Southeast Asia Industrial Pumps Market Size, Share, By Product Type (Centrifugal Pump, Reciprocating, Rotary, and Others), By Drive Mechanism (Electric Driven and Engine Driven), By End User (Oil & Gas, Chemicals, Power Generation, Water and Wastewater, General Industry, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4538

Published

January 22, 2026

Pages

298 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

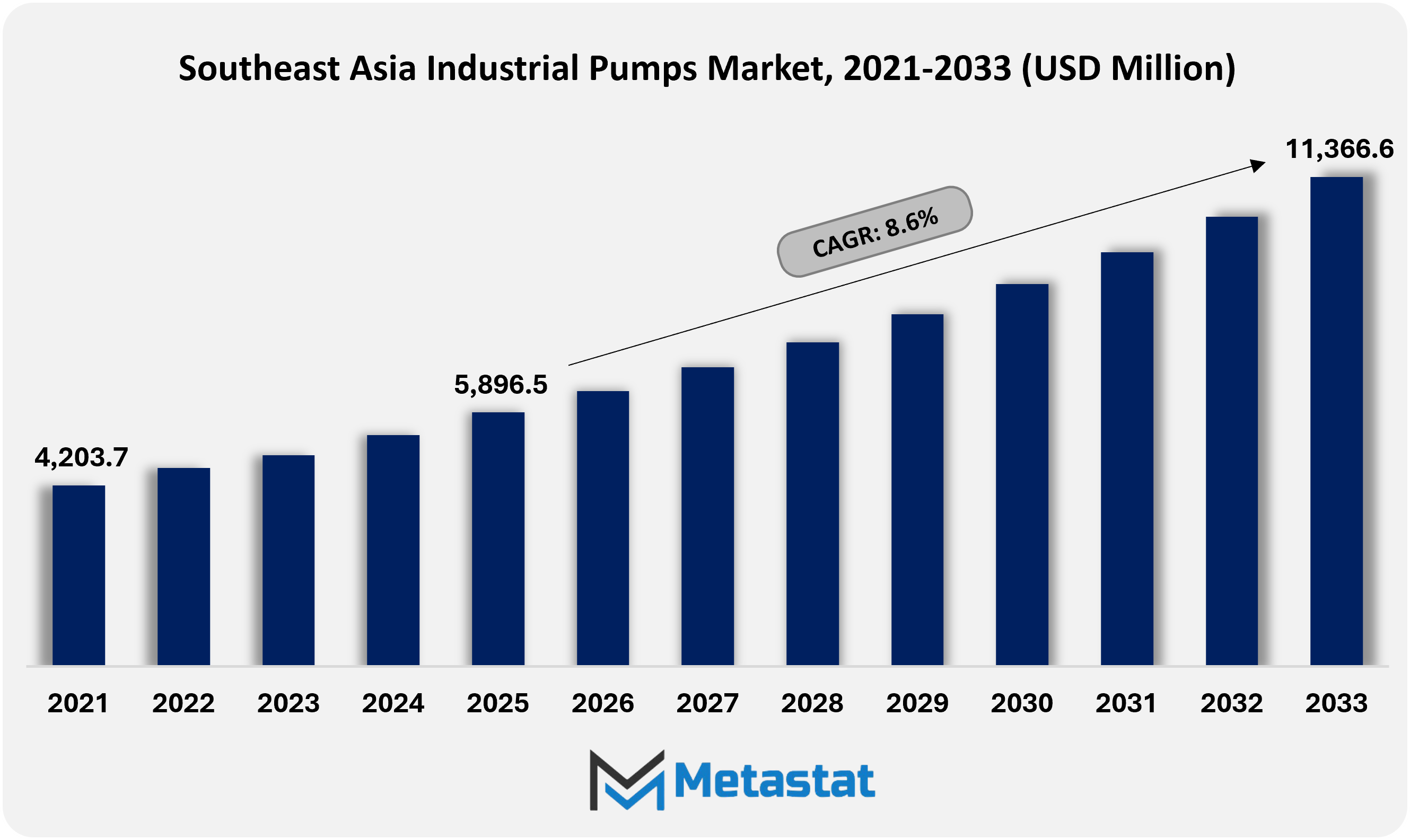

The Southeast Asia Industrial Pumps market size was valued at USD 5,896.5 million in 2025 and is projected to reach USD 11,366.6 million by 2033, registering a CAGR of 8.6% during 2026-2033.

