Affordable Housing Finance Market Size, Share, By Type (Affordable Homeownership Mortgages, Subsidized Mortgage Programs, Down Payment Assistance Loans, Affordable Rental Housing Construction Loans, Affordable Housing Projects Bridge Loans, Micro-mortgages, Incremental Housing Loans, and Others), By Lender Type (Public Sector Banks, Private Banks, Housing Finance Companies, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4706

Published

April 30, 2026

Pages

315 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

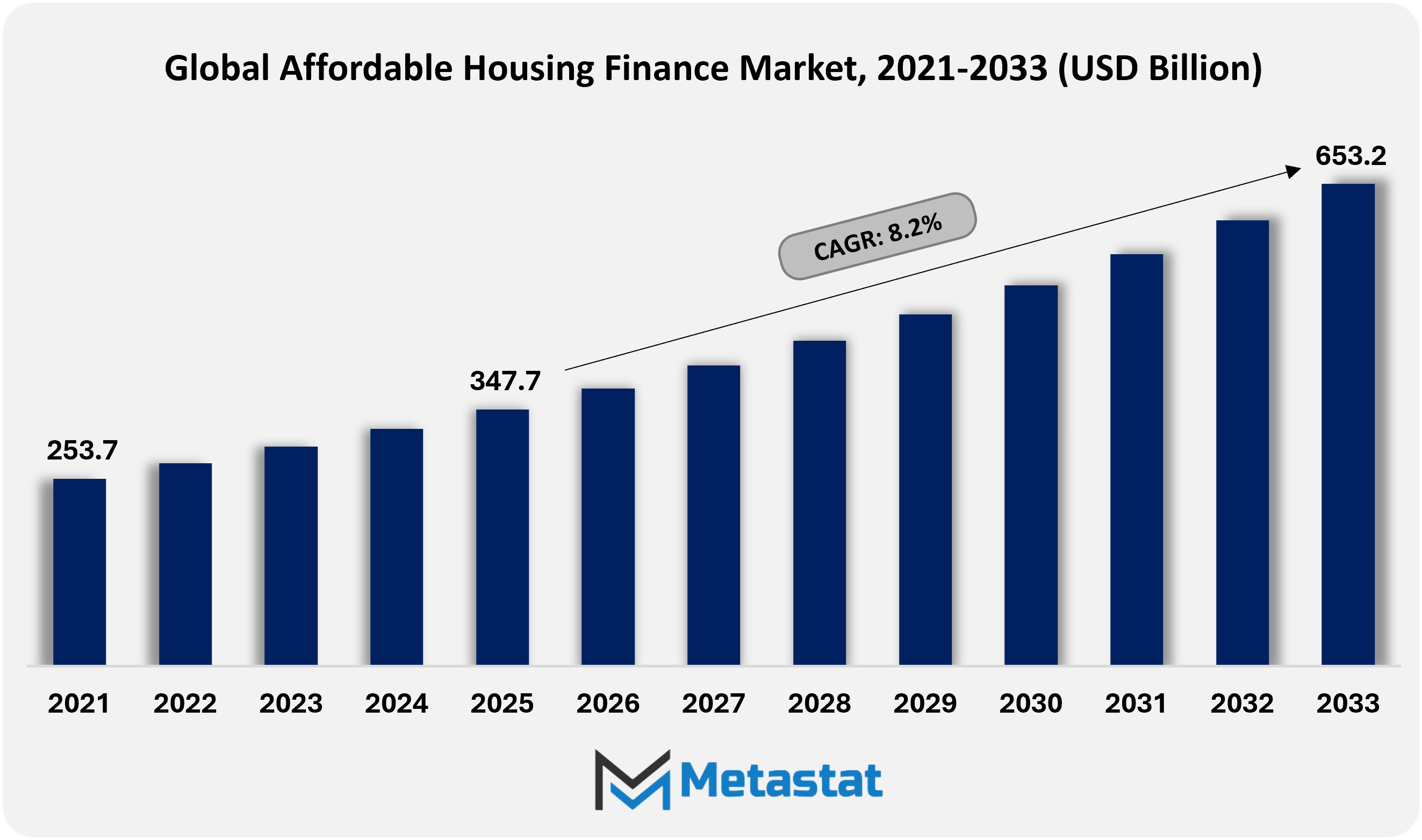

The Global Affordable Housing Finance market size was valued at USD 347.7 billion in 2025 and projected to grow at a CAGR of 8.2% during the forecast period, reaching USD 653.2 billion by 2033.

