Supply Side Platform (SSP) Market Size, Share, By Deployment Type (Cloud-Based SSP and On-Premisess SSP), By Ad Channel and Buying Method (Display Advertising, Video Advertising, Mobile Advertising, and Programmatic Advertising), By Organization Size (Small and Medium-Sized Businesses (SMBs) and Large Enterprises), By End Users (Retail and E-commerce, Media and Entertainment, Education, Travel and Tourism, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4537

Published

January 21, 2026

Pages

310 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

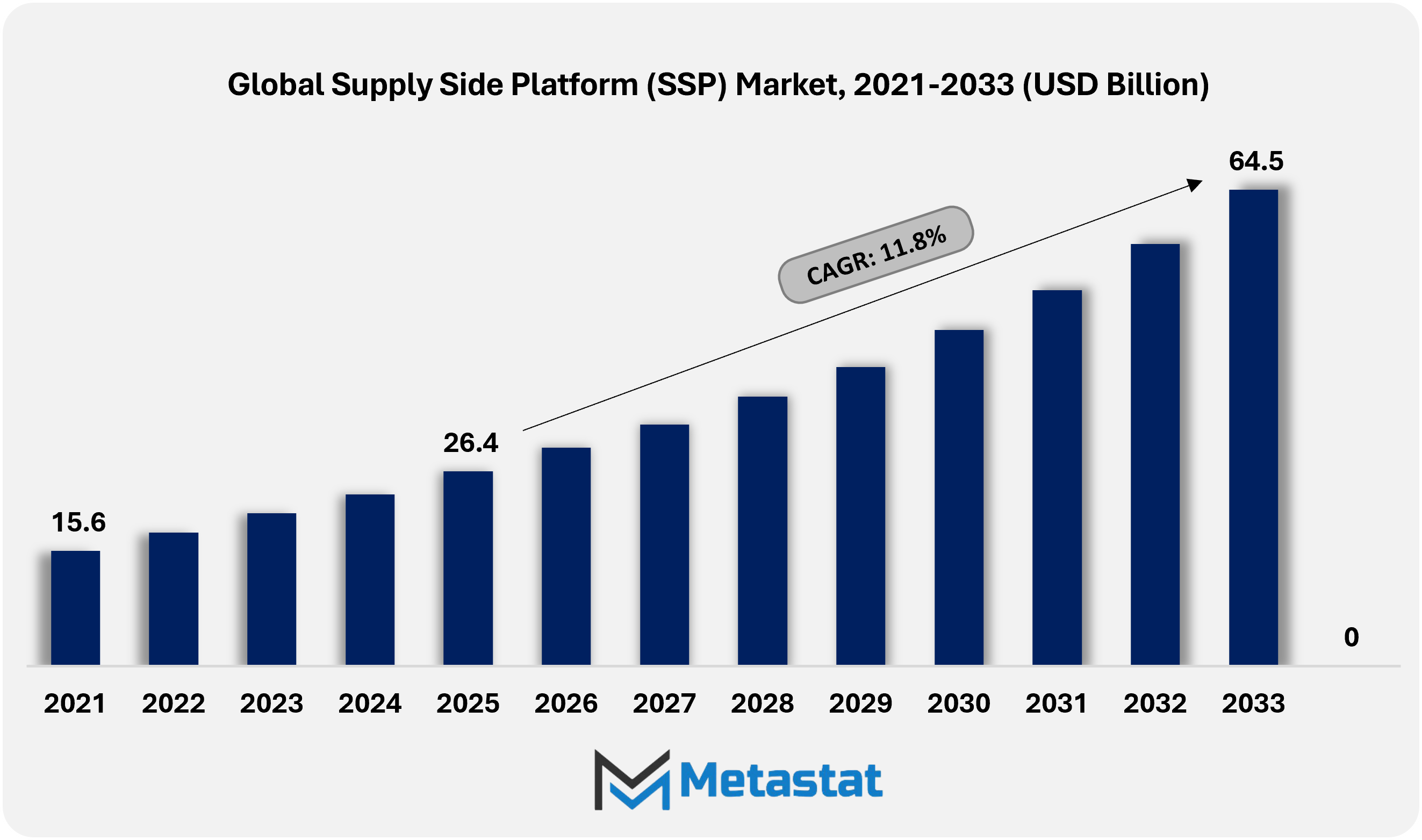

Global Supply Side Platform (SSP) market was valued at USD 26.4 billion in 2025 and is projected to expand at a CAGR of 11.8% from 2026 to 2033, reaching USD 64.5 billion by 2033.

