US Data Center Design-Build Infrastructure Services Market

United States Data Center Design-Build & Infrastructure Services Market Size, Share, By Service Type, By Design & Engineering Type, By Build & Delivery Type, By Power & Cooling Infrastructure Type, Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4544

Published

February 7, 2026

Pages

320 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

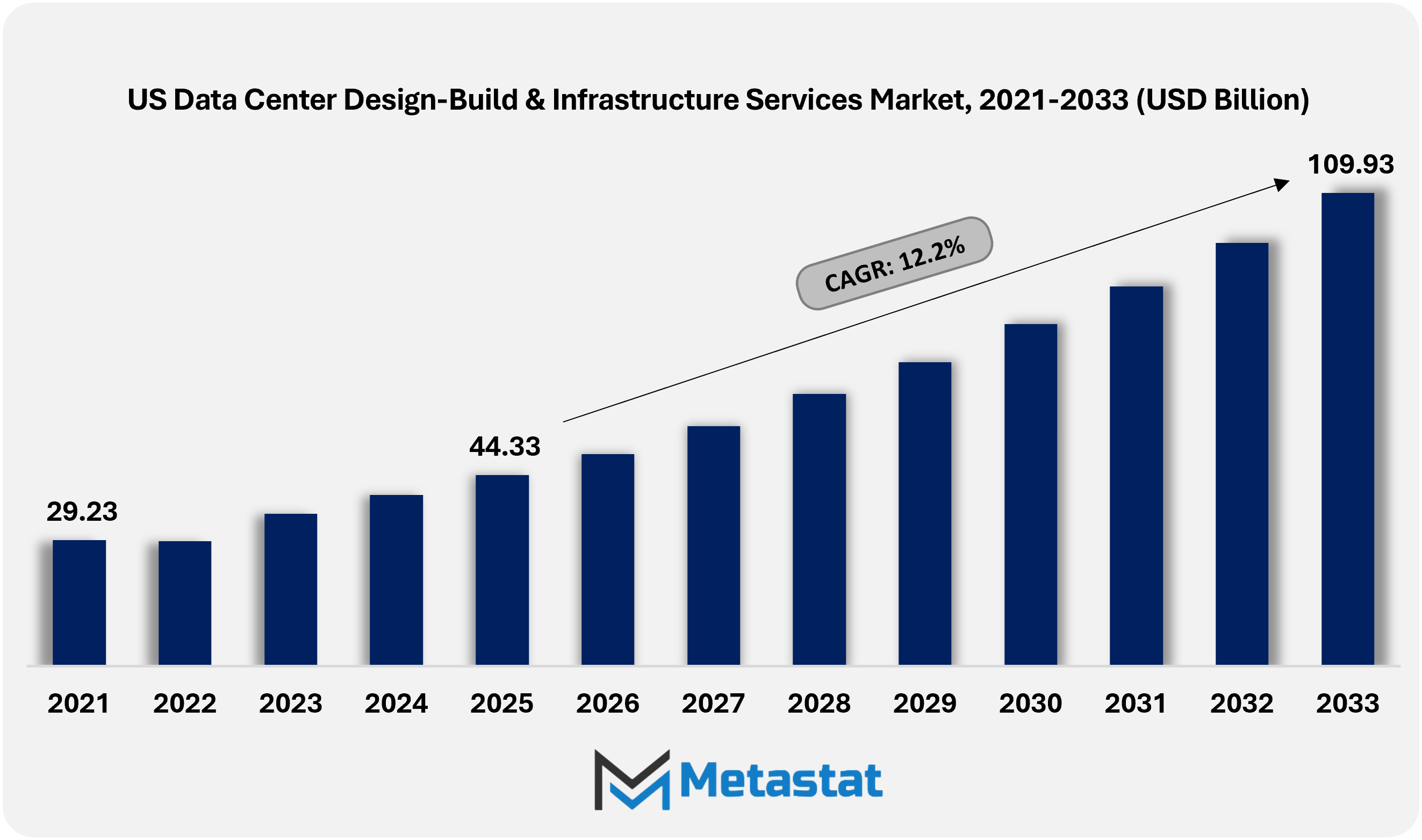

The United States Data Center Design-Build & Infrastructure Services market size was valued at USD 44.3 billion in 2025. The market is projected to grow from USD 49.2 billion in 2026 to USD 109.9 billion by 2033, exhibiting a CAGR of 12.2% during the forecast period.

