Managed Security Services Market Size, Share, By Service Type (Managed Detection Response (MDR), Managed Firewall Services, Managed SIEM, Managed Identity Access Management, Managed Risk Compliance Management Services, Managed Unified Threat Management, and Others), By Deployment Mode (On-Premise, Cloud-Based, and Hybrid), By Organization Size (Large Enterprises, Small Enterprises, and Medium‑sized Enterprises), By Industry Vertical (BFSI, Government, Healthcare, Telecommunication, IT, Enterprises, Retail, Energy, Utilities, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4740

Published

May 19, 2026

Pages

316 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

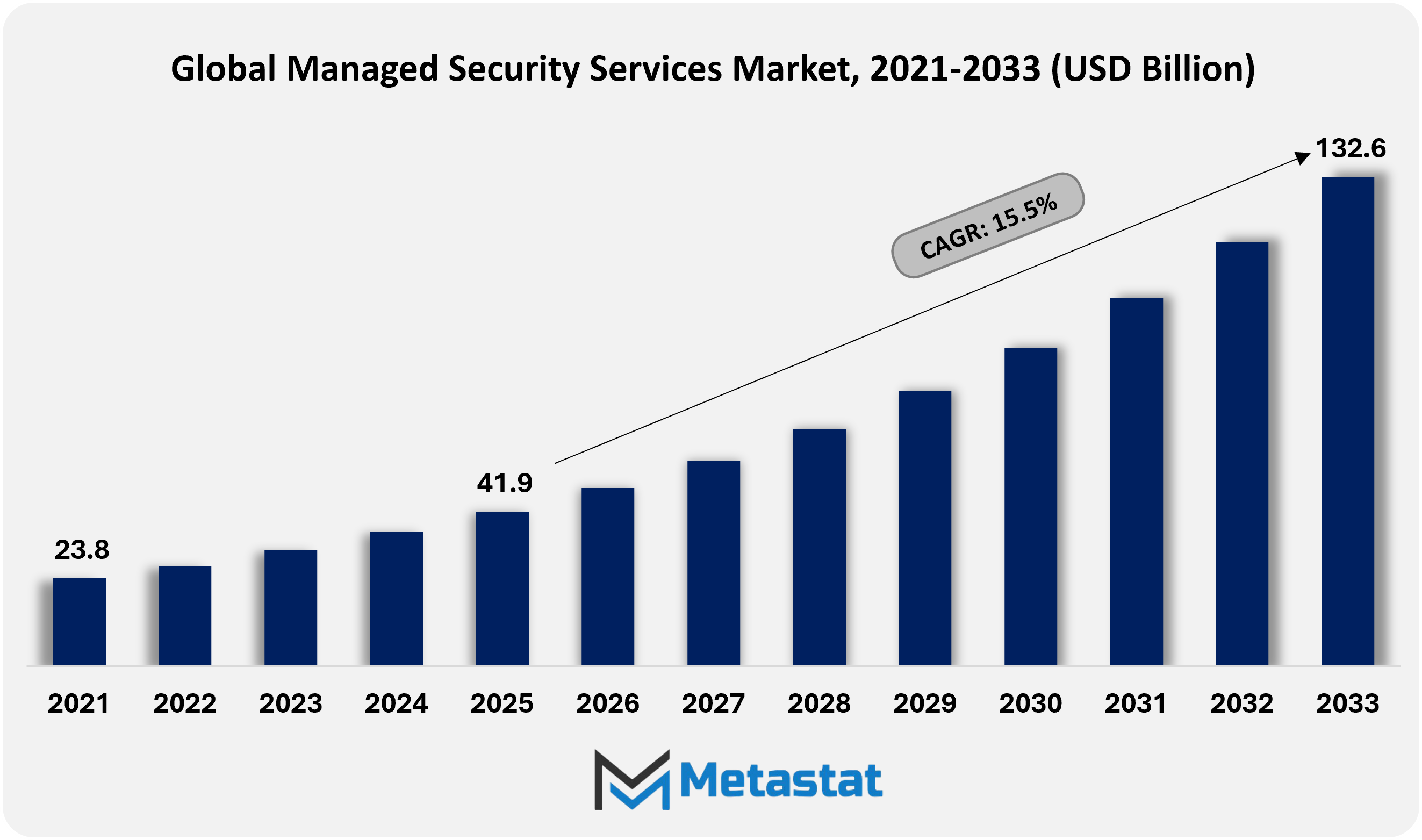

Global Managed Security Services market size is valued at USD 41.9 billion in 2025 and projected to grow at a CAGR of 15.5% during the forecast period, reaching USD 132.6 billion by 2033.

Global Managed Security Services Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Managed Security Services market valued at USD 41.9 billion in 2025, growing at a CAGR of 15.5% through 2033, with potential to exceed USD 132.6 billion.

