Global Operations Support Systems (OSS) Market Size, Share, By Component (Software and Services), By Deployment Mode (On-Premises and Cloud), By Application (Network Management, Service Assurance, Customer Management, Inventory Management, and Others), By End-User (Telecommunications, IT, BFSI, Healthcare, Retail, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4569

Published

March 2, 2026

Pages

311 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

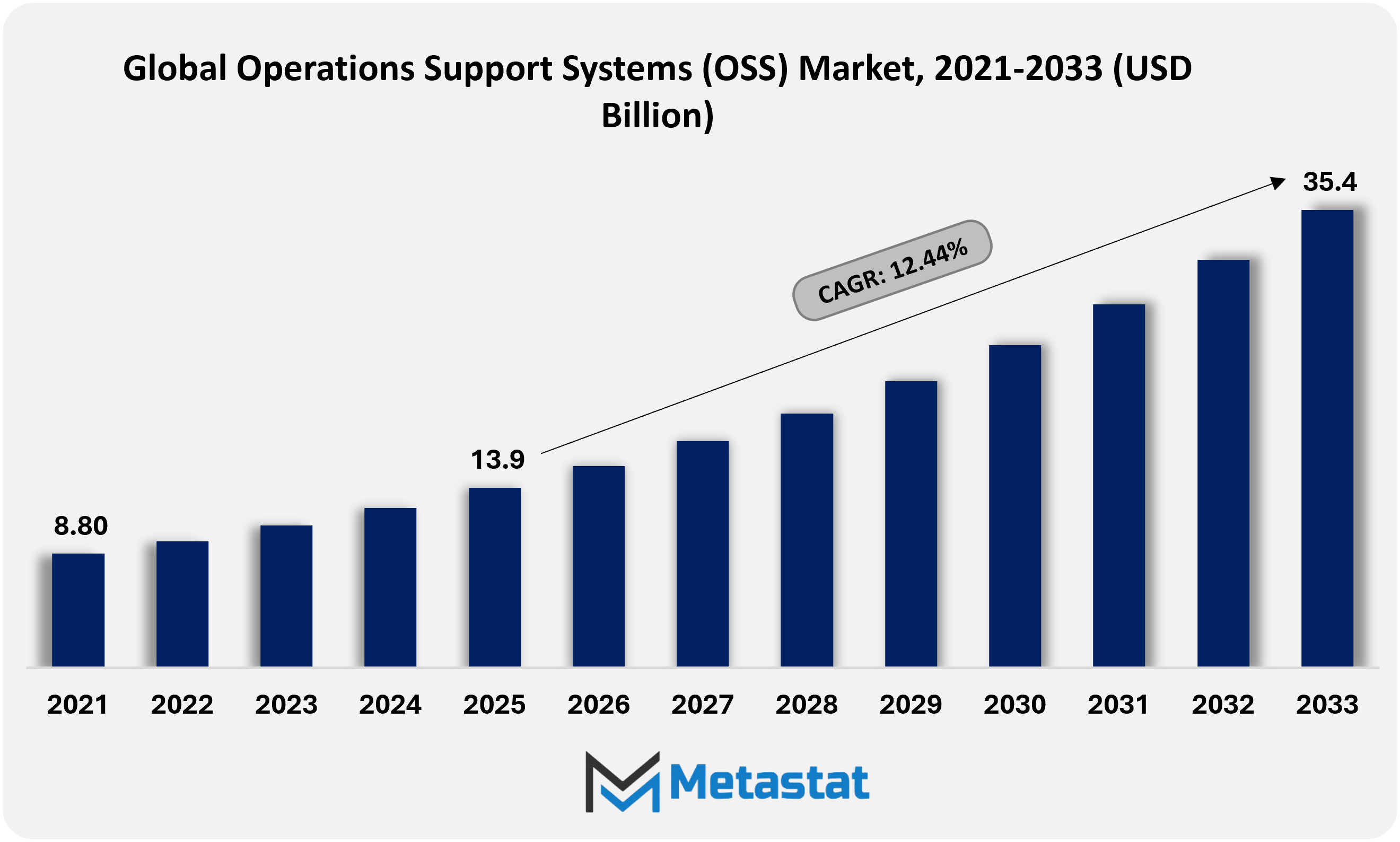

The Global Operations Support Systems (OSS) market size was valued at USD 13.9 billion in 2025. The market is projected to grow from USD 15.6 billion in 2026 to USD 35.4 billion by 2033, exhibiting a CAGR of 12.4% during the forecast period.