United States Data Center Design-Build & Infrastructure Services Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

United States Data Center Design-Build & Infrastructure Services market was valued at USD 44.3 billion in 2025 and is projected to grow at a CAGR of 12.2% through 2033, reaching USD 109.9 billion.

Design & Engineering segment accounts for a market share of 16.6% in 2025, supporting standardized delivery, performance-focused design, and scalable infrastructure programs.

Key trends driving growth include hyperscale and AI/ML workload surge (GPU-dense designs) accelerating capacity additions and high-density buildouts. Enterprise cloud and edge adoption, paired with low-latency use cases, is driving new builds and brownfield expansions across Tier II and Tier III metros.

Opportunities include sustainability-led retrofits such as liquid cooling, heat reuse, and on-site renewables or microgrids to meet ESG targets and reduce TCO.

Key insight: Integrated design-build models are increasingly shaping how data center infrastructure is planned, delivered, and scaled across the United States.

The United States data center design-build and infrastructure services market within the digital infrastructure and construction services industry will extend beyond traditional facility delivery and align with national priorities tied to data sovereignty, energy resilience, and advanced automation.

The market will increase its focus toward integrated ecosystems where physical infrastructure is planned alongside software-defined operations, predictive maintenance frameworks, and long-term adaptability to emerging computing architectures.

Future projects will not be limited to hyperscale or colocation environments and will support decentralized data delivery models, including deployments located near industrial corridors, defense installations, and smart city zones. Design-build strategies will anticipate faster retrofitting cycles, allowing facilities to absorb changes in chip density, cooling logic, and power routing without disruptive reconfiguration. The forward-looking orientation will encourage service providers to embed modular engineering philosophy that will shorten redevelopment timelines while preserving asset value.

Market Dynamics

Growth Drivers:

Hyperscale and AI/ML workload surge (GPU-dense designs) accelerating capacity additions and high-density buildouts.

Hyperscale expansion associated with artificial intelligence and machine learning workloads is shaping future-ready facilities. GPU-intensive layouts will require advanced cooling, flexible power paths, and modular construction. The United States data center design-build and infrastructure services market will see rapid capacity rollouts focused on efficiency, scalability, and long-term performance sustainability.

Enterprise cloud/edge adoption and low latency use cases driving new builds and brownfield expansions across Tier II/III metros.

Enterprise cloud migration and edge computing growth will continue to influence new features and upgrades. Low-latency requirements in Tier II and Tier III metros will support regional construction activity. The United States data center design-build and infrastructure services market will benefit from adaptive designs that support hybrid operations and distributed infrastructure planning.

Restraints and Challenges:

Power and land constraints, including interconnection queues, substation lead times, and zoning hurdles, delay projects and raise costs.

Availability of electricity and access to land continue to be limiting elements. Interconnection backlogs, extended substation timelines, and zoning approvals slow execution and increase development costs. The United States data center design-build and infrastructure services market faces pressure to align project schedules with utility readiness and municipal planning frameworks.

Supply-chain and skilled-labor bottlenecks, such as transformer and switchgear lead times and specialized trades availability, elongate delivery cycles.

Supply-chain disruptions and limited skilled labor pools are extending delivery timelines. Long lead times for transformers and switchgear, paired with shortages across specialized trades, will impact construction sequencing. The United States data center design-build and infrastructure services market will require early procurement strategies and workforce development to minimize project delays.