Southeast Asia Industrial Pumps Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Southeast Asia Industrial Pumps market was valued at USD 5,896.5 million in 2025 and is projected to reach USD 11,366.6 million by 2033, registering a CAGR of 8.6% during 2026-2033.

Southeast Asia Industrial Pumps sales volume is projected to reach by 2,788 thousand units by 2033.

Centrifugal Pump segment accounts for a market share of 64.4% in 2025.

Key trends driving growth include accelerating industrialization across manufacturing, mining, power generation, and chemical sector, increasing requirements for reliable fluid handling equipment, along with rising investments in water infrastructure, wastewater treatment, and flood control projects supported by urban expansion and regulatory pressure.

The key opportunities include growing demand for energy-efficient and smart pump systems aligned with sustainability targets and operational cost optimization.

Key insight: Southeast Asia industrial pumps market expansion is shaped by infrastructure-led requirements and efficiency-driven innovation, balanced against cost sensitivity and pricing pressure.

The Southeast Asia industrial pumps market will move toward operational specialization, deeper regional manufacturing, and tighter alignment with end-user process requirements. Industrial activity in Indonesia, Vietnam, Thailand, and Malaysia will increasingly prefer pump systems engineered for site-specific duty cycles rather than multipurpose deployment. Procurement teams will prioritize engineered configurations aligned with chemical handling, slurry transfer, desalination processes, and thermal management across power assets.

Over the forecast period, supplier strategies will shift toward localized assembly and component sourcing to reduce lead times and foreign exchange risk. Regional production hubs will support rapid customization while meeting local requirements set by public infrastructure agencies. Industrial buyers will increasingly require performance guarantees tied to energy draw, seal life, and maintenance intervals, with contracts structured around lifecycle outcomes rather than unit pricing.

Market Dynamics

Growth Drivers:

Accelerating industrialization across manufacturing, mining, power generation, and chemicals, increasing demand for reliable fluid handling equipment.

Rapid industrialization in manufacturing, mining, steel, and chemicals is increasing requirements for dependable fluid handling systems. Expansion of production scale, capacity modernization, and process continuity requirements are strengthening the need for reliable pumping equipment. Procurement teams prioritize operational stability, low downtime, and standardized equipment integration to support long-term output expansion across Southeast Asian industrial corridors.

Rising investments in water infrastructure, wastewater treatment, and flood control projects driven by urban expansion and regulatory pressure.

Purchasing activity is reinforced by increased funding for water infrastructure, wastewater treatment, and flood management projects in region such as Vietnam and Thailand. Urban growth and tight regulatory pressure forces municipalities and utilities to undertake advanced pumping solutions. Future infrastructure packages will emphasize sustainability, electricity optimization, and lifecycle performance to control population density and environmental compliance objectives.

Restraints and Challenges:

High initial capital expenditure and maintenance costs, limiting adoption among small and mid-sized industrial operators.

High initial capital expenditure and maintenance costs restrict adoption among small and mid-sized industrial operators. Budget sensitivity and limited access to financing slows down the replacement cycles. Planning will require value-to-performance alignment, extended service intervals, and vendor-backed retrofit models to balance performance requirements with constrained capital availability.

Volatility in raw material prices, affecting pump manufacturing costs and long-term pricing stability.

Volatility in raw material prices such as cast iron, stainless steel, bronze, carbon steel, and aluminum, affects pump manufacturing costs and long-term pricing stability. Fluctuations in steel, alloys, and component sourcing pressure margin forecasts. Procurement strategies will increasingly prioritize localized sourcing, material innovation, and contractual price-protection measures to stabilize supply chains and mitigate financial risk.

Opportunities:

Growing demand for energy-efficient and smart pump systems aligned with sustainability targets and operational cost optimization.

Rising demand for energy-efficient and smart pump systems aligns with sustainability targets and operational cost optimization. Digital monitoring, predictive maintenance, and automation optimization are gaining priority. Low energy consumption, data-driven performance management, and compliance with local efficiency standards will be prioritized in future installations.

Market Segmentation Analysis

The Southeast Asia Industrial Pumps market is segmented by Product Type, Drive Mechanism and End User.