Global Affordable Housing Finance Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

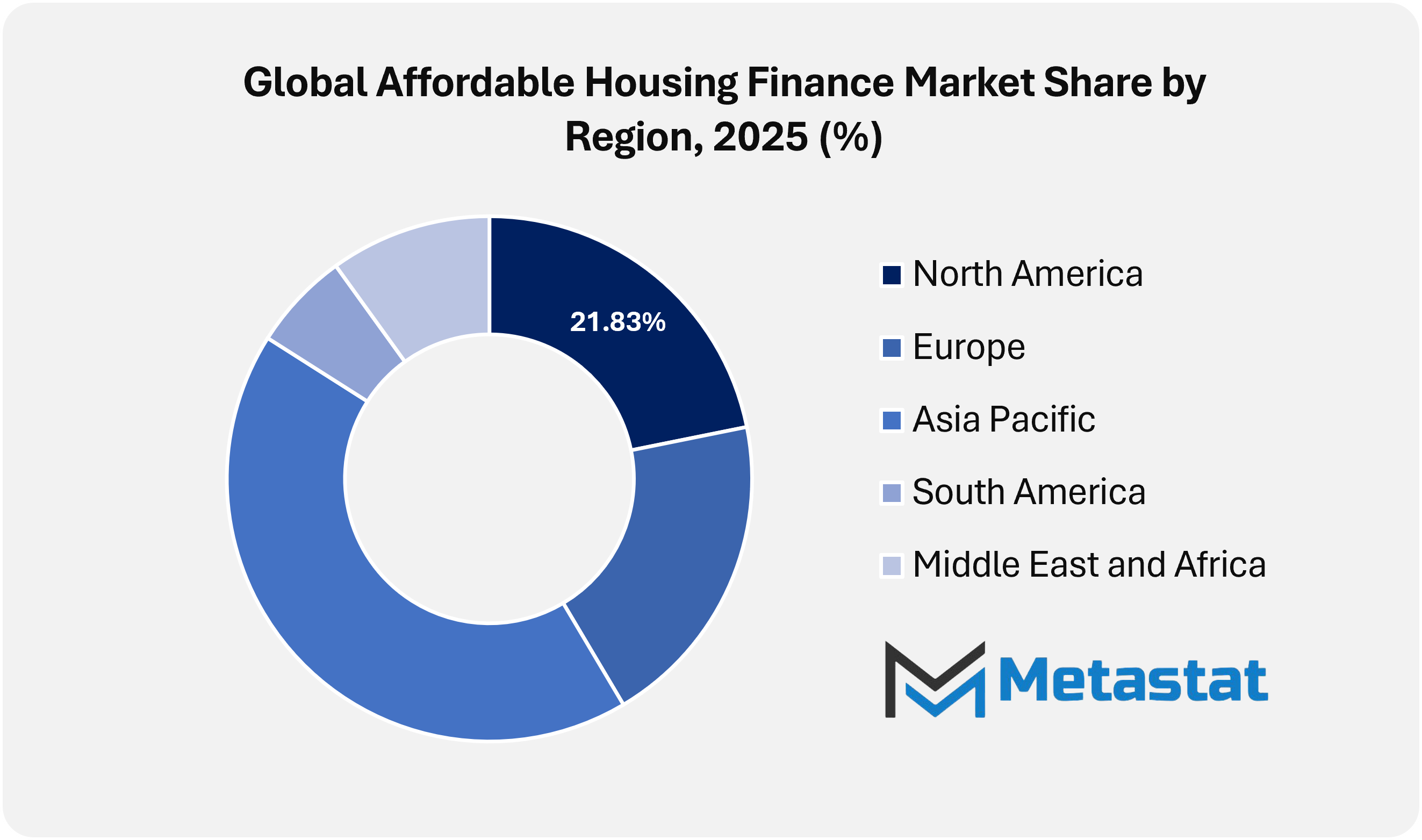

North America held a 21.8% market share in 2025, with the U.S. accounting for the leading share within the region.