Global Supply Side Platform (SSP) Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Supply Side Platform market valued at USD 26.4 billion in 2025, growing at a CAGR of around 11.8% through 2033, with potential to exceed USD 64.5 billion.

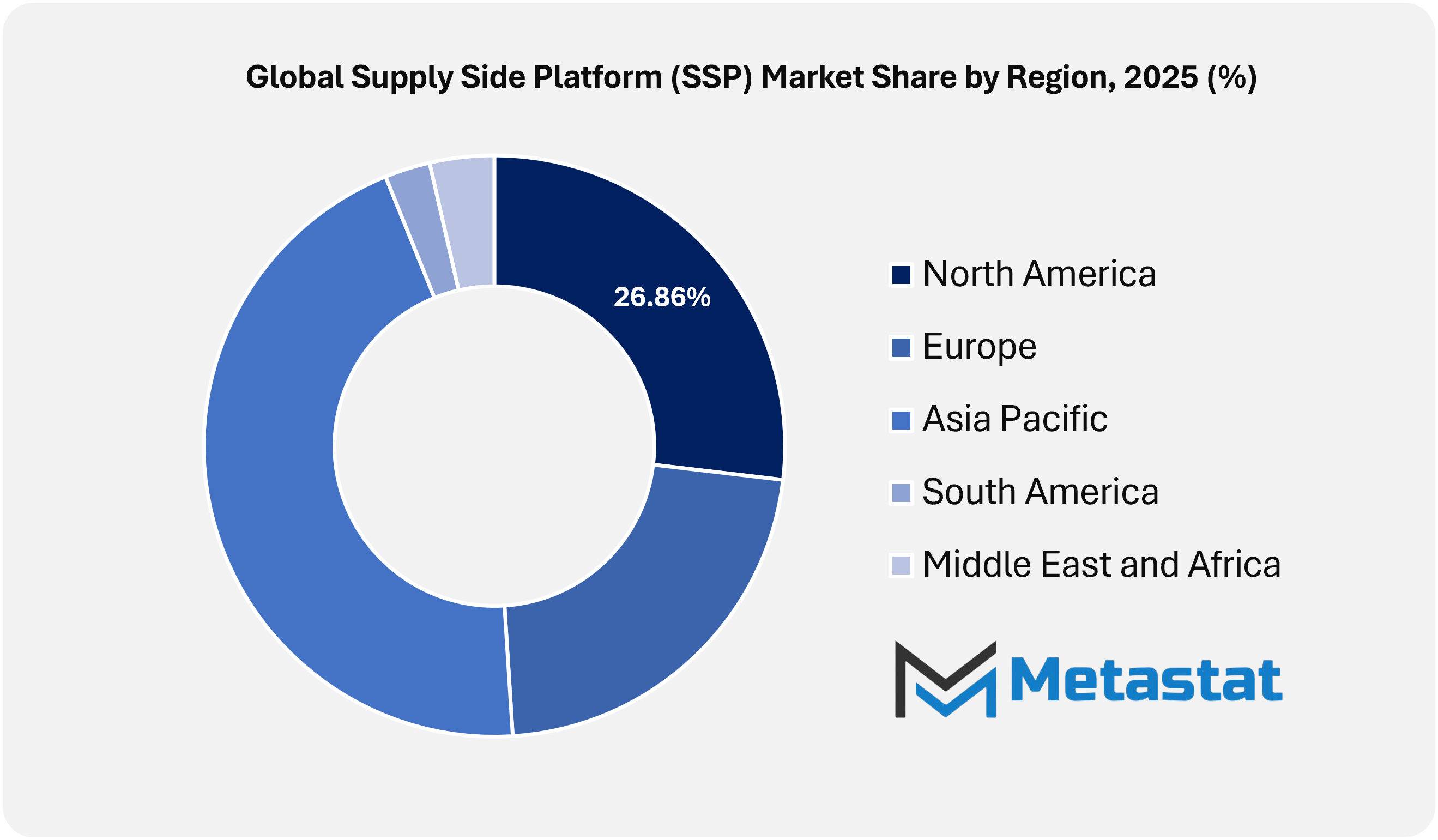

North America accounted for 26.9% of global revenue in 2025, led by the United States.

Cloud-Based SSP accounted for 69.4% market share in 2025, supported by faster onboarding, scalability, and continuous feature updates.

Key growth catalysts include accelerating programmatic ad buying, rising mobile-first consumption, and increased connected TV and video inventory.

