Machine Loading Robots Market Size, Share, By Type (Cartesian Robots, Articulated Robots, SCARA Robots, Collaborative Robots, and Others), By Payload Capacity (Up to 5 Kg, 5-10 Kg, 10-20 Kg, 20-50 Kg, and Above 50 Kg), By End-User (Automotive, Electronics, Manufacturing, Food, Beverages, Logistics, Industrial, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4612

Published

April 14, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

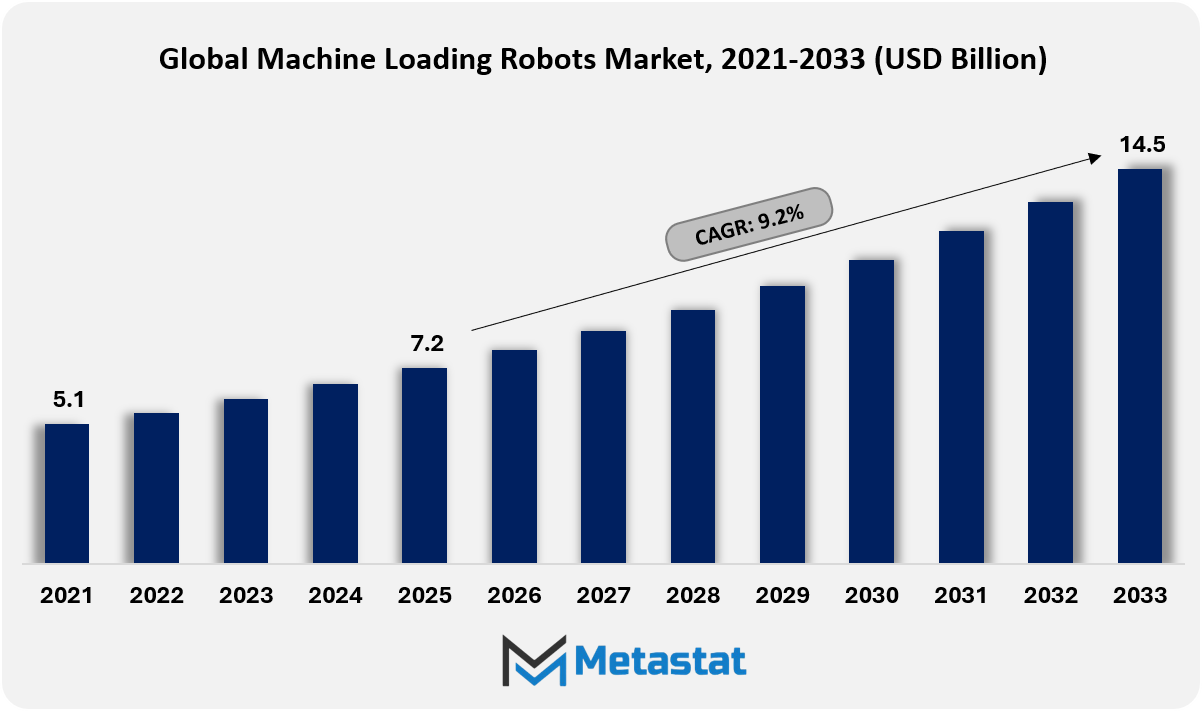

The Global Machine Loading Robots market size was valued at USD 7.2 billion in 2025 and projected to grow at a CAGR of 9.2% during the forecast period, reaching USD 14.5 billion by 2033.