The Affordable Homeownership Mortgages segment accounted for a 47.3% market share in 2025.

Key trends driving growth: Rapid urbanization and migration toward tier I and tier II cities increasing demand for low-cost housing finance solutions and government-backed subsidy schemes and priority sector lending norms strengthening institutional lending penetration.

Opportunities include fintech-led credit assessment models enabling inclusion of underserved borrowers with thin credit files.

Key insight: Expanding urban populations and policy-backed credit expansion accelerate growth across Global Affordable Housing Finance Market.

The Global Affordable Housing Finance Market within the housing finance industry is moving beyond traditional lending models toward a structure shaped by regulatory support, digital underwriting, blended capital strategies, and inclusive credit delivery. Over the coming years, financial institutions will expand their focus from urban low-income households toward informal workers, migrant populations, and climate-vulnerable communities that remain underserved by conventional mortgage channels. Loan products will be designed with adaptive repayment cycles aligned with seasonal income, gig-based earnings, and microenterprise cash flows.

Capital structures will increasingly combine social impact bonds, green housing credit lines, and multilateral guarantee frameworks to reduce perceived credit risk. Data analytics will refine borrower profiling through alternative credit scoring models that assess utility payments, rental histories, and digital transaction trails. Such systems will improve credit visibility for applicants outside formal payroll systems. Technology-driven appraisal tools will streamline property validation across peri-urban locations and tier II and tier III cities, where documentation gaps have historically restricted financing access.

Market Dynamics

Growth Drivers:

Rapid urbanization and migration toward tier I and tier II cities increasing demand for low-cost housing finance solutions.

Accelerated population movement toward tier I and tier II cities will intensify pressure on urban housing supply. Expanding employment corridors, infrastructure upgrades, and industrial clusters will attract first-time homebuyers seeking structured financing. Financial institutions in the Affordable Housing Finance Market will expand tailored products with flexible tenures and risk-adjusted pricing to meet rising demand for affordable home loans.

Supportive public policies will continue to channel formal credit toward economically weaker sections and low-income households. Interest subvention programs and regulatory mandates under priority sector frameworks will widen participation of banks and housing finance companies. Greater institutional penetration within the Affordable Housing Finance Market will improve credit access, standardize underwriting practices, and reduce dependency on informal borrowing channels.

Restraints and Challenges:

High credit risk linked to informal income segments limiting lender confidence.

Large borrower segments depending on informal or seasonal income streams will present assessment challenges. Limited income documentation and cash-based transactions will increase perceived default risk. Risk aversion among lenders operating in the Affordable Housing Finance Market will constrain portfolio expansion, encouraging conservative underwriting norms and stricter eligibility benchmarks for economically vulnerable applicants.

Rising interest rates increasing borrowing costs for low-income households.

Tightening monetary cycles will raise funding costs for financial institutions, leading to higher lending rates. Increased equated monthly installments will pressure the repayment capacity of low-income borrowers. The increases in sustained interest rate will moderate loan disbursement volumes and will delay purchase decisions among first-generation homeowners within the Affordable Housing Finance Market.

Opportunities:

Fintech-led credit assessment models enabling inclusion of underserved borrowers with thin credit files.

Advanced analytics, alternative data scoring, and digital verification tools will transform borrower assessment methods. Fintech integration will support real-time income estimation, behavioral assessment, and automated approval systems. Such innovation will expand borrower inclusion in the Affordable Housing Finance Market, strengthening outreach to individuals lacking formal credit histories while maintaining portfolio discipline.