Sustainability-led upgrades provide attractive growth opportunities. Liquid cooling systems, heat recovery solutions, and on-site renewable energy integration will support ESG targets and reduce operating costs. The United States data center design-build and infrastructure services market will benefit from retrofits that balance efficiency, compliance, and long-term cost control.

Market Segmentation Analysis

The United States Data Center Design-Build & Infrastructure Services market is classified by Service Type, Design & Engineering Type, Build & Delivery Type, and Power & Cooling Infrastructure Type.

By Service Type, the market is further segmented into:

Design & Engineering

Design & Engineering segment is valued at USD 8.2 billion in 2026 and is projected to reach USD 18.5 billion by 2033, at a CAGR of 12.4% during the forecast period.

Design and engineering services will shape how digital infrastructure is designed and developed within the United States. Long-term capacity planning, energy forecasting, and design optimization will lead facilities to greater levels of efficiency. Model-based design and compliance-oriented design will provide facilities that are scalable and less prone to redesigns with the rising data demands.

Build & Delivery

Build & Delivery segment is valued at USD 17 billion in 2026 and is projected to reach USD 36.4 billion by 2033, at a CAGR of 11.5% during the forecast period.

Build and delivery efforts will cover the pursuits of speed, precision, and integration as project schedules continue to compress. Build methodologies will use parallel workstreams to enable faster handoffs, supporting reliability, safety, and predictability amid growing cloud, enterprise, and edge computing requirements.

Power & Cooling Infrastructure

Power & Cooling Infrastructure segment is valued at USD 14.1 billion in 2026 and is projected to reach USD 31.9 billion by 2033, at a CAGR of 12.4% during the forecast period.

Infrastructure for power and cooling is expected to emerge as a crucial part of operational reliability. Data centers will implement robust electrical designs and efficient cooling systems to manage higher per-rack power density. Power usage effectiveness targets will shape infrastructure design choices.

Digital & Controls (DCIM & Monitoring Software)

Digital & Controls (DCIM & Monitoring Software) segment is valued at USD 4.9 billion in 2026 and is projected to reach USD 11.9 billion by 2033, at a CAGR of 13.5% during the forecast period.

Digital control and monitoring platforms will advance intelligent facility management. Real-time visibility into performance metrics will allow proactive decision making. Automation and analytics will support uptime goals, cost control and predictive maintenance, creating data centers that respond dynamically to operating conditions.

Quality & Operations (Commissioning & QA/QC)

Quality & Operations (Commissioning & QA/QC) segment is valued at USD 3 billion in 2026 and is projected to reach USD 6.8 billion by 2033, at a CAGR of 12.4% during the forecast period.

Quality and operations services will ensure performance consistency from deployment through live operation. Rigorous commissioning procedures will validate the system prior to activation. Ongoing QA/QC activities will help facilities maintain reliability standards while adopting technology upgrades and evolving workload profiles.

Others (Security Integration, Sustainability Consulting, Workplace Integration) segment is valued at USD 2 billion in 2026 and is projected to reach USD 4.4 billion by 2033, at a CAGR of 11.9% during the forecast period.

Additional services will address security, sustainability and workforce integration needs. Physical and digital security frameworks will strengthen asset protection. Sustainability consulting will guide energy and water optimization, while workplace planning will support operational teams managing increasingly complex environments.

By Design & Engineering Type the market is divided into:

Program Design

Program Design segment is projected to reach USD 8 billion by 2033, at a CAGR of 12.6% during the forecast period.

Program design will offer more organized frameworks for multi-site development projects. A set of organized design concepts will facilitate uniformity with regional modifications. Long-term strategic planning can enable organizations to direct financial spending according to future capacity demand in multi-site data centers.

A/E and Consulting

A/E & Consulting segment is projected to reach USD 7.1 billion by 2033, at a CAGR of 12.3% during the forecast period.