Global Machine Loading Robots Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

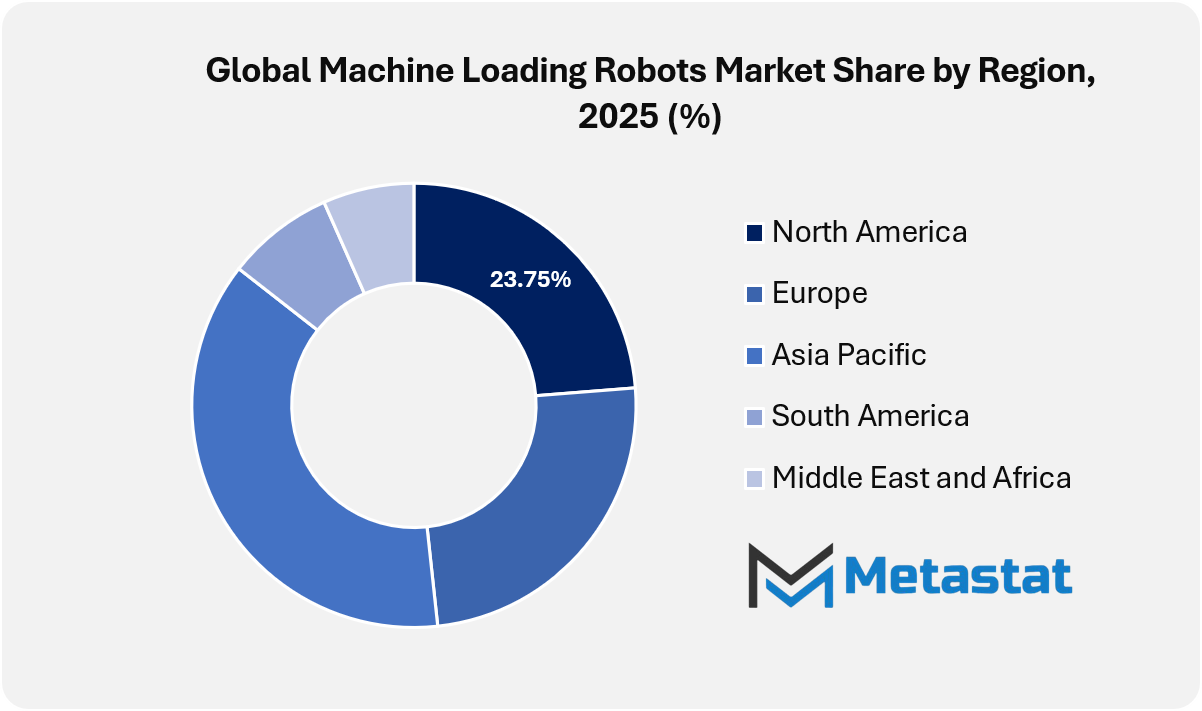

North America accounted for 23.7% of the global market in 2025, with the U.S. leading the regional market.

Articulated Robots segment accounted for the largest market share of 33.42% in 2025.

Key factors driving growth include rising demand for automation to improve production efficiency and reduce labor dependency, along with increasing adoption of robotics in the automotive, electronics, and metal fabrication industries.

Opportunities include growing adoption of collaborative and AI-enabled robots for flexible machine loading applications.

Key insight: Precision-driven automation and labor optimization are redefining machine loading robots from efficiency tools into core manufacturing assets.

The Global Machine Loading Robots market is entering a phase in which automation strategy is shaped less by unit replacement and more by system-wide orchestration across manufacturing ecosystems. Over the coming years, machine loading robots are expected to move beyond isolated work cells and become embedded within cyber-physical production environments where data, motion, and decision logic converge. Their role is likely to expand into dynamic scheduling, predictive task sequencing, and real-time coordination with upstream and downstream equipment, enabling factories to operate as adaptive networks rather than linear production lines.

Industrial buyers are likely to evaluate machine loading robots through a strategic lens tied to resilience and operational continuity. Deployment decisions are expected to account for how robotic systems respond to supply volatility, tooling variation, and rapid product redesign. The market is expected to emphasize modular intelligence, where software-defined capabilities enable robots to shift between machining centers, additive systems, and inspection stations without extended reconfiguration cycles. This flexibility is likely to reshape capital planning, shifting attention from fixed automation assets toward reprogrammable production capacity.

Market Dynamics

Growth Drivers:

Rising demand for automation to improve production efficiency and reduce labor dependency.

