Wheat Beer Market Size, Share, By Product Type (Hefeweizen, Witbier, American Wheat Beer, and Others), By Packaging (Bottle, Can, and Draft), By Alcohol Content (Low Alcohol Wheat Beer, Medium Alcohol Wheat Beer, and High Alcohol Wheat Beer), By Distribution Channel (Online Retailers, Supermarkets, Hypermarkets, Specialty Stores, Bars, and Restaurants), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4610

Published

April 14, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

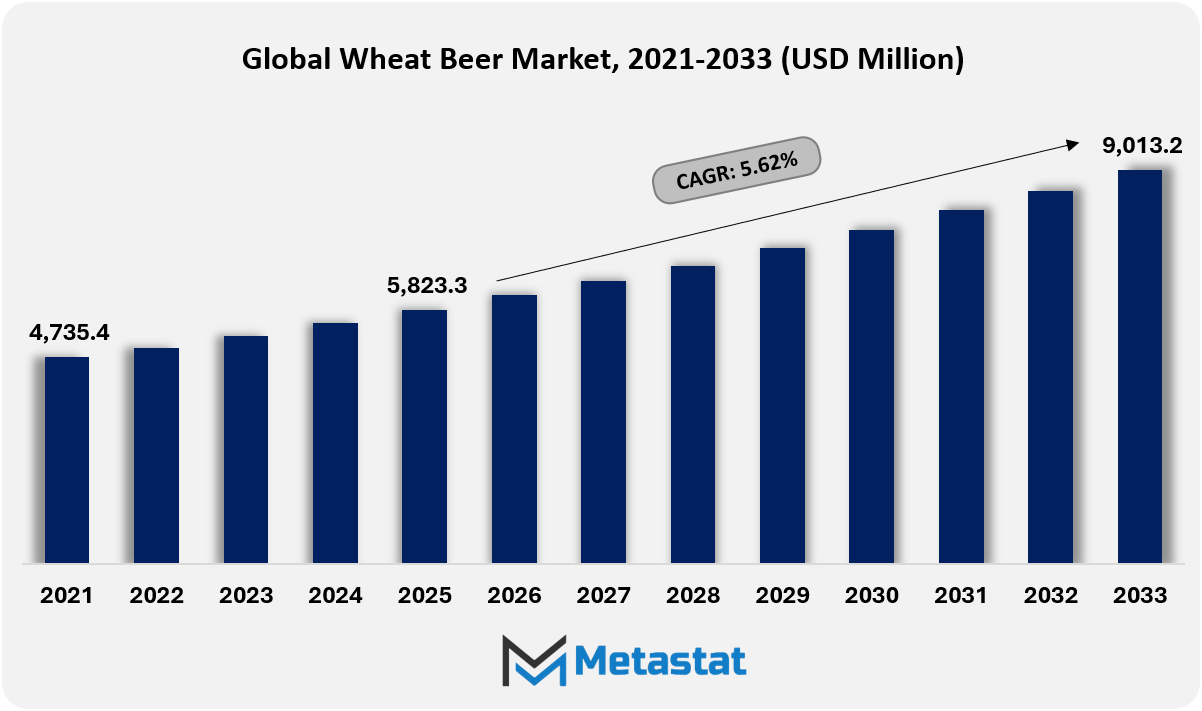

The Global Wheat Beer market was valued at USD 5,823.3 million in 2025 and is projected to reach USD 9,013.2 million by 2033, registering a CAGR of 5.6% during 2026-2033.