Key opportunities include AI-enabled yield optimization, advanced analytics, first-party data monetization, expansion across high-growth emerging markets, and new inventory formats.

Key insight: Increasing regulatory emphasis on data privacy regulations such as GDPR and CCPA is reshaping the SSP landscape, compelling providers to enhance consent management, data security, and transparent auction practices, strengthening competitive advantages for compliant solutions.

The Global Supply Side Platform (SSP) Market will maintain to play a crucial position in how digital advertising inventory is controlled and monetized. SSPs permit publishers to attach advert space with more than one advertiser without delay, supporting stronger yield per impression. Publishers will rely on SSP systems to automate advert income and decrease guide attempt owing to increased consumption of digital content material across websites, cellular apps and related gadgets. SSPs support real-time bidding, so one can help publishers keep manage over pricing whilst improving transparency in transactions. The shift will make advert operations smoother and more efficient for media proprietors of all sizes.

Over time, the marketplace will see stronger consciousness on information use, emblem safety, and privateness-pleasant marketing techniques. With converting facts guidelines worldwide, SSP carriers will adapt their structures to assist consent-primarily based focused on and contextual marketing. The demand for unified platforms that can control display, video, cell, and linked TV inventory will also upward push, encouraging constant upgrades in platform abilities. Overall, the Global Supply Side Platform (SSP) Market will move ahead as a key aid gadget for publishers seeking to balance sales boom with user experience in and regulatory wishes.

Market Dynamics

Market Drivers:

Rapid Growth in Digital & Programmatic Advertising

The sustained international boom in virtual advertising spend and the large adoption of programmatic advertising are riding sturdy demand for SSPs that enable automated, real-time monetization of writer inventory, improving yield and operational performance. Programmatic transactions account for the substantial majority of digital ad spend as publishers increasingly seek tools that deliver automatic pricing, real-time bidding, and inventory optimization to maximize sales.

Expansion of Mobile and Connected Media Channels

The proliferation of mobile devices and the rapid growth of connected TV (CTV) and video streaming have multiplied the forms of advertising inventory that publishers can monetize, leading to widespread SSP adoption. With cell advertising and marketing expected to represent a widespread portion of overall virtual ad spend and CTV/video consumption rising sharply, SSPs tailored to these channels will supply new monetization avenues past conventional display commercials within the forecast period.

Market Restraints:

Stringent Data Privacy Regulations

Evolving privacy laws consisting of GDPR and CCPA, along with third-party cookies, are constraining SSP abilities by limited data collection, targeting techniques, user monitoring, increased compliance fees, and technical complexity. These regulatory changes require SSP companies to constantly adapt to new systems and invest in privacy-compliant alternatives such as contextual concentrated on or first-party information, which can slow innovation and adoption, particularly for smaller structures.

Complexity and Technical Barriers

The technical complexity of integrating SSPs within current ad tech stacks, mixed with the state-of-the-art programmatic environment, poses adoption challenges, especially for smaller publishers with constrained resources. Integrations throughout call for resources, the want to manipulate header bidding setups, and preserving optimal performance while balancing latency and sales objectives can deter adoption or boom operational fees.

Market Opportunities:

AI, Advanced Analytics & First-Party Data Monetization

The integration of artificial intelligence (AI), machine learning (ML), and advanced analytics into SSP solutions presents a significant growth opportunity by using permitting more desirable target market insights, predictive targeting, and optimized inventory pricing while assisting privacy-centric processes. Multiple SSP systems successfully leverage AI and first-party data and offer publishers & advertisers higher precision, higher yields, and compliance with privacy norms.

Expansion in Emerging Markets & New Inventory Formats

Emerging regions such as Asia Pacific, Latin America, and the Middle East & Africa, which are experiencing high speed internet and mobile ad adoption, constitute sizable growth runway for SSP providers. Localized SSP tailored to local demand, mixed with boom in non-traditional stock which includes OTT, in-app, and retail media networks will create new monetization channels that could extend usual market reach.

Market Segmentation Analysis

The global Supply Side Platform (SSP) market is classified based on Deployment Type, Ad Format, Organization Size, and End-Users.

By Deployment Type the market is further segmented into:

Cloud-Based SSP

Cloud-Based SSP is expected to grow at a CAGR of 12.3% from 2026 to 2033. Cloud-based deployment will benefit desire due to flexible get entry to, reduced infrastructure expenses, and quicker updates. Future adoption will rise as publishers prioritize scalability, faraway accessibility, and simplified integration with rising advertising and marketing equipment.