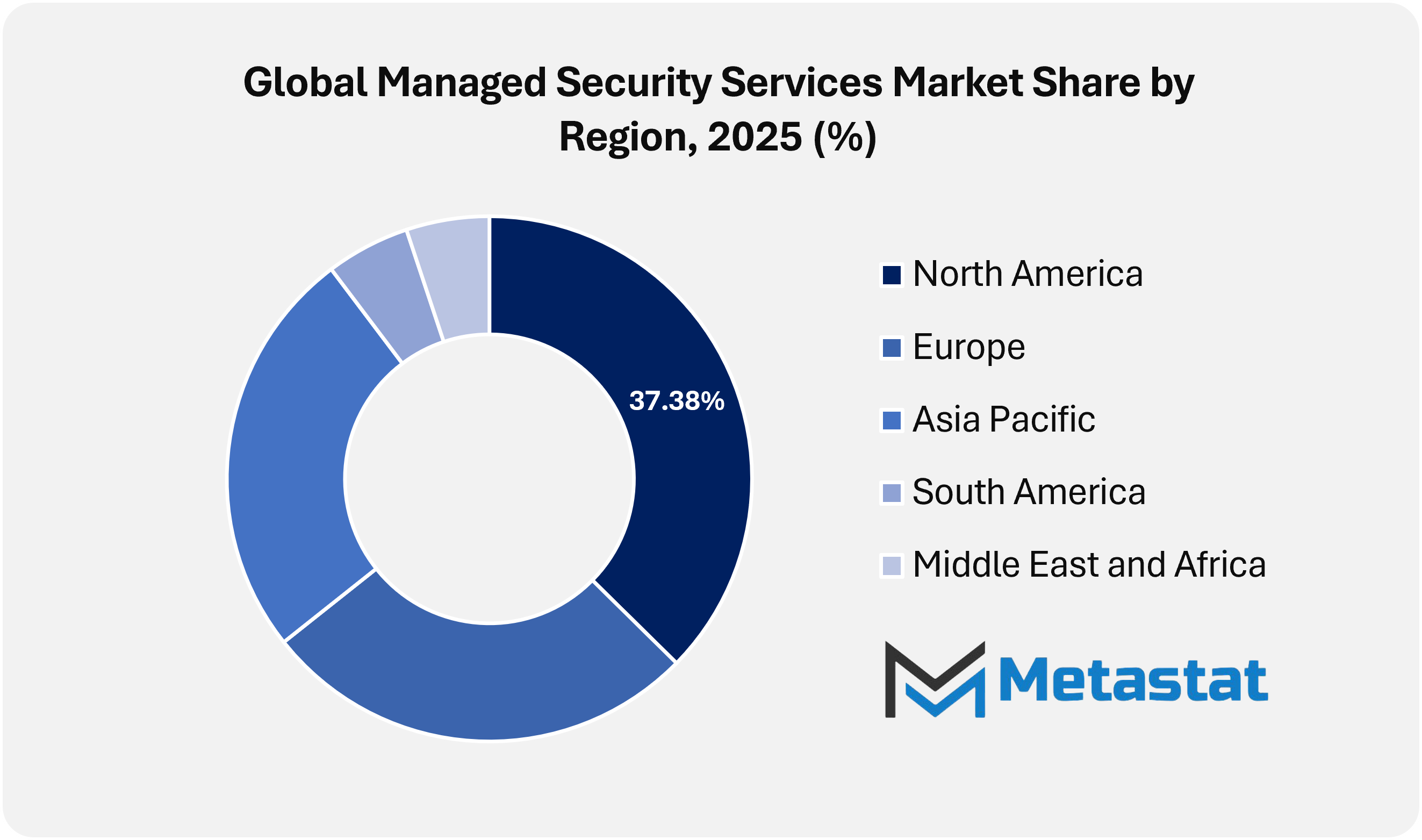

North America holds 37.4% in 2025 with US leading the market share in 2025.

Managed Detection and Response (MDR) segment account for a market share of 22.2% in 2025.

Key trends driving growth: Rising threat frequency and attack sophistication across enterprise IT, cloud, and hybrid environments, along with regulatory compliance pressure driving 24x7 monitoring, auditability, and incident readiness.

Opportunities include co-managed SOC and MDR expansion aligned with XDR adoption and cloud-native security operations.

Key insight: Rising cyber risk intensity and regulatory pressure accelerate enterprise dependence on outsourced security operations across the Global Managed Security Services Market.

The Global Managed Security Services market within the cybersecurity services industry is evolving beyond conventional threat monitoring and incident response toward a broader enterprise resilience function. Managed security providers are increasingly aligning security operations with risk governance, digital transformation priorities, and cross-border compliance requirements. Enterprises are engaging external partners not only to improve threat visibility and response speed, but also to strengthen board-level oversight, business continuity, and regulatory accountability.

Over the forecast period, managed detection and response frameworks will become more tightly integrated with cloud-native environments, zero-trust architectures, and identity-centric security models. Service providers will expand the use of advanced telemetry analytics, automation, and threat intelligence across hybrid infrastructures to support predictive defense and operational continuity. Commercial models will also shift toward outcome-based engagements tied to resilience, uptime, and incident containment performance, reinforcing long-term provider-client relationships.