Consulting in terms of architecture and engineering will inform decisions in terms of technical and regulatory issues. The services will include the aspect of risk mitigation and optimization for performance. The consultation will aid in making decisions concerning complex designs while ensuring readiness for future growth.

Others (Site Selection Advisory, Cost Estimation & Budgeting, Specialized Design Services) segment is projected to reach USD 3.4 billion by 2033, at a CAGR of 12% during the forecast period.

Expert design capabilities are available for informed decision-making during early-phase planning. Analysis for site selection will consider power, climate, and connectivity considerations. Cost analysis and budgeting will augment financial certainty, helping to boost investment confidence as size increases for infrastructure investment.

By Build & Delivery Type the market is further divided into:

EPC/General Contractor

EPC/General Contractors segment is projected to reach USD 8.1 billion by 2033 and accounted for a share of 23.2% in 2025.

EPC and general contracting services will provide integrated execution across construction phases. Centralized responsibility models will reduce coordination gaps and schedule delays. Project size and technical complexity are increasing, and turnkey accountability will remain important.

Turnkey MEP/Electrical Contractors

Turnkey MEP/Electrical Contractors segment is projected to reach USD 8.2 billion by 2033 with a share of 22.4% in 2025.

Turnkey MEPs and electrical contractors will manage critical system installations with precision. Expertise in power distribution, mechanical systems and controls will support seamless deployment. There will be increased demand for contractors capable of providing a full operational environment on accelerated timelines.

Modular & Prefabricated Systems

Modular & Prefabricated Systems segment is projected to reach USD 7.1 billion by 2033 with a share of 18.6% in 2025.

Modular and prefab systems will be adopted because of the speed and quality control benefits. Off-site manufacturing will reduce construction risk and labor dependency. Standardized modules will support rapid scaling while maintaining consistent performance benchmarks.

Racks, Containment & Fit Out

Racks, Containment & Fit Out segment is projected to reach USD 5.8 billion by 2033 with a share of 15.4% in 2025.

Rack systems and containment strategies will evolve to support higher power density requirements. Airflow design will see improvements in cooling performance. Fit-out services are likely to promote flexibility, with easy reconfigurability based on developments in hardware technologies.

Structured Cabling & Connectivity

Structured Cabling & Connectivity segment is projected to reach USD 4.5 billion by 2033 with a share of 12.3% in 2025.

Connectivity and cabling services will support high-speed data transfer. The new facilities would require well-structured cabling. The connectivity structures would continue to be a fundamental requirement for the new facilities.

Others (Logistics Management, Site Remediation & Preparation, Specialized Installation Services)

Others (Logistics Management, Site Remediation & Preparation, Specialized Installation Services) segment is projected to reach USD 2.7 billion by 2033 with a share of 8% in 2025.

Support services will include site readiness, material coordination, and logistics management to optimize equipment delivery. Site remediation, preparation, and specialized installation services will enable construction-ready sites and reliable installation of complex systems.

By Power & Cooling Infrastructure Type the United States Data Center Design-Build & Infrastructure Services market is divided as:

Critical Power Train (UPS, Switchgear, PDUs)

Critical Power Train (UPS, Switchgear, PDUs) segment is projected to grow at a CAGR of 12.8% during the forecast period.

Critical power systems remain central to uptime integrity. UPS technology, smart switchgear, and PDU efficiency are integral in providing stable power distribution. Redundancy in planning covers increased sensitivity in operational risk.

Thermal Management (Air & Liquid Cooling)

Thermal Management (Air & Liquid Cooling) segment is projected to grow at a CAGR of 12.6% during the forecast period.

Thermal management technologies also are projected to evolve to handle the ever-increasing heat loads. Air and liquid cooling technologies will be selected based on rack density and efficiency requirements.

Back-Up Generation & Energy

Back-Up Generation & Energy segment is projected to grow at a CAGR of 11.8% during the forecast period.