Market Segmentation Analysis

The Global Affordable Housing Finance market is classified based on Type and Lender Type.

Affordable Homeownership Mortgages segment is estimated at USD 178.1 billion in 2026 and is projected to reach USD 288.1 billion by 2033, at a CAGR of 7.1% during the forecast period.

Affordable Homeownership Mortgages will support access to property ownership for middle- and lower-income households across urban and semi-urban areas. Structured repayment plans, flexible tenures, and digital credit assessments will enhance approval efficiency. The Global Affordable Housing Finance Market will witness structured product innovation designed to expand eligibility while maintaining prudent underwriting standards.

Subsidized Mortgage Programs

Subsidized Mortgage Programs segment is estimated at USD 58.4 billion in 2026 and is projected to reach USD 91.4 billion by 2033, at a CAGR of 6.6% during the forecast period.

Subsidized Mortgage Programs will expand through coordinated government initiatives aimed at reducing interest burdens for eligible borrowers. Targeted subsidy frameworks will support first-time buyers and economically weaker households. The broader adoption of subsidized lending mechanisms will encourage long-term stability, improve repayment behavior, and enhance institutional participation within the Affordable Housing Finance Market.

Down Payment Assistance Loans

Down Payment Assistance Loans segment is estimated at USD 26.3 billion in 2026 and is projected to reach USD 45.1 billion by 2033, at a CAGR of 8% during the forecast period.

Down Payment Assistance Loans will address upfront capital constraints that limit home purchase decisions. Structured co-funding models and deferred repayment formats will widen participation among salaried and informal income groups. The Global Affordable Housing Finance Market will integrate digital verification systems to streamline eligibility assessment and improve disbursement transparency.

Affordable Rental Housing Construction Loans

Affordable Rental Housing Construction Loans segment is estimated at USD 58.0 billion in 2026 and is projected to reach USD 111.0 billion by 2033, at a CAGR of 9.7% during the forecast period.

Affordable Rental Housing Construction Loans will support large-scale development of affordable rental housing units across high-density corridors. Developers will access construction-linked financing tied to occupancy benchmarks and controlled rental caps. The Global Affordable Housing Finance Market will promote sustainable project design aligned with urban planning priorities and long-term tenant affordability.

Affordable Housing Projects Bridge Loans

Affordable Housing Projects Bridge Loans segment is estimated at USD 18.9 billion in 2026 and is projected to reach USD 33.3 billion by 2033, at a CAGR of 8.4% during the forecast period.

Affordable Housing Projects Bridge Loans will provide interim liquidity support during project development cycles. Short-tenure credit structures will assist developers facing delayed approvals or phased funding schedules. The Global Affordable Housing Finance Market will enhance risk monitoring tools to control exposure while ensuring timely completion of housing units.

Micro-mortgages and Incremental Housing Loans

Micro-mortgages and Incremental Housing Loans segment is estimated at USD 25.3 billion in 2026 and is projected to reach USD 65.3 billion by 2033, at a CAGR of 14.5% during the forecast period.

Micro-mortgages and Incremental Housing Loans will extend credit availability for informal-sector households seeking gradual home construction, expansion, or renovation. Smaller-ticket loans and simplified documentation norms will enhance outreach. The Global Affordable Housing Finance Market will adopt alternative credit scoring models to assess repayment capacity beyond conventional income records.

Others

Others segment is estimated at USD 11.2 billion in 2026 and is projected to reach USD 18.9 billion by 2033, at a CAGR of 7.8% during the forecast period.

Other financial instruments will include cooperative housing credit, community-backed lending pools, and blended finance structures. Innovation will focus on localized housing challenges and rural development projects. The Global Affordable Housing Finance Market will integrate climate-resilient financing frameworks to align affordability targets with environmental standards.

By Lender Type, the market is divided into:

Public Sector Banks

Public Sector Banks segment is projected to reach USD 160.0 billion by 2033, at a CAGR of 4.9% during the forecast period.