Market Dynamics

Growth Drivers:

Rising threat frequency and attack sophistication across enterprise IT, cloud, and hybrid environments.

Escalating cyberattacks, including ransomware, phishing automation, and zero-day exploitation, are increasing enterprise exposure across distributed IT environments. Expansion of hybrid cloud infrastructure and remote work models is widening the attack surface across industries. The Global Managed Security Services Market is benefiting from rising demand for predictive threat intelligence, continuous vulnerability management, and proactive detection frameworks designed to counter increasingly complex intrusion patterns.

Regulatory compliance pressure driving 24x7 monitoring, auditability, and incident readiness

Expanding regulatory frameworks across finance, healthcare, telecom, and critical infrastructure are enforcing stricter cybersecurity governance standards. Mandatory breach reporting timelines, audit trails, and continuous log retention requirements are increasing reliance on structured monitoring environments. The Global Managed Security Services Market is advancing through sustained investment in round-the-clock surveillance, compliance reporting automation, and rapid incident containment capabilities aligned with evolving global regulations.

Restraints and Challenges:

Data sovereignty, confidentiality, and control concerns limiting outsourced security scope

Data sovereignty rules, privacy regulations, and internal governance requirements are limiting cross-border visibility and centralized monitoring models in several industries. Sensitive workloads often face restrictions on third-party access because of confidentiality concerns and contractual obligations. The Global Managed Security Services Market will face slower outsourcing adoption in highly regulated sectors where control retention remains a strategic priority.