By Product Type, the market is further segmented into:

Centrifugal Pump

Centrifugal Pump segment is estimated at USD 4,118.3 million in 2026 and is projected to reach USD 7,659.9 million by 2033, at a CAGR of 9.3% during the forecast period.

Centrifugal pump segment in Southeast Asia will progress via system automation, city growth, and infrastructure enhancements. Industrial centres will prioritize strength performance, with the flow manipulate and low maintenance needs. Manufacturing modernization and enlargement of municipal tasks will guide the persistent, with design enhancements increasing operational reliability under high pressure and flow conditions.

Reciprocating

Reciprocating segment is estimated at USD 986.5 million in 2026 and is projected to reach USD 1,656.6 million by 2033, at a CAGR of 7.7% during the forecast period.

Demand for reciprocating pumps increases in applications requiring precise management and high stress performance. Oil processing, chemical dosing, and specialized business operations will keep aiding such systems. Technological refinements will enhance sturdiness and sealing performance, permitting longer provider life beneath disturbing working cycles in future business installations.

Rotary

Rotary segment is estimated at USD 932.3 million in 2026 and is projected to reach USD 1,488.1 million by 2033, at a CAGR of 6.9% during the forecast period.

The increase in viscous fluid handling in food processing, chemicals, and specialty manufacturing will propel the use of rotary pumps across the region. Consistent flow delivery and compact design will increase priority in space-constrained facilities. Future investments will focus on material enhancement and wear resistance to support continuous industrial production environments.

Others

Other pump categories will gain relevance through specific industrial requirements and customized engineering solutions. Mining, construction, and specialized manufacturing will require adaptable configurations. Innovation will emphasize modular design and application-specific performance, enabling suppliers to address diverse operational challenges in regional industrial development.

By Drive Mechanism, the market is divided into:

Electric Driven

Electric Driven segment is projected to reach USD 9,321.8 million by 2033, at a CAGR of 9.1% during the forecast period.

Electrically driven pump systems will dominate destiny installations owing to efficiency standards and sustainability goals. Industrial operators will adopt power solutions to reduce working charges and emissions. Grid enlargement and renewable integration will further support adoption, helping long-term operational sustainability within commercial facilities.

Engine Driven

Engine Driven segment is projected to reach USD 2,044.8 million by 2033, at a CAGR of 6.5% during the forecast period.

Engine-driven pumps will maintain significance in remote operations and emergency packages. Construction sites, temporary facilities, and off-grid business areas will rely upon such structures. Advances in fuel efficiency and emission controls will improve compliance with regional environmental policies while maintaining operational flexibility.

By End User, the market is further divided into:

Oil & Gas

Oil & Gas segment is projected to reach USD 2,471.2 million by 2033.

Oil and gas operations will continue to drive demand for pumps via exploration, refining, and transportation activities. Advanced recuperation methods and infrastructure enhancements will require robust pumping solutions. Future developments will focus on corrosion resistance and stress management to meet emerging operational and safety requirements.

Chemicals

Chemicals segment is projected to reach USD 1,244 million by 2033.

Chemical manufacturing will stimulate enduring demand for dependable pumping structures that help accuracy and safety. Process enhancement and chemical manufacturing would require advanced sealing and material compatibility. Technological advances will strengthen manipulation accuracy, helping to achieve higher manufacturing efficiency and regulatory compliance in chemical facilities.

Power Generation

Power Generation segment is projected to reach USD 1,266.5 million by 2033.

Power generation facilities will increase pump deployment to assist in cooling, fuel management and auxiliary operations. Emphasis on efficiency and reliability will guide system selection, ensuring uninterrupted energy delivery in thermal and renewable installations.

Water & Wastewater

Water & Wastewater segment is projected to reach USD 2,409.6 million by 2033.

Water and wastewater control will remain a significant boom driving force via urbanization and regulatory enforcement. Treatment plant expansion and community modernization would require higher ability pumping systems. Future making plans will prioritize sustainability and power savings to aid long-term public infrastructure sustainability.

General Industry

General industrial applications will generate broad-based demand in manufacturing, processing and logistics operations. Automation trends and productivity goals will influence pump selection. Equipment suppliers will align offerings with flexible performance requirements to support diverse industrial workflows.