Global Wheat Beer Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

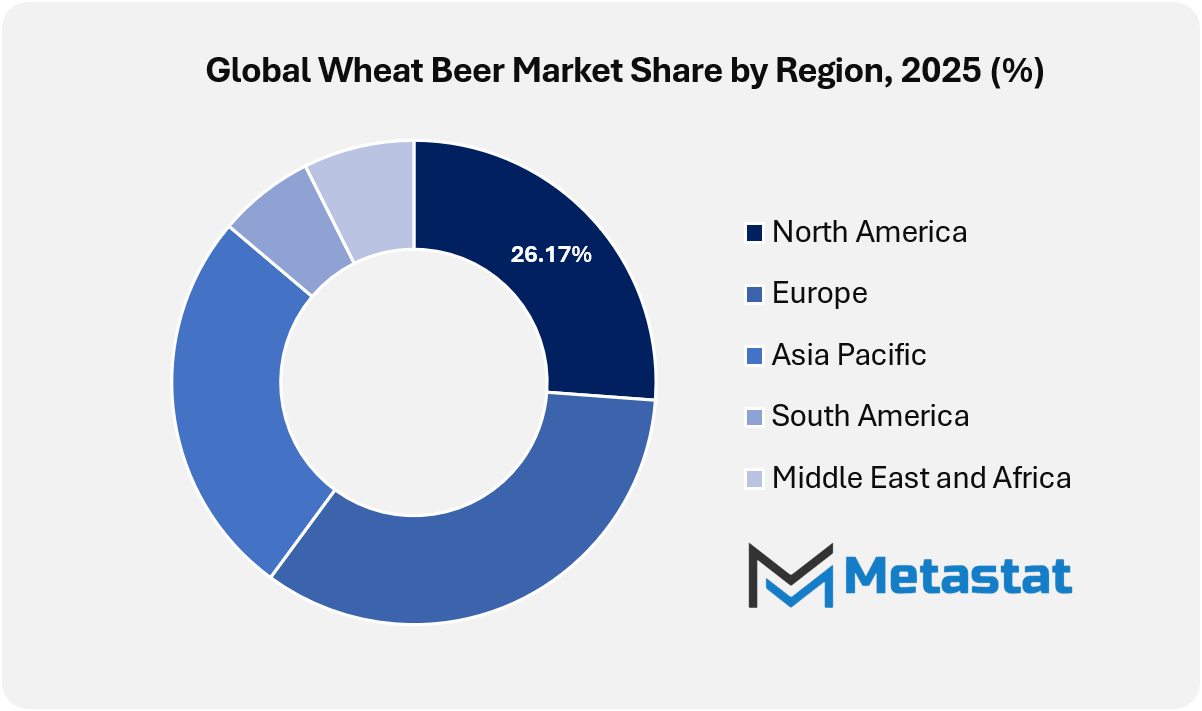

North America accounted for 26.2% of the global market in 2025, with the U.S. leading the regional market.

Hefeweizen segment accounts for a market share of 35.0% in 2025.

Key trends driving growth: Rising preference for mild, fruity, and low-bitterness craft beer variants among urban consumers, Increased adoption of premium and specialty beers across pubs, microbreweries, and taprooms

Opportunities include growing demand for flavoured wheat beers and low-alcohol craft formats across emerging Asia-Pacific markets.

Key insight: The global wheat beer market reflects steady momentum driven by craft beer adoption and premium consumption patterns, supported by innovation-led differentiation despite regulatory and pricing pressures.

The Global Wheat Beer market is moving beyond traditional production narratives, supported by experimentation, premiumization, and regional flavor innovation. Over the coming years, manufacturers are expected to shift from volume-driven portfolios toward smaller batches, heritage-inspired recipes, and differentiated sensory profiles that appeal to informed consumers. Wheat beer styles will increasingly serve as platforms for innovation, enabling brewers to explore yeast behavior, fermentation control, and grain sourcing with greater flexibility.

The industry is repositioning wheat beer across lifestyle-led consumption occasions. Future demand will be shaped by social settings, gastronomy pairings, and seasonal relevance, with wheat beer positioned as a lighter yet expressive alternative to stronger styles. Breweries are expected to invest in local identity, historical brewing traditions, and regional flavor profiles, helping wheat beer resonate across diverse cultural markets without relying on uniform branding.