Integration complexity across multi-vendor security stacks and legacy infrastructure

Fragmented cybersecurity architectures built on multiple vendor platforms continue to create interoperability gaps and operational silos. Legacy infrastructure with limited API compatibility complicates unified monitoring, orchestration, and response. The Global Managed Security Services Market will face implementation delays and higher onboarding costs where consolidation and standardized security frameworks remain underdeveloped.

Opportunities:

Co-managed SOC and MDR expansion aligned with XDR adoption and cloud-native security operations

Rising adoption of extended detection and response platforms is strengthening demand for collaborative security operating models. Co-managed SOC frameworks improve shared visibility, accelerate triage, and support internal teams with specialist expertise. The Global Managed Security Services Market is gaining opportunity through MDR integration with cloud-native analytics, automation-led threat hunting, and unified telemetry intelligence environments.

Market Segmentation Analysis

The Global Managed Security Services market is classified based on Service Type, Deployment Mode, Organization Size, and Industry Vertical.

By Service Type, the market is further segmented into:

Managed Detection and Response (MDR) segment is valued at USD 10.7 billion in 2026 and is projected to reach USD 31 billion by 2033, at a CAGR of 16.4% during the forecast period.

Managed Detection and Response is gaining traction through advanced threat analytics, continuous monitoring, and faster incident response. Security operations centers are increasingly adopting automated correlation, behavioral analysis, and rapid containment workflows. Improved threat intelligence and reduced dwell time are strengthening enterprise resilience against complex cyberattacks.

Managed Firewall Services

Managed Firewall Services segment is valued at USD 8.2 billion in 2026 and is projected to reach USD 19.3 billion by 2033, at a CAGR of 12.9% during the forecast period.

Managed Firewall Services are expanding through centralized policy administration and integration of next-generation firewall technologies. Distributed enterprises require real-time rule updates, traffic inspection, and secure remote connectivity across locations. Firewall orchestration is improving network segmentation, reducing unauthorized access risk, and strengthening perimeter security across digital environments.

Managed SIEM

Managed SIEM segment is valued at USD 7.1 billion in 2026 and is projected to reach USD 17.8 billion by 2033, at a CAGR of 14% during the forecast period.

Managed SIEM solutions are advancing through scalable log aggregation, analytics-driven alert prioritization, and better incident visibility. High-volume security event processing with improved accuracy is helping reduce false positives. Data-driven insights are also supporting compliance reporting, forensic investigation, and stronger governance across complex IT estates.

Managed Identity and Access Management segment is valued at USD 6 billion in 2026 and is projected to reach USD 18.2 billion by 2033, at a CAGR of 17.2% during the forecast period.

Managed Identity and Access Management is strengthening zero-trust security strategies across enterprises. Adaptive authentication, privileged access monitoring, and centralized identity governance are helping reduce identity misuse. Rising digital transformation initiatives are increasing reliance on identity-centric security controls across workforce, partner, and third-party access environments.

Managed Risk and Compliance Management Services

Managed Risk and Compliance Management Services segment is valued at USD 5.2 billion in 2026 and is projected to reach USD 17.1 billion by 2033, at a CAGR of 18.6% during the forecast period.

Managed Risk and Compliance Management Services are expanding in line with tighter regulatory oversight across industries. Continuous risk assessments, automated compliance checks, and policy monitoring tools are supporting structured governance. Enterprises are adopting proactive risk mitigation strategies to reduce penalties and protect brand credibility in regulated operating environments.

Managed Unified Threat Management

Managed Unified Threat Management segment is valued at USD 3.7 billion in 2026 and is projected to reach USD 8.2 billion by 2033, at a CAGR of 12.2% during the forecast period.

Managed Unified Threat Management continues to attract demand through integrated firewall, intrusion detection, content filtering, and endpoint protection capabilities. Consolidated threat visibility is helping reduce operational gaps and simplify administration. Cost-conscious organizations are adopting these platforms to secure branch networks and remote work environments with broader coverage.