Public Sector Banks will continue expanding housing portfolios under regulatory mandates, supporting inclusive growth. Strong branch networks and policy alignment will improve outreach across tier II and tier III cities. The Global Affordable Housing Finance Market will benefit from interest subvention programs supported through institutional capital channels.

Private Banks

Private Banks segment is projected to reach USD 274.3 billion by 2033, at a CAGR of 9.4% during the forecast period.

Private Banks will adopt advanced risk analytics and automated underwriting systems to accelerate mortgage processing. Competitive interest offerings and customer-centric repayment models will attract emerging urban borrowers. The Global Affordable Housing Finance Market will witness differentiated product design driven by technology-enabled credit assessment frameworks.

Housing Finance Companies

Housing Finance Companies segment is projected to reach USD 169.8 billion by 2033, at a CAGR of 10.2% during the forecast period.

Housing Finance Companies will focus on specialized lending solutions tailored for lower-income segments. Flexible eligibility assessment and doorstep service models will support market penetration. The Global Affordable Housing Finance Market will experience portfolio diversification through targeted regional expansion strategies implemented by these institutions.

Others

Others segment is projected to reach USD 49.0 billion by 2033, at a CAGR of 7.4% during the forecast period.

Other lenders, including non-banking financial institutions and cooperative credit societies, will address underserved borrower segments. Localized knowledge and community engagement will support credit delivery in semi-formal markets. The Global Affordable Housing Finance Market will gradually integrate fintech platforms to enhance transparency and operational efficiency.

By Region:

Based on geography, the Global Affordable Housing Finance market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

In North America, rising property prices and widening homeownership gaps are accelerating demand for structured affordable housing finance solutions.

Europe Affordable Housing Finance Market will witness steady expansion, supported by rising housing affordability pressure, urban rental shortages, and policy-backed financing programs across Germany, France, the UK, Italy, Spain, and the rest of Europe.

In Asia Pacific, rapid urban migration and expanding middle-income populations are creating strong opportunities for affordable housing finance expansion.

Across the Middle East, Africa, and South America, housing shortages and government-backed subsidy frameworks are generating steady momentum in the Affordable Housing Finance Market.

Competitive Landscape and Strategic Insights

The Global Affordable Housing Finance Market plays a significant role in helping low- and middle-income households secure stable housing. With rising property costs and expanding urban populations, access to suitable financing options will remain critical for social and economic stability. Governments, public institutions, commercial banks, and specialized housing finance companies are working together to expand credit access, reduce borrowing costs, and design products aligned with first-time buyers. Financial support through long-term loans, interest subsidies, credit guarantees, and refinancing programs will continue to shape how affordable housing projects are funded across developed and emerging economies.

In the United States, institutions including Fannie Mae and Freddie Mac provide liquidity to the mortgage market through securitized home loans, allowing lenders to offer competitive rates. Major banks, including Wells Fargo, Bank of America, JPMorgan Chase, Citigroup through Citi Community Capital, PNC Financial Services Group, and Truist Financial, also maintain strong affordable housing portfolios. In Canada, the Canada Mortgage and Housing Corporation (CMHC) supports mortgage insurance and housing initiatives focused on homeownership access and rental development. In the UK, Lloyds Banking Group, Barclays UK Corporate Bank, and NatWest Group contribute to financing solutions that support housing supply and urban regeneration.

Across Europe and Australia, publicly backed institutions maintain a strong presence. Caisse des Dépôts Group, through Banque des Territoires in France, and KfW Group in Germany provide structured financing programs that support sustainable and inclusive housing growth. Housing Australia supports funding models that connect private capital with public housing needs. In Latin America, Caixa Econômica Federal plays a leading role in Brazil’s housing credit system, offering loans tailored to lower-income borrowers. In Asia, PT Bank Tabungan Negara (Persero) Tbk (BTN) in Indonesia, Government Housing Bank in Thailand, and Pag-IBIG Fund in the Philippines remain important institutions expanding access to affordable mortgages for working households.