Market Dynamics

Growth Drivers:

Rising preference for mild, fruity, and low-bitterness craft beer variants among urban consumers.

Urban consumption patterns indicate steady interest in balanced flavor profiles that offer refreshment without pronounced bitterness. The Global Wheat Beer marketplace will gain from consumer awareness on session-pleasant liquids acceptable for social settings. Future product development will emphasize aroma, mouthfeel, and natural ingredients aligned with premium lifestyle preferences.

Increased adoption of premium and specialty beers across pubs, microbreweries, and taprooms

Hospitality venues aim to amplify curated beer menus, highlighting differentiated offerings. The Global Wheat Beer marketplace will gain traction through experiential consuming formats promoted through brewpubs and unbiased taprooms. Forward-looking investments will support small-batch innovation, regional recipes, and quality-driven positioning within premium on-trade channels.

Restraints and Challenges:

Higher production complexity and cost compared to conventional barley-based beers

Wheat-based brewing entails subtle processing steps, strict quality controls, and temperature-sensitive fermentation. Production economics can pressure margins across price-sensitive markets. The Global Wheat Beer marketplace will face operational challenges linked to ingredient sourcing and scalability, influencing pricing techniques and restricting competitive volume expansion in the near time.

Strict alcohol regulations and taxation policies limiting expansion in several markets

Regulatory frameworks across multiple geographies impose licensing controls, advertising limits, and elevated excise duties. Such regulations can slow distribution growth and hinder market entry efforts. The Global Wheat Beer market will require compliance-centered planning, localized partnerships, and adaptive go-to-market strategies to sustain long-term participation.

Opportunities:

Growing demand for flavoured wheat beers and low-alcohol craft formats across emerging Asia-Pacific markets

Rising demand for flavored wheat beers and low-alcohol craft formats across emerging Asia-Pacific markets. Changing customer attitudes throughout the Asia-Pacific region desire revolutionary flavors and mild alcohol intake. Brewers will explore fruit-infused profiles and lighter formulations aligned with wellness developments. Future growth will depend on localized flavor development, broader modern retail penetration, and brand storytelling that supports premium yet accessible wheat beer offerings.

Market Segmentation Analysis

The Global Wheat Beer market is classified based on Product Type, Packaging, Alcohol Content, and Distribution Channel.

By Product Type, the market is further segmented into:

Hefeweizen

Hefeweizen segment is estimated at USD 2,149.6 million in 2026 and is projected to reach USD 2,852.7 million by 2033, at a CAGR of 4.1% during the forecast period.

Hefeweizen will continue gaining recognition via robust sensory enchantment pushed by way of clouded look, banana notes, and clove-like aroma. Brewing innovation centered on yeast choice and fermentation precision will make for stronger product consistency. Premium positioning across urban centers will encourage consistent adoption inside the Global Wheat Beer market over the coming years.

Witbier

Witbier segment is estimated at USD 1,662.3 million in 2026 and is projected to reach USD 2,323.6 million by 2033, at a CAGR of 4.9% during the forecast period.

Witbier will benefit from the growing of lighter profiles supported through citrus peels and coriander blends. Craft-oriented branding and seasonal launches will beautify visibility. Health-conscious consumption patterns will in addition assist witbier expansion, developing favorable momentum throughout numerous purchaser companies inside the Global Wheat Beer marketplace.

American Wheat Beer

American Wheat Beer segment is estimated at USD 1,480.1 million in 2026 and is projected to reach USD 2,607.5 million by 2033, at a CAGR of 8.4% during the forecast period.

American wheat beer will witness an enlargement through experimental brewing techniques and hop-forward flavor modifications. Independent breweries will drive product differentiation via neighborhood sourcing and confined releases. Modern palates favoring balanced bitterness and clean finishes will improve class relevance within evolving consumption environments.