Global Operations Support Systems (OSS) Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Operations Support Systems (OSS) market valued at USD 13.9 billion in 2025, growing at a CAGR of 12.4% through 2033, with potential to exceed USD 35.4 billion.

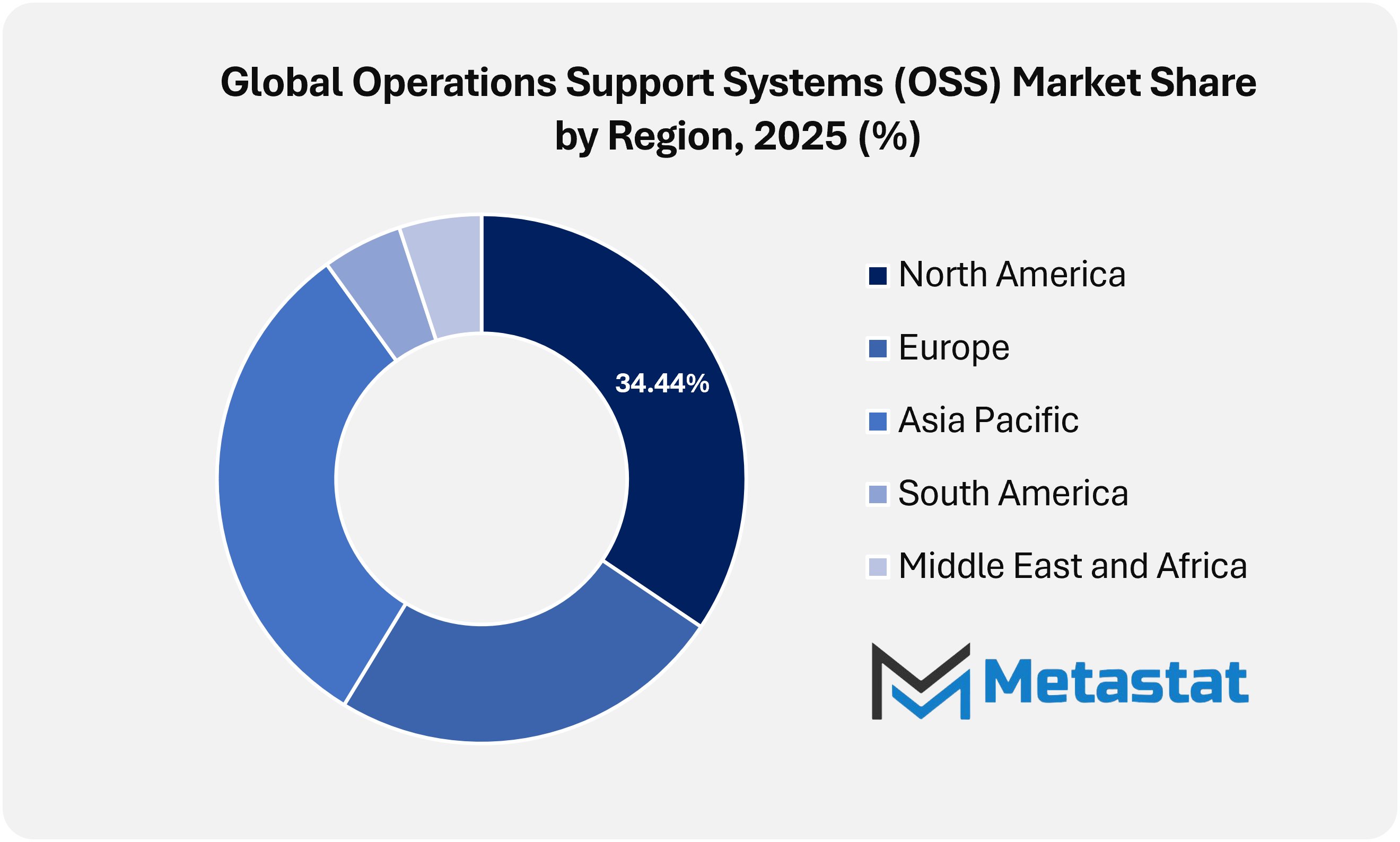

North America accounted for 34.4% of global revenue in 2025, led by the United States.