On-Premisess SSP

On-Premisess segment is expected to garner USD 18.38 billion by 2033. On-Premisess deployment will remain relevant among agencies disturbing better facts manipulate and inner customization. On-Premisess SSP segment will help strict compliance needs and internal protection policies. Long-time period utilization will depend on strong ad volumes and the ability to manage technical upkeep without operational disruption.

By Ad Format the market is divided into:

Display Advertising

Display Advertising segment holds 40% of the global SSP market in 2026. Display marketing will hold constant relevance over the visual brand placement throughout websites and programs. The display advertising format will guide focus-pushed campaigns and regular inventory usage. Advancements in focused accuracy will toughen overall performance measurement and beautify writer revenue predictability through the years.

Video Advertising

Video advertising will increase as digital video intake keeps increasing throughout structures at CAGR 12.4%. The segment will assist with immersive storytelling and higher engagement metrics. Future techniques will emphasize optimized load speeds, viewer retention, and monetization across short-form and lengthy-form content material environments.

Mobile Advertising

Mobile advertising segment holds USD 6.19 billion of the global SSP market in 2026. Mobile advertising and marketing will stay crucial owing to rising phone usage and app-based engagement. This phase will boost the region-aware shipping and responsive ad codecs. Increased demand will depend on seamless consumer revel and balanced advert frequency inside mobile ecosystems.

Programmatic Advertising

Programmatic advertising will dominate computerized ad transactions through data-driven pricing and placement. Market growth will rely on auctions, advanced fraud prevention, and delicate target market segmentation methods with the growth rate of 12.0%.

By Organization Size the market is further divided into:

Small and Medium-Sized Businesses (SMBs)

SMBs segment is expected to garner USD 36.75 billion by 2033. SMBs will undertake SSP solutions to maximize constrained inventory and improve revenue balance. Simplified dashboards and cost-effective deployment models will encourage participation.

Large Enterprises

Large enterprises segment is expected to grow at a CAGR of 11.2% from 2026 to 2033. Large enterprises will adopt superior SSP competencies for high-volume stock management. Custom integrations and deep analytics will assist strategic planning. Continued funding will create awareness on go-channel optimization and lengthy-time period monetization consistency.

By End-Users the global Supply Side Platform (SSP) market is divided as:

Retail & E-commerce

Retail and e-commerce segment holds USD 9.92 Billion of the global SSP market in 2026 end users will follow SSP to monetize high-visitor virtual storefronts. Personalized advert placements will beautify relevance. Growth will align with information-pushed vending and elevated digital buying conduct.

Media & Entertainment

Media and enjoyment platforms are expected to grow at a CAGR of 12.5% from 2026 to 2033 will rely upon SSP frameworks to control numerous content material inventories. Revenue optimization will support streaming, publishing, and virtual broadcasting models. Future growth will rely upon audience retention and adaptive ad codecs.

Education

The education segment is expected to garner USD 5.57 billion by 2033. Education systems will adopt SSP answers to help loose and occasional-cost content distribution. Expansion will align with virtual getting to know adoption throughout areas.

Travel & Tourism

Travel and tourism segments is expected to grow from USD 2.91 Billion in 2026 and will adopt to SSP tools to target purpose-driven audiences. Seasonal demand styles will affect ad techniques. Future increase will connect with virtual reserving traits and experiential content material merchandising.

Others

Other industries segment will combine SSP answers to explore opportunity sales streams. Others segment is expected to grow at a CAGR of 11.7% from 2026 to 2033. Niche virtual systems will advantage from controlled monetization systems. Adoption will rely on content material scale and advertiser alignment.

By Region:

Based on geography, the global Supply Side Platform (SSP) market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Supply Side Platform (SSP) Market is set to expand at a CAGR of 11.8% within the forecast period, reaching a market size (TAM) of USD 16.3 billion by the end of 2033.

Advanced Programmatic Advertising Infrastructure will propel the North American market for SSP Demand.

Strong Publisher Focus on Data Ownership in North America.

Asia Pacific will present strong opportunities as regional publishers increasingly monetize content material across cellular-first platforms.

Programmatic Adoption Beyond Tier-One in the Asia Pacific Markets

Across the Middle East, Africa, and South America, the Global Supply Side Platform (SSP) Market will replicate inconsistent, but meaningful progress formed via virtual infrastructure improvement. In these regions, SSP adoption will be stimulated less by way of superior automation and more via the need to organize fragmented virtual inventory. Growing cell penetration, local ad networks, and expanding nearby publisher ecosystems will progressively growth SSP relevance. Platforms that provide simplified onboarding, local compliance aid, and flexible pricing fashions will advantage traction, mainly among mid-sized publishers seeking structured monetization without immoderate technical overhead.