Other Wheat Beers

Other Wheat Beers segment is estimated at USD 852.4 million in 2026 and is projected to reach USD 1,229.4 million by 2033, at a CAGR of 5.4% during the forecast period.

Other wheat beers will enjoy a slight increase via nearby recipes and heritage-based brewing traditions. Breweries will revive lesser-acknowledged patterns to address interest-driven demand. Such services will upload portfolio depth and encourage exploration-led purchases across mature and rising beer-ingesting areas.

By Packaging, the market is divided into:

Bottle

Bottle segment is projected to reach USD 3,943.3 million by 2033, at a CAGR of 2.9% during the forecast period.

Bottle packaging will maintain sturdy relevance via top-class belief and prolonged shelf life. Glass packaging will aid flavor renovation whilst aligning with sustainability-targeted recycling tasks. Brand storytelling through label design will further support bottled wheat beer positioning across retail-driven purchasing channels.

Can

Can segment is projected to reach USD 3,639.5 million by 2033, at a CAGR of 11.2% during the forecast period.

Can packaging will expand rapidly owing to portability, faster chilling, and improved light protection. The advanced can-lining era will maintain taste integrity. Convenience-pushed consumption and outside social occasions will boost adoption across city markets and more youthful demographic segments.

Draft

Draft segment is projected to reach USD 1,430.4 million by 2033, at a CAGR of 2.8% during the forecast period.

Draft formats will gain momentum through hospitality-led intake and experiential consuming subculture. Breweries will put money into tap infrastructure to beautify the freshness perception. Draft wheat beer offerings will support on-premises differentiation and inspire brand loyalty through sensory-led engagement.

By Alcohol Content, the market is further divided into:

Low Alcohol Wheat Beer

Low Alcohol Wheat Beer segment is projected to reach USD 2,201 million by 2033.

Low alcohol wheat beer will gain traction owing to wellness-oriented preferences and moderation trends. Brewers will refine fermentation manipulation to preserve taste intensity. Workplace socializing and daylight hours intake activities will guide category expansion throughout innovative intake environments.

Medium Alcohol Wheat Beer

Medium Alcohol Wheat Beer segment is projected to reach USD 6,160.5 million by 2033.

Medium alcohol wheat beer will continue to be the dominant preference because of balanced energy and taste harmony. Product consistency and mainstream availability will enhance leadership across a couple of distribution networks.

High Alcohol Wheat Beer

High Alcohol Wheat Beer segment is projected to reach USD 651.7 million by 2033.

High alcohol wheat beer will appeal to niche consumer interest driven by bold flavor exploration and premium positioning. Aging techniques and forte batches will decorate the appeal. Limited availability will guide exclusivity-led buying behavior among skilled beer customers.

By Distribution Channel, the Global Wheat Beer market is divided as:

Online Retailers

Online Retailers segment is projected to grow at a CAGR of 13.7% during the forecast period.

Online retailers will gain traction through home delivery, wider product access, and digital promotions. Subscription models and centered tips will improve patron retention. Regulatory clarity throughout areas will enhance online participation in the Global Wheat Beer market.

Supermarkets/Hypermarkets

Supermarkets/Hypermarkets segment is projected to grow at a CAGR of 5% during the forecast period.

Supermarkets and hypermarkets will preserve serving volume-pushed sales via visibility and fee competitiveness. Dedicated beer aisles and promotional bundling will encourage impulse buying. Strong delivery chain integration will ensure constant product availability.

Specialty Stores

Specialty Stores segment is projected to grow at a CAGR of 6.4% during the forecast period.

Specialty stores will support top class wheat beer growth through curated picks and expert guidance. Consumer training tasks will enhance trial prices. Such stores will strengthen brand credibility and deepen appreciation for differentiated wheat beer styles.

Bars and Restaurants

Bars and Restaurants segment is projected to grow at a CAGR of 4.1% during the forecast period.

