74.8% in 2025.

Municipal end users will increase demand through urban population expansion and infrastructure renewal needs. Utilities serving municipalities will invest in potable supplies and flexible treatment systems that support reuse initiatives. Future municipal projects will emphasize scalability, regulatory alignment, and public health protection.

Industrial

Industrial segment is projected to reach USD 89.8 Billion by 2033 with a share of 25.2% in 2025.

Industrial end users will adopt advanced treatment systems to meet sector-specific discharge standards. Utilities supporting industrial sectors will focus on customized solutions addressing complex waste profiles. Future demand will be driven by water re-use, cost optimization and compliance-driven operational sustainability.

Regional Analysis

Based on geography, the Global Water & Wastewater Treatment Systems for Utilities market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Water & Wastewater Treatment Systems for Utilities Market is set to expand at a CAGR of 3.4% within the forecast period, reaching a market size (TAM) of USD 71.6 billion by the end of 2033.

In North America, aging municipal water infrastructure will drive utilities to invest in advanced treatment systems to reduce leaks, contamination risks, and service disruptions.

Across North America, tighter regulatory oversight of waste quality will accelerate the adoption of high-efficiency filtration, disinfection and monitoring technologies by utility operators.

In the Asia Pacific region, rapid urban expansion will create strong opportunities for integrated water treatment systems supporting new smart cities and municipal development.

Across the Asia Pacific region, government-backed investment in sustainable water management will open long-term opportunities for modern wastewater recycling and reuse solutions.

From an analyst perspective, the Middle East, Africa and South America will present uneven but strategic demand patterns, where water scarcity, infrastructure constraints and public sector funding limitations will encourage selective deployment of cost-efficient, scalable treatment systems aligned with regional utility priorities.

Competitive Landscape and Strategic Insights

The importance of global water and wastewater treatment systems to the utilities market continues to grow due to increasing pressure on public water infrastructure and increasing demand for a safe, reliable supply. Urban growth, business growth, and population increase will put heavy stress on current remedy centres. Utilities will focus on improving efficiency, reducing water loss, and meeting stricter discharge requirements. Advanced filtration, membrane structures, and energy-efficient tactics will support long-term sustainability while helping utilities manage operational costs. Governments and municipal bodies will increasingly rely upon technology partners to modernize treatment plants and enhance provider reliability.

Technology vendors inside the market will play a crucial position in supporting utilities through innovation and gadget integration. Companies that include Veolia Water Technologies, SUEZ SA, and Xylem Inc. will continue delivering big-scale treatment solutions overlaying drinking water, wastewater reuse, and sludge management. VA TECH WABAG Ltd., Aquatech International, and Ovivo Water Inc. Will make stronger their presence via custom-designed projects tailor-made to nearby water challenges. Fluence Corporation Limited, IDE Technologies, Acciona, S.A., and GS Inima Environment will support desalination, reuse, and advanced treatment projects, especially in water-harassed regions.

Tool and component manufacturers will remain essential to system performance and lifecycle management. Pentair plc, Toray Industries Inc., LG Water Solutions under LG Chem Ltd., and Asahi Kasei Corporation will drive advancements in membrane, filtration media, and separation technologies. Kovalus Separation Solutions, Huber SE, Andritz AG, and Industri di Nora S.p.A. Will contribute expertise in screening, sludge processing, electrochemical treatment, and resource recovery. These players will help utilities improve the quality of treatment while reducing energy and chemical consumption.

Pumping, aeration, and process control specialists will also shape the market growth. Grundfos Holding A/S, Sulzer Ltd., KSB Ltd., and Wilo SE will support efficient water movement and pressure management in the treatment network. Aqua-Aerobic Systems, Inc., Smith & Loveless, WasteTech Engineering, LLC, Parkson Corporation, and Nijhuis Solar Industries will provide integrated treatment systems and modular solutions suitable for both large utilities and medium-sized municipalities.

Forecast and Future Outlook

The market is forecast to rise from USD 254.4 billion in 2025 to USD 331.2 billion by 2033.

The global water and wastewater treatment system for the utilities market will move forward with a public health monitoring framework. Treatment systems will monitor biochemical markers within influent streams to aid in early detection of disease trends, environmental pollution, or industrial discharge violations. Utilities will collaborate with civic authorities, research institutes and urban planners to transform treatment data into actionable governance tools. In the long term, utilities will install water treatment infrastructure as a civic investment layer supporting smart cities, climate-resilient housing and sustainable industrial sectors. Such repositioning will redefine utility value creation, shifting emphasis from volume processing to intelligence-driven management, operational transparency, and long-horizon infrastructure accountability.

Water & Wastewater Treatment Systems for Utilities Market Key Segments:

Key Global Water & Wastewater Treatment Systems for Utilities Industry Players

Veolia Water Technologies

SUEZ SA

Xylem Inc.

VA TECH WABAG Ltd.

Aquatech International

Ovivo Water Inc.

Fluence Corporation Limited

IDE Technologies

Acciona, S.A.

GS Inima Environment

Pentair Plc

Toray Industries Inc.

LG Water Solutions (LG Chem, Ltd.)