In Africa and India, specialized housing finance institutions are driving meaningful expansion. Housing Finance Bank in Uganda, HF Group in Kenya, Kenya Mortgage Refinance Company (KMRC) PLC, and TUHF Limited in South Africa focus on urban housing development and refinancing systems that strengthen lending capacity. India has witnessed strong participation from LIC Housing Finance Limited, Can Fin Homes Limited, PNB Housing Finance Limited, Repco Home Finance Limited, Aavas Financiers Limited, Home First Finance Company India Limited, and Aptus Value Housing Finance India Limited. These companies concentrate on underserved segments by offering smaller-ticket loans and simplified approval processes. With housing needs rising globally, collaboration between banks, development finance institutions, and private lenders will remain crucial in closing the housing gap and supporting long-term financial stability.

Forecast and Future Outlook

Market size is forecast to rise from USD 347.7 billion in 2025 to over USD 653.2 billion by 2033.

Institutional investors will allocate larger portions of ESG-linked capital into structured affordable housing portfolios, treating housing finance not only as a social objective but also as a stable yield-generating asset class. Secondary markets for low-income housing loans will mature, enabling liquidity recycling and improved balance sheet management. Through financial engineering, regulatory recalibration, and data-driven inclusion, the industry will move beyond volume expansion toward sustainable capital architecture that embeds affordability within long-term financial systems.

Affordable Housing Finance Market Key Segments:

By Type:

Affordable Homeownership Mortgages

Subsidized Mortgage Programs

Down Payment Assistance Loans

Affordable Rental Housing Construction Loans

Affordable Housing Projects Bridge Loans

Micro-mortgages and Incremental Housing Loans

Others

By Lender Type:

Public Sector Banks

Private Banks

Housing Finance Companies

Others

Key Global Affordable Housing Finance Industry Players

This research report categorizes the Affordable Housing Finance market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Affordable Housing Finance market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Affordable Housing Finance market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 8.2% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Type, Lender Type, and Region

By Region

North America (By Type, Lender Type, and Country)

United States

Canada

Mexico

Europe (By Type, Lender Type, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Type, Lender Type, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Type, Lender Type, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Type, Lender Type, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Australia Parametric Insurance Market Size, Share, Trends, 2033

Australia Parametric Insurance market size is valued at USD 286.4 million in 2025 and is projected to reach USD 720.9 million in 2033, at a CAGR of 12.2% from 2026 to 2033.

Australia Parametric Insurance Market, Australia Parametric Insurance Market Size, Australia Parametric Insurance Market Share, Australia Parametric Insurance Market Analysis, Australia Parametric Insurance Market Growth, Australia Parametric Insurance Market Trends, Australia Parametric Insurance Market Research Report, Australia Parametric Insurance Market Forecast, Australia Parametric Insurance, Australia Parametric Insurance Market Research, Australia Parametric Insurance Industry, Australia Parametric Insurance Industry Report, Australia Parametric Insurance Market Data, Australia Parametric Insurance Statistics, Australia Parametric Insurance Market Statistics, Australia Parametric Insurance Industry Trends, Australia Parametric Insurance Market Report, Australia Parametric Insurance Market Trends, Australia Parametric Insurance Market News, Australia Parametric Insurance Forecasts, Australia Parametric Insurance Market Intelligence Report

Merchant Banking Services market size is valued at USD 68.3 billion in 2025 and is projected to reach USD 260.7 billion in 2033, at a CAGR of 18.3% from 2026 to 2033.

Global Debt Management Solutions market size is valued at USD 41.8 billion in 2025 and is projected to reach USD 72.8 billion in 2033, at a CAGR of 7.2% from 2026 to 2033

Global Corporate Treasury Management Software market size is valued at USD 6,964.9 million in 2025 and is projected to reach USD 10,763.8 million in 2033, at a CAGR of 5.6% from 2026 to 2033