Manufacturers face persistent pressure to increase output while controlling operational variability. Automated machine loading supports continuous production cycles, reduces manual handling, and stabilizes throughput. Adoption also supports workforce optimization, addresses skilled labor shortages, and improves manufacturing reliability, creating sustained demand across small, mid-sized, and large production facilities.

Increasing adoption of robotics in automotive, electronics, and metal fabrication industries.

Automotive assembly lines, electronics manufacturing facilities, and metal fabrication workshops are increasingly integrating robotic loading systems to manage high-volume repetitive tasks. Precision handling, reduced cycle time, and consistent quality standards support broader deployment. Industry-specific customization also enables alignment with complex machining requirements, encouraging deeper integration across diverse industrial environments.

Restraints and Challenges:

High initial investment and integration costs for robotic systems.

Capital expenditure associated with robotic hardware, software, and system integration remains a major barrier. Deployment requires alignment with existing equipment, safety infrastructure, and plant layouts. Budget limitations restrict adoption among cost-sensitive manufacturers, particularly in developing regions, slowing broader penetration despite long-term operational benefits.

Complexity in programming and maintaining robots for varied production tasks.

Machine loading applications require adaptability across product variants and machining processes. Programming complexity rises with production diversity, increasing the need for specialized technical expertise. Maintenance requirements add further operational burden, while limited availability of skilled technicians can reduce uptime and create hesitation among manufacturers seeking flexible automation.

Opportunities:

Growing adoption of collaborative and AI-enabled robots for flexible machine loading applications.

Collaborative robots and AI-enabled systems support safer human-machine interaction and more adaptive task execution. Advanced sensing, learning capabilities, and simplified programming help meet dynamic production needs. Flexible deployment models also improve suitability across a wide range of factory sizes, positioning advanced machine loading solutions for broader industrial adoption and sustained market growth.

Market Segmentation Analysis

The Global Machine Loading Robots market is classified based on Type, Payload Capacity, and End-User.

By Type, the market is further segmented into:

Cartesian Robots

Cartesian Robots segment is estimated at USD 1.7 billion in 2026 and is projected to reach USD 2.9 billion by 2033, at a CAGR of 7.5% during the forecast period.

Cartesian robots in the global machine loading robots market will benefit greatly because of linear precision, solid load handling, and predictable motion manipulation. Future manufacturing environments will prioritize accuracy, modular design, and integration with smart production lines, positioning Cartesian structures as dependable belongings for repetitive, high-velocity loading responsibilities.

Articulated Robots

Articulated Robots segment is estimated at USD 2.6 billion in 2026 and is projected to reach USD 4.4 billion by 2033, at a CAGR of 8% during the forecast period.

Articulated robots within the global machine loading robots market will enjoy sustained push with the aid of multi-axis flexibility and prolonged reach. Advanced factories will depend on articulated designs for complex loading styles, irregular components, and space-confined layouts, helping automation desires focused on adaptability, productivity growth, and reduced guide dependency.

SCARA Robots

SCARA Robots segment is estimated at USD 1.4 billion in 2026 and is projected to reach USD 2.6 billion by 2033, at a CAGR of 9.3% during the forecast period.

SCARA robots across the global machine loading robots market will advance through demand for pace-centered automation. Lightweight construction and selective compliance will aid unique vertical loading operations. Future meeting and packaging facilities will desire SCARA gadgets for compact footprints, energy performance, and consistent overall performance under non-stop manufacturing cycles.

Collaborative Robots

Collaborative Robots segment is estimated at USD 1.3 billion in 2026 and is projected to reach USD 3 billion by 2033, at a CAGR of 12.5% during the forecast period.

Collaborative robots within the global machine loading robots market will shape the destiny of work through secure human-machine interplay. Built-in sensors and adaptive controls will allow deployment without significant safety obstacles. Industrial settings will increasingly undertake collaborative models to balance automation performance with bendy project sharing and evolving manufacturing necessities.

Others

Others segment is estimated at USD 0.8 billion in 2026 and is projected to reach USD 1.5 billion by 2033, at a CAGR of 9.8% during the forecast period.