Others

Others segment is projected to reach USD 486 million by 2033.

Other end-user segments contribute to incremental growth through agriculture, construction and emerging industrial activities. Mechanization and resource management initiatives will encourage pump adoption. The forward-looking investments will emphasize adaptability and cost efficiency to meet diverse operational requirements across expanded regions.

Competitive Landscape and Strategic Insights

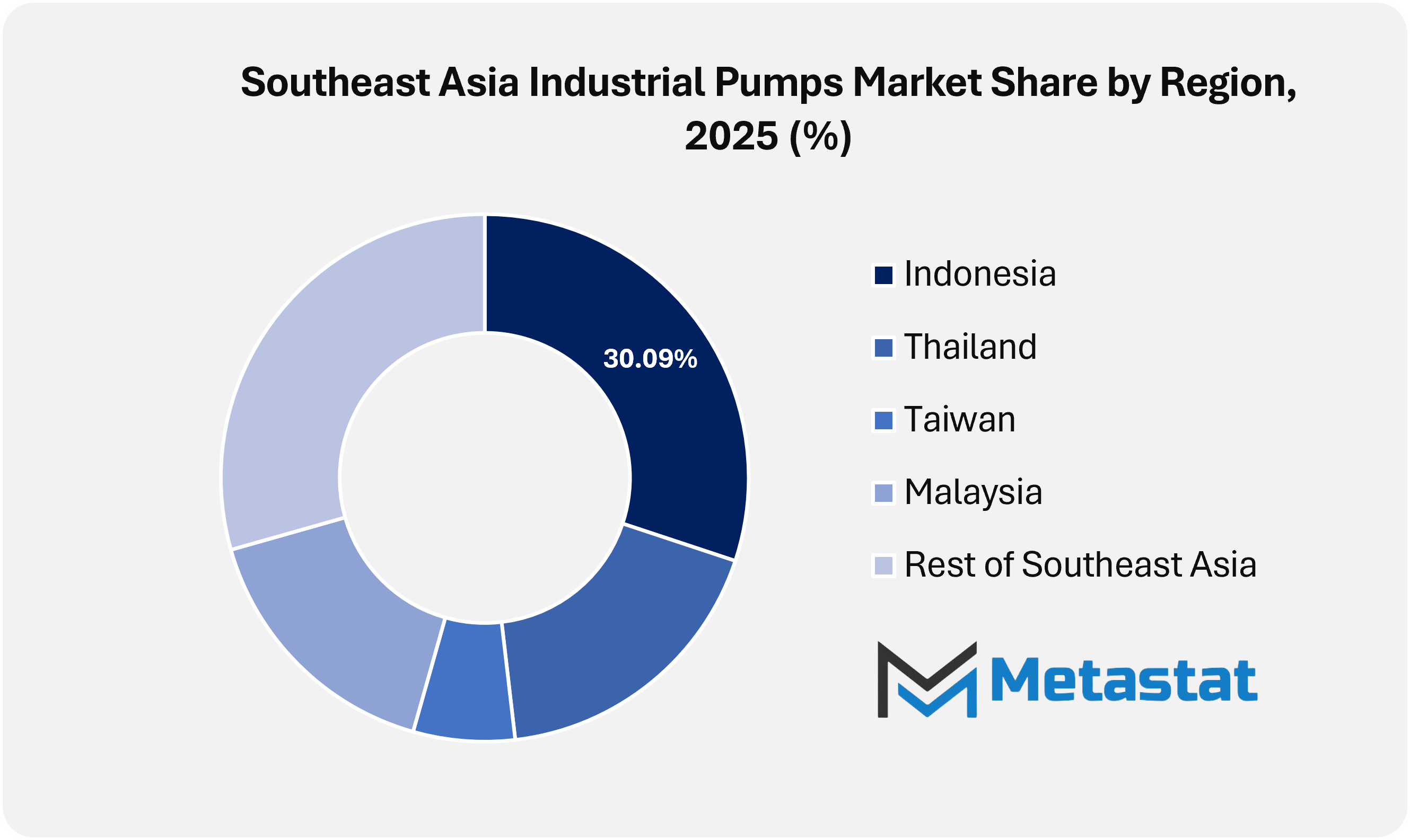

The Southeast Asia industrial pumps market continues to grow owing to rising business activity across production, electricity, water management, and construction industries. Rapid urban boom throughout countries like Indonesia, Vietnam, Thailand, and the Philippines will increase demand for dependable pumping systems utilized in water supply, wastewater treatment, and large infrastructure tasks. Expanding commercial zones and government-subsidized improvement applications will further help pump installations across each public and private centres. Industries will an increasing number of on sturdiness, power performance, and maintenance structures to control operating costs in difficult running situations.