Others

Others segment is valued at USD 7.4 billion in 2026 and is projected to reach USD 21 billion by 2033, at a CAGR of 16.1% during the forecast period.

Other service categories include vulnerability management, endpoint security, and specialized security consulting. Demand is rising for tailored offerings that address emerging technology environments such as AI systems and industrial control networks. Customized service bundles are improving flexibility across varied enterprise risk profiles.

By Deployment Mode, the market is divided into:

On-Premise

On-Premises segment is projected to reach USD 24.3 billion by 2033, at a CAGR of 6.8% during the forecast period.

On-Premises deployment remains relevant for organizations that require strong data sovereignty, internal control, and localized security oversight. Dedicated infrastructure and direct hardware governance continue to support sensitive operations. High-security industries are maintaining investment in on-premises architectures to preserve operational authority and regulatory alignment.

Cloud-Based

Cloud-Based segment is projected to reach USD 72.8 billion by 2033, at a CAGR of 19.6% during the forecast period.

Cloud-Based deployment is expanding through scalable monitoring platforms, subscription-led delivery models, and easier remote accessibility. Automated updates and lower upfront infrastructure costs are supporting adoption among digital-first enterprises. Advanced encryption, shared threat intelligence, and cloud-native analytics are improving defense efficiency across global operations.

Hybrid

Hybrid segment is projected to reach USD 35.5 billion by 2033, at a CAGR of 16.5% during the forecast period.

Hybrid deployment is bridging legacy environments with modern cloud security frameworks. Integrated visibility across on-site infrastructure and virtual workloads is improving operational continuity. Flexible workload distribution is supporting phased digital migration while preserving critical data controls for compliance-sensitive organizations.

By Organization Size, the market is further divided into:

Large Enterprises

Large Enterprises segment is projected to reach USD 72.9 billion by 2033.

Large Enterprises are prioritizing multilayered defense strategies supported by globally coordinated security operations. Cross-border compliance requirements, complex IT estates, and large-scale data processing are increasing reliance on managed security partners. Strategic outsourcing is improving operational efficiency while reducing pressure on internal security teams.

Small and Medium‑sized Enterprises (SMEs)

Small and Medium‑sized Enterprises (SMEs) segment is projected to reach USD 59.8 billion by 2033.

Small and Medium-sized Enterprises are adopting cost-efficient managed security models to address rising cyber threats and limited in-house expertise. Subscription-led offerings with simplified dashboards are improving accessibility. Scalable security frameworks are helping SMEs strengthen digital operations without substantial infrastructure investment.

By Industry Vertical, the Global Managed Security Services market is divided as:

Banking, Financial Services, and Insurance

Banking, Financial Services, and Insurance segment is projected to grow at a CAGR of 13.7% during the forecast period.

Banking, Financial Services, and Insurance organizations are strengthening fraud detection capabilities, transaction monitoring, and regulatory reporting systems. Rising digital payment activity and strict compliance mandates are increasing demand for continuous threat surveillance. Advanced encryption and identity verification frameworks are supporting protection of sensitive financial data.

Government

Government segment is projected to grow at a CAGR of 16.7% during the forecast period.

Government entities are increasing investment in national cyber defense programs and secure digital infrastructure. Protection of critical systems, citizen data, and public communication networks is shaping procurement priorities. Coordinated incident response capabilities are improving resilience against state-sponsored and organized cyber threats.

Healthcare

Healthcare segment is projected to grow at a CAGR of 17.2% during the forecast period.

Healthcare organizations are prioritizing patient data security, connected medical device protection, and secure access management. Electronic health records and telemedicine platforms require stronger monitoring and ransomware defense measures. Compliance-driven security adoption is increasing across hospitals, clinics, and healthcare networks.

Telecommunication

Telecommunication segment is projected to grow at a CAGR of 14.2% during the forecast period.

