Global Flexible Packaging Barrier Paper Market Size, Share, By Paper Type (Kraft Paper, Greaseproof Paper, Parchment Paper, Glassine Paper, and Others), By Barrier Property (Moisture Barrier, Oxygen Barrier, Grease Barrier, Oil Barrier, Vapor Barrier, Aroma Barrier, and Flavour Barrier), By Coating Type (Polymer Coatings, Wax Coatings, Aluminium Foil Coatings, Water-Based Coatings, Bio-Based Coatings, and Biodegradable Coatings), By End-Use Industry (Food, Beverages, Personal Care, Cosmetics, Pharmaceuticals, Retail, Consumer Goods, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4696

Published

April 30, 2026

Pages

316 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

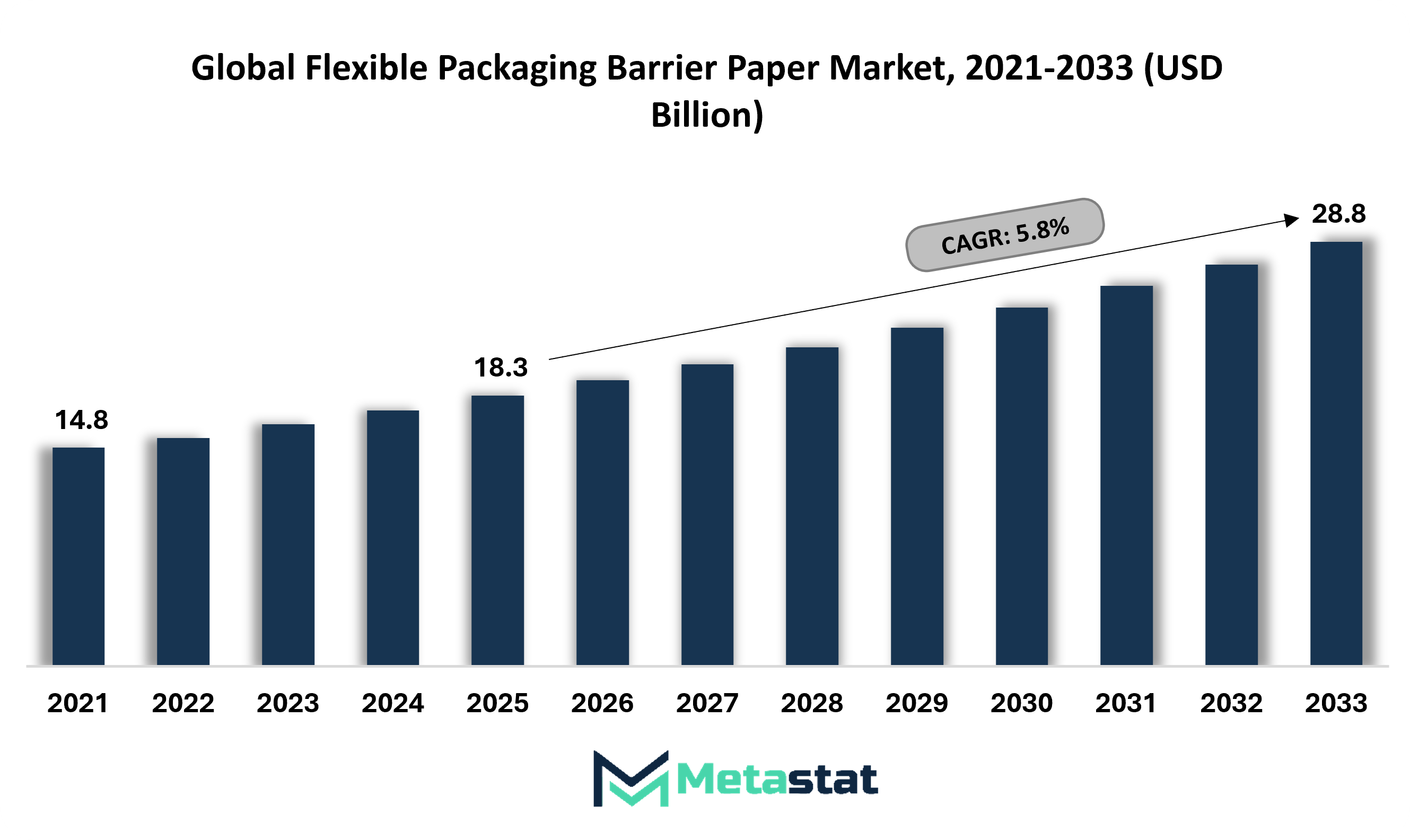

Global Flexible Packaging Barrier Paper market size is valued at USD 18.3 billion in 2025 and projected to grow at a CAGR of 5.8% during the forecast period, reaching USD 28.8 billion by 2033.