Software segment accounted for 64.6% share in 2025.

Key drivers include rapid deployment of 5G, fiber, and cloud-native networks that increase network operations complexity and propel demand for advanced OSS platforms, along with rising focus on service quality, uptime, and real-time network visibility that accelerates adoption of automated and analytics-driven OSS solutions.

Opportunities include increased adoption of AI, machine learning, and intent-based networking within OSS platforms, enabling predictive maintenance, autonomous networks, and operating cost optimization.

Key insight: Operational complexity across telecom and digital service networks is accelerating OSS modernization, positioning scalable, automation-driven platforms for sustained global demand.

The global operations support systems (OSS) market within the telecom and digital infrastructure industry is moving beyond traditional operational coordination and is reshaping how service ecosystems are designed, governed, and monetized. OSS frameworks will no longer sit quietly behind network layers. Platforms will act as intelligent conductors for autonomous service environments spanning satellites, private networks, edge nodes, and virtual operators.

Operational intelligence will be distributed rather than centralized. The OSS architecture will anticipate conditions, negotiate resources, and recalibrate service logic in multi-domain networks without manual sequencing. Predictive assurance will blend behavioral data, environmental signals, and contractual logic, enabling service quality commitments to be upheld through self-adjusting operational models. Network events will be interpreted contextually, enabling intent-driven outcomes rather than reactive workflows.

Market Dynamics

Growth Drivers:

Rapid deployment of 5G, fiber, and cloud-native networks is increasing the complexity of network operations, propelling demand for advanced OSS platforms.

Rapid deployment of 5G, fiber, and cloud-native infrastructure is reshaping the global operations support systems (OSS) market. Virtualized network functions and distributed edge environments increase operational complexity. Advanced OSS platforms support orchestration, configuration accuracy, and performance coordination, enabling telecom operators to manage multi-vendor, multi-technology environments with higher reliability and long-term operational stability.

Rising focus on service quality, uptime, and real-time network visibility is accelerating adoption of automated and analytics-driven OSS solutions.

The increasing emphasis on quality of service, uptime assurance, and real-time visibility over the network is accelerating OSS adoption. Automated tracking and analytics-driven structures will enhance fault detection and overall performance optimization. Telecom operators increasingly prioritize proactive issue resolution, driving OSS solutions toward continuous intelligence, actionable insights, and data-driven operational governance across complex service ecosystems.

Restraints and Challenges:

High implementation and integration costs with legacy BSS, network elements, and IT systems are limiting adoption among smaller operators.

High implementation costs and integration requirements with legacy BSS, network elements, and IT systems limit adoption, particularly among smaller operators. Modernization programs often require significant upfront investment and complex integration work. Adoption patterns remain uneven, shaped by capital availability, internal readiness, and the ability to align legacy operating models with modern digital architectures.

Complexity in migrating from monolithic legacy OSS to cloud-native and microservices-based architectures is slowing transformation timelines.

The shift from monolithic OSS structures to cloud-native, microservices-primarily based architectures introduces technical and organizational demanding situations. Extended transition timelines, operational risks, and dependency management slow down trade efforts. Phased deployment approaches and targeted skills development are essential to minimize disruption while maintaining service continuity during large-scale operational changes.

Opportunities:

Increasing adoption of AI, machine learning, and intent-based networking within OSS platforms, enabling predictive maintenance, autonomous networks, and operating cost optimization.

Adoption of artificial intelligence, machine learning, and intent-based networking opens new growth avenues. Predictive maintenance, autonomous operations, and cost optimization gain stronger prioritization. The global operations support systems (OSS) market will advance platforms capable of continuous learning, adaptive decision-making, and reduced manual intervention, supporting future-ready network operations at scale.

Market Segmentation Analysis

The Global Operations Support Systems (OSS) market is segmented based on Component, Deployment Mode, Application, and End User.

By Component, the market is further segmented into:

Software

Software segment was valued at USD 10.1 billion in 2026 and is projected to reach USD 21.4 billion by 2033, at a CAGR of 11.3% during the forecast period.

Software offerings will shape operational intelligence through modular structures, assisting analytics, automation, and defect resolution. Future software program layers will emphasize interoperability, real-time processing, and AI-assisted choice frameworks. Continued enhancements will support community scale growth even as permitting proactive operations, compliance alignment and cost governance throughout multi-technology infrastructure.