Telecommunication providers are focusing on securing 5G infrastructure, network virtualization, and large-scale subscriber data environments. Increasing traffic volumes and distributed network architectures are raising the need for automated threat intelligence and anomaly detection. Managed security services are helping telecom operators improve service continuity and reduce cyber risk exposure.

IT and Enterprises

IT and Enterprises segment is projected to grow at a CAGR of 17.3% during the forecast period.

IT and enterprise users are adopting integrated security operations to protect cloud-native applications, remote workforces, and distributed digital assets. DevSecOps alignment, endpoint monitoring, and vulnerability scanning are becoming essential to secure agile development environments. Security automation is also improving response speed across complex enterprise ecosystems.

Retail

Retail segment is projected to grow at a CAGR of 13.9% during the forecast period.

Retail companies are increasing adoption of managed security services in line with digital payment growth and omnichannel commerce expansion. Protection of point-of-sale systems, customer data, and e-commerce platforms is becoming increasingly critical. Scalable monitoring and fraud prevention capabilities are helping retailers maintain trust during peak transaction periods.

Energy and Utilities

Energy and Utilities segment is projected to grow at a CAGR of 16% during the forecast period.

Energy and utilities providers are focusing on protection of industrial control systems, smart grids, and critical infrastructure networks. Convergence of operational technology and information technology is increasing cyber risk exposure across utility environments. Continuous risk assessment, network segmentation, and threat monitoring are helping strengthen infrastructure resilience.

Others

Others segment is projected to grow at a CAGR of 12.3% during the forecast period.

Other industry verticals include education, manufacturing, and transportation. Increasing digital adoption across these sectors is driving reliance on managed security frameworks. Sector-specific compliance requirements and growing connected device deployment are shaping demand for tailored protection services.

By Region:

Based on geography, the Global Managed Security Services market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Managed Security Services Market is set to expand at a CAGR of 15.5% within the forecast period, reaching a market size (TAM) of USD 47.1 billion by the end of 2033.

In North America, strict data protection frameworks, high cyberattack frequency, and mature enterprise security spending continue to support strong adoption of outsourced security operations across major industries.

In Europe, GDPR-led compliance requirements, critical infrastructure protection mandates, and increasing ransomware incidents are supporting adoption of managed security services across public and private sector organizations.

In Asia Pacific, rapid digital transformation among SMEs, rising cloud deployment across banking, telecom, and manufacturing, and expanding cybersecurity investment are creating strong opportunities for scalable managed security services.

Across the Middle East, Africa, and South America, increasing cyber risk exposure, increasing internet penetration, and sluggish corporation modernization support steady uptake of managed protection offerings.

Competitive Landscape and Strategic Insights

The Global Managed Security Services Market is expanding steadily as enterprises increasingly recognize cybersecurity as a continuous operational priority rather than an occasional technical issue. Organizations across banking, healthcare, retail, manufacturing, and government are moving from reactive security approaches toward proactive monitoring, detection, and response frameworks. Outsourcing security operations is gaining wider acceptance since maintaining an in-house security operations center requires substantial investment, specialized expertise, and ongoing technology upgrades. Managed security services support enterprises with 24/7 monitoring, threat intelligence, incident detection, compliance support, and risk assessment, enabling them to focus on core business functions while strengthening overall digital resilience.

Large technology and consulting firms continue to play a major role in shaping the competitive landscape of the market. Companies such as IBM Corporation, Accenture plc, NTT Ltd., Cisco Systems, Inc., and Wipro Limited offer integrated security frameworks that combine consulting, managed detection, cloud security, and compliance management. Their global delivery capabilities allow them to support multinational clients through unified security policies and coordinated service execution across regions. At the same time, cybersecurity-focused companies such as Palo Alto Networks, Inc., Fortinet, Inc., Check Point Software Technologies Ltd., Trend Micro Incorporated, and Sophos Limited are strengthening the market through advanced firewall management, endpoint security, and extended detection and response services that remain critical for countering sophisticated threats.