The backup power generation systems will also support resilience for when there are disruptions in power generation. The energy strategies for these buildings will highlight fuel efficiency as well as emissions mitigation. Flexible power generation technologies will support facility continuity.

Grid Interconnect and HV Equipment

Grid Interconnect & HV Equipment segment is projected to grow at a CAGR of 12.7% during the forecast period.

Grid interconnection services will manage high-voltage integration challenges. Coordination with utilities will become more complex as electricity demand increases. Robust HV equipment will support stable energy flows and long-term capacity planning.

Water Treatment and Cooling Water Systems

Water Treatment & Cooling Water Systems segment is projected to grow at a CAGR of 11.8% during the forecast period.

Water treatment and cooling systems will prioritize conservation and efficiency. Improved filtration and reuse strategies will reduce resource dependence. Facilities will adopt better water management approaches to support sustainable operations.

Others (Energy Storage Systems, Heat Reuse Systems, Microgrid Integration) segment is projected to grow at a CAGR of 10.4% during the forecast period.

Emerging infrastructure solutions will support energy flexibility. Storage systems will stabilize supply, heat reuse will improve efficiency, and microgrid integration will increase energy independence. Such innovations will influence future planning in the United States data center design-build and infrastructure services market.

Competitive Landscape and Strategic Insights

The Data Center Design-Build & Infrastructure Services market in the United States has experienced steady growth, supported by rising needs for secure, dependable, and high-capacity digital infrastructure. Data centers are no longer viewed as basic infrastructure and are increasingly treated as strategic resources supporting cloud infrastructure, Artificial Intelligence, financial services, healthcare information systems, and government operations. To address increasing consumption, companies will continue to invest in more advanced Design Build strategies targeting efficiency, scalability, as well as long-term operational resilience, making this an attractive sector for specialists with knowledge of complex infrastructure services.

