Mobile TV Market Size, Share, By Content Type (Video-on-Demand, Online Video, and Live Streaming), By Technology (IPTV, OTT, Satellite, and Others), By Distribution Channel (Free to Air Service and Pay TV Service), By Applications (Commercial and Personal), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4629

Published

April 16, 2026

Pages

236 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

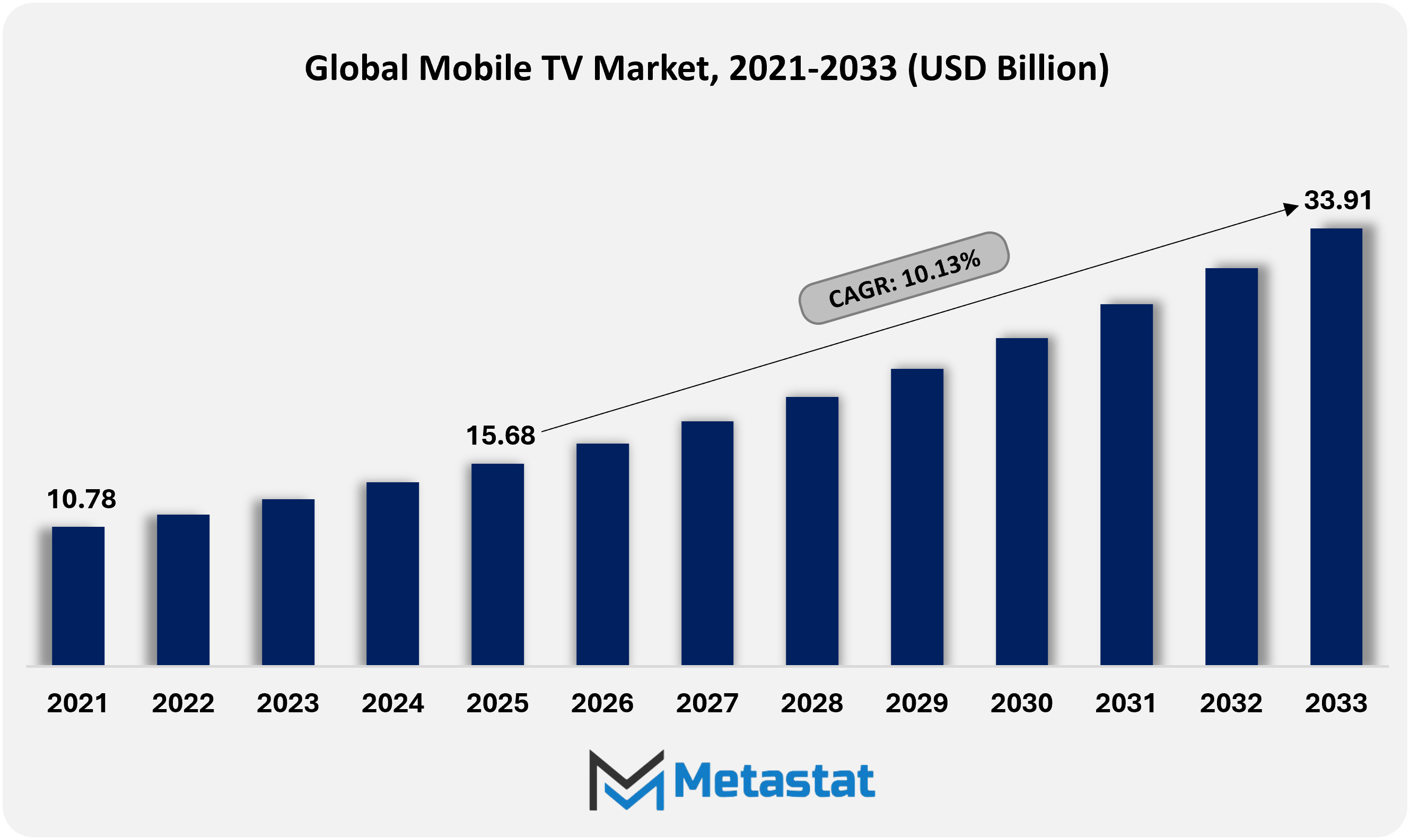

The Global Mobile TV market size was valued at USD 15.7 billion in 2025 and projected to grow at a CAGR of 10.1% during the forecast period, reaching USD 33.9 billion by 2033.