Global Flexible Packaging Barrier Paper Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

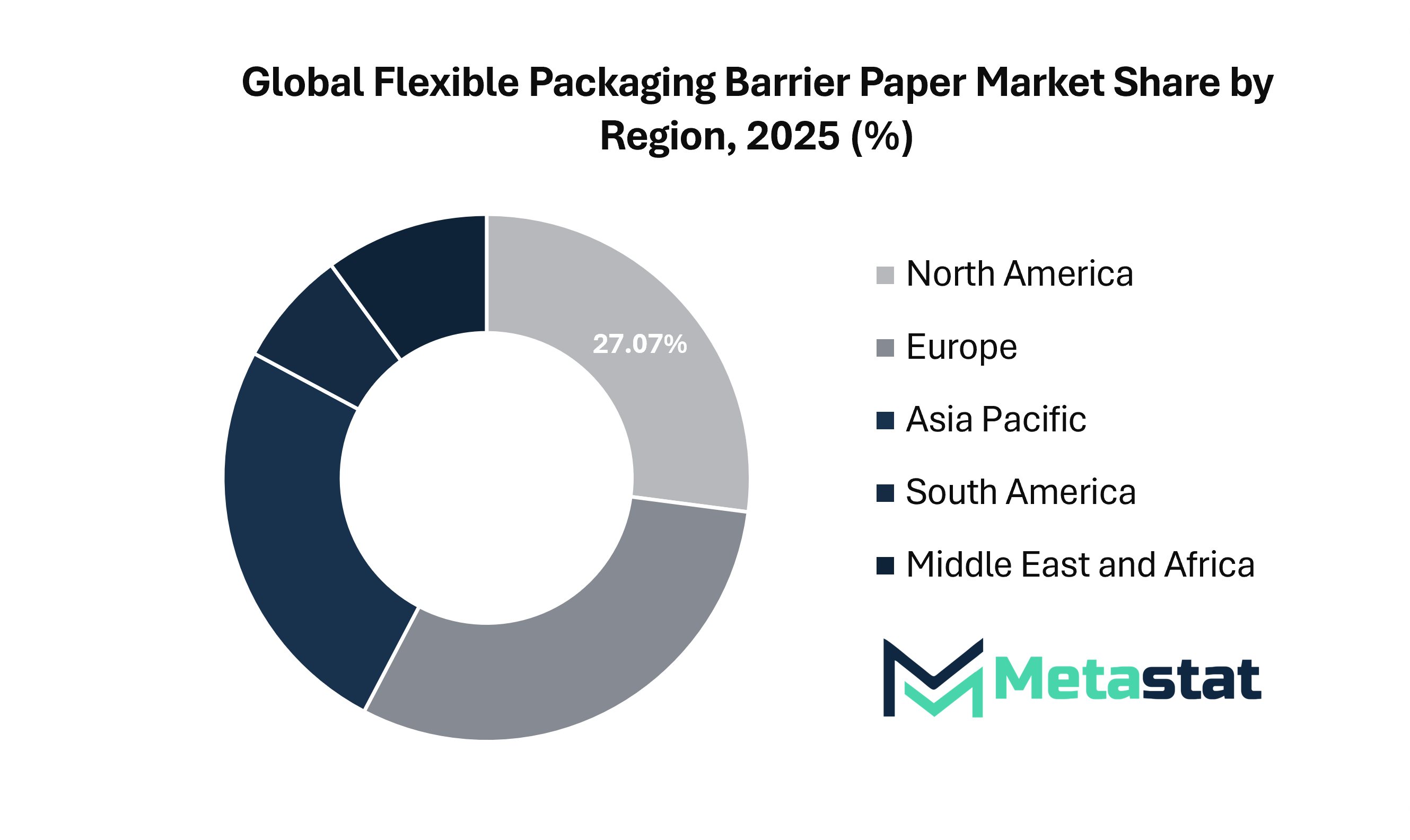

North America holds 27.1% in 2025 with US leading the market share in 2025.