Other robotic kinds in the global machine loading robots market will deal with the area of interest operational desires via customized configurations. Hybrid structures, cell loading devices, and alertness-precise robots will assist specialized industries. Technological experimentation will expand deployment options, encouraging tailored automation techniques aligned with future commercial diversification.

By Payload Capacity, the market is divided into:

Up to 5 Kg

Up to 5 Kg segment is projected to reach USD 3.8 billion by 2033, at a CAGR of 8.3% during the forecast period.

Up to 5 kg payload robots within the global machine loading robots market will support precision-driven industries requiring delicate handling. Electronics, scientific devices, and micro-assembly strains will depend on lightweight robots for velocity and accuracy. Future demand will rise through miniaturization trends and high-quantity, low-weight element manufacturing.

5-10 Kg

5-10 Kg segment is projected to reach USD 3.4 billion by 2033, at a CAGR of 9% during the forecast period.

Robots with 5–10 kg payload capability within the global machine loading robots market will serve mid-range packages, balancing strength and agility. Automated workstations will undertake these systems for steady loading throughout numerous product sizes. Future manufacturing fashions will emphasise flexibility, helping frequent changeovers without productivity compromise.

10-20 Kg

10-20 Kg segment is projected to reach USD 3.3 billion by 2033, at a CAGR of 9.7% during the forecast period.

The 10–20 kg segment of the Global Machine Loading Robots Market will align with increasing commercial automation. Manufacturing flora will make use of this ability for solid handling of heavy components. Growth will follow the scalable automation capable of helping assorted product portfolios and better operational throughout.

20-50 Kg

20-50 Kg segment is projected to reach USD 2.5 billion by 2033, at a CAGR of 10% during the forecast period.

Robots coping with 20–50 kg masses in the global machine loading robots market will address heavy-duty manufacturing needs. Automotive and business system production will depend on robust systems designed for durability. Future factories will combine these robots with advanced management software programs to enhance safety, performance, and load accuracy.

Above 50 Kg

Above 50 Kg segment is projected to reach USD 1.5 billion by 2033, at a CAGR of 9.2% during the forecast period.

Above 50 kg payload robots inside the global machine loading robots market will support large-scale commercial transformation. Heavy machinery, metal fabrication, and infrastructure production will require effective automation answers. Future deployment will focus on reliability, long operational cycles, and seamless integration with clever fabric coping with systems.

By End-User, the market is further divided into:

Automotive

Automotive segment is projected to reach USD 3.1 billion by 2033.

The automobile segment of the global machine loading robots market will improve via electric vehicle manufacturing and platform standardization. Automated loading will help precision meeting, decrease cycle times, and provide consistency. Future car plant life will increasingly rely upon robotics to fulfil extent targets and design complexity.

Electronics

Electronics segment is projected to reach USD 3 billion by 2033.

Electronics adoption inside the global machine loading robots market will grow owing to rising demand for compact, high-value components. Automation will allow infection management, precision alignment, and fast throughput. Future electronics manufacturing will rely on robot loading to support superior gadgets and shortened product lifecycles.

Manufacturing

Manufacturing segment is projected to reach USD 3 billion by 2033.

General production within the global machine loading robots market will boost automation investments to enhance efficiency and fee control. Robotic loading will guide standardized techniques throughout diverse product classes. Future manufacturing techniques will emphasize resilience, facts-driven optimization, and decreased dependency on guide material coping.

Food and Beverages

Food and Beverages segment is projected to reach USD 1.2 billion by 2033.

Food and beverage participation inside the global machine loading robots market will increase through hygiene-targeted automation. Robotic structures will guide steady handling, packaging accuracy, and regulatory compliance. Future processing facilities will prioritize automation to fulfil rising consumption demands while preserving safety and operational transparency.

Logistics

Logistics segment is projected to reach USD 1.8 billion by 2033.

Logistics applications within the global machine loading robots market will grow with e-trade expansion and warehouse automation. Robotic loading will guide faster order fulfillment and a blunder discount. Future logistics networks will integrate wise robots to enhance scalability, space utilization, and real-time operational responsiveness.