Global Mobile TV Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Mobile TV market valued at USD 15.7 billion in 2025, growing at a CAGR of 10.1% through 2033, with potential to exceed USD 33.9 billion.

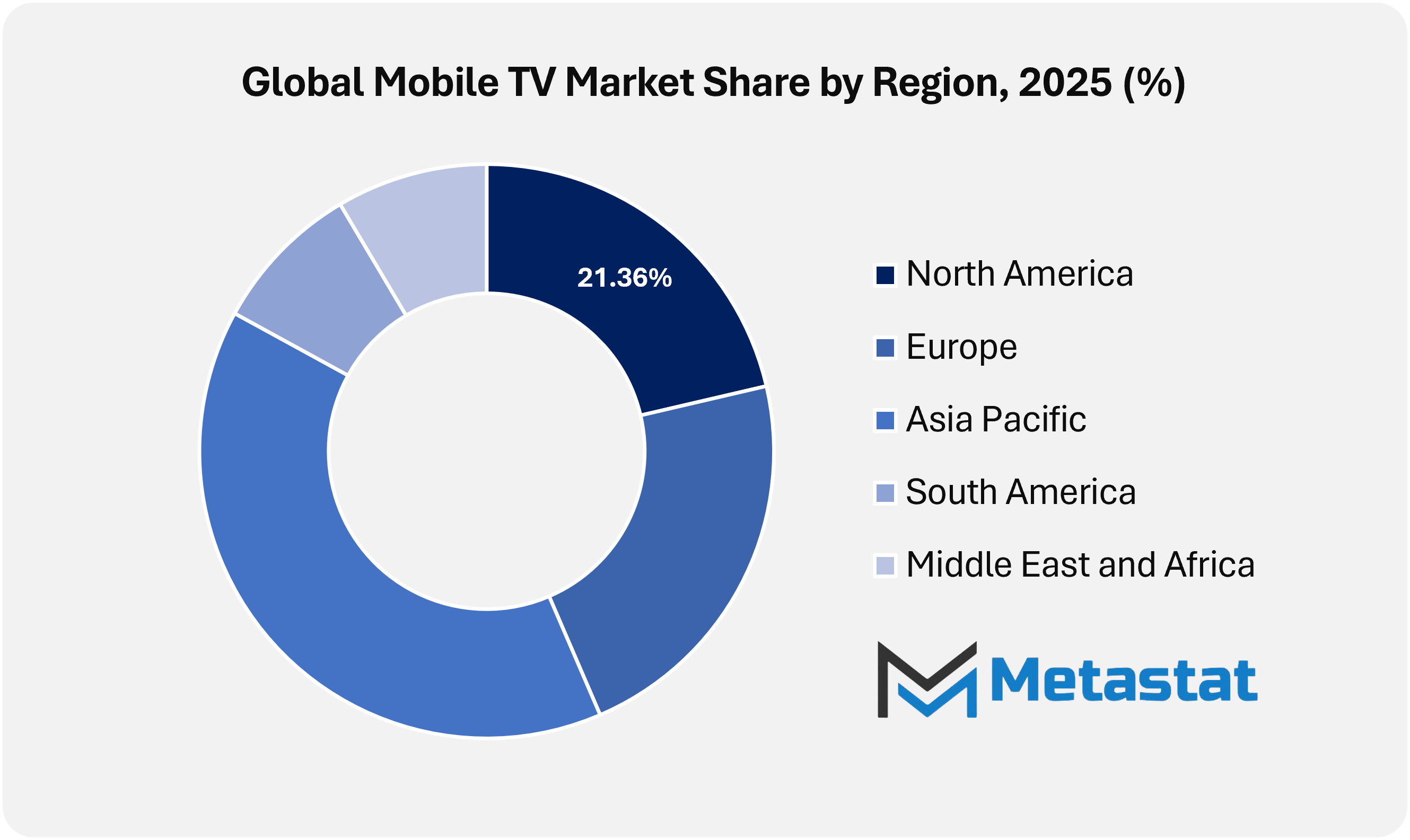

North America held 21.4% of the global Mobile TV market in 2025, with the United States accounting for the largest regional share.

The Video-on-Demand segment accounted for a 39.5% market share in 2025.

Key trends driving growth include rising consumption of video-on-the-go supported by high-speed 4G/5G expansion and affordable data plans, along with Increased integration of OTT apps, live sports streaming, and premium digital content partnerships across mobile platforms.