Kraft Paper segment account for a market share of 38.3% in 2025.

Key trends driving growth: Rising demand for sustainable and plastic-free packaging solutions, along with increasing need for extended shelf life and product protection in food and consumer goods.

Opportunities include development of bio-based and recyclable barrier coatings enabling full paper-based packaging solutions.

Key insight: The Global Flexible Packaging Barrier Paper market is gaining momentum owing to sustainability mandates, packaging innovation, brand commitments, and growing consumer preference for paper-based solutions.

The Global Flexible Packaging Barrier Paper market is expanding as packaging manufacturers shift from conventional wrapping applications toward high-performance protective packaging formats. Producers are focusing on paper-based systems that combine printability, shelf appeal, sealability, and barrier functionality while supporting recyclability targets. Brand owners are increasingly replacing complex plastic laminates with fiber-based materials that align with circular economy goals and sustainable packaging commitments.

Over the coming years, product development will focus on lightweight paper structures, improved sealing performance, and stronger resistance to oil, oxygen, aroma transfer, and moisture. The Global Flexible Packaging Barrier Paper market will benefit from investments in advanced coating chemistry, converting technologies, recyclable barrier systems, and commercially compostable solutions that support wider adoption across food, healthcare, personal care, and retail packaging formats.

Market Dynamics

Growth Drivers:

Rising demand for sustainable and plastic-free packaging solutions.

Consumer preference for eco-conscious packaging continues to increase across retail, foodservice, healthcare, and personal care categories. Brand owners are shifting toward paper-based formats with lower plastic content, improved recyclability, and stronger end-of-life outcomes. Regulatory pressure on single-use plastics further supports investment, product launches, and capacity expansion across the barrier paper value chain.

Increasing need for extended shelf life and product protection in food and consumer goods

Food waste reduction remains a major industrial priority for manufacturers, retailers, and foodservice operators. Barrier paper helps restrict moisture, grease, oxygen, and aroma transfer, supporting freshness retention and product quality preservation. Adoption across snacks, bakery products, frozen foods, household products, and hygiene goods will strengthen future market penetration.

Restraints and Challenges:

Technical challenges in achieving consistent high-performance barrier properties

Performance variation during coating application, converting, storage, and transportation creates quality concerns for producers. Consistent resistance to moisture, oxygen, oil, and migration requires strong process control, coating uniformity, and material standardization. High-speed packaging lines also require reliable sealing behavior, increasing development pressure on suppliers worldwide.

Complex manufacturing processes and higher cost of advanced coatings

Specialized coating lines, testing systems, skilled labor, and premium raw materials increase production costs across the value chain. Smaller converters often face investment barriers during technology upgrades. Cost sensitivity in mass-market packaging will slow adoption where low-cost plastic formats maintain strong commercial presence.

Opportunities:

Development of bio-based and recyclable barrier coatings enabling full paper-based packaging solutions

Research activity in water-based, compostable, fiber-compatible, and renewable coating systems creates strong future potential. Fully paper-based packaging formats improve recycling streams and support circular economy goals. Collaboration among paper mills, coating chemical suppliers, converters, and brand owners will accelerate scalable innovation with premium market value.

Market Segmentation Analysis

The Global Flexible Packaging Barrier Paper market is classified based on Paper Type, Barrier Property, Coating Type, and End-Use Industry.

By Paper Type, the market is further segmented into:

Kraft Paper segment is valued at USD 7.4 billion in 2026 and is projected to reach USD 11.2 billion by 2033, at a CAGR of 6.1% during the forecast period.

Kraft Paper adoption will increase owing to strong fiber structure, print compatibility, durability, and established recyclability. Food wraps, pouch liners, and dry goods packaging will support segment expansion. Lighter grammage formats, improved barrier layers, and better converting performance will strengthen cost efficiency across packaging lines in the coming years.

Greaseproof Paper

Greaseproof Paper segment is valued at USD 4.3 billion in 2026 and is projected to reach USD 6.6 billion by 2033, at a CAGR of 6.4% during the forecast period.