Cloud service providers and telecom-linked players are also broadening their managed security portfolios. Amazon Web Services, Inc. integrates security controls directly into cloud infrastructure, supporting scalable protection for enterprises shifting workloads to digital environments. Companies such as Infosys Limited, AT&T Inc., Verizon Communications Inc., Capgemini SE, and Fujitsu Limited combine connectivity expertise, infrastructure capabilities, and managed security services to deliver secure network environments and continuous threat monitoring. Their ability to offer cloud, connectivity, and cybersecurity services under integrated commercial models is attracting enterprises seeking operational simplicity and centralized vendor management.

Specialized and next-generation security providers are driving innovation through managed detection and response, automation, and AI-enabled threat analysis. Companies such as SentinelOne, Inc., Rapid7, Inc., Arctic Wolf Networks, Inc., Red Canary, Inc., eSentire, Inc., and Expel, Inc. are strengthening competition through continuous monitoring and rapid incident containment capabilities. Established firms including BAE Systems, Inc., Samsung SDS Co., Ltd., Tata Consultancy Services Limited, Kyndryl Holdings, Inc., DXC Technology Company, Atos SE, and Telefónica Tech are also supporting enterprise-grade managed security programs across industries. In addition, niche providers such as Kudelski Security SA, Orange Cyberdefense SAS, Blackpoint Cyber, LLC, Barracuda Networks, Inc., ProSOC Inc., F5, Inc., and BlueVoyant are adding competitive depth by delivering tailored services for mid-sized enterprises and regulated sectors.

As cyber risks continue to intensify in scale, complexity, and frequency, demand for managed security services will continue to rise across developed and emerging markets. Enterprises will increasingly prefer vendors that combine strong threat intelligence, automation capabilities, regulatory knowledge, and scalable cloud security models. Strategic partnerships, acquisitions, and AI integration will continue to shape competition among leading market participants. The future direction of the market will depend on how effectively providers align security operations with business continuity priorities, positioning cybersecurity as a core element of enterprise strategy rather than only a support function.

Forecast and Future Outlook

Market size is forecast to rise from USD 41.9 billion in 2025 to over USD 132.6 billion by 2033.

The Global Managed Security Services market will continue to expand strongly through 2033, supported by rising cyber risk intensity, broader compliance pressure, and increasing dependence on outsourced security expertise. Enterprises are moving toward service models that deliver continuous visibility, faster response, and stronger governance across complex digital environments. Managed security services will become increasingly embedded in business continuity planning, enterprise resilience strategy, and long-term digital risk management. This shift will reinforce the market’s role as a core component of modern enterprise cybersecurity operations.

Managed Security Services Market Key Segments:

By Service Type:

Managed Detection and Response (MDR)

Managed Firewall Services

Managed SIEM

Managed Identity and Access Management

Managed Risk and Compliance Management Services

Managed Unified Threat Management

Others

By Deployment Mode:

On-Premise

Cloud-Based

Hybrid

By Organization Size:

Large Enterprises

Small and Mediumsized Enterprises (SMEs)

By Industry Vertical:

Banking, Financial Services, and Insurance

Government

Healthcare

Telecommunication

IT and Enterprises

Retail

Energy and Utilities

Others

Key Global Managed Security Services Industry Players

This research report categorizes the Managed Security Services market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Managed Security Services market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Managed Security Services market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 15.5% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Service Type, Deployment Mode, Organization Size, Industry Vertical, and Region

By Region

North America (By Service Type, Deployment Mode, Organization Size, Industry Vertical, and Country)

United States

Canada

Mexico

Europe (By Service Type, Deployment Mode, Organization Size, Industry Vertical, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Service Type, Deployment Mode, Organization Size, Industry Vertical, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Service Type, Deployment Mode, Organization Size, Industry Vertical, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Service Type, Deployment Mode, Organization Size, Industry Vertical, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

New Zealand Optical Encryption Market Size, Share, Trends, 2033

New Zealand Optical Encryption market size is valued at USD 34.5 million in 2025 and is projected to reach USD 76.9 million in 2033, at a CAGR of 10.3% from 2026 to 2033.