Opportunities include accelerated adoption of 5G multicast and edge-optimized streaming, enabling richer Mobile TV experiences across global markets.

Key insight: The Global Mobile TV market is gaining momentum owing to rising handheld media consumption, network upgrades, device convergence, and evolving content delivery economics.

The Global Mobile TV market within the media and telecommunications industry is expected to expand far beyond linear content delivery and scheduled broadcasting models. It will play an increasingly significant role as a behavioral interface rather than merely serving as a viewing channel, where screen-based consumption will merge with real-time choice structures, contextual intelligence, and area-conscious content material orchestration. Mobile TV systems will no longer be the most effective way to distribute programming but will feature as adaptive layers embedded inside smartphones, wearables, connected vehicles, and public display infrastructure.

Over the coming years, content architecture will shift toward session-based viewing as opposed to software-based viewing, in which narrative codecs will be modular, responsive, and interruptible by design. The Global Mobile TV market will support formats built for short attention spans, allowing broadcasters and content owners to deliver content that adjusts in duration, resolution, and interactivity based on individual motion, community situations, and ambient context. Rights management systems will also evolve, with dynamic licensing models aligning playback permissions with geography, time sensitivity, and concurrent user density.

Market Dynamics

Growth Drivers:

Rising consumption of video-on-the-go supported by high-speed 4G/5G expansion and affordable data plans.

Rising consumption of video-on-the-go supported by high-speed 4G/5G expansion and affordable data plans will continue shaping target market behavior. Wider smartphone penetration and improved network coverage encourage continuous viewing during travel and work hours. The Global Mobile TV market gains momentum via constant connectivity improvements and competitive pricing models.

Increased integration of OTT apps, live sports streaming, and premium digital content partnerships across mobile platforms

Increased integration of OTT apps, live sports streaming, and premium digital content partnerships across mobile platforms will redefine content access patterns. Exclusive publicizes and interactive capabilities entice numerous viewer segments. Mobile ecosystems increasingly position TV-style experiences within handheld devices, encouraging longer engagement cycles and strengthening monetization capacity across digital entertainment networks.

Restraints and Challenges:

Limited bandwidth capacity and network congestion reducing viewing quality during peak periods

Limited bandwidth capacity and network congestion reducing viewing quality during peak periods will continue to be a structural situation. Urban density and simultaneous data demand places pressure on network infrastructure performance. Viewing interruptions weaken person's pride, influencing retention costs. Network optimization investments remain essential to balance traffic loads and keep proper streaming consistency.

Higher content licensing and platform development costs restricting profitability for service providers

Higher content licensing and platform development costs restricting profitability for service providers will challenge financial sustainability. Premium rights acquisition and continuous technology improvements increase operational expenditure. Smaller market participants face entry barriers, even as established gamers come across margin strain, developing a competitive environment requiring careful value control and long-time period strategic planning.

Opportunities:

Accelerated adoption of 5G multicast and edge-optimized streaming enabling richer mobile TV experiences across global markets

Accelerated adoption of 5G multicast and edge-optimized streaming, enabling richer mobile TV reviews across worldwide markets, will unlock new growth avenues. Reduced latency and green spectrum usage aid massive-scale live viewing. The Global Mobile TV market stands poised for immersive formats, real-time interaction, and scalable distribution formats pushed with the aid of next-generation infrastructure.

Market Segmentation Analysis

The Global Mobile TV market is segmented by Content Type, Technology, Distribution Channel, Application, and Region.

By Content Type, the market is further segmented into:

Video-on-Demand

Video-on-Demand segment is estimated at USD 6.8 billion in 2026 and is projected to reach USD 13.8 billion by 2033, at a CAGR of 10.7% during the forecast period.

The Video-on-Demand segment in the Global Mobile TV market will expand through flexible viewing models driven by time-shifted consumption habits. Audiences will favor content libraries offering lengthy-form amusement, local programming, and adaptive pricing. Platform investment will focus on advice structures, compression efficiency, and bandwidth optimization to beautify uninterrupted cellular viewing experiences.

Online Video

Online Video segment is estimated at USD 5.9 billion in 2026 and is projected to reach USD 9.8 billion by 2033, at a CAGR of 7.6% during the forecast period.