Greaseproof Paper usage will increase across bakery packaging, snack wraps, and quick-service food packaging. Dense sheet formation helps restrict oil migration and maintains clean surface presentation. Compostable grades, improved heat resistance, and fluorine-free barrier treatments will attract food processors seeking cleaner packaging standards.

Parchment Paper

Parchment Paper segment is valued at USD 2.6 billion in 2026 and is projected to reach USD 3.5 billion by 2033, at a CAGR of 4.1% during the forecast period.

Parchment Paper adoption will expand across baking, confectionery, and specialty food packaging. Heat tolerance and release performance create value for ovenable and food-processing applications. Improved surface finish, moisture control, and decorative printing options will support premium packaging opportunities across branded product categories.

Glassine Paper

Glassine Paper segment is valued at USD 2.4 billion in 2026 and is projected to reach USD 4 billion by 2033, at a CAGR of 7.5% during the forecast period.

Glassine Paper adoption will increase owing to its smooth texture, transparency appeal, and grease-resistant properties. Labels, confectionery wraps, personal care sachets, and premium retail packaging will create steady revenue potential. Enhanced stiffness, anti-static treatment, and recyclable barrier structures will support stronger shelf presentation across modern retail channels.

Others

Others segment is valued at USD 2.6 billion in 2026 and is projected to reach USD 3.4 billion by 2033, at a CAGR of 3.9% during the forecast period.

Other paper grades include custom blends, multilayer specialty sheets, and technical barrier papers for niche applications. Medical wraps, industrial liners, protective inserts, and specialty retail packs create future scope. Coating innovation, regional sourcing models, and customized paper structures will improve commercial acceptance over the forecast period.

By Barrier Property, the market is divided into:

Moisture Barrier

Moisture Barrier segment is projected to reach USD 7.4 billion by 2033, at a CAGR of 5% during the forecast period.

Moisture Barrier solutions will gain importance across cereals, powders, pet food, and dry snacks. Controlled humidity protection extends storage life and maintains product texture quality. Advanced coating systems, plant-based barrier layers, and precision converting lines will strengthen future packaging performance standards.

Oxygen Barrier

Oxygen Barrier segment is projected to reach USD 6.4 billion by 2033, at a CAGR of 6.5% during the forecast period.

Oxygen Barrier adoption will increase across coffee, processed food, and nutraceutical packaging where freshness retention remains essential. Reduced oxidation supports flavor stability and shelf value. Nanocoatings, multilayer paper formats, and recyclable high-barrier designs will guide next-generation packaging investment plans.

Grease/Oil Barrier

Grease/Oil Barrier segment is projected to reach USD 7.2 billion by 2033, at a CAGR of 6.5% during the forecast period.

Grease/Oil Barrier formats will expand across fried foods, ready meals, bakery products, and takeaway packaging. Surface cleanliness and stain prevention improve consumer experience. Fluorine-free chemistries, compostable treatments, and heat-stable coatings will shape safer and greener packaging standards ahead.

Vapor Barrier

Vapor Barrier segment is projected to reach USD 3.8 billion by 2033, at a CAGR of 4.3% during the forecast period.

Vapor Barrier materials will gain traction across sensitive ingredients, powders, and aroma-rich products requiring controlled transmission rates. Stable internal conditions protect product quality during storage and transportation. Engineered coatings, advanced sealing methods, and climate-focused packaging designs will encourage broader industrial adoption.

Aroma/Flavour Barrier

Aroma/Flavour Barrier segment is projected to reach USD 4.0 billion by 2033, at a CAGR of 6.7% during the forecast period.

Aroma/Flavor Barrier papers will support coffee, tea, spices, and premium snack categories where sensory retention influences repeat purchases. Controlled aroma retention preserves product value and brand quality perception. Hybrid barrier layers, precision closures, and recyclable pouch systems will expand premium packaging applications globally.

By Coating Type, the market is further divided into:

Polymer Coatings

Polymer Coatings segment is projected to reach USD 8.5 billion by 2033.

Polymer Coatings will remain significant owing to strong sealability, moisture protection, and broad machine compatibility. Food packaging and consumer goods packaging will create steady volume demand. Mono-material innovation, thinner coating gauges, and recycling-compatible systems will improve sustainability positioning across future supply chains.