New Zealand Optical Encryption Market, New Zealand Optical Encryption Market Size, New Zealand Optical Encryption Market Share, New Zealand Optical Encryption Market Analysis, New Zealand Optical Encryption Market Growth, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market Research Report, New Zealand Optical Encryption Market Forecast, New Zealand Optical Encryption, New Zealand Optical Encryption Market Research, New Zealand Optical Encryption Industry, New Zealand Optical Encryption Industry Report, New Zealand Optical Encryption Market Data, New Zealand Optical Encryption Statistics, New Zealand Optical Encryption Market Statistics, New Zealand Optical Encryption Industry Trends, New Zealand Optical Encryption Market Report, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market News, New Zealand Optical Encryption Forecasts, New Zealand Optical Encryption Market Intelligence Report

Retail Project Management Software market size is valued at USD 1,505.5 million in 2025 and is projected to reach USD 3,524.9 million in 2033, at a CAGR of 11.2% from 2026 to 2033.

Generative AI in Analytics Market Size, Share, Trends, 2033

Generative AI in Analytics market size is valued at USD 1.6 billion in 2025 and is projected to reach USD 10.9 billion in 2033, at a CAGR of 26.8% from 2026 to 2033.

Generative AI in Analytics Market, Generative AI in Analytics Market Size, Generative AI in Analytics Market Share, Generative AI in Analytics Market Analysis, Generative AI in Analytics Market Growth, Generative AI in Analytics Market Trends, Generative AI in Analytics Market Research Report, Generative AI in Analytics Market Forecast, Generative AI in Analytics, Generative AI in Analytics Market Research, Generative AI in Analytics Industry, Generative AI in Analytics Industry Report, Generative AI in Analytics Market Data, Generative AI in Analytics Statistics, Generative AI in Analytics Market Statistics, Generative AI in Analytics Industry Trends, Generative AI in Analytics Market Report, Generative AI in Analytics Market Trends, Generative AI in Analytics Market News, Generative AI in Analytics Forecasts, Generative AI in Analytics Market Intelligence Report

UK Immersive Entertainment & Experiential Property Market Size, Share, Trends, 2033

UK Immersive Entertainment & Experiential Property Market size is valued at USD 6.17 billion in 2025 and is projected to reach USD 26.16 billion in 2033, at a CAGR of 19.5% from 2026 to 2033

UK Immersive Entertainment & Experiential Property Market, UK Immersive Entertainment & Experiential Property Market Size, UK Immersive Entertainment & Experiential Property Market Share, UK Immersive Entertainment & Experiential Property Market Analysis, UK Immersive Entertainment & Experiential Property Market Growth, UK Immersive Entertainment & Experiential Property Market Trends, UK Immersive Entertainment & Experiential Property Market Research Report, UK Immersive Entertainment & Experiential Property Market Forecast, UK Immersive Entertainment & Experiential Property, UK Immersive Entertainment & Experiential Property Market Research, UK Immersive Entertainment & Experiential Property Industry, UK Immersive Entertainment & Experiential Property Industry Report, UK Immersive Entertainment & Experiential Property Market Data, UK Immersive Entertainment & Experiential Property Statistics, UK Immersive Entertainment & Experiential Property Market Statistics, UK Immersive Entertainment & Experiential Property Industry Trends, UK Immersive Entertainment & Experiential Property Market Report, UK Immersive Entertainment & Experiential Property Market Trends, UK Immersive Entertainment & Experiential Property Market News, UK Immersive Entertainment & Experiential Property Forecasts, UK Immersive Entertainment & Experiential Property Market Intelligence Report