Industrial

Industrial segment is projected to reach USD 1.8 billion by 2033.

Industrial utilization within the global machine loading robots market will continue to be a foundational driving force. Heavy manufacturing environments will undertake robot loading to enhance protection and throughput. Future business operations will combine robotics with virtual tracking structures to help with predictive maintenance and non-stop productivity improvement.

Others

Others segment is projected to reach USD 0.7 billion by 2033.

Other give-up-person segments in the global machine loading robots market will mirror emerging automation needs across healthcare, aerospace, and research facilities. Customized robotic loading solutions will address specialised workflows. Future adoption will be driven by means of innovation, operational precision, and expanding industry automation popularity.

By Region:

Based on geography, the Global Machine Loading Robots market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Machine Loading Robots Market is set to expand at a CAGR of 9.2% within the forecast period, reaching a market size (TAM) of USD 3.1 billion by the end of 2033.

In North America, great adoption of clever production and chronic skilled labor shortages boost the call for device loading robots.

North America benefits from excessive automation depth throughout the car and aerospace industries, strengthening uptake of gadget loading robots.

Asia Pacific offers a sturdy possibility via increasing electronics and metal fabrication potential, searching for higher throughput and price efficiency through robotic loading.

Across the Asia Pacific, government-backed Industry packages and growing SME automation budgets open new avenues for device loading robotic deployment.

Middle East, Africa, and South America show sluggish momentum supported with the aid of commercial diversification, greenfield factories, and selective automation funding throughout mining, meals processing, and number one production.

Competitive Landscape and Strategic Insights

The Global Machine Loading Robots Market features a huge blend of setup automation leaders and rapidly rising robotics specialists, each shaping industrial production via precision, pace, and reliability. Companies such as FANUC Corporation, ABB Ltd., KUKA SE & Co. KGaA, and Yaskawa Electric Corporation stand at the leading edge, offering robot structures broadly followed throughout automotive, electronics, and heavy production centers. Their longstanding presence rests on deep engineering knowledge, sturdy international service networks, and constant enhancements targeted on accuracy, safety, and cycle-time discount.

Japanese producers keep maintaining a sturdy position in the market. Companies such as Kawasaki Robotics, Nachi-Fujikoshi Corp., Seiko Epson Corporation, Yamaha Motor Co., Ltd., Mitsubishi Electric Corporation, Denso Corporation, and Shibaura Machine CO., LTD make contributions to superior movement management, compact robotic designs, and excessive-velocity loading solutions. The companies focus closely on reliability and repeatability, assisting factories looking for solid output in high-volume production lines.

European firms add every other layer of electricity through flexibility and device integration capabilities. Stäubli International AG., Festo AG & Co. KG, and Agile Robotic Systems emphasize precision management, cleanroom compatibility, and collaborative automation principles. Universal Robots USA, Inc., Techman Robot Inc., JAKA Robotics Co., Ltd., AUBO Robotics, Dobot, and Elite Robots further amplify collaborative robot adoption, permitting small and mid-sized manufacturers to automate gadget loading responsibilities without complicated infrastructure.

Chinese automation carriers deliver scale and fee performance into awareness. Companies including Siasun Robot & Automation CO., Ltd., GSK CNC Equipment Co., Ltd., ESTUN AUTOMATION CO., LTD, Guangdong Huayan Robotics Co., Ltd., and Efort Robotics Srl boom home and international reach via competitive pricing and a rapidly evolving era. The presence strengthens adoption across steel processing, plastics, and trendy production sectors.

Together, the competitors create an aggressive marketplace shaped through innovation, accessibility, and performance-driven automation. Continuous funding in smarter controls, imaginative and prescient systems, and adaptive gripping solutions helps wider use of device loading robots throughout varied industrial settings, reinforcing their role in cutting-edge production environments.

Forecast and Future Outlook

Market size is forecast to rise from USD 7.2 billion in 2025 to over USD 14.5 billion by 2033.