Online video services will be shaped by short-form formats optimized for handheld screens. Growth will align with social media integration, author-pushed ecosystems, and fast content refresh cycles. Monetization techniques will expand through hybrid advertising models and branded collaborations, positioning online video as a dynamic engagement channel within cellular television services.

Live Streaming

Live Streaming segment is estimated at USD 4.6 billion in 2026 and is projected to reach USD 10.3 billion by 2033, at a CAGR of 12.3% during the forecast period.

Live streaming will strengthen real-time audience participation throughout sports activities, news, and interactive occasions. Technological advancements will guide reduced latency and higher mobile balance. Content proprietors will emphasize one-of-a-kind live access and target audience analytics, allowing stay broadcasting to remain a central engagement driving force in cellular-centric leisure shipping models.

By Technology, the market is divided into:

IPTV

IPTV segment is projected to reach USD 7 billion by 2033, at a CAGR of 8.5% during the forecast period.

IPTV technology will retain relevance through controlled networks, delivering consistent quality and managed distribution. Telecom operators will expand bundled services, integrating Mobile TV access. Future deployments will prioritize network reliability and service personalization, enabling IPTV frameworks to conform smoothly to mobile utilization patterns without compromising streaming performance.

OTT

OTT segment is projected to reach USD 22.1 billion by 2033, at a CAGR of 12.1% during the forecast period.

OTT platforms will continue reshaping Mobile TV consumption through software-based delivery independent of traditional infrastructure. Service growth will rely upon scalable cloud architectures and content localization. Competitive differentiation will emerge via user interface simplicity, adaptive streaming protocols, and strategic partnerships, assisting seamless mobile access.

Satellite

Satellite segment is projected to reach USD 2.2 billion by 2033, at a CAGR of 2.1% during the forecast period.

Satellite-based Mobile TV services will serve connectivity-confined regions by means of allowing wide-area coverage. Technological refinement will improve signal efficiency and tool compatibility. Strategic use cases will encompass far-flung broadcasting and emergency communication, assisting broader inclusion within mobile television ecosystems beyond dense city markets.

Others

Others segment is projected to reach USD 2.6 billion by 2033, at a CAGR of 8.9% during the forecast period.

Emerging technology will supplement installed delivery methods through experimental transmission fashions and hybrid frameworks. Innovation will raise awareness on price reduction, energy performance, and tool integration. Such developments will support diversified access routes while helping future adaptability across evolving cell enjoyment infrastructures.

By Distribution Channel, the market is segmented into:

Free to Air Service

Free to Air Service segment is projected to reach USD 15.1 billion by 2033.

Free-to-air services will expand audience reach through ad-supported content delivery models. Accessibility without subscription obstacles will entice mass viewership segments. Broadcasters will invest in cell-optimized scheduling and localized programming, allowing sustainable revenue generation through advertising without restricting consumer access.

Pay TV Service

Pay TV Service segment is projected to reach USD 18.8 billion by 2033.

Pay TV services will emphasize premium experiences through exclusive programming and enhanced viewing features. Subscription-based access will aid funding in high-priced content material and advanced capabilities. Personalization equipment and bundled offerings will support purchaser retention in aggressive cellular tv environments.

By Applications, the Global Mobile TV market is divided as:

Commercial

Commercial segment is projected to grow at a CAGR of 7.8% during the forecast period.

Commercial applications will leverage mobile television systems for targeted advertising and brand storytelling. Businesses will adopt interactive codecs, assisting real-time engagement and measurable consequences. Integration with data analytics will refine marketing campaign precision, positioning cellular tv as a strategic channel for virtual marketing evolution.

Personal

Personal segment is projected to grow at a CAGR of 11% during the forecast period.

Personal applications will prioritize individualized entertainment consumption tailored to user preferences and daily routines. Mobile tv usage will align with life-style mobility and on-demand get right of entry to expectations. Continuous interface enhancements and adaptive content material delivery will enhance pride across numerous customer demographics.

By Region:

Based on geography, the Global Mobile TV market is divided into North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

North America Mobile TV Market is set to expand at a CAGR of 10.1% within the forecast period, reaching a market size (TAM) of USD 6.2 billion by the end of 2033.

North America is witnessing rising Mobile TV adoption owing to high 5G penetration and strong demand for live sports streaming on handheld devices.

In North America, Mobile TV market growth gains momentum from premium content partnerships among broadcasters, telecom operators, and OTT platforms.