Services

Services segment was valued at USD 5.5 billion in 2026 and is projected to reach USD 14.0 billion by 2033, at a CAGR of 14.2% during the forecast period.

The service-based offering will support deployment optimization, lifecycle management, and operational advisory. Managed services will expand through long-term partnerships focusing on performance assurance and system resiliency. Consulting, integration, and maintenance functions will evolve toward results-based delivery models supporting adaptive operating strategies and continued platform efficiency.

By Deployment Mode, the market is divided into:

On-Premises

On-Premises segment is projected to reach USD 14.2 billion by 2033, at a CAGR of 7.9% during the forecast period.

On-premises deployment will remain relevant for environments requiring tight controls, regulatory alignment and data sovereignty. Future on-site systems will integrate layers of automation, reducing manual inspection. Hybrid compatibility will be stronger, allowing controlled modernization without infrastructure displacement while maintaining predictable performance and governance standards.

Cloud

Cloud segment is projected to reach USD 21.2 billion by 2033, at a CAGR of 16.5% during the forecast period.

Cloud deployment will accelerate scalability through elastic resources and centralized control. Future cloud-native OSS platforms will support fast provisioning, continuous updates, and distributed access. Subscription-based adoption will increase operational agility while enabling advanced analytics, inter-regional monitoring, and cost transparency across larger network footprints.

By Application, the market is further divided into:

Network Management

Network Management segment is projected to reach USD 9.2 billion by 2033 and accounted for 29.9% share in 2025.

Network management functions will shift toward predictive monitoring and self-adaptation frameworks. Advanced telemetry ingestion will support early fault detection and dynamic capacity planning. Automation-driven controls will reduce outage exposure while supporting increasing network density in virtualized and software-defined environments.

Service Assurance

Service Assurance segment is projected to reach USD 10.5 billion by 2033 and accounted for 25.8% share in 2025.

Service assurance will emphasize experience-centric monitoring through real-time quality metrics. Future solutions will correlate performance data with automated corrective actions. Predictive alerts will minimize downtime while supporting service-level compliance across enterprise and consumer-grade offerings within complex operational ecosystems.

Customer Management

Customer Management segment is projected to reach USD 3.7 billion by 2033 and accounted for 13.8% share in 2025.

Customer management applications will integrate operational data with service interaction workflows. Future platforms will support integrated views on provisioning, billing alignment, and problem resolution. Automation will improve response accuracy while analytics-driven insights will strengthen service personalization and long-term customer value retention.

Inventory Management

Inventory Management segment is projected to reach USD 5.6 billion by 2033 and accounted for 18.4% share in 2025.

Inventory management systems will transition toward dynamic asset visibility and automated reconciliation. Digital twins and real-time updates will improve usage accuracy. Future inventory layers will support rapid scaling, lifecycle tracking, and dependency mapping across physical and virtual network components.

Others

Others segment is projected to reach USD 6.3 billion by 2033 and accounted for 12.1% share in 2025.

Additional applications will include analytics hubs, compliance monitoring, and orchestration engines. Future adoption will focus on specific operational controls supporting network functions. Modular expansion will allow tailored configurations to align with evolving operational models and emerging technology frameworks.

By End-User, the Global Operations Support Systems (OSS) market is divided as:

Telecommunications

Telecommunications segment is projected to grow at a CAGR of 10.3% during the forecast period.

Telecom operators will remain the primary adopters due to network scale and service complexity. Future deployments will support 5G expansion, virtualization, and edge operations. The OSS framework will enable automated provisioning and performance assurance in dense customer environments and diverse service portfolios.

IT

IT segment is projected to grow at a CAGR of 13.6% during the forecast period.

IT enterprises will adopt OSS platforms that support infrastructure convergence and service optimization. Future use will emphasize visibility in hybrid environments. Integrated monitoring and automation will support uptime assurance, workload balancing and operational cost discipline within the enterprise digital ecosystem.

BFSI

BFSI segment is projected to grow at a CAGR of 14.8% during the forecast period.

BFSI organizations will leverage OSS solutions that support secure operations and compliance-driven monitoring. Flexibility, transaction continuity and audit readiness will be prioritized in future implementation. Controlled automation will increase service reliability in digital banking, payment platforms and data-intensive financial operations.