Asahi Kasei Corporation

Kovalus Separation Solutions

HUBER SE

ANDRITZ AG

Industrie De Nora S.p.A

Grundfos Holding A/S

Sulzer Ltd

KSB Limited

WILO SE

Aqua-Aerobic Systems, Inc.

Smith & Loveless

WesTech Engineering, LLC

Parkson Corporation

Nijhuis Saur Industries

Report Coverage

This research report categorizes the Water & Wastewater Treatment Systems for Utilities market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Water & Wastewater Treatment Systems for Utilities market. Recent market developments and competitive strategies such as expansion, product launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Water & Wastewater Treatment Systems for Utilities market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 3.4% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Treatment Type, Process and Technology, End-User and Region

By Region

North America (By Treatment Type, Process and Technology, End-User and Country)

United States

Canada

Mexico

Europe (By Treatment Type, Process and Technology, End-User and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of the Europe

Asia Pacific (By Treatment Type, Process and Technology, End-User and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Treatment Type, Process and Technology, End-User and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Treatment Type, Process and Technology, End-User and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Full In-Depth Analysis of the Parent Industry

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Former, On-Going, and Projected Market Analysis

Assessment Of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Major Market Players

Vapor Degreasing Solvent market size is valued at USD 1,004.1 million in 2025 and projected to reach USD 1,576.4 million by 2033, growing at a CAGR of 5.8%.

Bangladesh Flavours and Fragrances Market Size, Share, Trends, 2033

Bangladesh Flavours and Fragrances market size is valued at USD 793.9 million in 2025 and is projected to reach USD 1,447.9 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Bangladesh Flavours and Fragrances Market, Bangladesh Flavours and Fragrances Market Size, Bangladesh Flavours and Fragrances Market Share, Bangladesh Flavours and Fragrances Market Analysis, Bangladesh Flavours and Fragrances Market Growth, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market Research Report, Bangladesh Flavours and Fragrances Market Forecast, Bangladesh Flavours and Fragrances, Bangladesh Flavours and Fragrances Market Research, Bangladesh Flavours and Fragrances Industry, Bangladesh Flavours and Fragrances Industry Report, Bangladesh Flavours and Fragrances Market Data, Bangladesh Flavours and Fragrances Statistics, Bangladesh Flavours and Fragrances Market Statistics, Bangladesh Flavours and Fragrances Industry Trends, Bangladesh Flavours and Fragrances Market Report, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market News, Bangladesh Flavours and Fragrances Forecasts, Bangladesh Flavours and Fragrances Market Intelligence Report

Biocatalysis and Enzyme Biocatalysts Market Size, Share, Trends, 2033

Biocatalysis and Enzyme Biocatalysts market size is valued at USD 737.8 million in 2025 and is projected to reach USD 1,221.0 million in 2033, at a CAGR of 6.5% from 2026 to 2033.

Biocatalysis and Enzyme Biocatalysts Market, Biocatalysis and Enzyme Biocatalysts Market Size, Biocatalysis and Enzyme Biocatalysts Market Share, Biocatalysis and Enzyme Biocatalysts Market Analysis, Biocatalysis and Enzyme Biocatalysts Market Growth, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market Research Report, Biocatalysis and Enzyme Biocatalysts Market Forecast, Biocatalysis and Enzyme Biocatalysts, Biocatalysis and Enzyme Biocatalysts Market Research, Biocatalysis and Enzyme Biocatalysts Industry, Biocatalysis and Enzyme Biocatalysts Industry Report, Biocatalysis and Enzyme Biocatalysts Market Data, Biocatalysis and Enzyme Biocatalysts Statistics, Biocatalysis and Enzyme Biocatalysts Market Statistics, Biocatalysis and Enzyme Biocatalysts Industry Trends, Biocatalysis and Enzyme Biocatalysts Market Report, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market News, Biocatalysis and Enzyme Biocatalysts Forecasts, Biocatalysis and Enzyme Biocatalysts Market Intelligence Report

Malaysia Tyre Pyrolysis Products Market Size, Share, Trends, 2033

Malaysia Tyre Pyrolysis Products market size is valued at USD 205.9 million in 2025 and is projected to reach USD 421.8 million in 2033, at a CAGR of 9.3% from 2026 to 2033.

Malaysia Tyre Pyrolysis Products Market, Malaysia Tyre Pyrolysis Products Market Size, Malaysia Tyre Pyrolysis Products Market Share, Malaysia Tyre Pyrolysis Products Market Analysis, Malaysia Tyre Pyrolysis Products Market Growth, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market Research Report, Malaysia Tyre Pyrolysis Products Market Forecast, Malaysia Tyre Pyrolysis Products, Malaysia Tyre Pyrolysis Products Market Research, Malaysia Tyre Pyrolysis Products Industry, Malaysia Tyre Pyrolysis Products Industry Report, Malaysia Tyre Pyrolysis Products Market Data, Malaysia Tyre Pyrolysis Products Statistics, Malaysia Tyre Pyrolysis Products Market Statistics, Malaysia Tyre Pyrolysis Products Industry Trends, Malaysia Tyre Pyrolysis Products Market Report, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market News, Malaysia Tyre Pyrolysis Products Forecasts, Malaysia Tyre Pyrolysis Products Market Intelligence Report