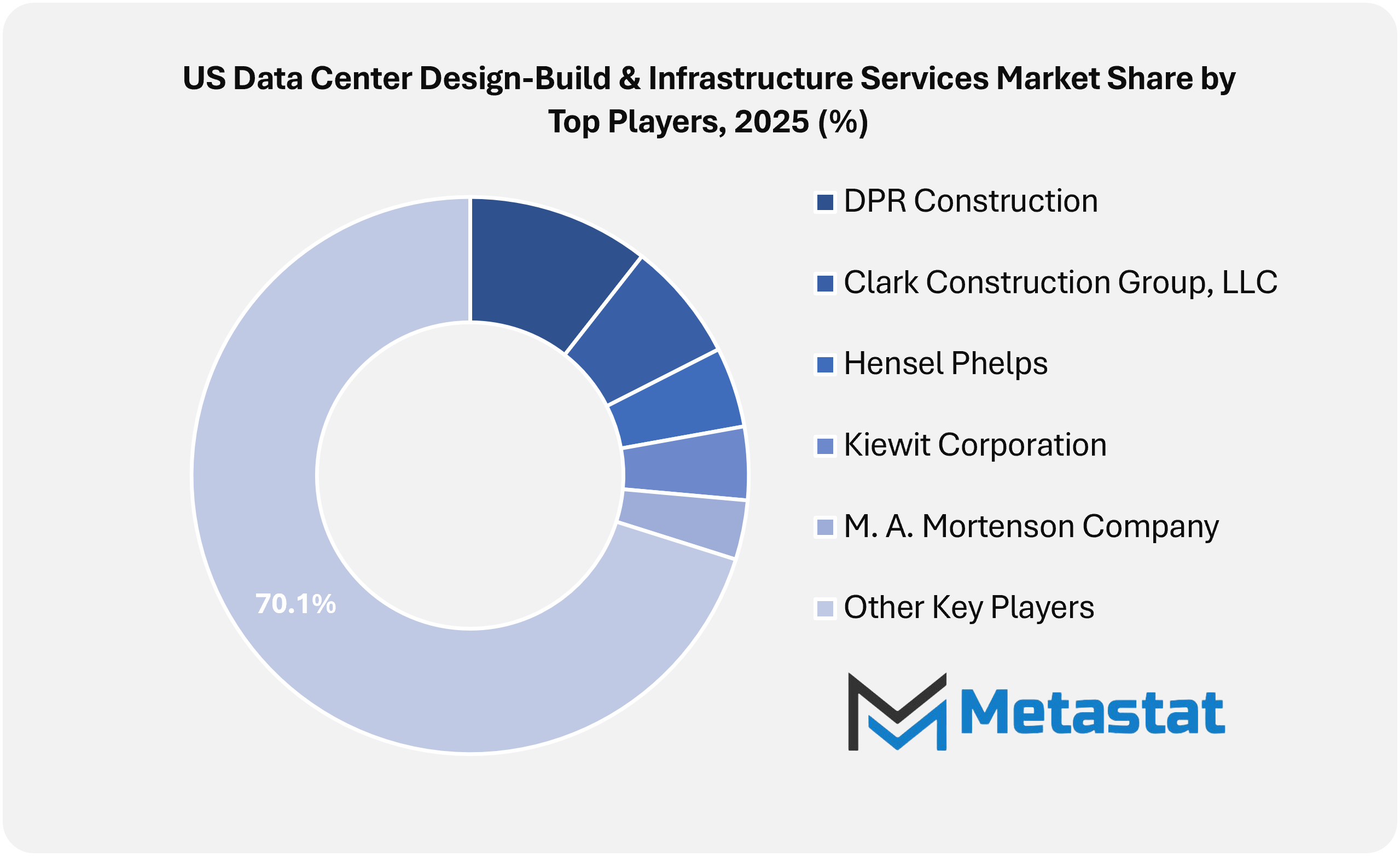

Several well-established construction companies are playing a crucial role in determining the market for such projects through the execution of customized data center projects across the nation. DPR Construction, Clark Construction Group, LLC, M. A. Mortenson Company, Holder Construction Group, and Hensel Phelps Construction Company are some of the major market players who have been able to create a name through their experience in handling complex projects such as data centers. These market players often combine design, construction, and project management, reducing coordination gaps, delays, and cost overruns.

Specialist electrical, mechanical, and infrastructure contractors also hold strong influence in this sector. Their contribution to data center projects includes specialized knowledge for construction and engineering. On the other hand, companies whose main emphasis is on power distribution, cooling, or managing energy include Rosendin Electric, Inc., M.C. Dean, Inc., Cupertino Electric, Inc., Faith Technologies Incorporated (FTI), and Southland Industries. Their services are also critical, as data center operations demand continuous power supply as well as controlled conditions to run efficiently.

Altogether, these companies play an important role in creating a competitive arena in which the aspects of reliability and competency are most valued. Together, these companies shall play an important role in the development of future data centers with adequate capacity for the data in addition to adherence to stricter regulations set by authorities. With increased online operations by organizations, these companies shall continue to play an important role in creating future capacity while maintaining operational control.

Forecast and Future Outlook

Market size is forecast to rise from USD 44.3 billion in 2025 to over USD 109.9 billion by 2033.

The United States data center design-build and infrastructure services market will also be more closely aligned with utilization planning, advanced materials science, and secure supply chain coordination. Collaboration with energy producers, semiconductor logistics partners and local authorities will shape how future facilities will be conceived and approved. The convergence will place the market at the center of long-term national digital readiness, establishing it as the foundation of innovation that will extend well beyond traditional data center boundaries.

Data Center Design-Build & Infrastructure Services Market Key Segments:

This research report categorizes the Data Center Design-Build & Infrastructure Services market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyzes the key growth drivers, opportunities, and challenges influencing the Data Center Design-Build & Infrastructure Services market. Recent market developments and competitive strategies such as expansion, service launch, product development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Data Center Design-Build & Infrastructure Services market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 12.2% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Service Type, Design & Engineering Type, Build & Delivery Type, Power & Cooling Infrastructure Type, and Region

New Zealand Optical Encryption Market Size, Share, Trends, 2033

New Zealand Optical Encryption market size is valued at USD 34.5 million in 2025 and is projected to reach USD 76.9 million in 2033, at a CAGR of 10.3% from 2026 to 2033.