Asia-Pacific presents significant opportunities for the Global Mobile TV market through increasing cell phone user bases and inexpensive data plans across emerging economies.

Within the Asia Pacific, the Global Mobile TV panorama benefits from growing interest in regional language content and mobile-first entertainment consumption.

Across the Middle East, Africa, and South America, the Global Mobile TV market progresses through slow digital infrastructure enlargement, rising mobile internet access, and growing desire for on-the-go video consumption in urban populations.

Competitive Landscape and Strategic Insights

The Global Mobile TV marketplace continues to gain steady attention as viewing habits shift closer to monitors that suit into regular existence. Audiences now count on live tv, on-demand content, and interactive formats to work smoothly on smartphones and tablets. This exchange in conduct has encouraged telecom operators, broadcasters, and virtual structures to rethink how video is introduced. Network power, data affordability, and tool compatibility will shape how cell TV grows throughout regions, particularly in areas where cellular internet is the primary means of access for enjoyment.

In North America, agencies that include AT&T Inc., Verizon Communications Inc., Comcast Corporation, Charter Communications, Inc., Cox Communications, Inc., United States Cellular Corporation, Consolidated Communications Holdings, Inc., Altice USA, Inc., Rogers Communications Inc., and TELUS Corporation play a major role in integrating mobile TV with current broadband and wi-fi services. These competitors focus on improving the streaming experience and bundling content with data plans to hold customers engaged. Their strategies frequently join conventional television fashions with app-based viewing, growing flexible options for customers who decide to watch content on the move.

Across Europe, companies such as Vodafone Group Plc, Telefónica S.A., Deutsche Telekom AG, Orange S.A., Swisscom AG, KPN N.V., Telia Company AB, Telecom Italia S.P.A. (TIM), Proximus Group, Telenet Group Holding N.V., Iliad S.A., Altice France S.A. (SFR), Virgin Media O2 UK Limited, and Sky Group Limited retain to reinforce mobile TV through partnerships and localized content material. These companies focus on regional preferences, language diversity, and flexible subscription models. Their presence helps strike a balance between live broadcasting and streaming offerings tailored for mobile-first users.

In Asia-Pacific and different rapidly growing markets, operators along with Bharti Airtel Limited, Tata Play Limited, Asianet Satellite Communications Ltd., Singapore Telecommunications Limited (Singtel), StarHub Ltd., Rakuten Group, Inc., Tencent Holdings Ltd., and MultiChoice Group Limited display how mobile TV adapts to large user volumes and varied price sensitivities. These companies frequently integrate telecom offerings with sturdy virtual structures, making mobile TV more available to wider audiences. Innovation in information utilization and app-based viewing will continue to be vital to growth in those regions.

Forecast and Future Outlook

Market size is forecast to rise from USD 15.7 billion in 2025 to over USD 33.9 billion by 2033.

The Global Mobile TV market is expected to increasingly integrate with creator-led distribution ecosystems, where independent producers will launch serialized live content without traditional network backing. Regulatory frameworks will adapt to these hybrid models, balancing spectrum usage, content accountability, and user privacy, while redefining what mobile broadcasting will represent in a screen-saturated digital society.

This research report categorizes the Mobile TV market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Mobile TV market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Mobile TV market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 10.1% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Content Type, Technology, Distribution Channel, Applications, and Region

By Region

North America (By Content Type, Technology, Distribution Channel, Applications, and Country)

United States

Canada

Mexico

Europe (By Content Type, Technology, Distribution Channel, Applications, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Content Type, Technology, Distribution Channel, Applications, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Content Type, Technology, Distribution Channel, Applications, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Content Type, Technology, Distribution Channel, Applications, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share and Revenue

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

Import-Export Trade Statistics

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Top players operating in the Mobile TV industry include AT&T Inc., Charter Communications, Inc., Comcast Corporation, Consolidated Communications Holdings, Inc., Cox Communications, Inc., United States Cellular Corporation, and Verizon Communications Inc.

Global Mobile TV market is estimated to reach USD 33.9 billion by 2033.

Limited bandwidth capacity and network congestion reducing viewing quality during peak periods will hamper market growth within the forecast period.

North America region dominates the market.

The Metastat Insights study shows that the Global Mobile TV market size was USD 15.7 billion in 2025.

The Global Mobile TV market is likely to grow at a CAGR of 10.1% over the forecast period (2026-2033).