Competitive Landscape and Strategic Insights

Key players in the SSP market equip publishers with advanced monetization solutions, real-time bidding capabilities, and seamless integration across various demand sources. Google LLC and Amazon.com, Inc. As market leaders leverage a comprehensive ecosystem to deliver scalable SSP offerings supported by sophisticated analytics, cloud infrastructure and broad advertiser reach. These platforms enable publishers to increase yield through efficient impression management, optimized pricing strategies, and access to a broad demand pool, strengthening their leadership in programmatic advertising innovation.

In addition to the major players, established technology companies including Microsoft Corporation, Magnite, Inc. and OpenX Technologies Inc. Like specialized advertising technology providers, play a vital role in driving the growth of the market. These companies emphasize transparency, header bidding support, and integrated auction structures that help publishers improve revenue performance while maintaining ad quality and user experience. Their global presence, strong customer base and ongoing investment in machine learning-based optimization further strengthens their competitive position.

The competitors in the global SSP market include Google LLC, Amazon.com, Inc., Magnite Inc., Microsoft Corporation, OpenX Technologies Inc., PubMatic Inc., Index Exchange Inc., Smaato Inc., Sovrn Inc., SmartyAds Inc., FreeWheel Media Inc., InMobi, and Media.net Advertising FZ-LLC. Although all these players differ in their scale, expertise, and strategic focus, they define the programmatic advertising ecosystem together. Independent SSPs like PubMatic and Index Exchange forge publisher-centric value propositions, while companies like Smaato and Sovrn focus on mobile and developer-oriented monetization solutions. This competitive group of players jointly drives continuous improvement in auction efficiency, data integration, and cross-platform monetization.

SmartyAds Inc., Sovrn, Inc. and FreeWheel Media, Inc. are key strategically agile companies, including differentiate themselves through specific market focus and customized service offerings. For instance, FreeWheel leverages its expertise in premium video monetization, particularly across connected TV (CTV) and long-form content, to address the evolving needs of video-focused publishers..Meanwhile, InMobi and Media.Internet Advertising FZ-LLC liberate marketplace diversification via the inclusion of local demand, cell-first answers, and bendy yield-management abilities targeted on regional and emerging markets.

The key players are probably to hold strengthening their technological portfolios thru strategic partnerships, acquisitions, and improvements in AI-powered predictive analytics. Amidst converting privateness policies and patron expectations, SSP providers may additionally develop statistics governance, server-facet technologies, and cross-device optimization to maintain competitive facet and in the meantime empower publishers to achieve robust sales overall performance throughout the worldwide inventory channels.

Forecast and Future Outlook

Market size is forecast to rise from USD 26.4 billion in 2025 to over USD 64.5 billion by 2033.

Over time, the market has proven regular progress as programmatic advertising will become a standard exercise. Advertisers are increasingly adopting data-driven buying strategies, with SSPs supporting this transition through real-time bidding capabilities and enhanced audience targeting. This allows publishers advantage truthful fee for his or her stock at the same time as advertisers attain relevant users extra correctly. The attention is also moving in the direction of privateness-friendly answers, as structures adjust to information regulations and modifications in monitoring techniques. These modifications will affect how SSPs perform and how publishers plan their lengthy-term marketing strategies.

Supply Side Platform (SSP) Market Key Segments:

By Deployment Type:

Cloud-Based SSP

On-Premises SSP

By Ad Format / Ad Channel:

Display Advertising

Video Advertising

Mobile Advertising

Programmatic Advertising

By Organization Size:

Small and Medium-Sized Businesses (SMBs)

Large Enterprises

By End-Users:

Retail & E-commerce

Media & Entertainment

Education

Travel & Tourism

Others

Key Global Supply Side Platform (SSP) Industry Players

This research report categorizes the Supply Side Platform (SSP) market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Supply Side Platform (SSP) market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Supply Side Platform (SSP) market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 11.8% from 2026 to 2033

Revenue Unit

USD Million

Segmentation

By Deployment Type, Ad Format, Organization Size, End-Users, and Region

By Deployment Type

Cloud-Based SSP

On-Premise SSP

By Ad Format

Display Advertising

Video Advertising

Mobile Advertising

Programmatic Advertising

By Organization Size

Small and Medium-Sized Businesses (SMBs)