Industrial pumps play an important role throughout oil and fuel operations, chemical processing, energy system, and mining operations within Southeast Asia. Growing investments in wastewater treatment facilities will reinforce the market call since nearby authorities will prioritize easy water access and environmental protection. Agricultural irrigation projects also make contributions to pump adoption, mainly in areas facing seasonal water shortages. End users will opt for solutions offering lengthy carrier life, solid performance, and compatibility with virtual tracking gear.

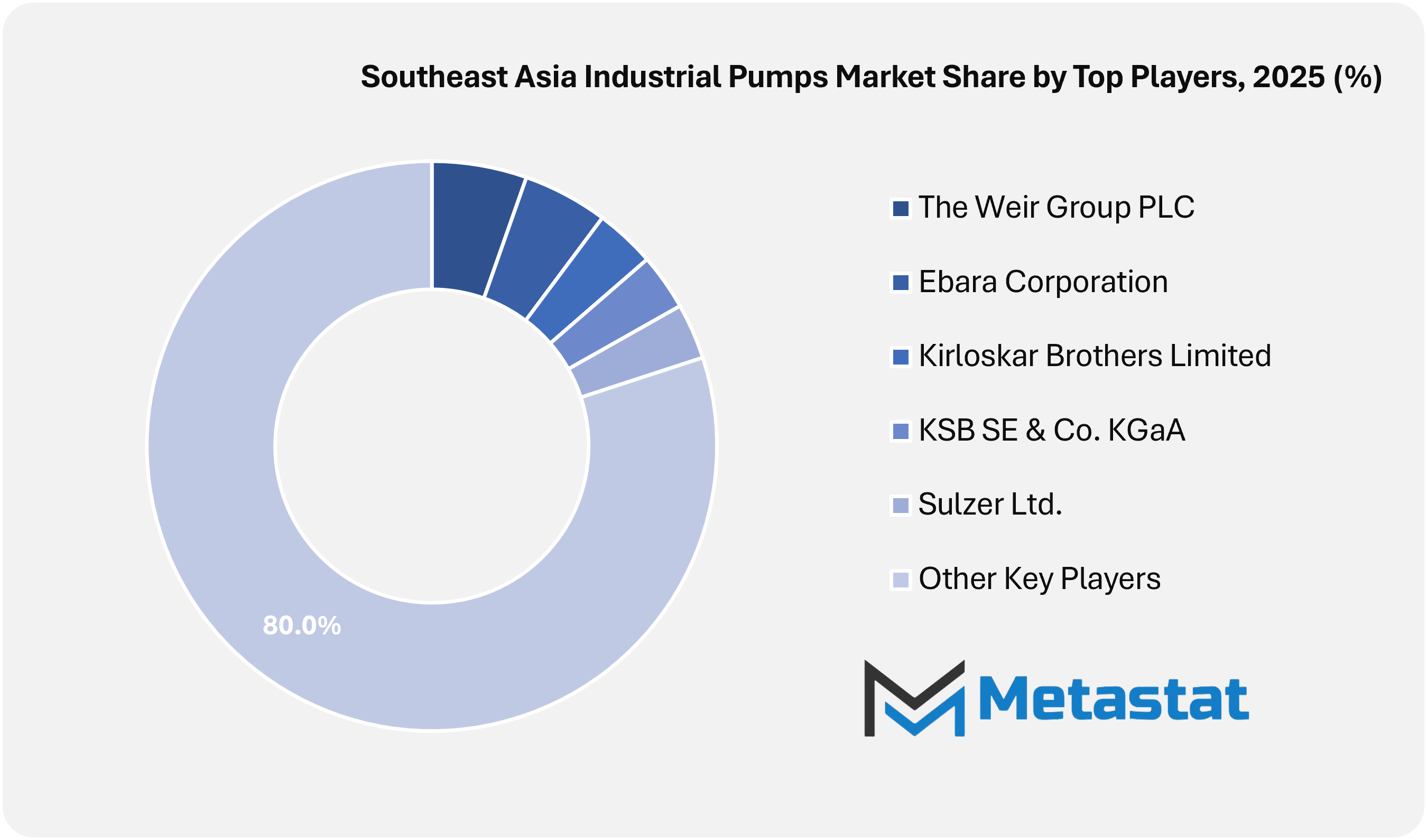

Several global and regional manufacturers maintain a strong presence in the Southeast Asia industrial pump market. Companies such as Grundfos Holding A/S, Flowserve Corporation, Sulzer Ltd., and Ebara Corporation remain active through product innovation and localized service networks, alongside Kirloskar Brothers Limited, Torishima Pump Mfg. Co., Ltd., and Tsurumi Manufacturing Co., Ltd.

Competition will continue to be intense with key players, including The Weir Group PLC, Wilo, ITT Inc., and Pentair PLC, increasing distribution partnerships and after-sales support at some stage in Southeast Asia. Market participants will invest in product upgrades and service reliability to secure long-term contracts across industrial sectors. Local manufacturing centres and nearby delivery chains will help reduce lead times and enhance customer response. Technological refinements, enlargement of infrastructure, and developing environmental attention will draft the purchase decisions within the Southeast Asia industrial pumps market.

Forecast and Future Outlook

Market size is forecast to rise from USD 5,896.5 million in 2025 to over USD 11,366.6 million by 2033. Looking ahead, the Southeast Asia industrial pumps market is shaped by collaboration between global technology holders and regional engineering firms. Knowledge transfer, localized testing facilities and workforce training investments will strengthen technological resilience on an industrial basis. Market progress will depend less on volume expansion and more on precision engineering, reliability assurance and inherent operational intelligence within pump systems.