The Metastat Insights analysis shows that the North America Mobile TV market size is estimated to be USD 6.2 billion by 2033.

The Online Video is the leading type segment in the Global market.

Rising consumption of video-on-the-go supported by high-speed 4G/5G expansion and affordable data plans and Increased integration of OTT apps, live sports streaming, and premium digital content partnerships across mobile platforms are key driving factors, boosting the market.

Cognitive Radio market size is valued at USD 9,332.8 million in 2025 and projected to reach USD 31,030.5 million by 2033, growing at a CAGR of 16.2%.

Cognitive Radio market, Cognitive Radio Market Size, Cognitive Radio Market Share, Cognitive Radio Market Analysis, Cognitive Radio Market Growth, Cognitive Radio Market Trends, Cognitive Radio Market Research Report, Cognitive Radio Market Forecast, Cognitive Radio, Cognitive Radio Market Research, Cognitive Radio Industry, Cognitive Radio Industry Report, Cognitive Radio Market Data, Cognitive Radio Statistics, Cognitive Radio Market Statistics, Cognitive Radio Industry Trends, Cognitive Radio Market Report, Cognitive Radio Market Trends, Cognitive Radio Market News, Cognitive Radio Forecasts, Cognitive Radio Market Intelligence Report, Cognitive Radio market 2033, Cognitive Radio market outlook, Cognitive Radio market segmentation, Cognitive Radio market drivers, Cognitive Radio market restraints, Cognitive Radio market opportunities, Cognitive Radio market CAGR, Cognitive Radio suppliers, Cognitive Radio manufacturers, Cognitive Radio market by region, North America Cognitive Radio market, Asia Pacific Cognitive Radio market, Europe Cognitive Radio market, Cognitive Radio market competitive landscape, Cognitive Radio market key players, Cognitive Radio hardware market, Cognitive Radio software market, Cognitive Radio services market, Cognitive Radio government & defense market, Cognitive Radio telecommunications market, Cognitive Radio transportation market

Data-as-a-Service (DaaS) market size was valued at USD 23.2 billion in 2025 and projected to reach USD 151.4 billion by 2033, growing at a CAGR of 26.4%.

Data-as-a-Service (DaaS) market, Data-as-a-Service (DaaS) Market Size, Data-as-a-Service (DaaS) Market Share, Data-as-a-Service (DaaS) Market Analysis, Data-as-a-Service (DaaS) Market Growth, Data-as-a-Service (DaaS) Market Trends, Data-as-a-Service (DaaS) Market Research Report, Data-as-a-Service (DaaS) Market Forecast, Data-as-a-Service (DaaS), Data-as-a-Service (DaaS) Market Research, Data-as-a-Service (DaaS) Industry, Data-as-a-Service (DaaS) Industry Report, Data-as-a-Service (DaaS) Market Data, Data-as-a-Service (DaaS) Statistics, Data-as-a-Service (DaaS) Market Statistics, Data-as-a-Service (DaaS) Industry Trends, Data-as-a-Service (DaaS) Market Report, Data-as-a-Service (DaaS) Market Trends, Data-as-a-Service (DaaS) Market News, Data-as-a-Service (DaaS) Forecasts, Data-as-a-Service (DaaS) Market Intelligence Report, Data-as-a-Service (DaaS) market 2033, Data-as-a-Service (DaaS) market outlook, Data-as-a-Service (DaaS) market segmentation, Data-as-a-Service (DaaS) market drivers, Data-as-a-Service (DaaS) market restraints, Data-as-a-Service (DaaS) market opportunities, Data-as-a-Service (DaaS) market CAGR, Data-as-a-Service (DaaS) suppliers, Data-as-a-Service (DaaS) manufacturers, Data-as-a-Service (DaaS) market by region, North America Data-as-a-Service (DaaS) market, Asia Pacific Data-as-a-Service (DaaS) market, Europe Data-as-a-Service (DaaS) market, Data-as-a-Service (DaaS) market competitive landscape, Data-as-a-Service (DaaS) market key players, Business and Company Data DaaS, Consumer and Demographic Data DaaS, Sales and Marketing Intelligence DaaS, Risk, Fraud and Compliance Intelligence DaaS, APIs and Real-Time Data Feeds DaaS, Cloud Data Marketplaces and Native Data Shares DaaS, BFSI DaaS, IT and Telecommunications DaaS.