Wax Coatings

Wax Coatings segment is projected to reach USD 4.2 billion by 2033.

Wax Coatings will serve bakery wraps, frozen foods, and moisture-sensitive products requiring cost-effective protection. Smooth release properties and water resistance add functional value across food packaging applications. Natural wax blends, cleaner processing methods, and compostable combinations will renew commercial interest in the coming years.

Aluminium Foil Coatings

Aluminium Foil Coatings segment is projected to reach USD 3.7 billion by 2033.

Aluminum Foil Coatings will support premium barrier requirements across pharmaceuticals, coffee, and high-value food categories. Strong resistance to light, oxygen, and moisture creates high protection levels. Lightweight foil structures, downgauging technologies, and recycling-focused recovery systems will improve efficiency across production networks.

Water-Based Coatings

Water-Based Coatings segment is projected to reach USD 7.9 billion by 2033.

Water-Based Coatings will gain momentum through low-emission processing, safer handling, and regulatory alignment. Brands seeking greener packaging will increase procurement activity across food, personal care, and consumer goods categories. Faster drying systems, stronger adhesion, and printable surfaces will make commercial scaling highly attractive across multiple industries.

Bio-Based/Biodegradable Coatings

Bio-Based/Biodegradable Coatings segment is projected to reach USD 4.4 billion by 2033.

Bio-Based and Biodegradable Coatings will expand with sustainability targets and rising compostable packaging adoption. Renewable feedstock usage supports circular economy goals and reduces dependence on fossil-based coating materials. Barrier performance research, industrial compost certification, and wider raw material availability will create strong future revenue opportunities across packaging converters.

By End-Use Industry, the Global Flexible Packaging Barrier Paper market is divided as:

Food and Beverages

Food and Beverages segment is projected to grow at a CAGR of 6.2% during the forecast period.

Food and Beverage will lead adoption across snacks, bakery products, frozen foods, dairy powders, and beverage ingredients. Shelf-life protection and branding value remain major drivers across packaged food applications. Sustainable packaging transitions and convenience-led consumption trends will sustain long-term segment momentum.

Personal Care and Cosmetics

Personal Care and Cosmetics segment is projected to grow at a CAGR of 6.7% during the forecast period.

Personal Care and Cosmetics usage will increase across sachets, refill packs, soap wraps, and beauty accessory packaging. Premium appearance with eco-friendly appeal attracts brands targeting sustainable product positioning. Moisture control, fragrance retention, and decorative printing advances will support category expansion in future markets.

Pharmaceuticals segment is projected to grow at a CAGR of 7.1% during the forecast period.

Pharmaceutical adoption will increase across powders, medical devices, diagnostic kits, and over-the-counter products requiring hygiene-focused packaging. Barrier reliability, contamination control, and traceability remain critical procurement factors. Tamper-evident formats, sterile converting standards, and smart labeling integration will strengthen future usage across healthcare channels.

Retail and Consumer Goods

Retail and Consumer Goods segment is projected to grow at a CAGR of 3.9% during the forecast period.

Retail and Consumer Goods applications will expand across household items, stationery, electronics accessories, and seasonal product packaging. Lightweight paper formats reduce logistics burden while supporting shelf appeal. Attractive graphics, easy-open designs, and recyclable structures will improve adoption across organized retail networks.

Others

Others segment is projected to grow at a CAGR of 2.8% during the forecast period.

Other end-use sectors include agriculture, industrial components, pet care, and hospitality packaging applications. Custom pack sizes and strong barrier formats create steady commercial opportunities. Regional production expansion, export activity, and sustainability mandates will widen adoption across additional business segments.

By Region:

Based on geography, the Global Flexible Packaging Barrier Paper market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America is witnessing rising Flexible Packaging Barrier Paper adoption owing to corporate sustainability targets, strong packaged food consumption, and growing retailer preference for recyclable packaging formats.

Europe dominates the Flexible Packaging Barrier Paper market, supported by strict packaging waste regulations, strong sustainability commitments, and high adoption of recyclable paper-based packaging.

Asia-Pacific offers strong opportunities for the Flexible Packaging Barrier Paper market owing to expanding manufacturing capacity, rising packaged food consumption, and increasing demand for consumer goods packaging.