Large Enterprises

By End-Users

Retail & E-commerce

Media & Entertainment

Education

Travel & Tourism

Others

By Region

North America (By Deployment Type, Ad Format, Organization Size, End-Users, and Country)

United States

Canada

Mexico

Europe (By Deployment Type, Ad Format, Organization Size, End-Users, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of the Europe

Asia Pacific (By Deployment Type, Ad Format, Organization Size, End-Users, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Deployment Type, Ad Format, Organization Size, End-Users, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Deployment Type, Ad Format, Organization Size, End-Users, and Country)

New Zealand Optical Encryption Market Size, Share, Trends, 2033

New Zealand Optical Encryption market size is valued at USD 34.5 million in 2025 and is projected to reach USD 76.9 million in 2033, at a CAGR of 10.3% from 2026 to 2033.

New Zealand Optical Encryption Market, New Zealand Optical Encryption Market Size, New Zealand Optical Encryption Market Share, New Zealand Optical Encryption Market Analysis, New Zealand Optical Encryption Market Growth, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market Research Report, New Zealand Optical Encryption Market Forecast, New Zealand Optical Encryption, New Zealand Optical Encryption Market Research, New Zealand Optical Encryption Industry, New Zealand Optical Encryption Industry Report, New Zealand Optical Encryption Market Data, New Zealand Optical Encryption Statistics, New Zealand Optical Encryption Market Statistics, New Zealand Optical Encryption Industry Trends, New Zealand Optical Encryption Market Report, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market News, New Zealand Optical Encryption Forecasts, New Zealand Optical Encryption Market Intelligence Report

Generative AI in Analytics Market Size, Share, Trends, 2033

Generative AI in Analytics market size is valued at USD 1.6 billion in 2025 and is projected to reach USD 10.9 billion in 2033, at a CAGR of 26.8% from 2026 to 2033.

Generative AI in Analytics Market, Generative AI in Analytics Market Size, Generative AI in Analytics Market Share, Generative AI in Analytics Market Analysis, Generative AI in Analytics Market Growth, Generative AI in Analytics Market Trends, Generative AI in Analytics Market Research Report, Generative AI in Analytics Market Forecast, Generative AI in Analytics, Generative AI in Analytics Market Research, Generative AI in Analytics Industry, Generative AI in Analytics Industry Report, Generative AI in Analytics Market Data, Generative AI in Analytics Statistics, Generative AI in Analytics Market Statistics, Generative AI in Analytics Industry Trends, Generative AI in Analytics Market Report, Generative AI in Analytics Market Trends, Generative AI in Analytics Market News, Generative AI in Analytics Forecasts, Generative AI in Analytics Market Intelligence Report

Retail Project Management Software market size is valued at USD 1,505.5 million in 2025 and is projected to reach USD 3,524.9 million in 2033, at a CAGR of 11.2% from 2026 to 2033.

UK Immersive Entertainment & Experiential Property Market Size, Share, Trends, 2033

UK Immersive Entertainment & Experiential Property Market size is valued at USD 6.17 billion in 2025 and is projected to reach USD 26.16 billion in 2033, at a CAGR of 19.5% from 2026 to 2033

UK Immersive Entertainment & Experiential Property Market, UK Immersive Entertainment & Experiential Property Market Size, UK Immersive Entertainment & Experiential Property Market Share, UK Immersive Entertainment & Experiential Property Market Analysis, UK Immersive Entertainment & Experiential Property Market Growth, UK Immersive Entertainment & Experiential Property Market Trends, UK Immersive Entertainment & Experiential Property Market Research Report, UK Immersive Entertainment & Experiential Property Market Forecast, UK Immersive Entertainment & Experiential Property, UK Immersive Entertainment & Experiential Property Market Research, UK Immersive Entertainment & Experiential Property Industry, UK Immersive Entertainment & Experiential Property Industry Report, UK Immersive Entertainment & Experiential Property Market Data, UK Immersive Entertainment & Experiential Property Statistics, UK Immersive Entertainment & Experiential Property Market Statistics, UK Immersive Entertainment & Experiential Property Industry Trends, UK Immersive Entertainment & Experiential Property Market Report, UK Immersive Entertainment & Experiential Property Market Trends, UK Immersive Entertainment & Experiential Property Market News, UK Immersive Entertainment & Experiential Property Forecasts, UK Immersive Entertainment & Experiential Property Market Intelligence Report