Operational Technology (OT) and Industrial Cybersecurity Mar

Operational Technology (OT) and Industrial Cybersecurity market size is valued at USD 25.8 billion in 2025 and projected to reach USD 82.7 billion by 2033.

Operational Technology (OT) and Industrial Cybersecurity market, Operational Technology (OT) and Industrial Cybersecurity Market Size, Operational Technology (OT) and Industrial Cybersecurity Market Share, Operational Technology (OT) and Industrial Cybersecurity Market Analysis, Operational Technology (OT) and Industrial Cybersecurity Market Growth, Operational Technology (OT) and Industrial Cybersecurity Market Trends, Operational Technology (OT) and Industrial Cybersecurity Market Research Report, Operational Technology (OT) and Industrial Cybersecurity Market Forecast, Operational Technology (OT) and Industrial Cybersecurity, Operational Technology (OT) and Industrial Cybersecurity Market Research, Operational Technology (OT) and Industrial Cybersecurity Industry, Operational Technology (OT) and Industrial Cybersecurity Industry Report, Operational Technology (OT) and Industrial Cybersecurity Market Data, Operational Technology (OT) and Industrial Cybersecurity Statistics, Operational Technology (OT) and Industrial Cybersecurity Market Statistics, Operational Technology (OT) and Industrial Cybersecurity Industry Trends, Operational Technology (OT) and Industrial Cybersecurity Market Report, Operational Technology (OT) and Industrial Cybersecurity Market Trends, Operational Technology (OT) and Industrial Cybersecurity Market News, Operational Technology (OT) and Industrial Cybersecurity Forecasts, Operational Technology (OT) and Industrial Cybersecurity Market Intelligence Report, Operational Technology (OT) and Industrial Cybersecurity market 2033, Operational Technology (OT) and Industrial Cybersecurity market outlook, Operational Technology (OT) and Industrial Cybersecurity market segmentation, Operational Technology (OT) and Industrial Cybersecurity market drivers, Operational Technology (OT) and Industrial Cybersecurity market restraints, Operational Technology (OT) and Industrial Cybersecurity market opportunities, Operational Technology (OT) and Industrial Cybersecurity market CAGR, Operational Technology (OT) and Industrial Cybersecurity suppliers, Operational Technology (OT) and Industrial Cybersecurity manufacturers, Operational Technology (OT) and Industrial Cybersecurity market by region, North America Operational Technology (OT) and Industrial Cybersecurity market, Asia Pacific Operational Technology (OT) and Industrial Cybersecurity market, Europe Operational Technology (OT) and Industrial Cybersecurity market, Operational Technology (OT) and Industrial Cybersecurity market competitive landscape, Operational Technology (OT) and Industrial Cybersecurity market key players, OT Security Platforms and Software market, Network Security Appliances and Industrial Gateways market, Professional and Advisory Services in OT Cybersecurity, Managed OT Security Services market, Asset Discovery, Inventory and Exposure Assessment market, Network Monitoring, Threat Detection and Incident Response market, Vulnerability, Risk and Compliance Management market, Supervisory Control and Data Acquisition Systems market, Distributed Control Systems market, Programmable Logic Controllers and Safety Systems market, Industrial IoT and Edge Devices market, Manufacturing OT and Industrial Cybersecurity market, Energy and Utilities OT and Industrial Cybersecurity market.

New Zealand Optical Encryption Market Size, Share, Trends, 2033

New Zealand Optical Encryption market size is valued at USD 34.5 million in 2025 and is projected to reach USD 76.9 million in 2033, at a CAGR of 10.3% from 2026 to 2033.

New Zealand Optical Encryption Market, New Zealand Optical Encryption Market Size, New Zealand Optical Encryption Market Share, New Zealand Optical Encryption Market Analysis, New Zealand Optical Encryption Market Growth, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market Research Report, New Zealand Optical Encryption Market Forecast, New Zealand Optical Encryption, New Zealand Optical Encryption Market Research, New Zealand Optical Encryption Industry, New Zealand Optical Encryption Industry Report, New Zealand Optical Encryption Market Data, New Zealand Optical Encryption Statistics, New Zealand Optical Encryption Market Statistics, New Zealand Optical Encryption Industry Trends, New Zealand Optical Encryption Market Report, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market News, New Zealand Optical Encryption Forecasts, New Zealand Optical Encryption Market Intelligence Report