Across South America, the Middle East, and Africa, the Flexible Packaging Barrier Paper market is progressing through gradual industrial growth, rising food packaging demand, and improving paper converting capabilities.

Competitive Landscape and Strategic Insights

The Global Flexible Packaging Barrier Paper market is gaining attention as companies across food, healthcare, home care, personal care, and retail seek packaging that delivers product protection while reducing plastic use. Barrier paper is valued for restricting moisture, grease, oxygen, aroma, and light exposure, which supports shelf-life extension and product safety. Adoption will rise as manufacturers pursue packaging formats that meet performance needs, consumer expectations, recyclability targets, and responsible sourcing standards.

Established paper and packaging companies are shaping competition through product development, coating technology, print quality, converting strength, and supply reliability. Mondi plc remains a major player with a broad packaging network and continued investment in sustainable materials. Billerud AB is recognized for strong paper grades and performance packaging solutions. UPM-Kymmene Corporation uses its paper expertise to support new barrier options across multiple industries, while Sappi Limited continues to expand specialty paper offerings for premium packaging applications.

Amcor plc and Huhtamäki Oyj bring deep packaging expertise and global customer reach, supporting faster responses to evolving packaging requirements. Koehler Paper SE and Lecta continue to strengthen their positions through functional papers designed for flexible packaging uses. Ahlstrom Oyj and Nippon Paper Industries Co., Ltd. add value through technical expertise and material innovation. TOPPAN Inc. is active in advanced packaging systems, while delfortgroup AG focuses on specialty papers with enhanced protection features.

Walki Group Oy, Coveris Management GmbH, Graphic Packaging International, LLC, and ProAmpac LLC are important participants owing to their ability to connect material science with commercial packaging requirements. International Paper Company, including DS Smith operations, strengthens its position through circular packaging capabilities and fiber-based packaging scale. Parkside Flexibles and Felix Schoeller Holding GmbH & Co. KG bring niche strengths for brands seeking customized packaging solutions. Pudumjee Paper Products Limited and Appvion also support market expansion through specialty paper development.

Miquel y Costas & Miquel, S.A., Constantia Flexibles Group GmbH, and Sonoco Products Company continue to compete through innovation, technical capability, and customer partnerships. BOBST Group SA supports the broader industry through converting and manufacturing equipment that improves packaging output. Michelman, Inc., Dow Inc., BASF SE, Sun Chemical Corporation, and Heidelberger Druckmaschinen AG play a strong supporting role through coatings, inks, chemicals, adhesives, printing systems, and process technologies.

Competition in the Global Flexible Packaging Barrier Paper market will intensify as brands demand stronger barrier performance, improved print appeal, scalable recyclability, and lower environmental impact. Companies that combine cost control, product quality, regulatory alignment, and scalable supply chains will remain well positioned over the coming years.

Forecast and Future Outlook

Market size is forecast to rise from USD 18.3 billion in 2025 to over USD 28.8 billion by 2033.

The Global Flexible Packaging Barrier Paper market will increasingly integrate with circular packaging systems where recyclability, renewable sourcing, and lower carbon intensity influence procurement decisions. Advancements in barrier science, coating efficiency, and converting performance will accelerate adoption across premium and mass-market packaging categories.

Flexible Packaging Barrier Paper Market Key Segments:

By Paper Type:

Kraft Paper

Greaseproof Paper

Parchment Paper

Glassine Paper

Others

By Barrier Property:

Moisture Barrier

Oxygen Barrier

Grease/Oil Barrier

Vapor Barrier

Aroma/Flavour Barrier

By Coating Type:

Polymer Coatings

Wax Coatings

Aluminium Foil Coatings

Water-Based Coatings

Bio-Based/Biodegradable Coatings

By End-Use Industry:

Food and Beverages

Personal Care and Cosmetics

Pharmaceuticals

Retail and Consumer Goods

Others

Key Global Flexible Packaging Barrier Paper Industry Players

This research report categorizes the Flexible Packaging Barrier Paper market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Flexible Packaging Barrier Paper market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Flexible Packaging Barrier Paper market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 5.8% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Kilotons

Segmentation

By Paper Type, Barrier Property, Coating Type, End-Use Industry, and Region

By Region

North America (By Paper Type, Barrier Property, Coating Type, End-Use Industry, and Country)