Bars and restaurants will drive experiential consumption via pairing menus and seasonal taps. Social dining traits will aid wheat beer visibility. On-premise engagement will have an impact on emblem belief and inspire repeat purchases throughout urban hospitality hubs.

By Region:

Based on geography, the Global Wheat Beer market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Wheat Beer Market is set to expand at a CAGR of 5.6% within the forecast period, reaching a market size (TAM) of USD 2,002.5 million by the end of 2033.

In North America, rising preference for craft and specialty beers is driving stronger demand for wheat beer across urban and premium consumption segments.

In North America, growing preference for natural ingredients and lighter beer profiles is supporting wider acceptance of wheat beer among health-conscious consumers.

In Asia-Pacific, the growing young adult population and greater exposure to international beer cultures are creating new opportunities for the wheat beer market.

In Asia-Pacific, the rapid expansion of microbreweries and premium on-trade channels is creating new opportunities for regionally brewed wheat beer variants.

Across South America and selected markets in the Middle East & Africa, gradual shifts toward premium alcoholic beverages, urban lifestyle changes, and improving distribution networks are supporting steady traction for wheat beer among niche consumer groups.

Competitive Landscape and Strategic Insights

The global wheat beer marketplace maintains a strong location inside the broader beer industry, supported by means of lengthy-standing brewing traditions and a growing interest in flavorful yet refreshing beer styles. Wheat beer is frequently associated with smoother textures, subtle fruit notes, and clean drinkability, which appeals to both seasoned beer consumers and new audiences. Demand will continue to be constant in regions in which wheat beer has cultural roots, while newer markets display rising curiosity pushed by way of changing taste preferences and exposure to international beer patterns.

European breweries play a defining role in shaping the marketplace, mainly the ones primarily based in Germany, where wheat beer has deep historic ties. Producers consisting of Bayerische Staatsbrauerei Weihenstephan, Paulaner Brauerei Gruppe, Privatbrauerei Erdinger Weissbräu, Weissbierbrauerei G. Schneider & Sohn, Brauerei Gebr. Maisel, Klosterbrauerei Andechs, Hofbräu München, Brauerei Gutmann, König Ludwig Schlossbrauerei, Spaten-Franziskaner-Bräu, Hacker-Pschorr Bräu, Schöfferhofer, Tucher Bräu, Oettinger Brauerei, Kapuziner Weissbier, Brauerei zum Kuchlbauer, Warsteiner Brauerei, Krombacher Brauerei, and Benediktiner Weissbräu strive to meet exceptional requirements and customer expectations. Their strong logo recognition and constant brewing methods will help keep loyalty while nevertheless allowing room for gradual innovation.

Beyond Germany, wheat beer production has received traction throughout Belgium, the Netherlands, and France, where breweries mix nearby brewing identities with wheat-based styles. Companies including AB InBev Belgium, Duvel Moortgat, Brasserie du Bocq, Brasserie Lefebvre, Brouwerij De Brabandere, Brasserie St-Feuillien, De Koningshoeven, Brouwerij ’t IJ, Royal Swinkels, Koninklijke Grolsch, Brasserie Kronenbourg, Brasserie Meteor, and Brasserie Licorne contribute to the market range by offering numerous interpretations of wheat beer. These producers will benefit from the export call and the growing appeal of local European beers in international markets.

The competitive surroundings inside the wheat beer marketplace are formed by means of a stability among history and adaptation. Established brewers rely upon legacy, trust, and regular taste, whilst additionally adjusting packaging, alcohol content, and product positioning to satisfy modern customer behavior. As worldwide beer clients show interest in lighter, smoother alternatives with awesome character, wheat beer will continue to stand out. Supported with the aid of a robust lineup of world players and constant worldwide demand, the marketplace is predicted to preserve its relevance and slow growth over the approaching years.

Forecast and Future Outlook

Market size is forecast to rise from USD 5,823.3 million in 2025 to over USD 9,013.2 million by 2033.