Sustainability narratives are set to persuade design priorities. Energy-aware movement making plans, decreased idle cycles, and cloth-green handling behaviors are predicted to place machine loading robots within broader commercial decarbonization agendas. In parallel, regulatory attention is projected to move towards algorithmic responsibility, facts governance, and operational traceability, expanding the strategic verbal exchange past productiveness metrics.

Machine Loading Robots Market Key Segments:

By Type:

Cartesian Robots

Articulated Robots

SCARA Robots

Collaborative Robots

Others

By Payload Capacity:

Up to 5 Kg

5-10 Kg

10-20 Kg

20-50 Kg

Above 50 Kg

By End-User:

Automotive

Electronics

Manufacturing

Food and Beverages

Logistics

Industrial

Others

Key Global Machine Loading Robots Industry Players

This research report categorizes the Machine Loading Robots market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Machine Loading Robots market. Recent market developments and competitive strategies such as expansion, new site development, partnership, merger, and acquisition are included to present the competitive landscape.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Machine Loading Robots market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 9.2% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Thousand Units

Segmentation

By Type, Payload Capacity, End-User, and Region

By Region

North America (By Type, Payload Capacity, End-User, and Country)

United States

Canada

Mexico

Europe (By Type, Payload Capacity, End-User, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Type, Payload Capacity, End-User, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Type, Payload Capacity, End-User, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Type, Payload Capacity, End-User, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share and Revenue

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

Import-Export Trade Statistics

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Top players operating in the Machine Loading Robots industry include FANUC Corporation, KUKA SE & Co. KGaA, ABB Ltd., Yaskawa Electric Corporation, Nachi-Fujikoshi Corp., and Kawasaki Robotics.

Asia Pacific region dominates the market.

Global Machine Loading Robots market is estimated to reach USD 14.5 billion by 2033.

Rising demand for automation to improve production efficiency and reduce labor dependency. and increasing the adoption of robotics in the automotive, electronics, and metal fabrication industries. are key driving factors, boosting the market.

The Articulated Robots is the leading type segment in the Global market.

High initial investment and integration costs for robotic systems, will hamper market growth within the forecast period.

The Global Machine Loading Robots market is likely to grow at a CAGR of 9.2% over the forecast period (2026-2033).

The Metastat Insights analysis shows that the North America Machine Loading Robots market size is estimated to be USD 3.1 billion by 2033.

The Metastat Insights study shows that the Global Machine Loading Robots market size was USD 7.2 billion in 2025.

Stage Hoist market size is valued at USD 236.3 million in 2025 and is projected to reach USD 395.3 million in 2033, at a CAGR of 6.3% from 2026 to 2033.

Global Taper Lock Bushing market is valued at USD 1,187.8 million in 2025 and is projected to reach USD 1,808.0 million in 2033, at a CAGR of 5.4% from 2026 to 2033

Europe Mini Excavators Market Size, Share, Trends, 2033

Europe Mini Excavators market size is valued at USD 2,162.9 million in 2025 and is projected to reach USD 3,004.1 million in 2033, at a CAGR of 4.2% from 2026 to 2033

Europe Mini Excavators Market, Europe Mini Excavators Market Size, Europe Mini Excavators Market Share, Europe Mini Excavators Market Analysis, Europe Mini Excavators Market Growth, Europe Mini Excavators Market Trends, Europe Mini Excavators Market Research Report, Europe Mini Excavators Market Forecast, Europe Mini Excavators, Europe Mini Excavators Market Research, Europe Mini Excavators Industry, Europe Mini Excavators Industry Report, Europe Mini Excavators Market Data, Europe Mini Excavators Statistics, Europe Mini Excavators Market Statistics, Europe Mini Excavators Industry Trends, Europe Mini Excavators Market Report, Europe Mini Excavators Market Trends, Europe Mini Excavators Market News, Europe Mini Excavators Forecasts, Europe Mini Excavators Market Intelligence Report

Global Switch Actuators market size is valued at USD 18.4 billion in 2025 and is projected to reach USD 30.6 billion in 2033, at a CAGR of 6.6% from 2026 to 2033