The research report categorizes the Industrial Pumps market based on key segments and regions, forecasts revenue growth, and analyses trends in each sub and regional market. The report analyses the key growth drivers, opportunities, and challenges influencing the Industrial Pumps market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Industrial Pumps market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 8.6% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Thousand Units

Segmentation

By Product Type, Drive Mechanism, and End User

By Product Type

Centrifugal Pump

Reciprocating

Rotary

Others

By Drive Mechanism

Electric Driven

Engine Driven

By End User

Oil & Gas

Chemicals

Power Generation

Water & Wastewater

General Industry

Others

WHAT REPORT PROVIDES

Key Company Market Share and Revenue

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Prepositions of Leading Market Players

Stage Hoist market size is valued at USD 236.3 million in 2025 and is projected to reach USD 395.3 million in 2033, at a CAGR of 6.3% from 2026 to 2033.

Global Taper Lock Bushing market is valued at USD 1,187.8 million in 2025 and is projected to reach USD 1,808.0 million in 2033, at a CAGR of 5.4% from 2026 to 2033

Europe Mini Excavators Market Size, Share, Trends, 2033

Europe Mini Excavators market size is valued at USD 2,162.9 million in 2025 and is projected to reach USD 3,004.1 million in 2033, at a CAGR of 4.2% from 2026 to 2033

Europe Mini Excavators Market, Europe Mini Excavators Market Size, Europe Mini Excavators Market Share, Europe Mini Excavators Market Analysis, Europe Mini Excavators Market Growth, Europe Mini Excavators Market Trends, Europe Mini Excavators Market Research Report, Europe Mini Excavators Market Forecast, Europe Mini Excavators, Europe Mini Excavators Market Research, Europe Mini Excavators Industry, Europe Mini Excavators Industry Report, Europe Mini Excavators Market Data, Europe Mini Excavators Statistics, Europe Mini Excavators Market Statistics, Europe Mini Excavators Industry Trends, Europe Mini Excavators Market Report, Europe Mini Excavators Market Trends, Europe Mini Excavators Market News, Europe Mini Excavators Forecasts, Europe Mini Excavators Market Intelligence Report

Global Switch Actuators market size is valued at USD 18.4 billion in 2025 and is projected to reach USD 30.6 billion in 2033, at a CAGR of 6.6% from 2026 to 2033