Healthcare

Healthcare segment is projected to grow at a CAGR of 13.7% during the forecast period.

Healthcare institutions will adopt OSS platforms that support system availability and data integrity. Future frameworks will support critical service monitoring in connected medical infrastructure. These platforms will minimize operational disruption risks while supporting regulatory alignment and patient-centric digital service delivery.

Retail

Retail segment is projected to grow at a CAGR of 17.9% during the forecast period.

Retail enterprises will implement OSS tools that support omnichannel operations and infrastructure stability. Future use will emphasize demand-responsive scalability and service uptime. Integrated monitoring will support digital storefronts, supply chain connectivity and customer engagement platforms during high-volume activity periods.

Others

Others segment is projected to grow at a CAGR of 13.9% during the forecast period.

Additional end-user segments will include government, manufacturing and logistics sectors. Future adoption will focus on operational transparency and automation. OSS platforms will support infrastructure modernization initiatives while enabling reliable service delivery in distributed operational environments.

By Region:

Based on geography, the Global Operations Support Systems (OSS) market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

The North America Operations Support Systems (OSS) market is set to expand at a CAGR of 12.4% during 2026-2033, reaching USD 11.2 billion by 2033.

In North America, accelerated 5G network densification will force operators to rely on OSS platforms capable of handling real-time service assurance and automated fault resolution.

Across North America, growing enterprise demand for private networks will drive OSS adoption toward platforms that support multi-tenant visibility and lifecycle governance.

Within Asia Pacific, rapid telecom customer expansion will create an opportunity for OSS vendors to provide scalable provisioning aligned with high-volume service rollouts.

Asia Pacific will provide opportunities for customized OSS solutions for hybrid cloud integration supporting diverse operator maturity levels.

The Middle East, Africa, and South America will reflect uneven OSS deployment patterns shaped by infrastructure modernization priorities, regulatory pace, and operator focus on cost-efficient service continuity rather than advanced monetization layers.

Competitive Landscape and Strategic Insights

The global operations support systems market continues to influence how telecom operators manage networks, services, and customer experiences. OSS platforms support network monitoring, service fulfillment, fault management, and performance optimization, enabling stability while scaling digital services. Growing data traffic, cloud adoption, and the need for faster service delivery remain core market accelerators, supporting sustained momentum for established players and new entrants.

The large technology companies have a strong position in the market because of their experience in the industry and comprehensive offerings. The companies that will be at the forefront of OSS implementation for large telcos include Amdocs, Netcracker Technology, Ericsson, Nokia, Huawei, ZTE, Oracle Communications, IBM, and Hewlett Packard Enterprise. The key companies’ solutions handle complex networks and are designed to support long-term digital transformation strategies. NEC and Fujitsu are also important players, particularly in the Asia-Pacific region, where network modernization initiatives are constantly being expanded.

Medium-sized and focused vendors bring flexibility and focused innovation to the OSS field. Companies including Comviva, CSG Systems International, Comarch, Tecnotree, Subex, Cerillion, Hansen Technologies, gaiia, Optiva, Whale Cloud, TEOCO, Rakuten Symphony, Enghouse Networks, Tecalis, DigitalRoute, Telarix, iconectiv, Mobileum, and Infovista offer targeted solutions for analytics, revenue assurance, service orchestration, and assurance management. Their offering attracts operators seeking modular systems, fast deployment cycles, and cost efficiency. Zipit Wireless, Inc., MYCOM OSI, Anritsu, and Elisa Polystar strengthen market depth through advanced testing, assurance, and performance monitoring tools.

Competition within the OSS market is going to intensify as operators focus on automation, data-driven decision-making, and customer-centric network management. Vendors will prioritize scalable architecture, AI-supported insights, and seamless compatibility with BSS platforms. Partnerships, regional expansion and continuous platform upgrades will remain common strategies.

Forecast and Future Outlook

Market size is forecast to rise from USD 13.9 billion in 2025 to over USD 35.4 billion by 2033.

The global operations support systems (OSS) market will also impact workforce structures. Human roles will shift toward policy design, ethical oversight, and exception governance, while machine-led operations will manage routine orchestration. The skills in demand will focus on systems thinking and cross-domain fluency rather than latent network expertise. By extending operational intelligence across the strategic, commercial and governance layers, the global operations support systems (OSS) market will define how digital services industries will work, collaborate and scale in the network economies of the future.