United States

Canada

Mexico

Europe (By Paper Type, Barrier Property, Coating Type, End-Use Industry, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Paper Type, Barrier Property, Coating Type, End-Use Industry, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Paper Type, Barrier Property, Coating Type, End-Use Industry, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Paper Type, Barrier Property, Coating Type, End-Use Industry, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Europe Premium Molded Fiber Market Size, Share, Trends, 2033

Europe Premium Molded Fiber market size is valued at USD 448.0 million in 2025 and is projected to reach USD 901.0 million in 2033, at a CAGR of 9.2% from 2026 to 2033

Europe Premium Molded Fiber Market, Europe Premium Molded Fiber Market Size, Europe Premium Molded Fiber Market Share, Europe Premium Molded Fiber Market Analysis, Europe Premium Molded Fiber Market Growth, Europe Premium Molded Fiber Market Trends, Europe Premium Molded Fiber Market Research Report, Europe Premium Molded Fiber Market Forecast, Europe Premium Molded Fiber, Europe Premium Molded Fiber Market Research, Europe Premium Molded Fiber Industry, Europe Premium Molded Fiber Industry Report, Europe Premium Molded Fiber Market Data, Europe Premium Molded Fiber Statistics, Europe Premium Molded Fiber Market Statistics, Europe Premium Molded Fiber Industry Trends, Europe Premium Molded Fiber Market Report, Europe Premium Molded Fiber Market Trends, Europe Premium Molded Fiber Market News, Europe Premium Molded Fiber Forecasts, Europe Premium Molded Fiber Market Intelligence Report

North America Infant Formula Metal Packaging Market Size, Share, Trends, 2033

North America Infant Formula Metal Packaging market size is valued at USD 7,665.5 million in 2025 and is projected to reach USD 12,123.8 million in 2033, at a CAGR of 5.7% from 2026 to 2033

North America Infant Formula Metal Packaging Market, North America Infant Formula Metal Packaging Market Size, North America Infant Formula Metal Packaging Market Share, North America Infant Formula Metal Packaging Market Analysis, North America Infant Formula Metal Packaging Market Growth, North America Infant Formula Metal Packaging Market Trends, North America Infant Formula Metal Packaging Market Research Report, North America Infant Formula Metal Packaging Market Forecast, North America Infant Formula Metal Packaging, North America Infant Formula Metal Packaging Market Research, North America Infant Formula Metal Packaging Industry, North America Infant Formula Metal Packaging Industry Report, North America Infant Formula Metal Packaging Market Data, North America Infant Formula Metal Packaging Statistics, North America Infant Formula Metal Packaging Market Statistics, North America Infant Formula Metal Packaging Industry Trends, North America Infant Formula Metal Packaging Market Report, North America Infant Formula Metal Packaging Market Trends, North America Infant Formula Metal Packaging Market News, North America Infant Formula Metal Packaging Forecasts, North America Infant Formula Metal Packaging Market Intelligence Report

RTD Packaging Systems Market Size, Share, Trends, 2033

Global RTD Packaging Systems market size is valued at USD 134.3 billion in 2025 and is projected to reach USD 220.4 billion in 2033, at a CAGR of 6.4% from 2026 to 2033

RTD Packaging Systems Market, RTD Packaging Systems Market Size, RTD Packaging Systems Market Share, RTD Packaging Systems Market Analysis, RTD Packaging Systems Market Growth, RTD Packaging Systems Market Trends, RTD Packaging Systems Market Research Report, RTD Packaging Systems Market Forecast, RTD Packaging Systems, RTD Packaging Systems Market Research, RTD Packaging Systems Industry, RTD Packaging Systems Industry Report, RTD Packaging Systems Market Data, RTD Packaging Systems Statistics, RTD Packaging Systems Market Statistics, RTD Packaging Systems Industry Trends, RTD Packaging Systems Market Report, RTD Packaging Systems Market Trends, RTD Packaging Systems Market News, RTD Packaging Systems Forecasts, RTD Packaging Systems Market Intelligence Report

Global Tinplate market size is valued at USD 31.9 billion in 2025 and is projected to reach USD 41.4 billion in 2033, at a CAGR of 3.3% from 2026 to 2033