New Zealand Optical Encryption Market, New Zealand Optical Encryption Market Size, New Zealand Optical Encryption Market Share, New Zealand Optical Encryption Market Analysis, New Zealand Optical Encryption Market Growth, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market Research Report, New Zealand Optical Encryption Market Forecast, New Zealand Optical Encryption, New Zealand Optical Encryption Market Research, New Zealand Optical Encryption Industry, New Zealand Optical Encryption Industry Report, New Zealand Optical Encryption Market Data, New Zealand Optical Encryption Statistics, New Zealand Optical Encryption Market Statistics, New Zealand Optical Encryption Industry Trends, New Zealand Optical Encryption Market Report, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market News, New Zealand Optical Encryption Forecasts, New Zealand Optical Encryption Market Intelligence Report

Generative AI in Analytics Market Size, Share, Trends, 2033

Generative AI in Analytics market size is valued at USD 1.6 billion in 2025 and is projected to reach USD 10.9 billion in 2033, at a CAGR of 26.8% from 2026 to 2033.

Generative AI in Analytics Market, Generative AI in Analytics Market Size, Generative AI in Analytics Market Share, Generative AI in Analytics Market Analysis, Generative AI in Analytics Market Growth, Generative AI in Analytics Market Trends, Generative AI in Analytics Market Research Report, Generative AI in Analytics Market Forecast, Generative AI in Analytics, Generative AI in Analytics Market Research, Generative AI in Analytics Industry, Generative AI in Analytics Industry Report, Generative AI in Analytics Market Data, Generative AI in Analytics Statistics, Generative AI in Analytics Market Statistics, Generative AI in Analytics Industry Trends, Generative AI in Analytics Market Report, Generative AI in Analytics Market Trends, Generative AI in Analytics Market News, Generative AI in Analytics Forecasts, Generative AI in Analytics Market Intelligence Report

Retail Project Management Software market size is valued at USD 1,505.5 million in 2025 and is projected to reach USD 3,524.9 million in 2033, at a CAGR of 11.2% from 2026 to 2033.

UK Immersive Entertainment & Experiential Property Market Size, Share, Trends, 2033

UK Immersive Entertainment & Experiential Property Market size is valued at USD 6.17 billion in 2025 and is projected to reach USD 26.16 billion in 2033, at a CAGR of 19.5% from 2026 to 2033

UK Immersive Entertainment & Experiential Property Market, UK Immersive Entertainment & Experiential Property Market Size, UK Immersive Entertainment & Experiential Property Market Share, UK Immersive Entertainment & Experiential Property Market Analysis, UK Immersive Entertainment & Experiential Property Market Growth, UK Immersive Entertainment & Experiential Property Market Trends, UK Immersive Entertainment & Experiential Property Market Research Report, UK Immersive Entertainment & Experiential Property Market Forecast, UK Immersive Entertainment & Experiential Property, UK Immersive Entertainment & Experiential Property Market Research, UK Immersive Entertainment & Experiential Property Industry, UK Immersive Entertainment & Experiential Property Industry Report, UK Immersive Entertainment & Experiential Property Market Data, UK Immersive Entertainment & Experiential Property Statistics, UK Immersive Entertainment & Experiential Property Market Statistics, UK Immersive Entertainment & Experiential Property Industry Trends, UK Immersive Entertainment & Experiential Property Market Report, UK Immersive Entertainment & Experiential Property Market Trends, UK Immersive Entertainment & Experiential Property Market News, UK Immersive Entertainment & Experiential Property Forecasts, UK Immersive Entertainment & Experiential Property Market Intelligence Report