Operations Support Systems (OSS) Market Key Segments:

By Component:

Software

Services

By Deployment Mode:

On-Premises

Cloud

By Application:

Network Management

Service Assurance

Customer Management

Inventory Management

Others

By End-User:

Telecommunications

IT

BFSI

Healthcare

Retail

Others

Key Global Operations Support Systems (OSS) Industry Players

This research report categorizes the Operations Support Systems (OSS) market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyzes the key growth drivers, opportunities, and challenges influencing the Operations Support Systems (OSS) market. Recent market developments and competitive strategies such as expansion, product launch, platform development, partnership, merger, and acquisition have been included to map the competitive landscape.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Operations Support Systems (OSS) market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 12.4% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Component, Deployment Mode, Application, End-User, and Region

By Component

Software

Services

By Deployment Mode

On-Premises

Cloud

By Application

Network Management

Service Assurance

Customer Management

Inventory Management

Others

By End-User

Telecommunications

IT

BFSI

Healthcare

Retail

Others

By Region

North America (By Component, Deployment Mode, Application, End-User, and Country)

United States

Canada

Mexico

Europe (By Component, Deployment Mode, Application, End-User, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of the Europe

Asia Pacific (By Component, Deployment Mode, Application, End-User, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Component, Deployment Mode, Application, End-User, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Component, Deployment Mode, Application, End-User, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Full In-Depth Analysis of the Parent Industry

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historic and Projected Market Analysis

Assessment Of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Major Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

The Metastat Insights study shows that the Global Operations Support Systems (OSS) market size was USD 13.9 billion in 2025.

The Global Operations Support Systems (OSS) market is likely to grow at a CAGR of 12.4% over the forecast period (2026-2033).

The Metastat Insights analysis shows that the North America Operations Support Systems (OSS) market size is estimated to be USD 11.2 billion by 2033.

Software is the leading component segment in the global market.

Rapid deployment of 5G, fiber, and cloud-native networks is increasing the complexity of network operations and propelling demand for advanced OSS platforms. Rising focus on service quality, uptime, and real-time network visibility is accelerating adoption of automated and analytics-driven OSS solutions.

North America region dominates the market.

High implementation and integration costs with legacy BSS, network elements, and IT systems limit adoption among smaller operators and hamper market growth during the forecast period.

Global Operations Support Systems (OSS) market is estimated to reach USD 35.4 billion by 2033.

Top players operating in the Operations Support Systems (OSS) industry include Amdocs, Netcracker Technology, Ericsson, Nokia, Huawei, ZTE, Oracle Communications, and IBM.

Global Online Dating market size reached USD 3.7 billion in 2025 and is forecast to hit USD 7.8 billion by 2033 at a 9.6% CAGR. Segment and regional data.

Online Dating market, Online Dating Market Size, Online Dating Market Share, Online Dating Market Analysis, Online Dating Market Growth, Online Dating Market Trends, Online Dating Market Research Report, Online Dating Market Forecast, Online Dating, Online Dating Market Research, Online Dating Industry, Online Dating Industry Report, Online Dating Market Data, Online Dating Statistics, Online Dating Market Statistics, Online Dating Industry Trends, Online Dating Market Report, Online Dating Market Trends, Online Dating Market News, Online Dating Forecasts, Online Dating Market Intelligence Report, Online Dating market 2033, Online Dating market outlook, Online Dating market segmentation, Online Dating market drivers, Online Dating market restraints, Online Dating market opportunities, Online Dating market CAGR, Online Dating suppliers, Online Dating manufacturers, Online Dating market by region, North America Online Dating market, Asia Pacific Online Dating market, Europe Online Dating market, Online Dating market competitive landscape, Online Dating market key players, Online Dating Apps market, Online Matchmaking Services market, Subscription-Based Online Dating market, Mobile Applications Online Dating market.

Global Containers-As-A-Service (CAAS) market size: USD 7.8 billion in 2025, forecast USD 83.9 billion by 2033 at a 34.4% CAGR. Segment and regional data.

Managed Mobility Services market size is valued at USD 5.8 billion in 2025 and projected to reach USD 20.5 billion by 2033, growing at a CAGR of 17.1%.