Regulatory clarity around labeling, alcohol content disclosure, and ingredient transparency will shape how the Global Wheat Beer market is positioned across mature and emerging economies. Compliance will increasingly serve as a brand-trust mechanism, particularly for export-oriented brewers. Over time, wheat beer is expected to evolve from a seasonal or secondary choice into a year-round category supported by innovation, cultural relevance, and increasingly sophisticated consumer expectations.

This research report categorizes the Wheat Beer market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Wheat Beer market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Wheat Beer market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 5.6% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Million Liters

Segmentation

By Product Type, Packaging, Alcohol Content, Distribution Channel, and Region

By Region

North America (By Product Type, Packaging, Alcohol Content, Distribution Channel, and Country)

United States

Canada

Mexico

Europe (By Product Type, Packaging, Alcohol Content, Distribution Channel, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Product Type, Packaging, Alcohol Content, Distribution Channel, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Product Type, Packaging, Alcohol Content, Distribution Channel, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Product Type, Packaging, Alcohol Content, Distribution Channel, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share and Revenue

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

Import Export Trade Statistics

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Top players operating in the Wheat Beer industry include Bayerische Staatsbrauerei Weihenstephan, Paulaner Brauerei Gruppe, Privatbrauerei Erdinger Weissbräu, Weissbierbrauerei G. Schneider & Sohn, Brauerei Gebr. Maisel, and Klosterbrauerei Andechs.

The Metastat Insights analysis shows that the North America Wheat Beer market size is estimated to be USD 2,002.5 million by 2033.

The Global Wheat Beer market is likely to grow at a CAGR of 5.6% over the forecast period (2026-2033).

Higher production complexity and cost compared to conventional barley-based beers will hamper market growth within the forecast period.

Global Wheat Beer market is estimated to reach USD 9,013.2 million by 2033.

Rising preference for mild, fruity, and low-bitterness craft beer variants among urban consumers and Increased adoption of premium and specialty beers across pubs, microbreweries, and taprooms are key driving factors, boosting the market.

Europe region dominates the market.

The Metastat Insights study shows that the Global Wheat Beer market size was USD 5,823.3 million in 2025.

The Hefeweizen is the leading type of segment in the Global market.

Reduced Sugar Food & Beverages market size is valued at USD 793.9 billion in 2025 and projected to reach USD 1,447.9 billion by 2033, growing at a CAGR of 7.8%.

Kazakhstan Frozen Potato Products market size is valued at USD 26.4 million in 2025 and is projected to reach USD 53.0 million in 2033, at a CAGR of 9.0% from 2026 to 2033.

Switzerland Poke Food market size is valued at USD 29.2 million in 2025 and is projected to reach USD 44.5 million in 2033, at a CAGR of 5.5% from 2026 to 2033.

Netherlands Food and Beverages QA, QC, and Compliance Software Solutions Market Size, Share, Trends, 2033

Netherlands F&B QA, QC, and Compliance Software Solutions market size is valued at USD 272.5 million in 2025 and is projected to reach USD 421.3 million in 2033, at a CAGR of 5.6% from 2026 to 2033.

Netherlands F&B QA, QC, and Compliance Software Solutions Market, Netherlands F&B QA, QC, and Compliance Software Solutions Market Size, Netherlands F&B QA, QC, and Compliance Software Solutions Market Share, Netherlands F&B QA, QC, and Compliance Software Solutions Market Analysis, Netherlands F&B QA, QC, and Compliance Software Solutions Market Growth, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Forecast, Netherlands F&B QA, QC, and Compliance Software Solutions, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research, Netherlands F&B QA, QC, and Compliance Software Solutions Industry, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Data, Netherlands F&B QA, QC, and Compliance Software Solutions Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Market Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market News, Netherlands F&B QA, QC, and Compliance Software Solutions Forecasts, Netherlands F&B QA, QC, and Compliance Software Solutions Market Intelligence Report